P 10-42

1. Standard Standard

Usage Cost

Direct materials……………………

…

$ 4 25.000 $100.00

2. There would be unfavorable labor efficiency variances for the first 320 units

because the standard hours are much lower than the actual hours at this level.

3. The cumulative average time per unit is an averag

e

. For example, the first

40 units take an average of 2.50 hours per unit. The second 40 take an

average of 1.5 hours per unit [(80 × 2) – (40 × 2.5)]/40 = 1.5, and, therefore,

Standard

Price

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-43

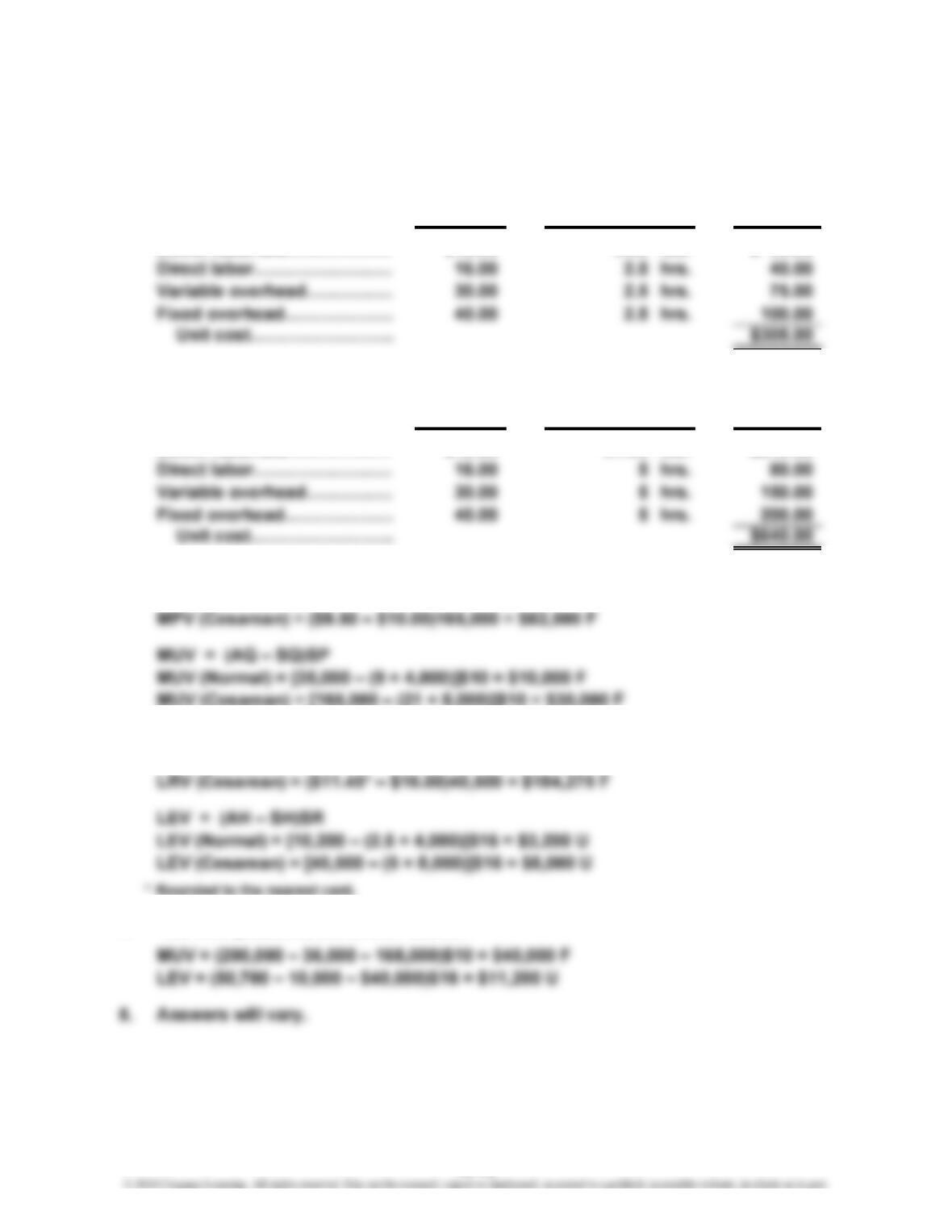

1. Normal delivery:

Standard Standard

Price Cost

Direct materials……………… $10.00 9.00 lbs. $ 90.00

Cesarean delivery:

