CHAPTER 9 Profit Planning

P 9-51 (Continued)

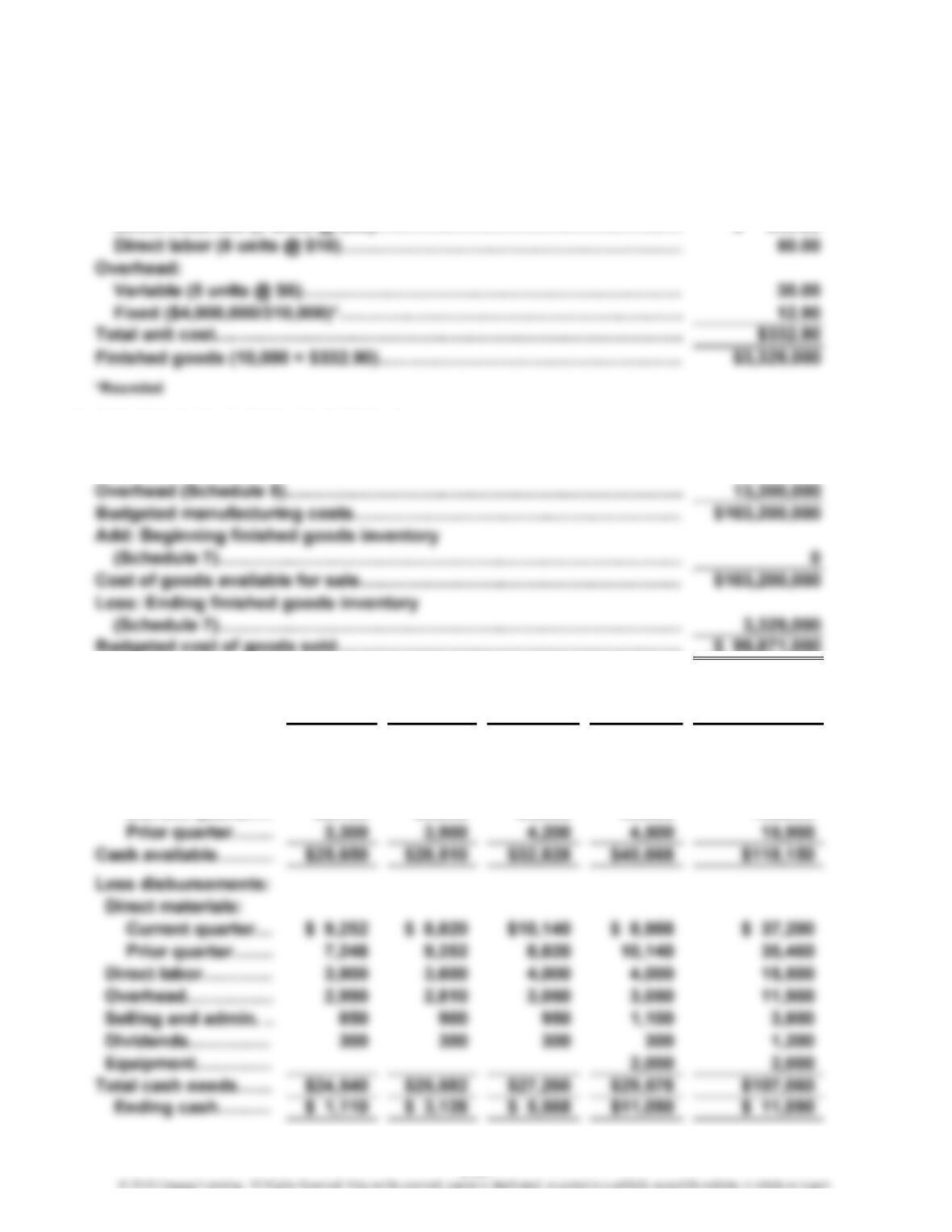

7. Schedule 7: Ending Finished Goods Inventory Budget

Unit cost computation:

Direct materials (3 units @ $80)……………………………………………

…

$ 240.00

8. Schedule 8: Cost of Goods Sold Budget

Direct materials used (Schedule 3)……………………………………………

…

$ 74,400,000

Direct labor used (Schedule 4)…………………………………..……………

…

15,500,000

9. Cash Budget (in thousands)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Beginning cash……

…

$ 250 $ 1,110 $ 3,128 $ 5,568 $ 250

Collections:

Credit sales:

