CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-47 (Continued)

Before-the-fact flexible budgeting allows managers to assess risk and uncertainty.

3. The financial performance as revealed in Requirements 1 and 2 is not very

promising. Two out of three scenarios lose money. Only the optimistic scenario

promises a positive return, and it is only about 3% of sales. Most steering

committees would be reluctant to press ahead with the new product given

these projected financial results. There are a number of possibilities. One

possibility is to instruct engineering to produce a design that reduces the cost—

especially the acquisition cost. It may be possible to produce a design that lowers

the manufacturing cost of the outsourced producers and Stillwater Designs’

acquisition cost. By reducing the weight and bulkiness of the product, freight costs

may also be reduced. After all the cost improvements are obtained that can be, then

the question becomes—if the return is questionable—would the company still

want to produce the product?

Producing a product that will not stand by itself is sometimes desirable. The

11-20

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-48

1. 1,700 Direct labor hours:

Maintenance [$7,500 + ($5 × 1,700)]……………………………

…

$16,000

2. For costs that don’t change, the formula is simply the fixed component.

To prepare the formulas for the costs that change, use the high-low method:

Maintenance:

Supplies:

V = ($4,600 – $2,300)/(2,000 – 1,000) = $2.30

F = $4,600 – $2.30(2,000) = $0

Supplies Cost = $2.30X

11-21

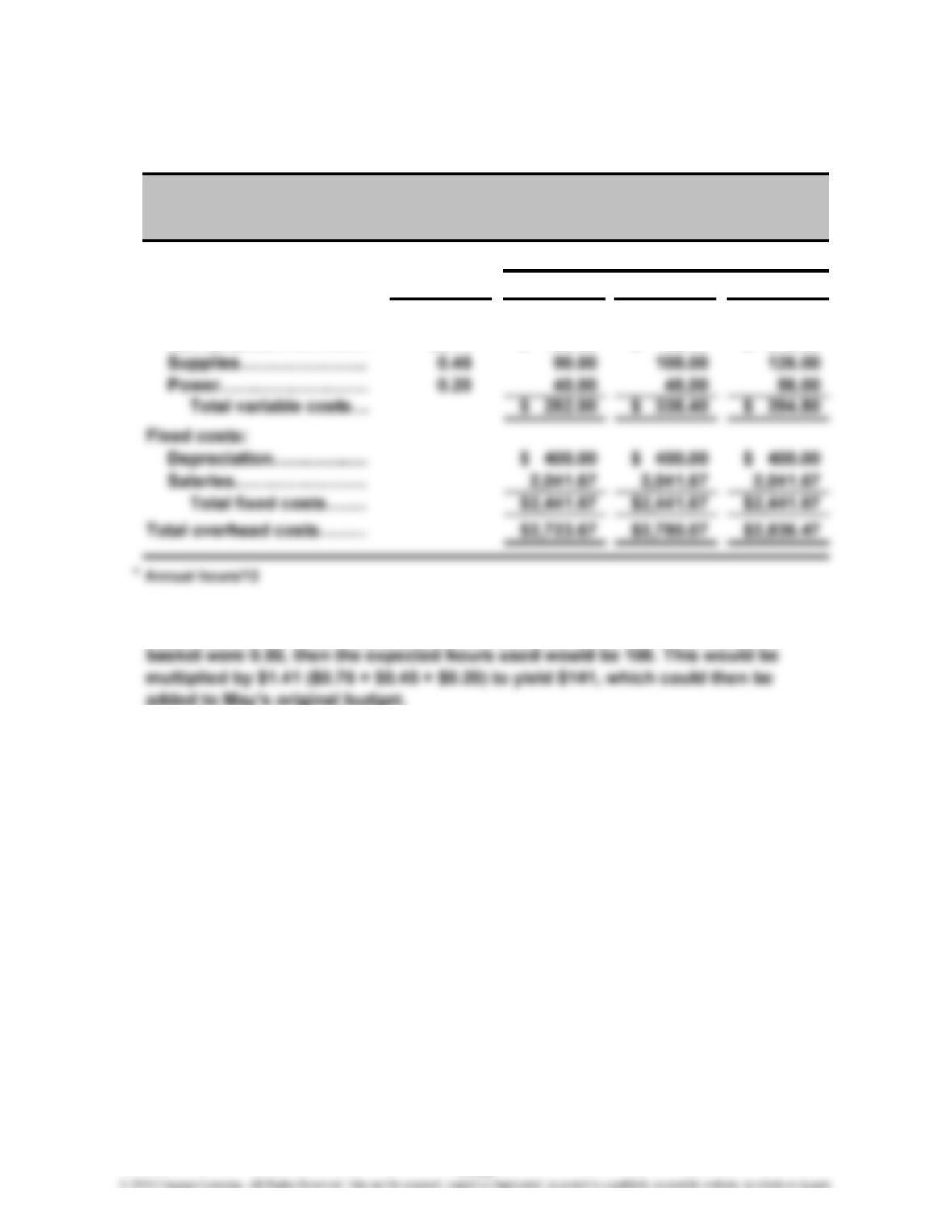

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-49

1.

Formula 200 240 280

Variable costs:

Maintenance……………

…

$0.76 $ 152.00 $ 182.40 $ 212.80

