1. Standard costs are essentially budgeted amounts on a per-unit basis. Unit standards serve as

inputs in building budgets.

2. Unit standards are used to build flexible budgets. Unit standards for variable costs are the

variable cost component of a flexible budgeting formula.

5. Standard costing systems improve planning and control and facilitate product costing.

6. By identifying standards and assessing deviations from the standards, managers can locate

areas where change or corrective behavior is needed.

9. Managers generally tend to have more control over the quantity of an input used rather than the

price paid per unit of input.

10. A standard cost variance should be investigated if the variance is material and if the benefit of

investigating and correcting the deviation is greater than the cost.

13. Disagree. A materials usage variance can be caused by factors beyond the control of the

production manager, e.g., purchase of a lower (or higher) quality of material than normal.

14. Disagree. Using higher-priced workers to perform lower-skilled tasks is an example of an event

that will create a rate variance that is controllable.

10 STANDARD COSTING:

A MANAGERIAL CONTROL TOOL

DISCUSSION QUESTIONS

10-1

CHAPTER 10 Standard Costing: A Managerial Control Tool

15. Some possible causes of an unfavorable labor efficiency variance are inefficient labor, machine

downtime, and poor-quality materials.

16. A kaizen standard is the planned improvement for the coming period. Usually, kaizen focuses on

17. Target costing is a cost management method that is used to reduce costs to a level that reflects

10-2

CHAPTER 10: Standard Costing: A Managerial Control Tool

10-1. a

10-2. e

10-9. d

10-10. a

10-11. c

10-12. d

MULTIPLE-CHOICE QUESTIONS

10-3

CHAPTER 10 Standard Costing: A Managerial Control Tool

CE 10-20

CE 10-21

CE 10-22

CORNERSTONE EXERCISES

Actual Costs Budgeted Costs Total Variance

60,000

65,000

70,000

10-4

CHAPTER 10: Standard Costing: A Managerial Control Tool

CE 10-23

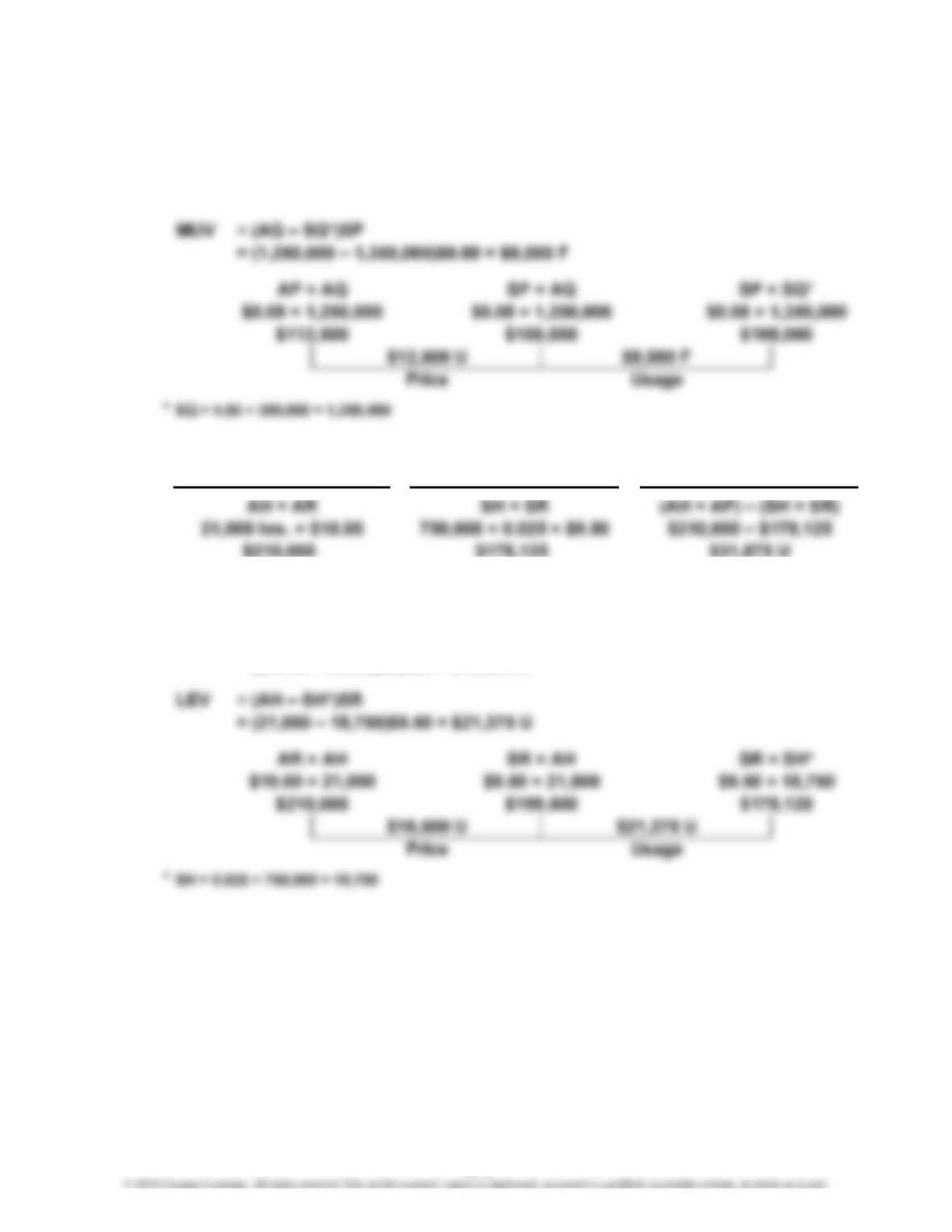

MPV = (AP – SP)AQ

= ($0.09 – $0.08)1,250,000 oz. = $12,500 U

CE 10-24

CE 10-25

LRV = (AR – SR)AH

= ($10.00 – $9.50)21,000 = $10,500 U

Budgeted Costs

Actual Costs

Total Variance

10-5

CHAPTER 10 Standard Costing: A Managerial Control Tool

E 10-26

1. SH = 5 × 7,500 = 37,500 hours

E 10-27

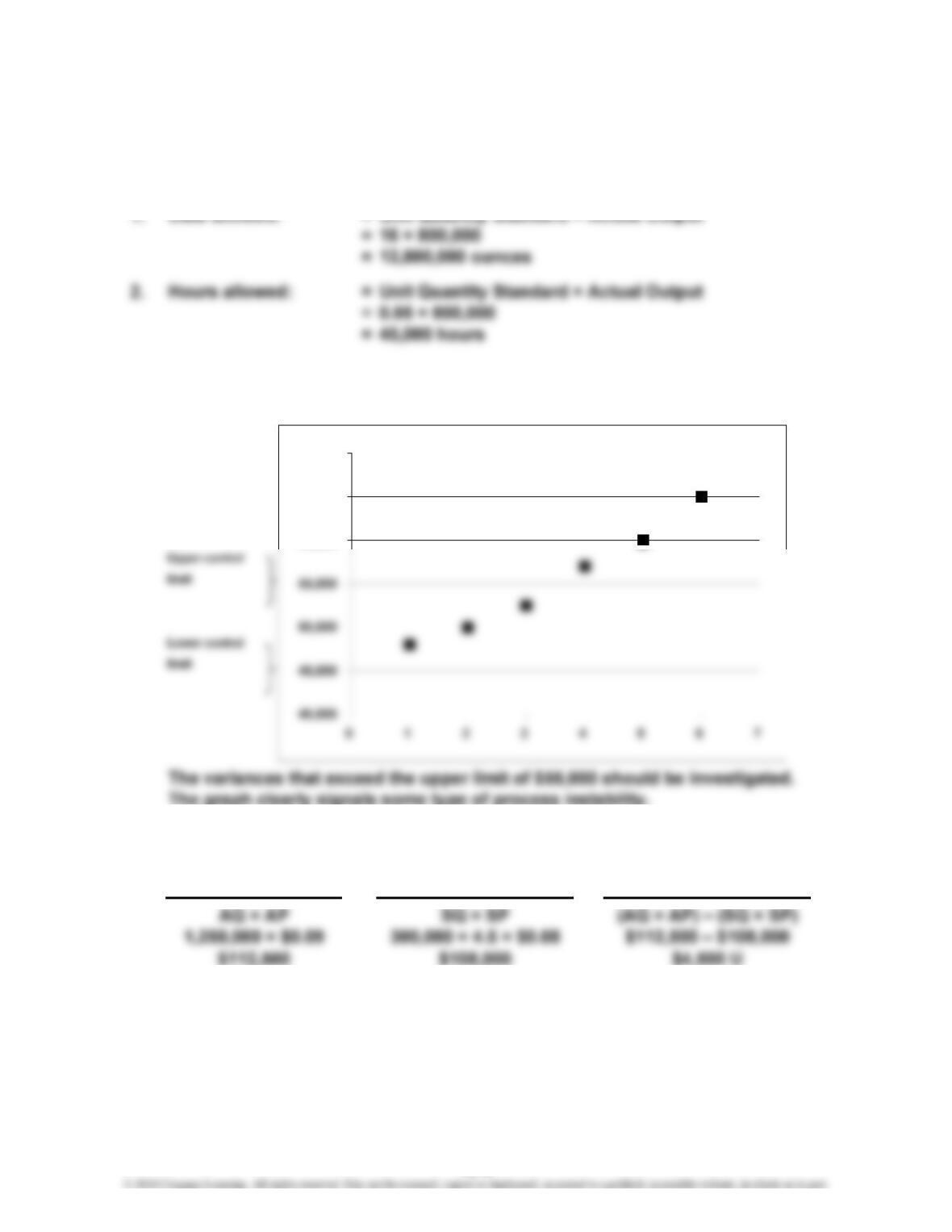

1. Cases needing investigation:

Week 2: Exceeds the 10% rule.

