1. CVP analysis allows managers to focus on selling prices, volume, costs, profits, and

sales mix. Many different “what-if” questions can be asked to assess the effect of

changes in key variables on profits.

4.

A

t the break-even point, all fixed costs are covered. Above the break-even point, only

variable costs need to be covered. Thus, contribution margin per unit is profit per unit,

provided that the unit selling price is greater than the unit variable cost (which it must be

for breakeven to be achieved).

5. Variable Cost Ratio = Variable Cost per Unit/Price

8. Packages of products, based on the expected sales mix, are defined as a single product.

Selling price and cost information for this package can then be used to carry out CVP

analysis.

9. This statement is wrong; break-even analysis can be easily adjusted to focus on targeted

profit.

A

4COST-VOLUME-PROFIT ANALYSIS:

A MANAGERIAL PLANNING TOOL

DISCUSSION QUESTIONS

4-1

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

12. Margin of safety is the sales activity in excess of that needed to break even. The higher the

margin of safety, the lower the risk.

15.

A

declining margin of safety means that sales are moving closer to the break-even point.

Profit is going down, and the possibility of loss is greater. Managers should analyze the

reasons for the decreasing margin of safety and look for ways to increase revenue and/or

decrease costs.

4-1. b

4-2. d

4-8. d

4-9. d Break-Even Units = $7,200/($12 – $3) = 800

MULTIPLE-CHOICE QUESTIONS

4-2

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

CE 4-13

3.