2. The additional baskets will require additional direct labor hours and will increase

the budgeted variable overhead for May. For example, if the hours used per

Activity Level (hours)*

Orchard Fresh Inc.

Overhead Budget

For the Month of May

11-22

…

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-50

1. Flexible budget for a normal school month:

Revenue:

Sandwiches (5,000 × $4.50)…………………………………………… $22,500

Sodas (5,000 × $1.50)…………………………………………………

…

7,500

Total revenue………………………………………………………………

…

$30,000

Variable food costs:

Direct laborc ($1,720 + $1,032)…………………………………………

…

2,752

Total costs…………………………………………………………………

…

$22,127

aCost per Sandwich:

* Rounded

bCost per 12 oz. Drink

= 12/128 × $2.56

= $0.24

11-23

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-50 (Continued)

2. Flexible budget for October:

Revenue:

Sandwiches (6,500 × $4.50)……………………………………………

…

$29,250

Sodas (6,500 × $1.50)……………………………………………………

…

9,750

Total revenue…………………………………………………………………

…

$39,000

aCost per sandwich:

Meat: (4/16 × $7)………………………………………………………

…

$1.75

Cheese: (2/16 × $6)…………………………………………………… 0.75

Roll: ($28.80/144)……………………………………………………… 0.20

*Rounded

bCost per 12 oz. Drink

= 12/128 × $2.56

= $0.24

3.

Y

es, the increase in revenue was $9,000 ($30,000 – $39,000) but, cost increased b

y

only $5,460 ($27,587 – $22,127). Thus, profit increases by $3,540.

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-51

1.

A

ctual Costs

Direct labor……………

…

$210,000 $200,000 $ 10,000 U

2.

A

ctual Costs

Direct labor……………

…

$210,000 $200,000 $10,000 U

3. The multiple cost driver approach captures the cause-and-effect cost

relationships and, consequently, is more accurate than the direct labor-based

approach.

