CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-35 (Continued)

2. d. Both fixed cost and unit variable cost increase:

E 4-36

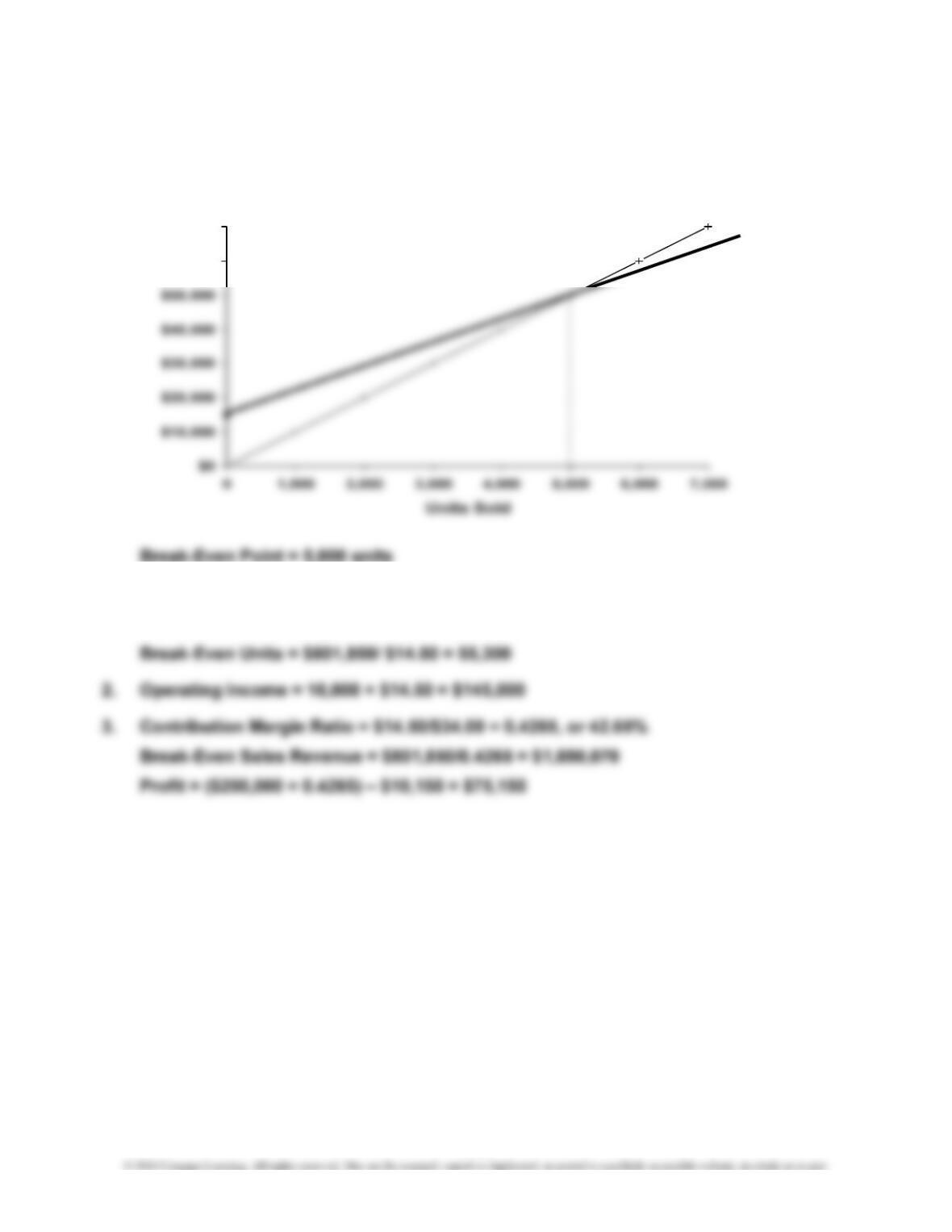

1. Unit Contribution Margin = $791,700/54,600 = $14.50

$60,000

$70,000

4-18

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-37

1. Break-Even Sales Dollars = $733,320/0.42* = $1,746,000

*Contribution Margin Ratio = $756,000/$1,800,000 = 0.42, or 42%

E 4-38

1. Sales Total

Product Price

–

=CM ×Mix=CM

Vases $40 $10 2 $20

2. The new sales mix is 3 vases to 2 figurines.

Sales Total

Product Price

–

=CM ×Mix=CM

Vases $40 $10 3 $30

$30

Variable

Variable

Cost

Cost

$30

4-19

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-39

1. a. Variable Cost per Unit = $8,190,000/450,000 = $18.20

b. Contribution Margin per Unit = $3,510,000/450,000 = $7.80

3. Additional Operating Income = $50,000 × 0.30 = $15,000

4. Margin of Safety in Units = 450,000 – 289,000 = 161,000 units

Margin of Safety in Sales Dollars = $11,700,000 – $7,514,000 = $4,186,000

4-20

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-40

3. Contribution Margin Ratio = $6/$24 = 0.25

With additional sales of $160,000, the additional profit would be

P 4-41

=Break-Even Units1.