Total Per Unit

Sales ($75 × 5,000 helmets)…………………………

…

$375,000 $75.00

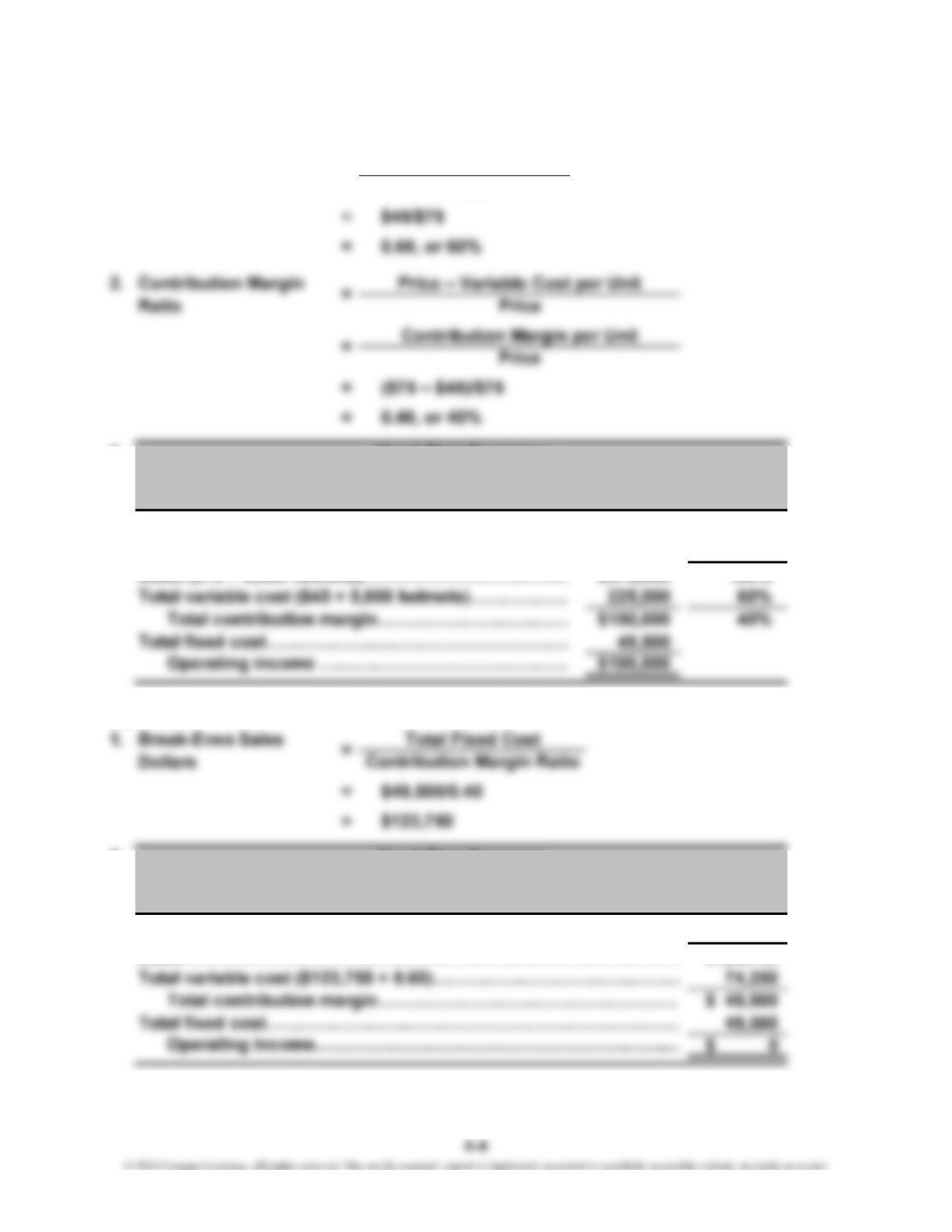

CE 4-14

2.

Total

A

t Break-Even Poin

t

For the Coming Year

Head-First Company

CORNERSTONE EXERCISES

Contribution Margin Income Statement

Head-First Company

Contribution Margin Income Statement

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

CE 4-15

3.

Percent

of Sales

Sales ($75 × 5,000 helmets)……………………………

…

$375,000 100%

CE 4-16

2.