Budget Variance

Budgeted Costs Budget Variance

Budgeted Costs

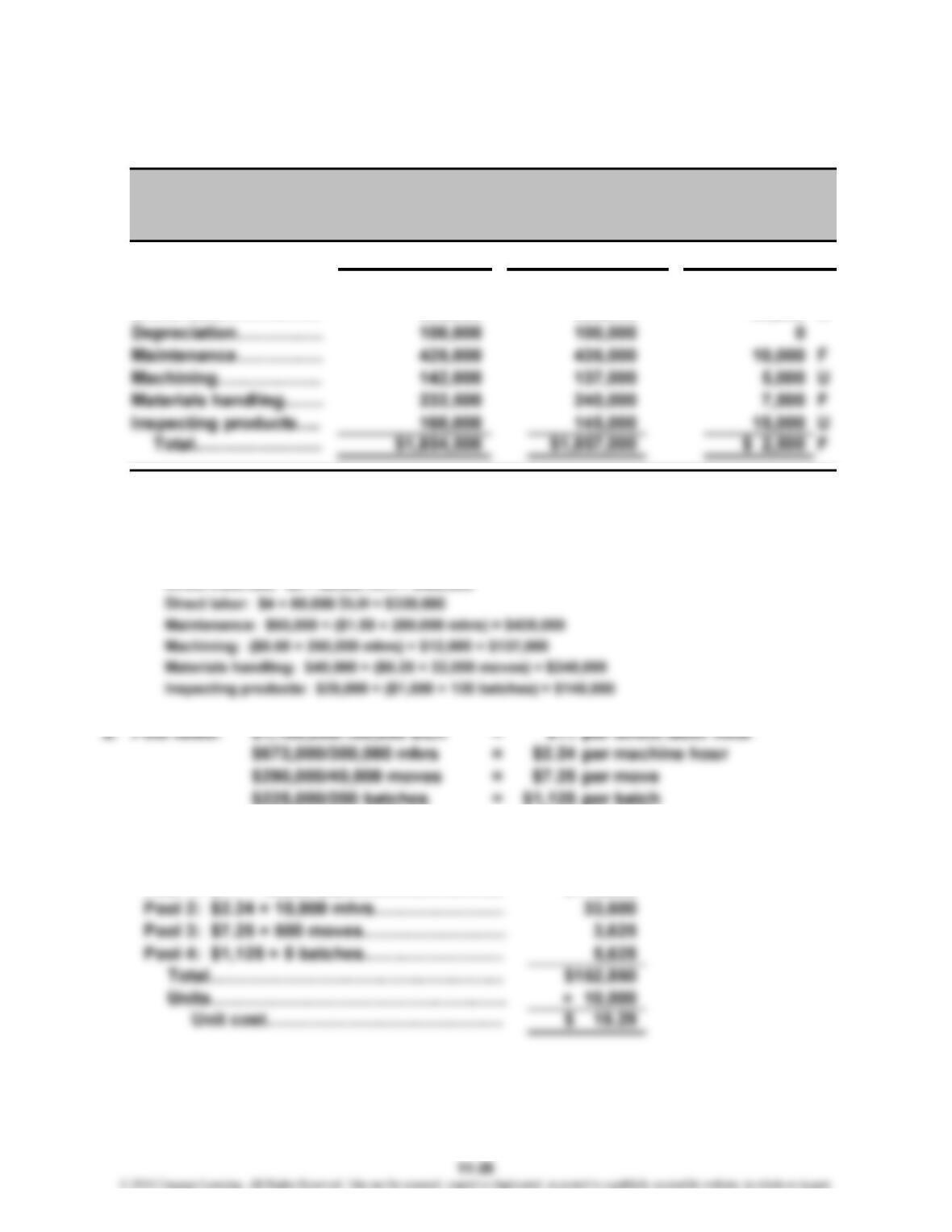

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-52

1.

Actual Costs

Direct materials………

…

$ 440,000 $40,000 F

Direct labor……………

…

355,000 35,000 U

*Budget formulas for each item can be computed by using the high-low method (using the

appropriate cost driver for each method). Using this approach, the budgeted costs for the actual

activity levels are computed as follows:

Budget formulas using high low method:

Direct materials: $6 × 80,000 DLH = $480,000

= per batch

Note: The first pool has material and labor costs, as well as depreciation, included.

Unit cost:

Pool 1: $11 × 10,000 DLH……………………

…

$225,000/200 batches

$1,125

$110,000

Westcott Inc.

Performance Report

For the Year 2014

Budget VarianceBudgeted Costs*

$ 480,000

320,000

…

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-52 (Continued)

3. Knowing the resources consumed by activities and how the resource costs

change with the activity driver should provide more insight into managing the

Materials handling:

Forklifts………………………………………

…

$ 40,000 $ 40,000

20,000 moves 40,000 moves

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-53

1.

Direct Labor = $10 × Direct Labor Hours

Utilities = $3,000 + ($0.15 × Direct Labor Hours)