Standard Standard

Price Cost

Direct materials……………… $10.00 21.00 lbs. $210.00

2. MPV = (AP – SP)AQ

MPV (Normal) = ($9.50 – $10.00)35,000 = $17,500 F

3. LRV = (AR – SR)AH

LRV (Normal) = ($11.45* – $16.00)10,200 = $46,410 F

4. Yes. Computations are shown below.

Usage

Standard

Usage

Standard

10-16

CHAPTER 10: Standard Costing: A Managerial Control Tool

P 10-44

1. Liquid Standard = 4.5 × 250,000 × $0.40 = $450,000

Upper control limit (UCL): $495,000 or $470,000; lesser = $470,000

Lower control limit (LCL): $405,000 or $430,000; greater = $430,000

2. Total Liquid Variance = $567,000 – $450,000 = $117,000 U

MPV = ($0.42 – $0.40)1,350,000 = $27,000 U

MUV = (1,350,000 – 1,125,000)$0.40 = $90,000 U

3. Total Labor Variance = $733,000 – $750,000 = $17,000 F

LRV = ($15.19* – $15.00)48,250 = $9,168 U

LEV = (48,250 – 50,000)$15.00 = $26,250 F

10-17

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-45

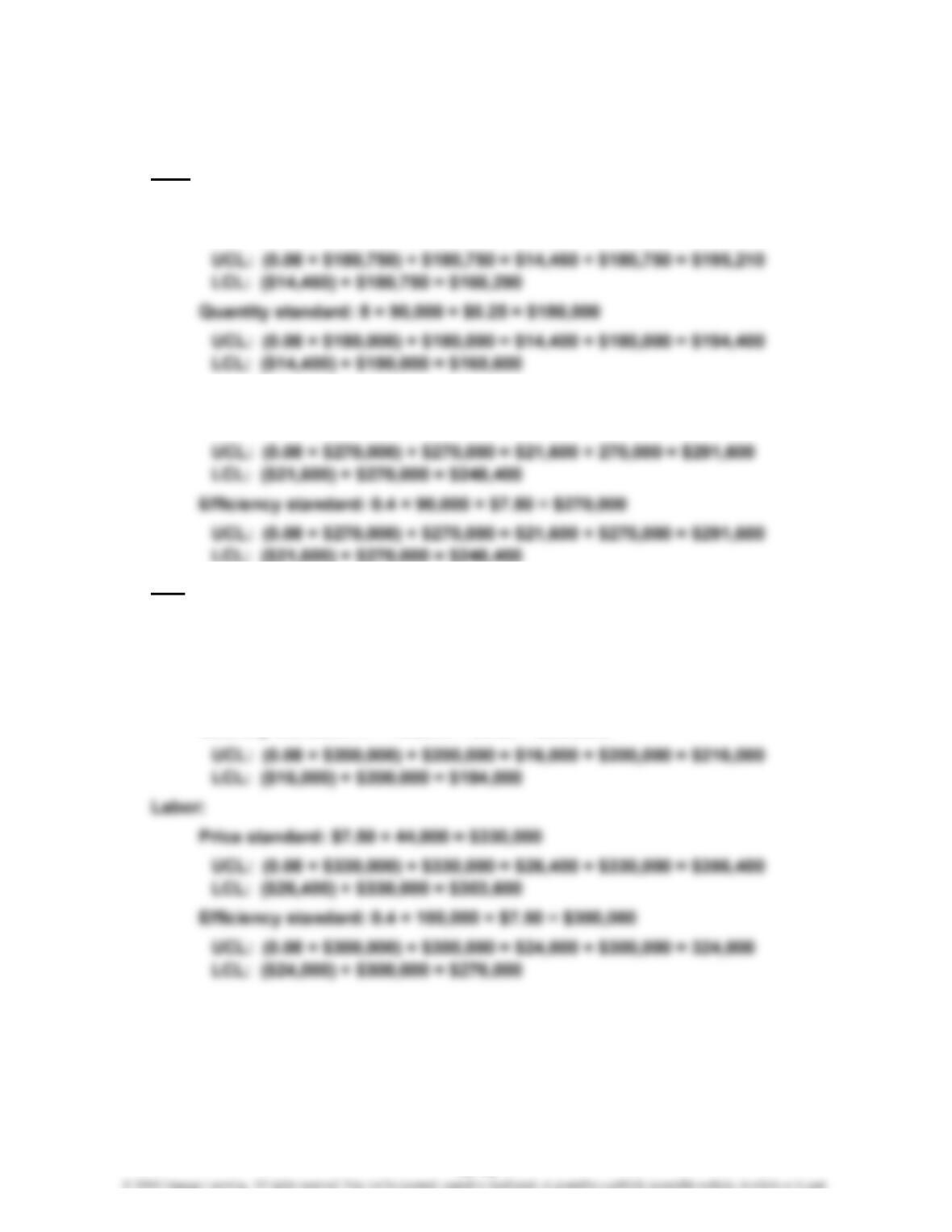

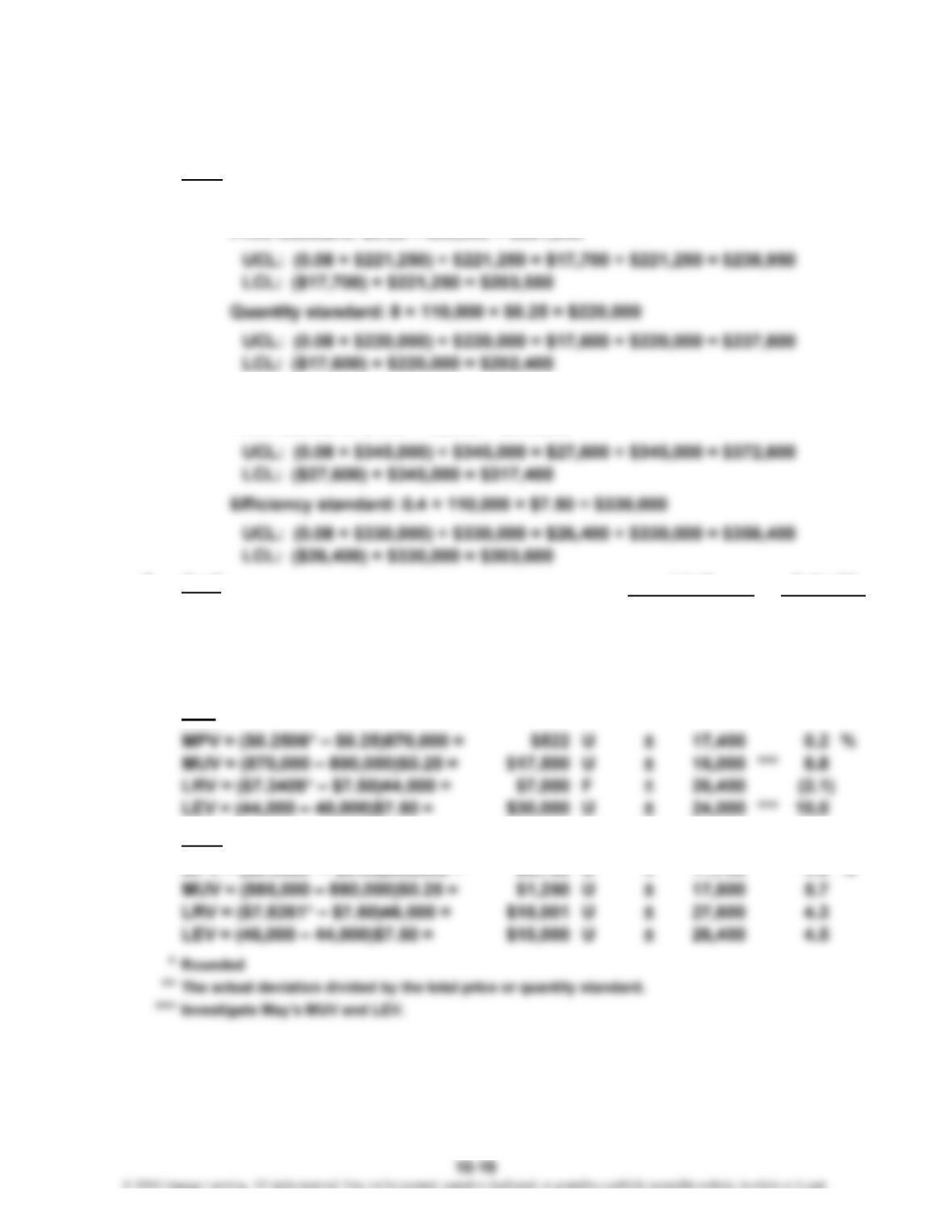

1. April (UCL = Upper control limit, and LCL = Lower control limit)

Materials:

Price standard: $0.25 × 723,000 = $180,750

Labor:

Price standard: $7.50 × 36,000 = $270,000

LCL: ($21,600) + $270,000 = $248,400

May

Materials:

Price standard: $0.25 × 870,000 = $217,500

UCL: (0.08 × $217,500) + $217,500 = $17,400 + $217,500 = $234,900

LCL: ($17,400) + $217,500 = $200,100

Quantity standard: 8 × 100,000 × $0.25 = $200,000

10-18

CHAPTER 10: Standard Costing: A Managerial Control Tool

P 10-45 (Continued)

June

Materials:

Price standard: $0.25 × 885,000 = $221,250

Labor:

Price standard: $7.50 × 46,000 = $345,000

2. April

MPV = ($0.2614* – $0.25)723,000 = $8,242 U ± $14,460 4.6 %

MUV = (723,000 – 720,000)$0.25 = $750 U ± 14,400 0.4

LRV = ($7.5000 – $7.50)36,000 = $0 ± 21,600 0.0

LEV = (36,000 – 36,000)$7.50 = $0 ± 21,600 0.0

May

June

MPV = ($0.2599* – $0.25)885,000 = $8,762 U ± 17,700 4.0 %

A

ctual*

*

Limit

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-45 (Continued)

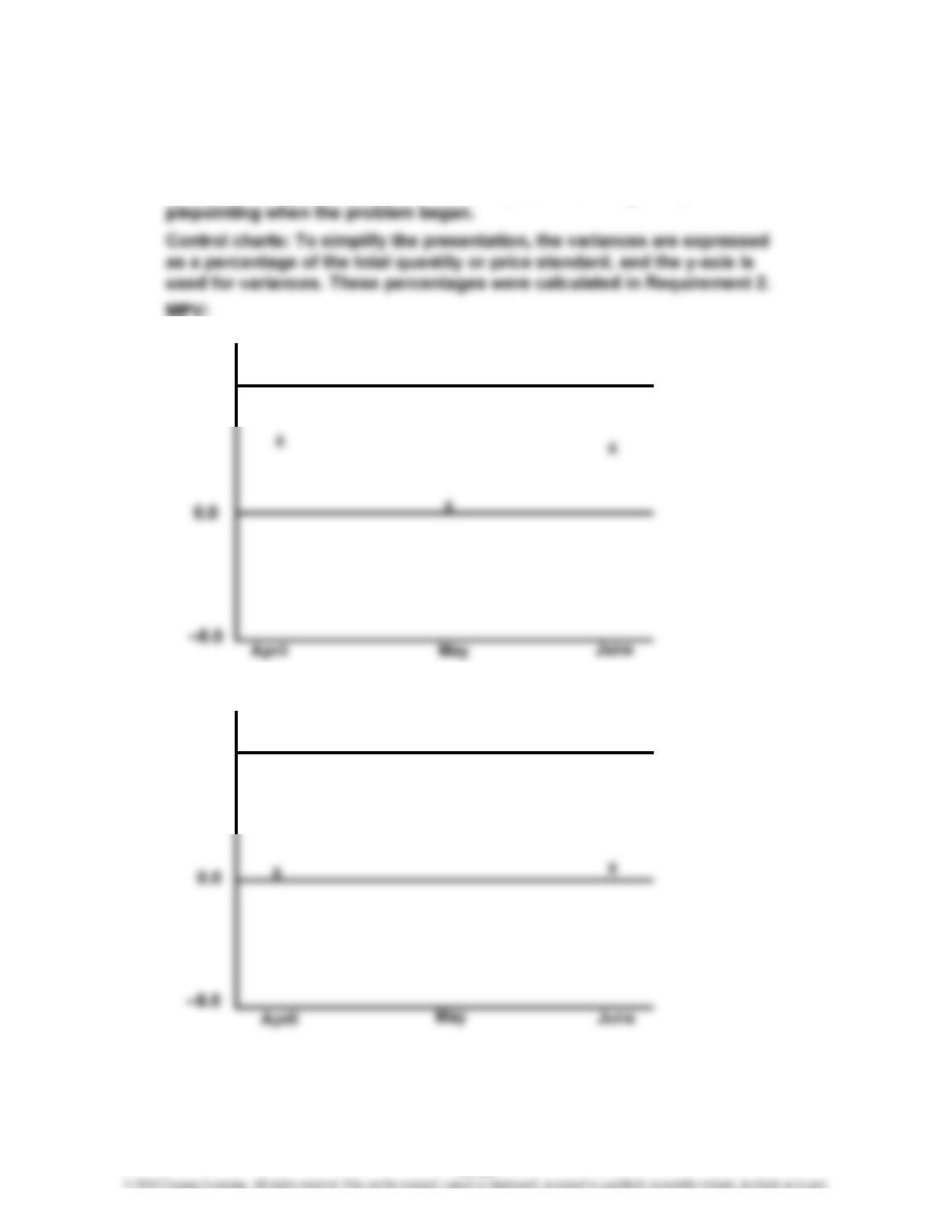

3. Control charts allow us to see when the variances are outside an

acceptable range. They may also show a pattern that might help in

%

MUV:

%

8.0

10.0

8.0

10.0

X

10-20

CHAPTER 10: Standard Costing: A Managerial Control Tool

P 10-45 (Continued)

LRV:

%

LEV:

%

8.0

10.0

8.0

10.0

X

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-46

1. MPV = (AP – SP)AQ

= ($1.55 – $1.50)44,250 = $2,213* U

* Rounded to the nearest dollar.

2. LRV = (AR × AH) – (SR × AH)

= Actual Labor Cost – (SR × AH)

3. LRV = (AR × AH) – (SR × AH)

= Actual Labor Cost – (SR × AH)

= $132,000 – ($10 × 13,200) = $0

P 10-47

1. MPV = (AQ × AP) – (SP × AQ)

= Actual Materials Cost – (SP × AQ)

2. LRV = (AR × AH) – (SR × AH)

= Actual Labor Cost – (SR × AH)

10-22

CHAPTER 10: Standard Costing: A Managerial Control Tool

P 10-47 (Continued)

3. The basic advantages offered by a standard costing system include its

use in planning, control, and decision making. A standard costing system

helps in budgeting since the unit standard costs can be multiplied by the

predicted level of production to obtain total costs. Standard costs are