PROBLEMS

Fixed Cost

(Price – Variable Cost per Unit)

Fixed Cost

4-21

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-42

1. Unit Contribution Margin = $6,090,000/203,000 = $30

2. Increased contribution margin ($1,000,000 × 0.4286)……………….

…

$428,600

Less: Increased advertising expense………………………….………

…

250,000

Increased operating income………………………………….………

…

$178,600

4-22

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-43

1. Sales mix:

Basic: $3,000,000/$30 = 100,000 units

Aero: $2,400,000/$60 = 40,000 units

Variable Sales Total

Product Price

–

Cost* = × Mix = CM

2. New mix:

Variable Sales Total

Product Price

–

Cost* = × Mix = CM

Basic sleds $30 $10 5 $100

3. Increase in contribution margin for aerosleds (12,000 × $35)……

…

Decrease in contribution margin for basic sleds (5,000 × $20)……

$ 420,000

(100,000)

Contribution

Margin

$20

Margin

Contribution

4-23

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-44

1. Break-Even Units = $58,140/($3.40 – $2.55) = 68,400

Margin of Safety in Units = 81,600 – 68,400 = 13,200

2. Sales revenue ($3.40 × 81,600)……………………..………………..… $277,440

Total variable cost ($2.55 × 81,600)……………….…………….……

…

208,080

4. Operating Income = Sales – (Variable Cost Ratio × Sales) – Fixed Cost

P 4-45

1. Contribution Margin Ratio = $294,592/$460,300 = 0.64, or 64%

2. Break-Even Sales Revenue = $150,000/0.64 = $234,375

4. Additional variable expense: $460,300 × 0.04 = $18,412

New Contribution Margin = $294,592 – $18,412 = $276,180

5. Projected contribution margin*………………………………………

…

$324,180

Present contribution margin………………….………………………

…

294,592

Increase in contribution margin/profit………………………………

…

$ 29,588

*($460,300 + $80,000) × 0.60 = $324,180

4-24

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-45 (Continued)

Operating leverage will decrease because the increase in variable cost

P 4-46

2. Of total sales revenue, 60% is produced by floor lamps and 40% by desk lamps.

$360,000/$30 = 12,000 units

$240,000/$20 = 12,000 units

Thus, the sales mix is 1:1.

Variable Sales Total

Product Price

–

Cost = × Mix = CM

3.

Operating Leverage =

Operating Income

Contribution

Margin

Contribution Margin

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-47

1.

CM = $3 = $3

CM ratio = 0.25 = 0.375

3. Sales mix (from Requirement 2): 1 door handle to 2 trim kits

Sales Total

Product Price

–

= × Mix CM

Door handle $12 1 $3.00

Trim Kits = 2 × 16,222 = 32,444

4. Revenue (70,000 × $8)…………………….…………………………………

V

ariable cost (70,000 × $5)…………………….…………………………

…

P 4-48

1. Break-Even Units = $300,000/ $14* = 21,429**

=

$9

$8 – $5

$3/$8

Trim Kits

Contribution

Margin

560,000$

$3

350,000

V

ariable

Cost

Door Handles

$12 – $9

$3/$12

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-48 (Continued)

3. Sales………………………………………………………………………

…

$1,218,000

V

ariable cost (0.45 × $1,218,000)……………….…………..………

…

548,100

P 4-49

= 0.22, or 22%

2. Break-Even Sales Revenue = $110,000/0.22 = $500,000

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-50

1. Income = Revenue – Variable Cost – Fixed Cost

P 4-51

1. Contribution Margin per Unit = $5.60 – $4.20*

= $1.40

3. Sales ($5.60 × 35,000)…….…………………………..…………………

…

196,000$

V

ariable cost ($4.20 × 35,000)………………………………………..…

…

147,000

OR

4-28

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

2.

X = $50,000/(1 – 0.80)