$0.15 per direct

labor hour

Fixed Cost = $21,000 – ($0.15)(120,000) = $3,000

Depreciation =

Supplies = $0.25 × Direct Labor Hours

$2.20 per direct

labor hour

Fixed Cost = $284,000 – ($2.20)(120,000) = $20,000

120,000 hours – 100,000 hours

$225,000

$21,000 – $18,000

High Cost – Low Cost

High Activity – Low Activity

120,000 hours – 100,000 hours

$284,000 – $240,000

=

=

Variable Rate

=

=

=

Variable Rate

Variable Rate

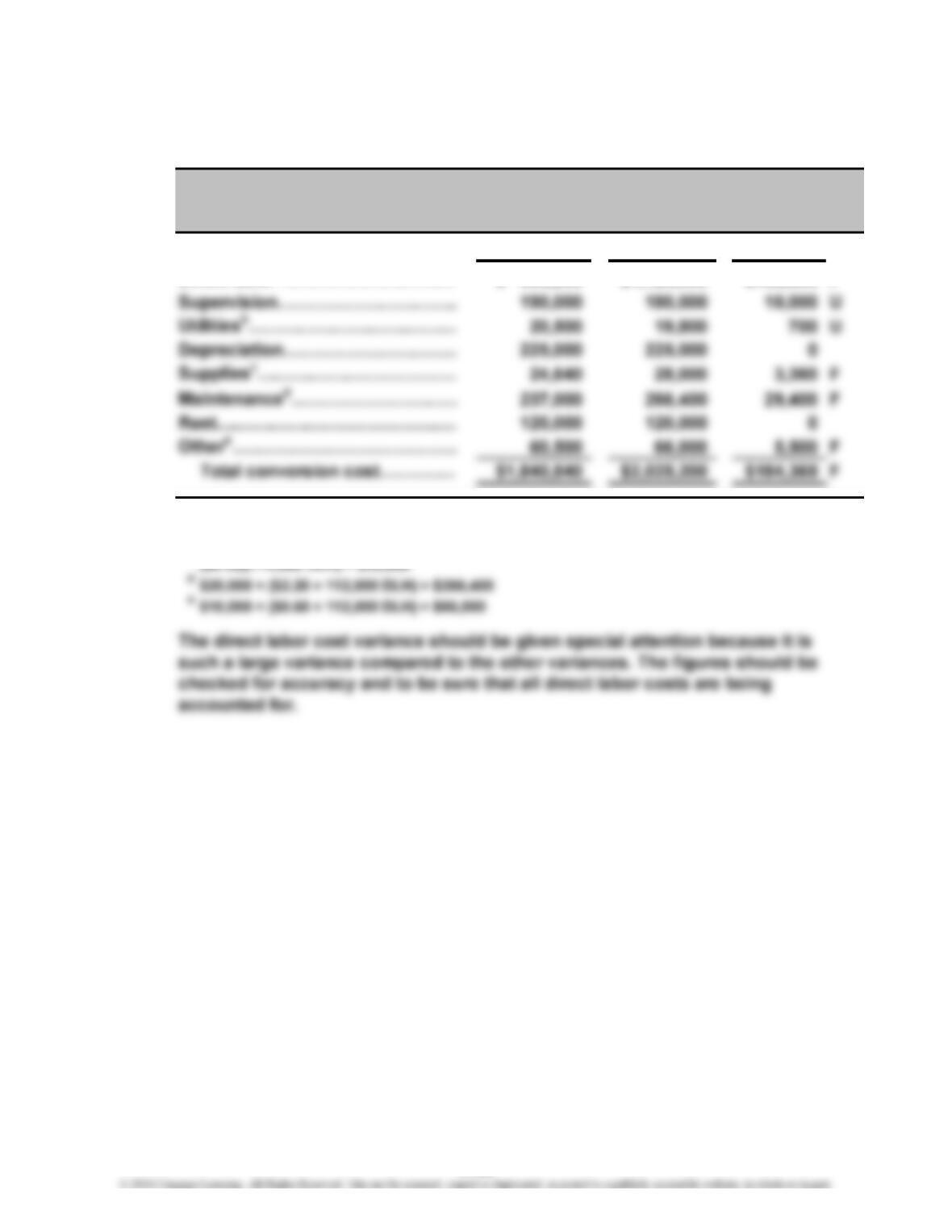

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-53 (Continued)

2.

Conversion Cost

A

ctual Budget

V

ariance

Direct labo

r

a

…………………………

…

$ 963,200 $1,120,000 $156,800 F

a($10)(112,000 DLH) = $1,120,000

b$3,000 + ($0.15 × 112,000 DLH) = $19,800

c($0.25)(112,000 DLH) = $28,000

d

Thorpe Inc.