Total

Sales…………………………………………………………………………

…

$123,750

Variable Cost Ratio1. = Variable Cost per Unit

Price

At Break-Even Poin

t

For the Coming Year

Head-First Company

Contribution Margin Income Statement

Head-First Company

Contribution Margin Income Statement

CE 4-17

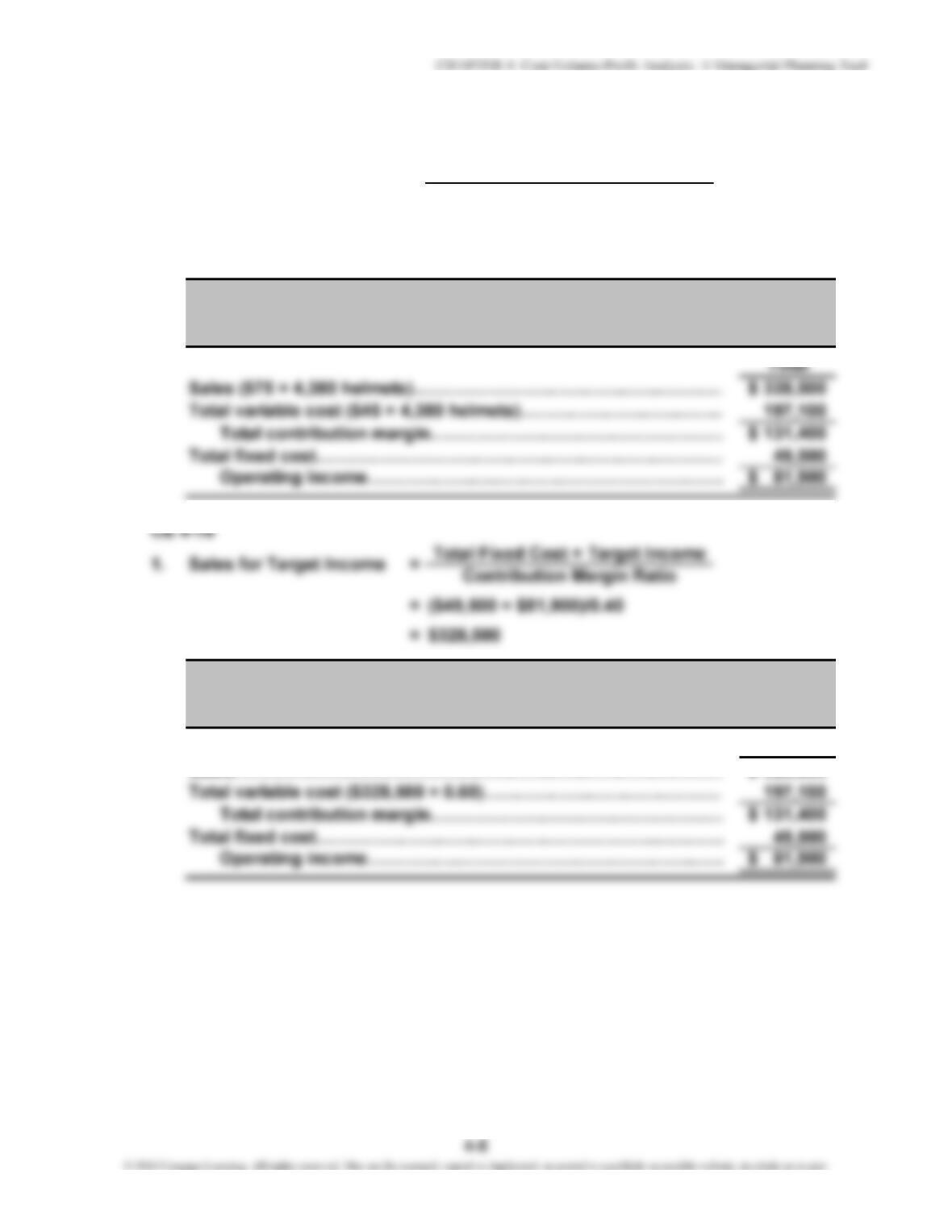

= ($49,500 + $81,900)/($75 – $45)

= 4,380 helmets

2.

…

2.

Total

Sales…………………………………………………………………………

…

328,500$

Break-Even Units

A

t 4,380 Helmets Sold

Head-First Company

Contribution Margin Income Statement

1.