X = $50,000/ 0.20

3. Duncan: 3 × 30% = 90%

Macduff: 9 × 30% = 270%

Duncan

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

P 4-53

1. Contribution margin ratios:

2. Fixed costs:

May of current year = $680 + 4,300 + $5,600 + $9,750 = $20,330

3. Margin of safety:

4. Clearly, the sharp rise in fixed cost from the prior year to the current year has

had a strong impact on the break-even point and the margin of safety. Kicker

4-30

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

Case 4-54

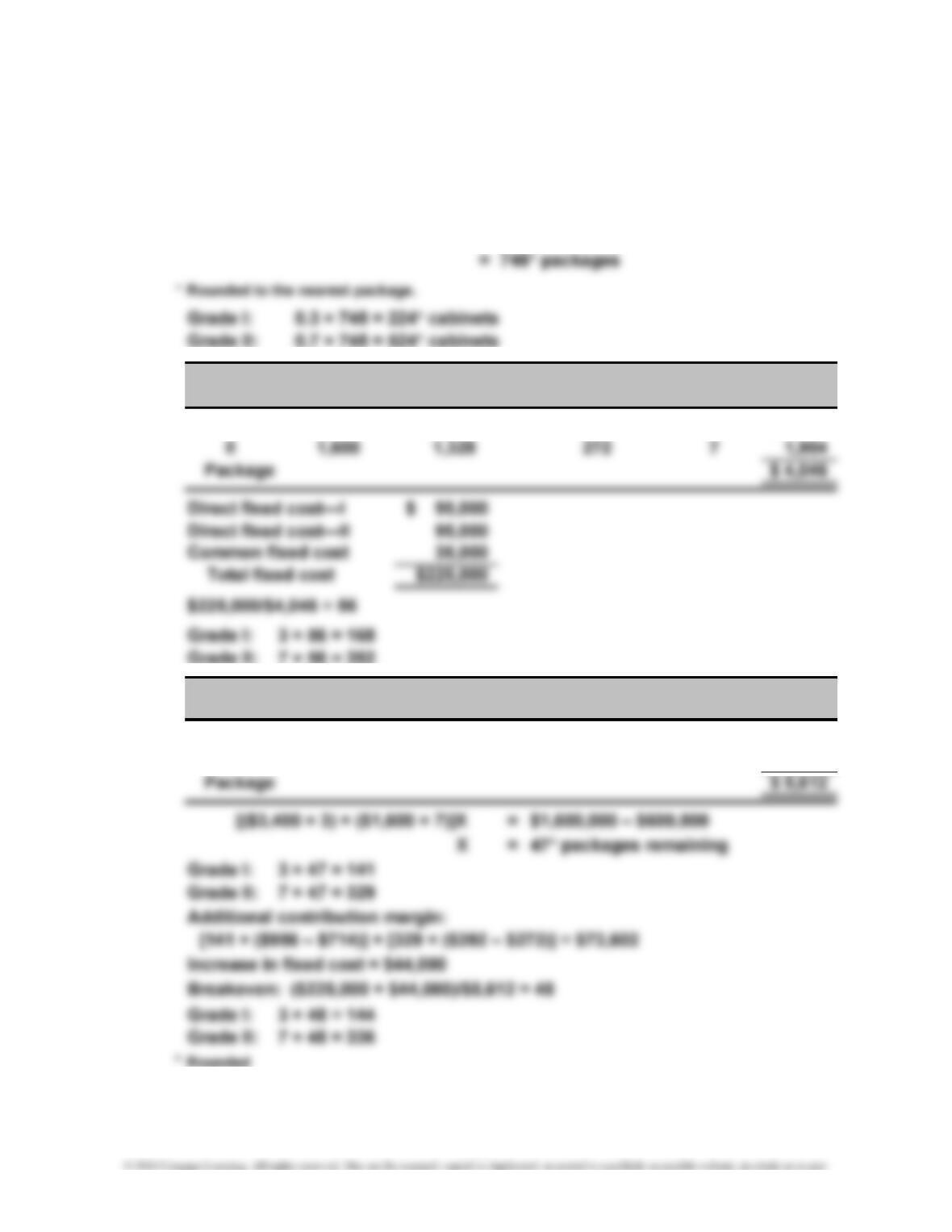

1. Let X be a package of 3 Grade I cabinets and 7 Grade II cabinets.

0.30X($3,400) + 0.70X($1,600) =

2. Contribution Sales Total

Product Price

–

= Margin × Mix = CM

I $3,400 $714 3 2,142$

3.

V

ariable Contribution Sales Total

Product Price

–

Cost = Margin × Mix = CM

I $3,400 $2,444 $956 3 2,868$

II 1,600 1,208 392 7 2,744

*

CASES

$1,600,000

Variable

Cost

$2,686

*

*

4-31

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

Case 4-54 (Continued)

If the new break-even point is interpreted as a revised break-even point for the

current year, then total fixed cost must be reduced by the contribution margin

already earned (through the first five months) to obtain the units that must be

4. Variable Sales Total

Product Price

–

Cost = × Mix = CM

I $3,400 $2,686 $714 1 $714

…

Increase in fixed costs:

$70,000 × (7/12)………………………………………………

…

40,833

Increase in operating income………………………………

…

$25,365

The break-even point (for the current year and the remaining 7 months,

respectively) is computed as follows:

Contribution

Margin

*

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

Case 4-54 (Concluded)

To this, add the units already sold, yielding the revised break-even point:

Case 4-55

3. The right to decide which process should be chosen belongs to the divisional

manager. Danna has an ethical obligation to report the correct information to her

superior. By altering the sales forecast, Danna unfairly and unethically influenced

the decision-making process. Managers certainly have a moral obligation to

assess the impact of their decisions on employees, and every effort should be

taken to be fair and honest with employees. Danna’s behavior, however, is not

justified by the fact that it helped a number of employees retain their employment.

First, Danna had no right to make that decision. Danna certainly has the right to

voice her concerns about the impact of automation on the employees’ well-being.