Conversion Cost Report

For Last Yea

r

11-29

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-54

1. Standard Fixed Overhead Rate = $2,160,000/(120,000 units × 5 DLH)

= $3.60 per DLH

Standard Variable Overhead Rate = $1,440,000/(120,000 units × 5 units)

= $2.40 per DLH

3. Fixed overhead analysis:

expected level.

4.

V

ariable overhead analysis:

Budgeted FOH

Actual VOH

$2.40 × 592,300 hours

A

pplied FOH

Budgeted VOH

A

pplied VOH

Actual FOH

V

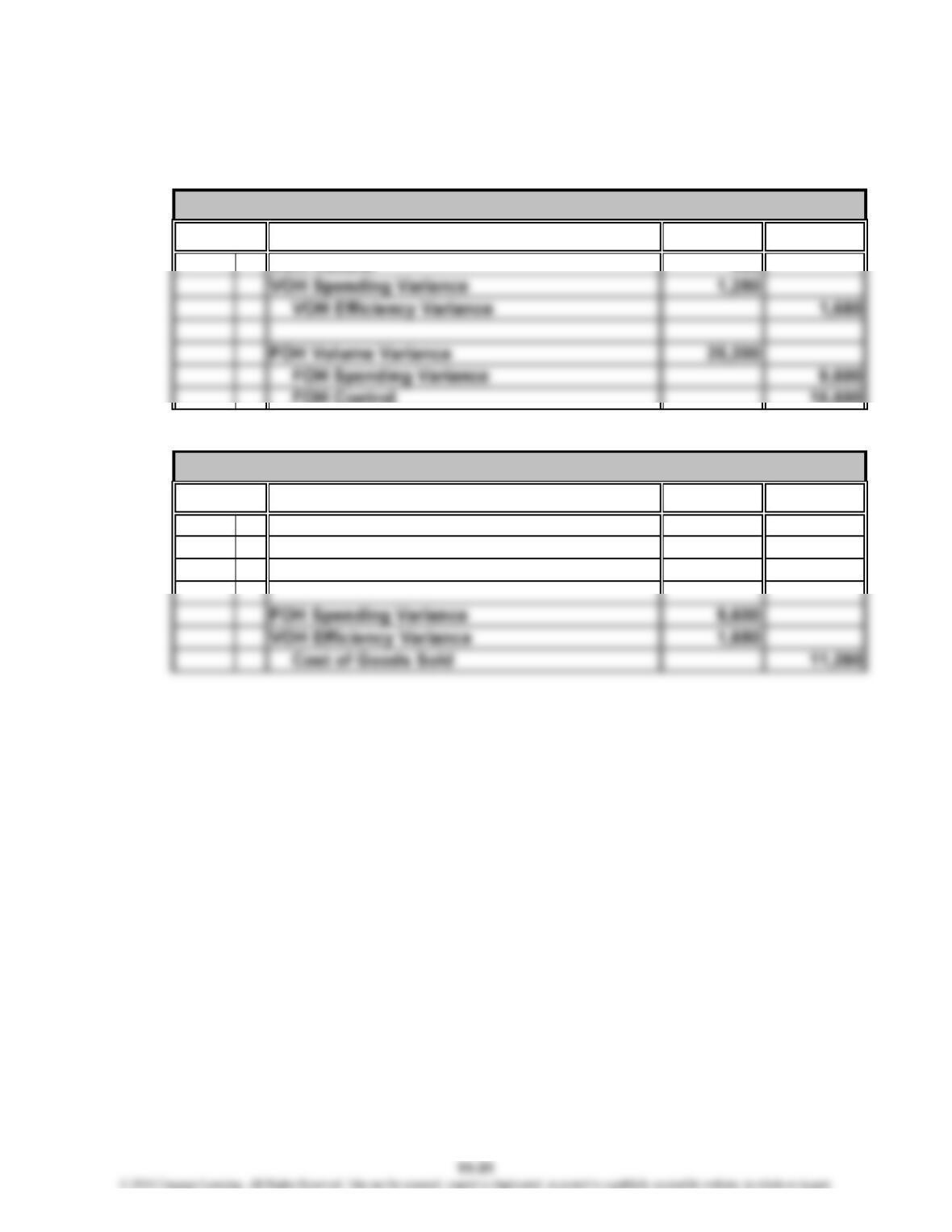

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-54 (Continued)

5. Overhead variance isolation:

Debit Credit

VOH Control 400

FOH Control 15,600

Closing to Cost of Goods Sold:

Debit Credit

Cost of Goods Sold 26,480

VOH Spending Variance 1,280

FOH Volume Variance 25,200

Date Account & Explanation

Journal

Date Account & Explanation

Journal

P 11-55

1.