Contribution Margin Income Statement

A

t 4,380 Helmets Sold

Total Fixed Cost + Target Income

Price – Variable Cost per Unit

Head-First Company

=

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

CE 4-19

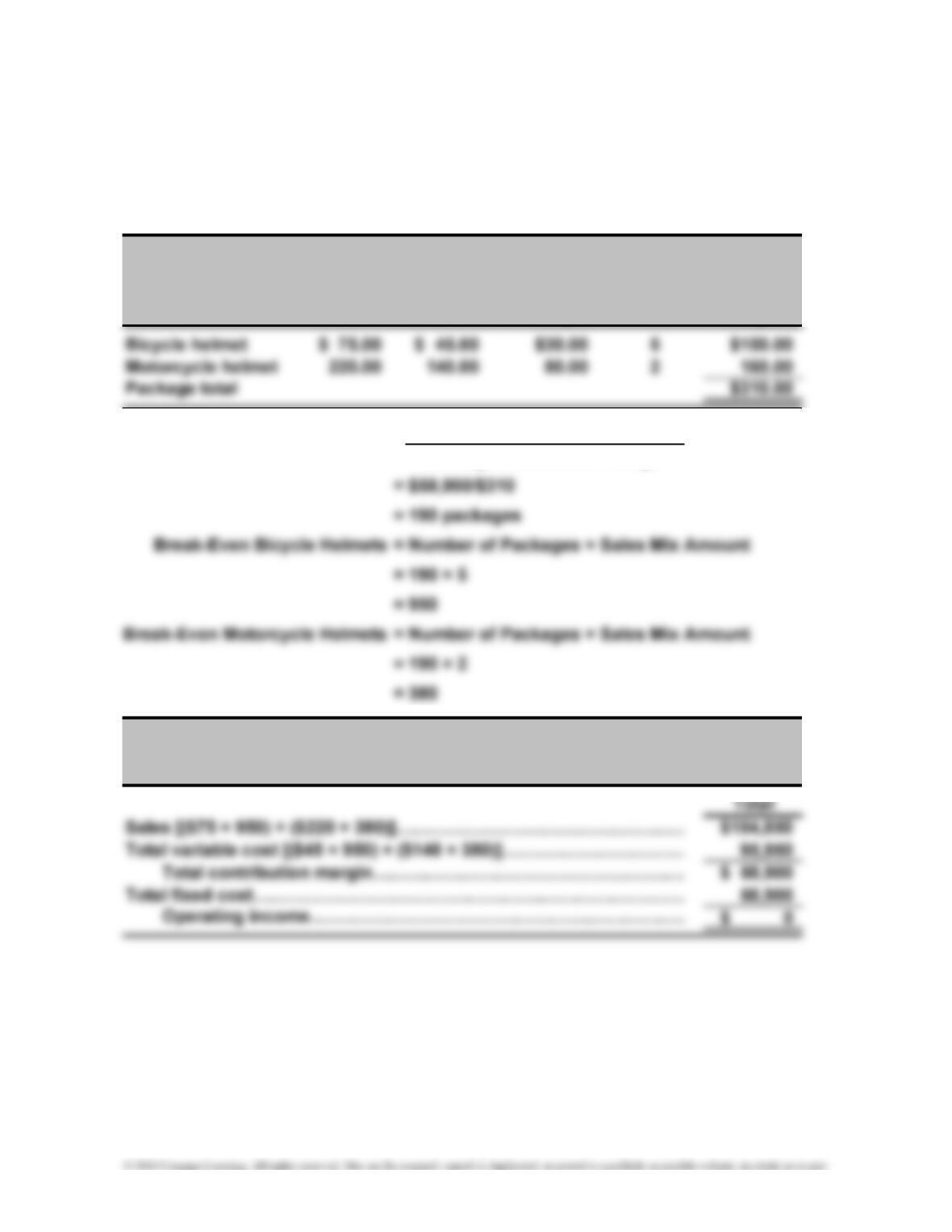

1. Any package with 5 bicycle helmets for every 2 motorcycle helmets is fine. For

example, 5:2, or 10:4, or 30:12. Throughout the rest of this exercise, we will use

5:2.

Package

Unit Unit Unit

Variable Contribution Sales Contribution

Product Price – Cost = Margin × Mix = Margin

Total Fixed Cost

3.

At Break-Even Poin

t

Head-First Company

Package Contribution Margin

Break-Even Packages =2.

Contribution Margin Income Statement

4-6

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

CE 4-20

2.