Current quarter… 22,100 23,800 25,500 30,600 102,000

9-32

…

P 9-51 (Continued)

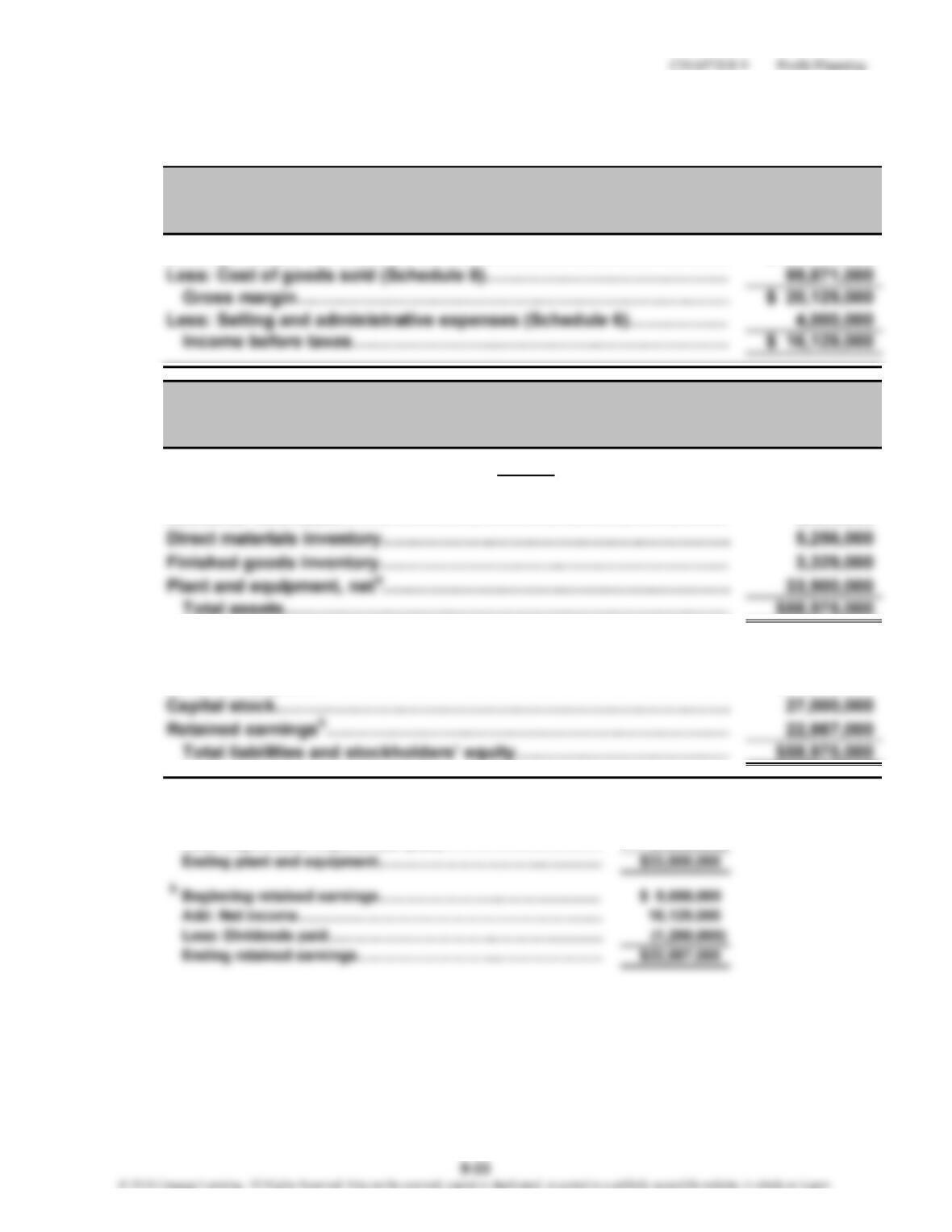

10.

Pro Forma Income Statement

Sales (Schedule 1)…………………………………..………………………

…

$120,000,000

…

11.

