CHAPTER 7 Activity Based Costing and Management

P 7-54

1. Plantwide Rate = $990,000/440,000 DLHs = $2.25 per DLH

Overhead cost per unit:

Model A: ($2.25 × 140,000)/10,000 units = $31.50

Model B: ($2.25 × 300,000)/100,000 units = $6.75

Activity rates:

Driver

2. Overhead assignment: Model A Model B

Setups:

$2,700 × 40…………………………………

…

$108,000

$2,700 × 60…………………………………

…

$162,000

Inspections:

3. Departmental rates:

Overhead cost per unit:

4. A common justification is to use machine hours for machine-intensive departments

and labor hours for labor-intensive departments. Using activity-based costs as the

Activity Activity Rate

7-19

CHAPTER 7 Activity Based Costing and Management

P 7-55

1. Labor and gasoline are driver tracing.

Labor (0.75 × $120,000)…………………

…

$ 90,000 Time = Resource Driver

2. Plantwide Rate = $600,000/20,000 direct labor hours

= $30 per DLH

Unit cost: Basic Deluxe

3. Activity rates:

Maintenance: $114,000/4,000 = $28.50 per maintenance hour

Engineering: $120,000/6,000 = $20 per engineering hour

Unit cost: Basic Deluxe

Prime costs……………………………

…

$3,200,000 $3,200,000

Overhead:

Maintenance:

CHAPTER 7 Activity Based Costing and Management

P 7-55 (Continued)

Setting up:

$53.33 × 250……….…………….………

…

13,333

$53.33 × 500……….…………….………

…

26,665

Paying suppliers:

$40 × 250……….…………….…………

…

10,000

$40 × 500……….…………….…………

…

20,000

4. Consumption ratios: Basic Deluxe

Maintenance……………….…………….

…

0.25 0.75

Engineering………………….……………. 0.25 0.75

5. When products consume activities in the same proportion, the activities with the

same proportions can be combined into one pool. This is so because the pooled

*

CHAPTER 7 Activity Based Costing and Management

P 7-55 (Continued)

Pool 1:

Pool 2:

Materials handling……………………………………

…

$120,000

Pool 3:

Purchasing……………………………………………

…

$ 60,000

Receiving………………………………………………

…

40,000

Pool 4:

Providing space………………………………………

…

$20,000

7-22

…

CHAPTER 7 Activity Based Costing and Management

P 7-56

1. The cost of supervision is computed as follows:

Salary of supervisor (Direct)…………………………

…

$ 80,000

Salary of secretary (Direct)…………………………… 35,000

2. First, the cost of the secondary activity (supervision) must be assigned to

the primary activities (various nursing care activities) that consume it

(the driver is the number of nurses):

Maternity nursing care assignment:

Nursing care:

$1,270,000/50,000 = $25.40 per nursing hour

Finally, the cost per patient day type can be computed:

Patient Daily Rate

Normal…………………………………

…

$213.50

a

7-23

…

CHAPTER 7 Activity Based Costing and Management

P 7-56 (Continued)