Total

Sales…………………………………………………………………………

…

$184,466

CE 4-21

1. Margin of Safety in Units = Budgeted Units – Break-Even Units

Head-First Company

Contribution Margin Income Statement

A

t Break-Even Sales Dollars

CE 4-22

*Rounded

CE 4-23

1. Percent Change in Operating Income = DOL × Percent Change in Sales

4-8

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-24

1. Direct materials…………………………………….……………….……

…

$1.90

Direct labor………………………………………….……………….……

…

1.40

2. Contribution Margin Ratio = $13/$20 = 0.65, or 65%

Variable Cost Ratio = $7/$20 = 0.35, or 35%

…

Operating income…………………….……………….………………

…

$0

E 4-25

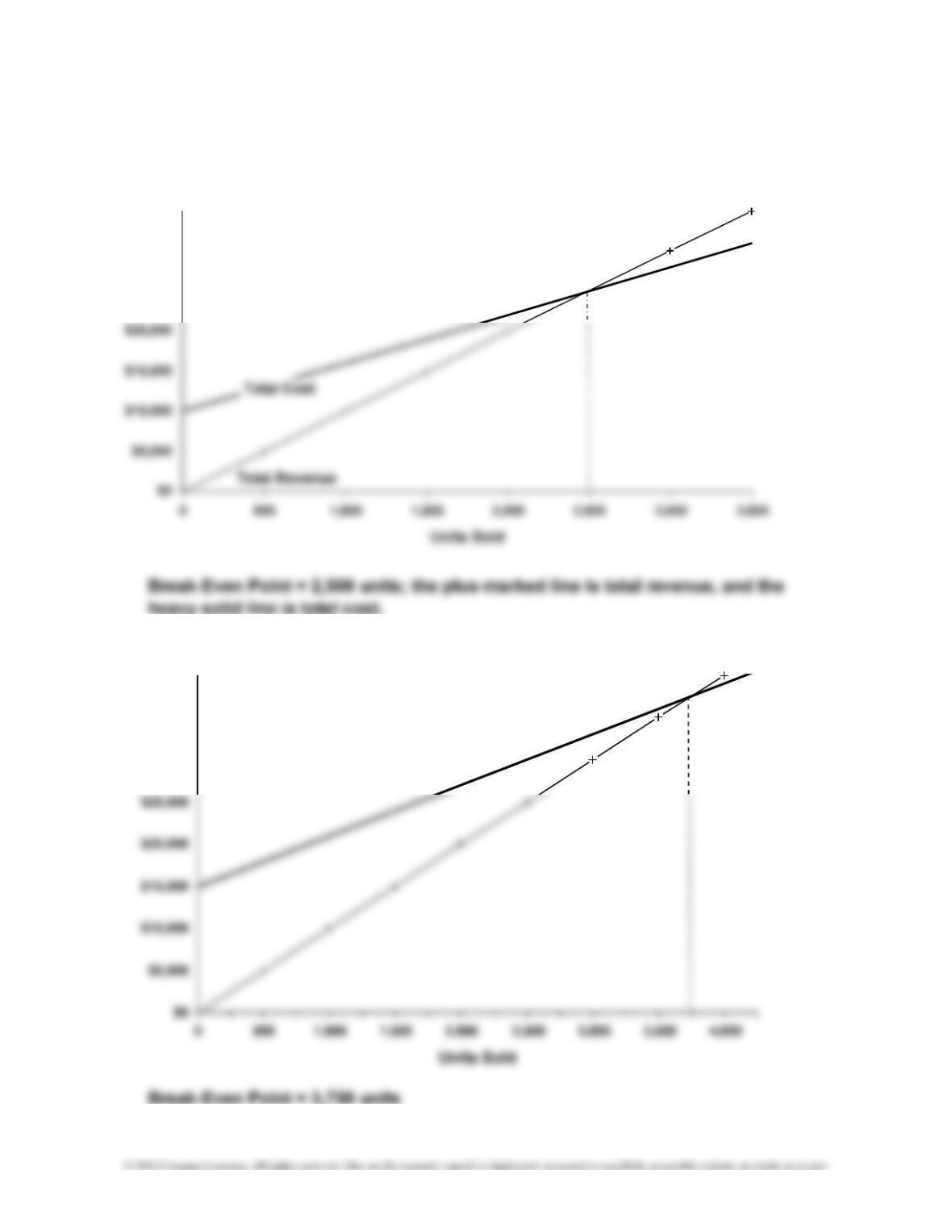

1. At breakeven:

2. Operating Income = (Price × Quantity) – (Variable Cost per Unit × Quantity) –

Fixed Cost

EXERCISES

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-25 (Continued)

3. Total Contribution Margin = Actual Revenue × Contribution Margin Ratio

4. Break-Even Units = Total Fixed Cost/(Price – Variable Cost per Unit)

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-26

1. Contribution Margin

Ratio

= $26,600/$95,000 = 0.28, or 28%

4. To increase operating income without increasing sales revenue, Pelley

would have to find a way to decrease variable cost (thus decreasing the

variable cost ratio and increasing the contribution margin ratio), decrease

fixed cost, or do a combination of both.

E 4-27

1. Sales ($16.00 × 26,800)………………..………………………..…… 428,800$

.

E 4-28

1. Break-Even Units = ($111,425 + $48,350)/($2.75 – $1.65)

= $159,775/$1.10

=

2. Unit variable cost includes all variable costs on a unit basis:

Direct materials…………………………………………………….…

…

$0.37

145,250

Contribution Margin

Sales

=

4-11

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-28 (Continued)

Unit variable manufacturing cost includes the variable costs of production

on a unit basis:

=

4. Sales revenue to earn $13,530 = 157,550 × $2.75 = $433,262.50

E 4-29

1. Break-Even Units = ($245,650 + $297,606)/($8.12 – $4.56) = 152,600

2. Expected sales in units……………………………………………..

…

225,000

4. If the price decreases, then the risk facing the company will go up. The

price decrease means that the contribution margin per unit will decrease

E 4-30

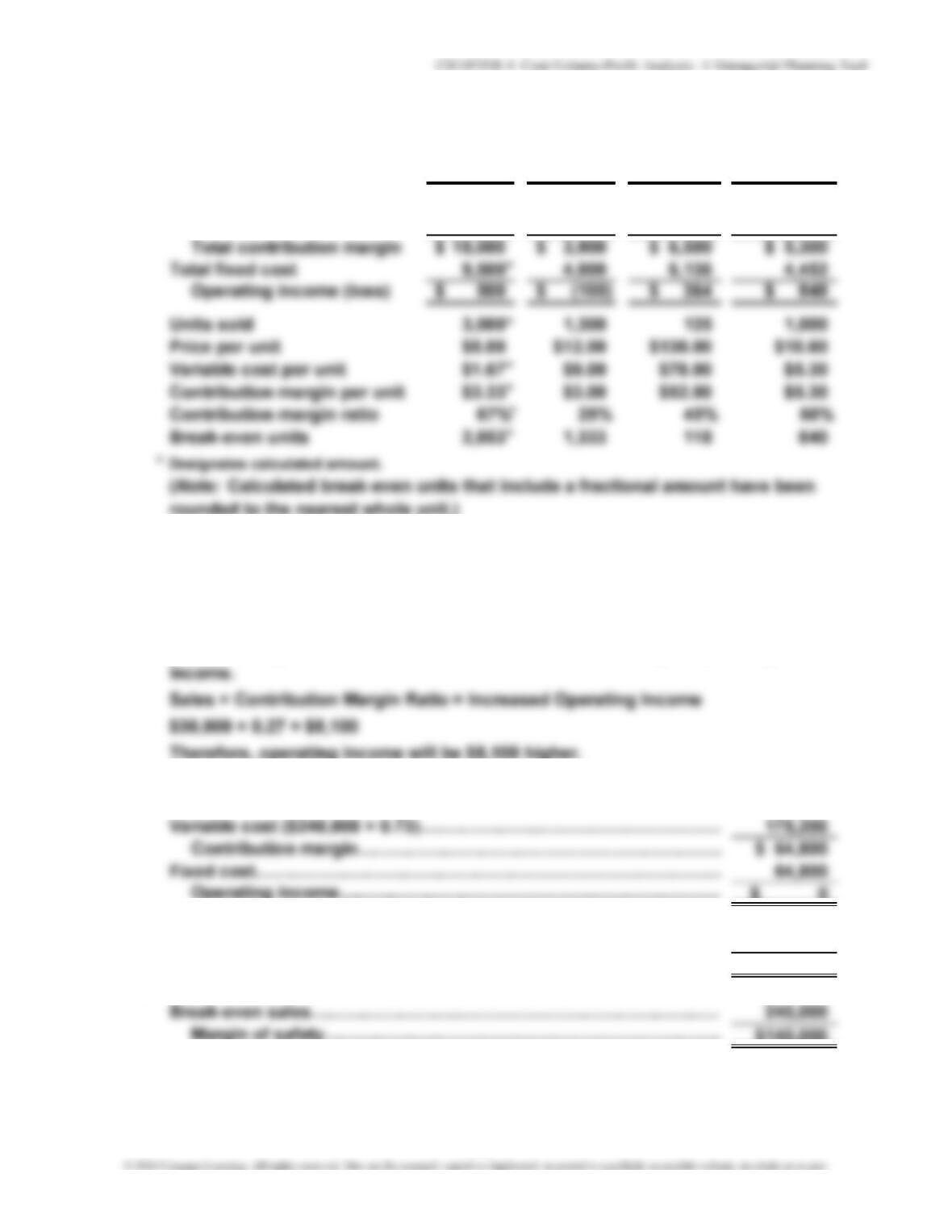

Laertes Ophelia Fortinbras Claudius

Sales 15,000$ 15,600$ $16,250 $10,600

Total variable cost 5,000 11,700 9,750 5,300

E 4-31

1. Variable Cost Ratio = $302,950/$415,000 = 0.73, or 73%

Contribution Margin Ratio = $112,050/$415,000 = 0.27, or 27%

2. Because all fixed costs are covered at breakeven, the contribution margin

portion of any revenue above breakeven contributes directly to operating

3. Break-Even Sales Revenue = $64,800/0.27 = $240,000

Sales……………………………………………………………………………

…

$240,000

4. Expected sales………………………………………………………………

…

$415,000

Break-even sales…………………………………….………………………

…

240,000

Margin of safety………………………..…………………………………

…

$175,000

5. Sales revenue………………..………………………………………………