E 10-28

1. Materials:

Labor:

2. Actual Cost* Budgeted Cost

EXERCISES

V

ariance

$12 × 92,000 = $1,104,000

$ 9 × 92,000 = $828,000

CHAPTER 10: Standard Costing: A Managerial Control Tool

E 10-29

1. MPV = (AP – SP)AQ

= ($3.60 – $4.00)287,500 strips = $115,000 F

2. The suggestion of the purchasing manager is premature. A favorable

materials price can produce an effect on both materials usage and labor

E 10-30

1. LRV = (AR – SR)AH

= ($12.50 – $12.00)78,200 = $39,100 U

2. The feedback from the production manager pinpoints the cause of the

variances. The favorable materials variance is apparently due to the

10-7

CHAPTER 10 Standard Costing: A Managerial Control Tool

E 10-31

1. MPV = (AP – SP)AQ

3. MUV = (AQ – SQ)SP

$4,000 = [2,000,000 – 128 (Quantity Produced)] × $0.05

80,000 = 2,000,000 – 128 (Quantity Produced)

E 10-32

1. LRV = (AR – SR)AH

= ($9.50 – $10.00)360,000 = $180,000 F

10-8

E 10-33

1. MPV = (AP – SP)AQ

= ($5.10 – $5.00)1,860,000

= $186,000 U

2. LRV = (AR – SR)AH

= ($11.85 – $12.00)725,000

= $108,750 F

E 10-34

1. Tom purchased the large quantity to obtain a lower price so that the price

standard could be met. In all likelihood, given the reaction of Jackie Iverson,

2. It sounds like the price standard may be out of date. Revising the price standard

and implementing a policy concerning quantity purchases would likely prevent

this behavior from reoccurring.

3. Tom apparently acted in his own self-interest when making the purchase. He

surely must have known that the quantity approach was not the objective. Yet

10-9

CHAPTER 10 Standard Costing: A Managerial Control Tool

E 10-35

Materials:

E 10-36

Debit Credit

1. Materials 75,525

MPV 12,525

Accounts Payable 63,000

2. Work in Process 68,400

$68,400

Journal

Date Account & Explanation

SP × SQ*

$0.95 × 79,500 $0.95 × 72,000

AP × AQ SP × AQ

$63,000 $75,525

CHAPTER 10: Standard Costing: A Managerial Control Tool

E 10-37

1. MPV = (AP – SP)AQ

= ($8.35 – $8.25)38,000 = $3,800 U

2.

Debit Credit

Materials 313,500

MPV 3,800

E 10-38

1. LRV = (AR* – SR)AH

= ($9.80 – $9.65)25,040 = $3,756 U

2.

Debit Credit

Work in Process 247,040

Date Account & Explanation

Journal

Journal

Date Account & Explanation

10-11

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-39

1. a. The managers of each cost center should be involved in setting standards.

They understand the actual conditions and are the primary source fo

r

information on quantity used and wages paid. The newly designated

materials purchasing manager is the information source for material

2. Once the standards are set, actual results can be compared with the standards

and variances can be calculated. Of course, the variances themselves are onl

y

indicators of potential problems. The underlying causes of the variances must

be determined to decide whether or not corrective action is needed. For this

reason, responsibility for the variances will be assigned to those with the most

PROBLEMS

CHAPTER 10: Standard Costing: A Managerial Control Tool

P 10-40

1. Materials:

2. Labor for new process:

3. Labor for new process, one week later:

AR × AH

$11 × 10,800

SR × SH**

AR × AH SR × AH SR × SH

SP × SQ*

$3.50 × 72,000

AP × AQ

$3.55 × 69,000

SP × AQ

$3.50 × 69,000

$11 × 9,000

$11 × 10,200

SR × AH

$11 × 10,200

10-13

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-41

1. Granite:

MPV = Actual Cost – (AQ × SP)

= $79,048 – (1,640 × $50) = $2,952 F

2. Cutting Labor:

LRV = (AR – SR)AH

= ($15 – $15)180 = $0

3. It would probably not be worthwhile for Charlene to establish standards

for every different type of installation. Tom and Tony have a small enough

10-14