V

ariable overhead variances:

V

V

2. Fixed overhead variances:

V

Efficiency

$20,000 U$40,000 U

Spending

Actual VOH

$820,000

Actual VOH Budgeted VOH

$10 × 80,000 hrs.

A

pplied VOH

$800,000

$10 × 82,000 hrs.

$860,000

$6 × 1.60 hrs. ×

$6 × 1.60 hrs. ×

Budgeted VOH

60,000 units

50,000 units

Applied VOH

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-56

1. Standard Fixed Overhead Rate = $1,286,400/(120,000 units × 4 DLH)

2. Fixed: 119,000 × 4 × $2.68 =

Variable: 119,000 × 4 × $1.85 =

3. Fixed overhead analysis:

4. Variable overhead analysis:

$1.85 × 487,900 hours

$24,395 U

$927,010 $902,615

$1,275,680

$880,600

Actual VOH Budgeted VOH

Actual FOH

$1,300,000 $1,275,680

Applied FOHBudgeted FOH

$1,286,400

$880,600

$1.85 × 476,000 hours

Applied VOH

$22,015 U

11-33

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-57

1. The budgeted overhead costs are broken down into fixed and variable costs by

the high-low method:

Standard VOH Rate =

2. Budgeted Fixed Overhead = Y2 – VX2

= $540,000 – $12(30,000)

3. To find the VOH spending variance, we need to find the actual hours. To find AH,

we first need to find the standard hours, SH:

Fixed OH Volume Variance = Budgeted Fixed Overhead –

(Fixed Overhead Rate × SH)

4. 26,667 hours/100,000 units = 0.26667 hour per unit

Change in Cost

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-58

1.

Actual

Costs Costs*

Direct materials…………………

…

$ 775,000 $ 750,000 $25,000 U

2. a. FOH variances:

Spending Variance = Actual FOH – Budgeted FOH

= $180,000 – $165,000

*Note: FOH rate is calculated as follows:

Hours Allowed = 60,000 hours/50,000 units

b.

V

OH variances:

V

ariable OH Rate = $300,000/60,000 hours

= $5.00 per hou

r

A

V

ariance

Budgeted

Shumaker Company

Performance Report

11-35

…

V

CHAPTER 11 Flexible Budget and Overhead Analysis

Case 11-59

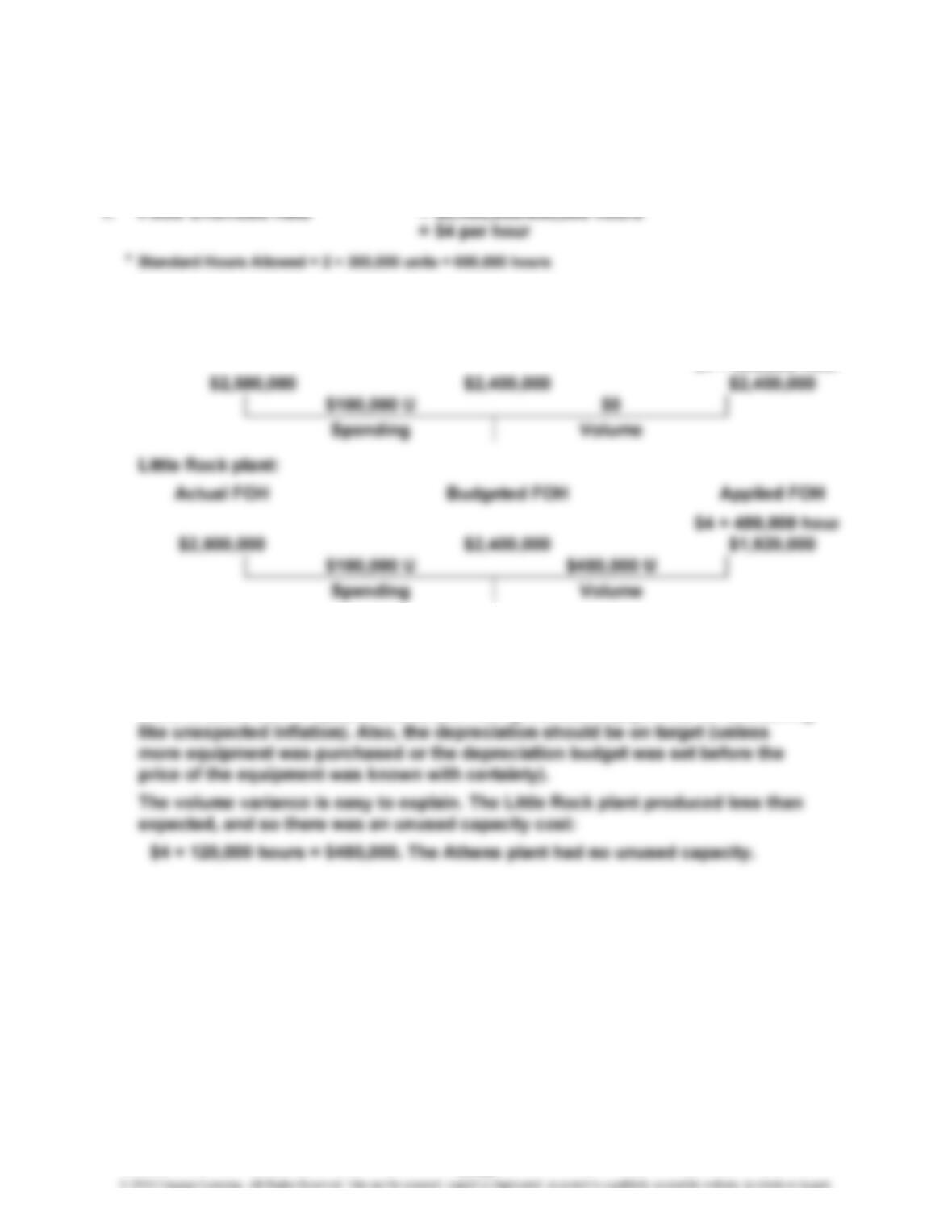

2. Athens plant:

r

The spending variance is almost certainly caused by supervisor salaries (for

example, an unexpected midyear increase due to union pressures). It is unlikely

that the lease payments or depreciation would be greater than budgeted.

Changing the terms on a 10-year lease in the first year would be unusual (unless

there is some sort of special clause permitting increased payments for something

Actual FOH Budgeted FOH

Applied FOH

CASES

$4 × 600,000 hou

r

11-36

CHAPTER 11 Flexible Budget and Overhead Analysis

Case 11-59 (Continued)

3. It appears that the 120,000-hour unused capacity (60,000 subassemblies)

is permanent for the Little Rock plant. This plant has 10 supervisors, each

making $50,000. Supervision is a step-cost driven by the number of

production lines. Unused capacity of 120,000 hours means that 2 lines

can be shut down, saving the salaries of two supervisors ($100,000 at the

4. For each plant, the standard fixed overhead rate is $4 per direct labo

r

hour. Since each subassembly should use two hours, the fixed overhead

cost per unit is $8, regardless of where they are produced. Should they

differ? Some may argue that the rate for the Little Rock plant needs to be

recalculated. For example, one possibility is to use expected actual

capacity, instead of practical capacity. In this case, the Little Rock plant

would have a fixed overhead rate of $2,400,000/480,000 hours = $5 per

11-37

CHAPTER 11 Flexible Budget and Overhead Analysis

Case 11-60

1. If reducing negative environmental impacts is a legitimate firm-wide

objective or if legally mandated, then there is an ethical obligation to help

achieve the desired reduction. Furthermore, if it is possible to reduce

environmental impacts while simultaneously reducing costs, then this

2. Any financial officer should be concerned with cost reduction. If reducing

environmental waste or pollutants also produces a reduction in cost, then

it seems like there is an ethical obligation to undertake and support these

3. A variety of answers will emerge. There are always ethical dilemmas that

can surface when performance evaluations occur. For example, is it

ethical for a financial executive to deliberately and systematically overstate

the unit variable cost in a flexible budget? (The objective may be to force

11-38