…

$380,000

…

4-13

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

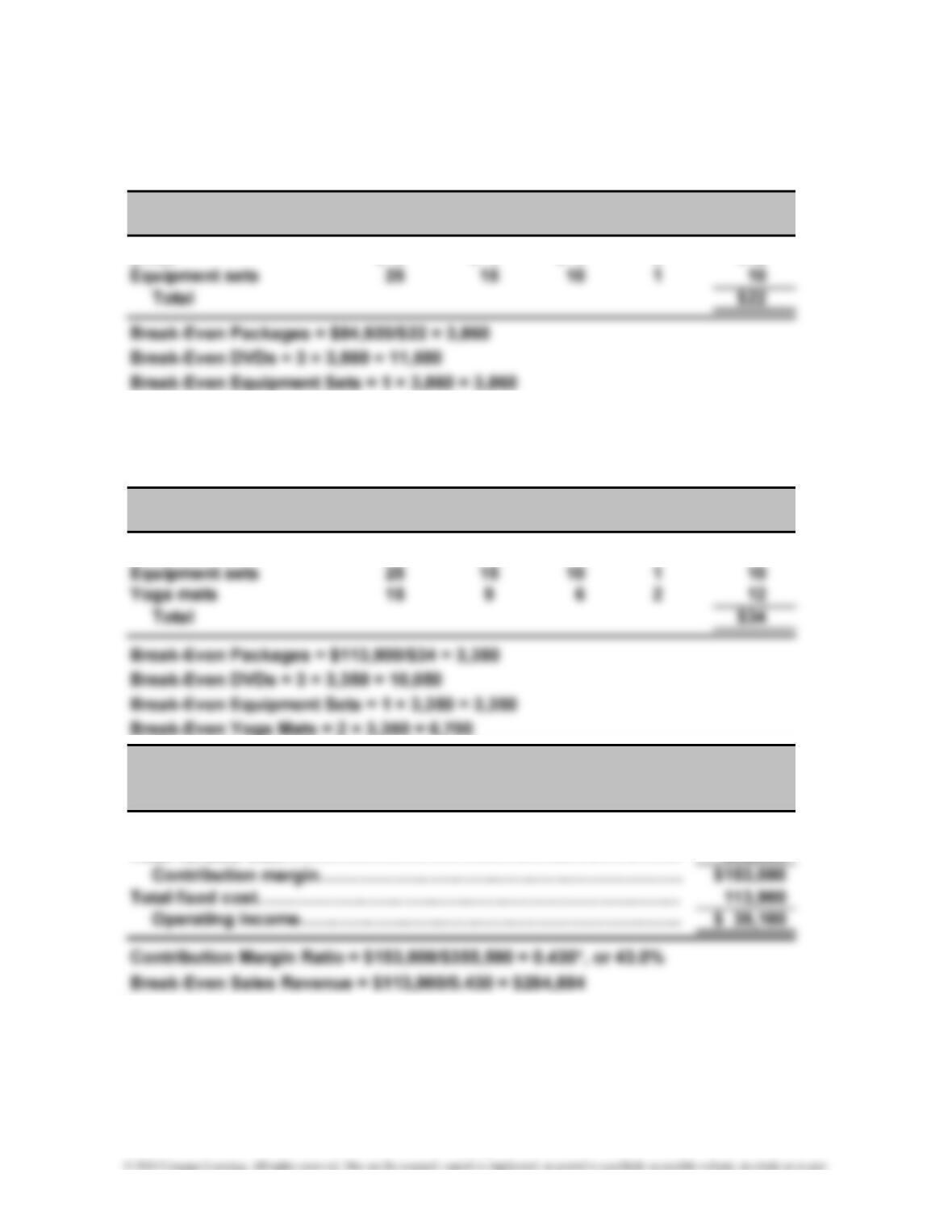

E 4-32

1. Sales mix is 3:1 (three times as many DVDs are sold as equipment sets).

2. Variable Sales Total

Product Price

–

Cost = CM × Mix = CM

DVDs $ 8 $ 4 $ 4 3 $12

E 4-33

1. Sales mix is 3:1:2 (three times as many DVDs will be sold as equipment sets,

and twice as many yoga mats will be sold as equipment sets).

2. Variable Sales Total

Product Price

–

Cost = CM × Mix = CM

DVDs $ 8 $ 4 $ 4 3 $12

3.

Sales……………………………………………………………………………

…

Total variable cost……………………………………………………………

*Rounded

4. Margin of Safety = $355,500 – $264,884 = $90,616

Cherry Blossom Products Inc.

Income Statement

For the Coming Year

$355,500

202,500

4-14

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-34

1. Sales mix is 4:10:1 (four times as many portable grills will be sold as smokers,

and 10 times as many stationary grills will be sold as smokers).

2. Variable Sales Total

Product Price

–

Cost = CM × Mix = CM

Portable $ 90 $ 45 $ 45 4 $180

3.