P 10-48

1. MPV = (AP – SP)AQ

= ($4.70 – $5.00)260,000 = $78,000 F

MUV = (AQ – SQ*)SP

2. LRV = (AR – SR)AH

= ($13 – $12)82,000 = $82,000 U

LEV = (AH – SH**)S

R

CHAPTER 10 Standard Costing: A Managerial Control Tool

P 10-48 (Continued)

Production is usually responsible for labor efficiency. In this case, efficiency may

3. Three variances are potentially affected by material quality:

MPV…………………………………

…

$ 78,000 F

4.

Debit Credit

Materials 1,300,000

MPV 78,000

Journal

Date Account & Explanation

10-24

CHAPTER 10: Standard Costing: A Managerial Control Tool

Case 10-49

1. By using a standard costing system, Crunchy Chips can increase control

of its manufacturing inputs. By developing price and quantity standards

for each input, management can compute price and usage variances for

2. The engineering standards are ideal standards. The president’s concern

is probably reflecting doubt that the labor standards can be achieved. If

CASES

CHAPTER 10 Standard Costing: A Managerial Control Tool

Case 10-49 (Continued)

3. Standard cost sheet (for one box of chips):

Direct materials:

Potatoes (15.9375* lbs. @ $0.238)…

…

$3.7931

Direct labor:**

Potato inspection (0.006 hr. @ $15.20)………………………

…

$0.0912

Chip inspection (0.0225 hr. @ $10.30)………………………

…

0.2318

Frying monitor (0.0118 hr. @ $14.00)…………………………

…

0.1652

…

4. MU

V

= (AQ – SQ****)S

P

= (9,500,000 – 9,350,000)$0.23

8

= $35,700 U

***

*

SQ = 15.9375 × 8,800,000/15 = 9,350,000

10-26

CHAPTER 10: Standard Costing: A Managerial Control Tool

Case 10-50

1. Pat’s decision was wrong and not in the best interests of the company.

His concern for his bonus and promotion was apparently more important

2. The use of standards to evaluate performance and assess rewards

apparently was influential in Pat’s decision. He clearly had a desire to

receive his annual bonus and wanted to present an impressive

3. Purchasing agents have ethical responsibilities similar to accountants.

Integrity is a universally desirable characteristic. Pat and other purchasing

4. Answers will vary.