Cash……………………………………………………………………………

…

$11,090,000

Accounts receivable………………………………….……………………… 5,400,000

Total assets…………………………………………………………………

…

$58,975,000

Accounts payable……………………………………………………………

…

$ 8,988,000

Beginning plant and equipment $33,500,000

Add: New equipment………………………………………………… 2,000,000

Less: Depreciation expense (for year)……………………………

…

(1,600,000)

a

Liabilities and Stockholders’ Equity

Assets

Optima Company

For the Year Ending December 31, 2014

Optima Company

December 31, 201

4

Pro Forma Balance Sheet

CHAPTER 9 Profit Planning

P 9-52

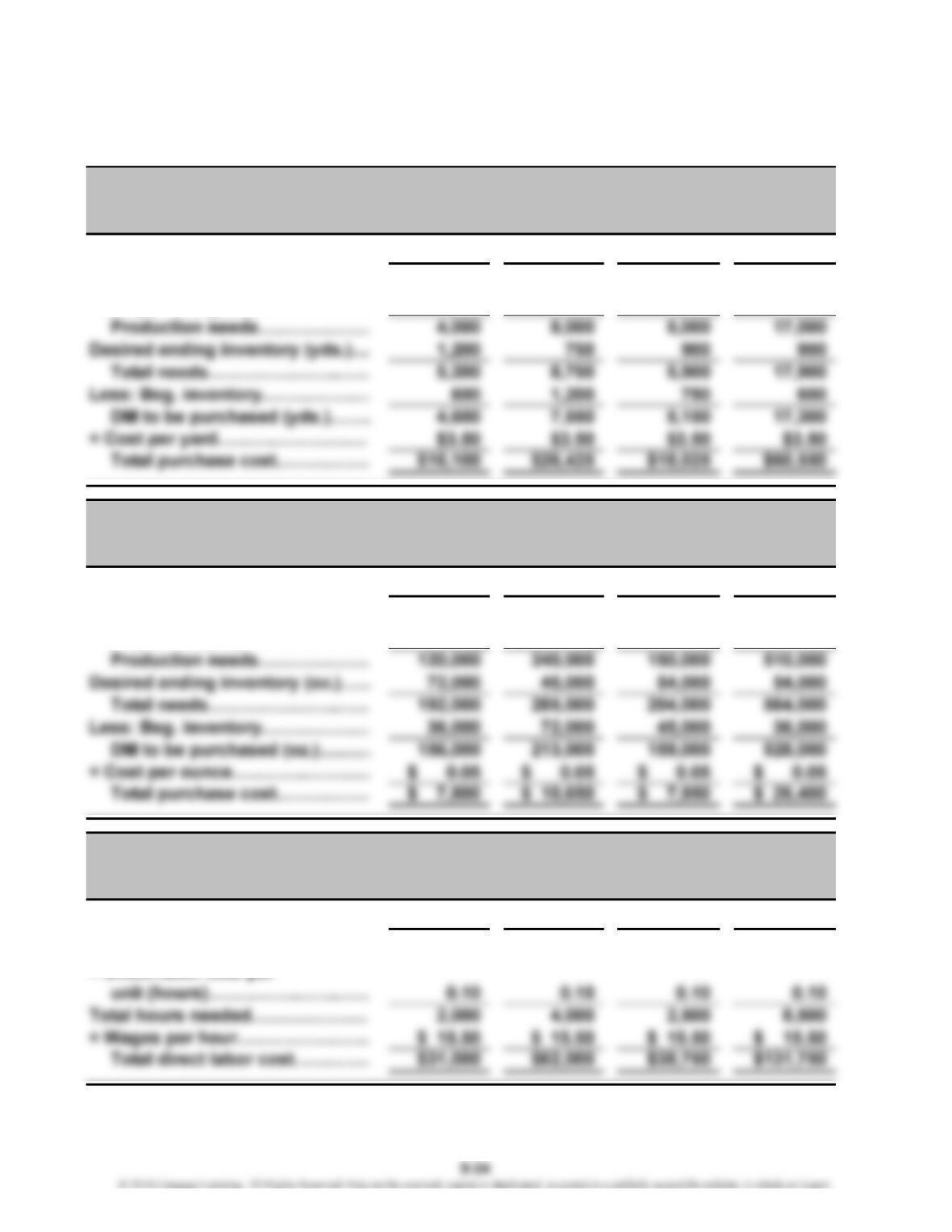

1.

October Novembe

r

December Total

Units to be produced……………… 20,000 40,000 25,000 85,000

× DM per unit (yds.)………………

…

0.20 0.20 0.20 0.20

2.

October Novembe

r

December Total

Units to be produced……………… 20,000 40,000 25,000 85,000

× DM per unit (oz.)…………………. 6666

3.