Sales………………………………………………………………………

…

Total variable cost………………………………………………………

…

Income Statement

For the Coming Year

Texas-Q Company

$13,050,000

8,100,000

4-15

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-35

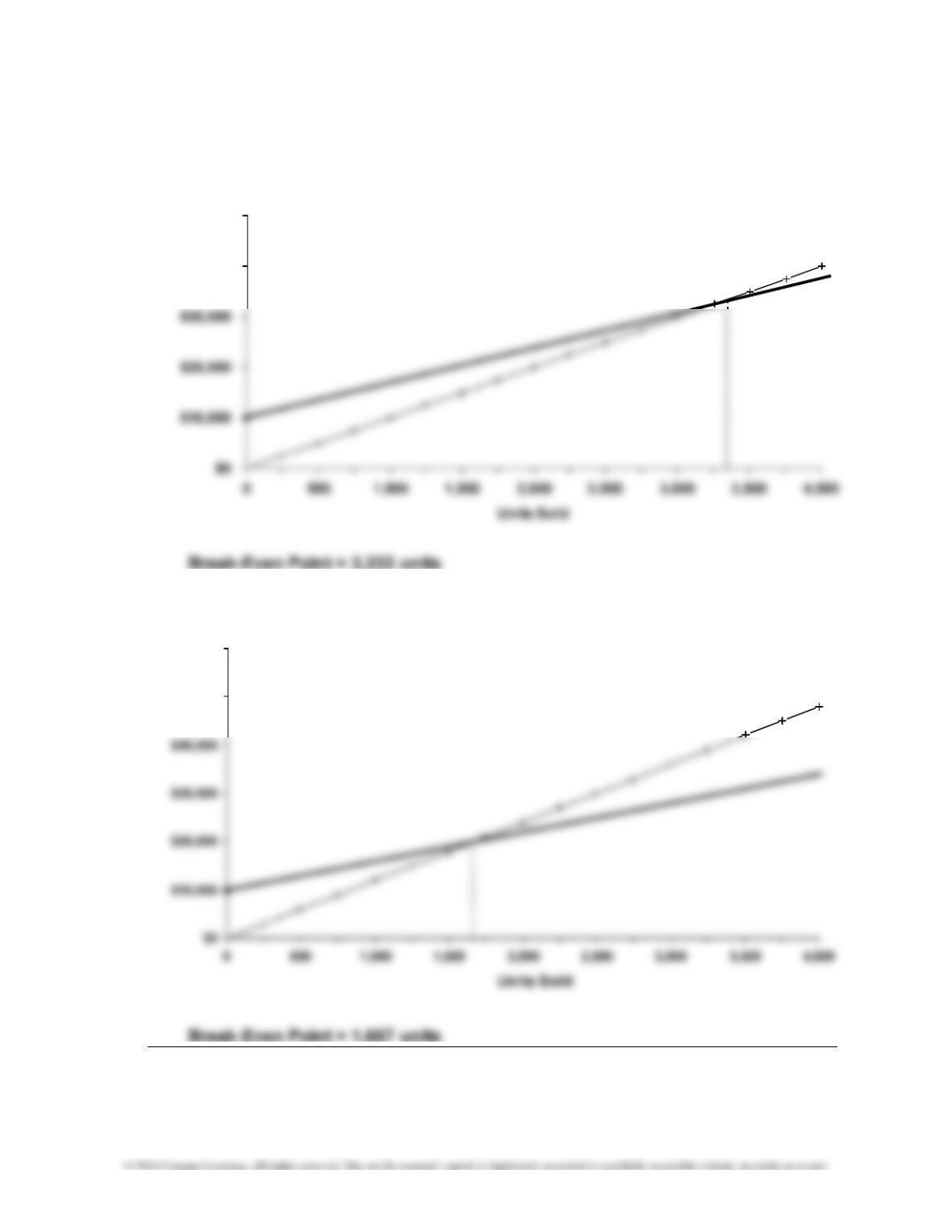

1.

2. a. Fixed cost increases by $5,000:

$25,000

$30,000

$35,000

$30,000

$35,000

$40,000

4-16

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool

E 4-35 (Continued)

2. b. Unit variable cost increases to $7:

2. c. Unit selling price increases to $12:

$50,000

$60,000

$40,000

$50,000

4-17