October Novembe

r

December Total

Units to be produced……………… 20,000 40,000 25,000 85,000

× Direct labor time per

For the Fourth Quarter

Purchase Budget for Fabric

For the Fourth Quarter

Willison Company

Willison Company

Purchase Budget for Polyfiberfill

For the Fourth Quarter

Willison Company

Direct Labor Budget

P 9-53

1.

August September

Cash sales:

($75,000 × 0.75)….…………………………………..………

…

$56,250

…

…

*Check collections for:

(0.25 × $75,000)….…………………………………..…

…

$18,750

(0.25 × $80,000)….…………………………………..…

…

$20,000

…

…

…

…

July August September

2. a. Revised cash sales estimates:

($60,000 × 1.20 × 0.05)…………………..

…

$ 3,600

($75,000 × 1.20 × 0.05)…………………..

…

$ 4,500

($80,000 × 1.20 × 0.05)…………………..

…

$ 4,800

…

…

…

Schedule of Cash Receipts

9-35

CHAPTER 9 Profit Planning

P 9-53 (Continued)

3. August September

Cash sales:

($90,000 × 0.05)….…………………………………..……

…

$ 4,500

($96,000 × 0.05)….…………………………………..……

…

$ 4,800

9-36

CHAPTER 9 Profit Planning

Case 9-54

Answers will vary.

Case 9-55

1.

Cash collections and cash available*…………………………………………

…

$21,360

Less cash disbursements:

Salaries………………………………………………………………………

…

$12,700

Benefits………………………………………………………………………

…

1,344

Building lease………………………………………………………………

…

1,500

*Total revenues for a month:

Fillings ($50 × 90)…………………………

…

$ 4,500

Crowns ($300 × 19)………………………… 5,700

…

Dr. Roger Jones

Cash Budget

CASES

9-37

…

CHAPTER 9 Profit Planning

Case 9-55 (Continued)

2. Dr. Jones must either increase revenues to make up the deficiency or cut costs or a

combination of the two. Three possible approaches are outlined as follows:

a. Extend office hours so that a total of 40 hours are worked each week. This could

increase revenues by as much as $5,340. Based on a four-week month, the current

revenue earned per hour is $166.88($21,360/128). Thus, the total revenue increase

Approach 1 carries with it some risk. Increasing office hours may not increase

business. If business does not increase as expected, the cash flow problems

could be aggravated rather than relieved. The likelihood of increasing business

would be increased if the additional hours are offered in the early evening instead

9-38

CHAPTER 9 Profit Planning

Case 9-55 (Continued)

Cash collections and cash available ($21,360 + $5,340)………………..

.

$26,700

Less cash disbursements:

Interest payments…………………………………………………………

…

500

Miscellaneous……………………………………………………………… 200

Total cash needs………………………………………………………………

…

$26,560

Excess cash available over needs…………………………………………

…

$ 140

*Dental supplies, utilities, and lab fees are variable expenses. The proportion of total variable

expenses of each is:

%

Dental supplies $1,200 18.2%

b. Cut one dental assistant, eliminate the salary to Mrs. Jones and the

activities she does, and cut Dr. Jones’s salary back by $1,000 per month:

The savings are as follows:

…

Dr. Roger Jones

Revised Cash Budget

CHAPTER 9 Profit Planning

Case 9-55 (Continued)

Although this achieves the savings, the solution may not be feasible. The solution

depends to a large extent on how well the Jones family can do with a $2,000 per

c. A third possibility is to increase the fees charged for the various dental services

Assuming a variable cost ratio of 31% (from the first approach), the increase in

revenues needed to cover the $2,900 deficiency can be computed as follows:

This increase would call for fees to increase an average of 19.7%. Whether this

increase is possible or not depends to some extent on how Dr. Jones’s charges

compare with other dentists in the area. If some increase is possible, then the

increase could be combined with elements of the other two approaches, (e.g., a

Case 9-56

1. Linda’s behavior is not ethical. In the budgeting process, she is deliberately

misrepresenting the capabilities of her division for personal gain. To ensure that she

CHAPTER 9 Profit Planning

Case 9-56 (Continued)

2. There are few, if any, legitimate reasons for deferring the closing of sales. Thus, if a

marketing manager was asked to engage in this behavior, the first response must

3. It would be hard to go against a common practice that seems to have the approval

of the plant managers. The widespread knowledge of the practice may even suggest

that higher-level management is aware of it and essentially condones the practice—or

4. This violates the IMA’s Statement of Ethical Professional Practice. A management

accountant is obligated to report information fairly and objectively and to disclose all

information that can be expected to influence a user’s understanding of accounting