3. The laundry department cost would increase the total cost of the maternity

department by $115,200 (240,000/1,250,000 × $600,000). This would

increase the cost per patient day by $11.52 ($115,200/10,000). The activity

7-24

CHAPTER 7 Activity Based Costing and Management

P 7-57

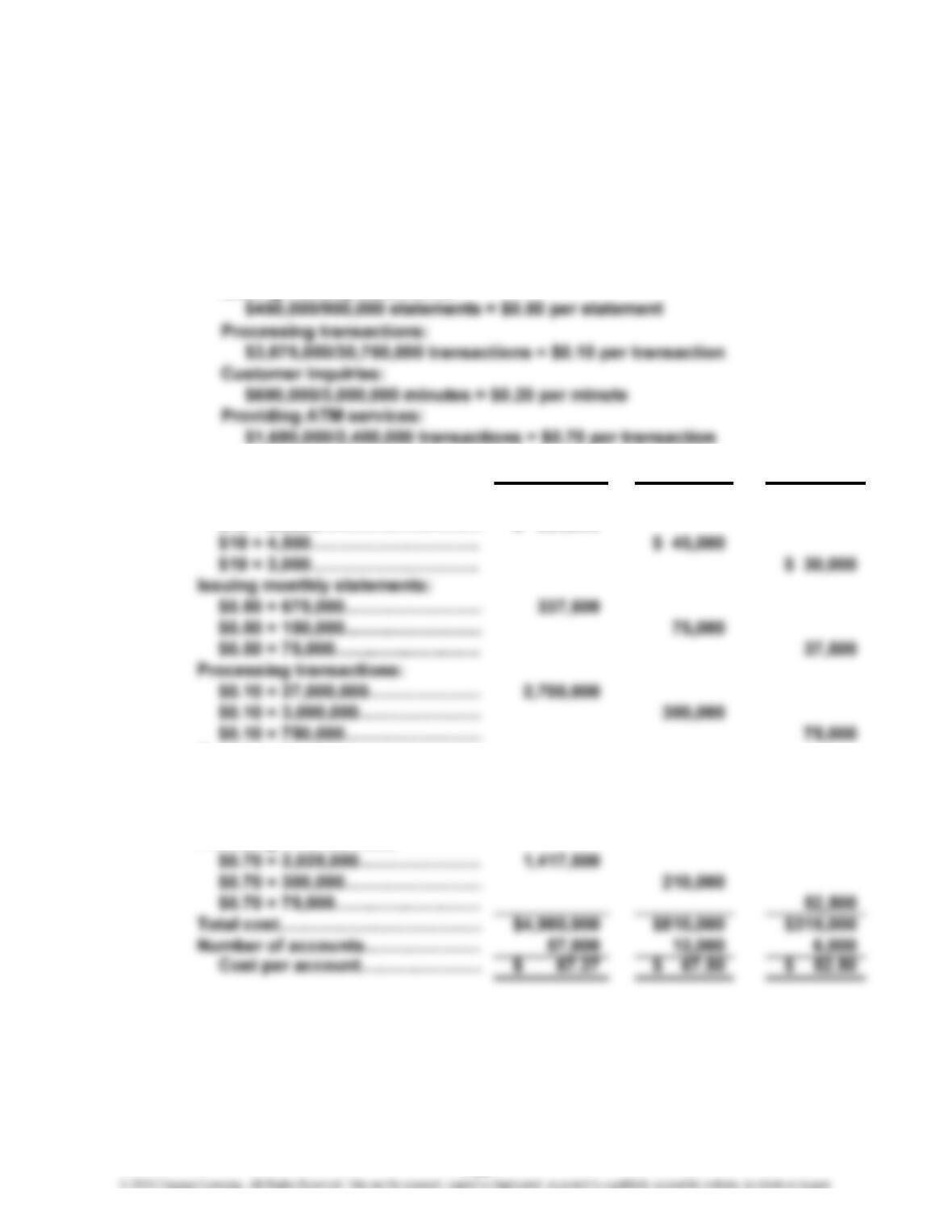

1. Cost per Account = $6,105,000/75,000 accounts = $81.40

Average Fee per Month = $81.40/12 months = $6.78

2. Activity rates:

Opening and closing accounts:

$300,000/30,000 accounts = $10 per accoun

t

Issuing monthly statements:

Costs assigned: Low Medium High

Opening and closing:

$10 × 22,500………………………

…

$ 225,000

…

…

…

Customer inquiries:

$0.20 × 1,500,000………………… 300,000

$0.20 × 900,000…………………

…

180,000

$0.20 × 600,000…………………

…

120,000

Providing ATM services:

…

7-25

CHAPTER 7 Activity Based Costing and Management

P 7-57 (Continued)

3. Average profit per account: $90.00 – $81.40 = $8.60

ABC profit measure:

4. First, calculate the profits from loans, credit cards, and other products by

customer category (using ABC data). Next, compare 50% of the cross-sales

P 7-58

1. GAAP mandates that all nonmanufacturing costs be expensed during the

period in which they are incurred. GAAP is the most likely cause of the practice.

The limitations of GAAP-produced information for cost management should be

CHAPTER 7 Activity Based Costing and Management

P 7-58 (Continued)

2. The average order-filling cost per unit produced is computed as follows:

$9,000,000/180,000,000* units = $0.05 per uni

t

*(600 × 100,000) + (1,000 × 60,000) + (1,500 × 40,000) = 180,000,000

Thus, order-filling costs are about 6 to 10% of the selling price, clearly not a

3. With the pricing incentive feature, the average order size has been increased

to 2,000 units for all three product families. The number of orders now

processed can be calculated as follows:

CHAPTER 7 Activity Based Costing and Management

P 7-58 (Continued)

Customers were placing smaller and more frequent orders than necessary.

They were receiving a benefit without being charged for it. By charging for

the benefit and allowing customers to decide whether the benefit is worth

Competitive advantage is created by providing the same customer value

for less cost or better value for the same or less cost. By reducing the

cost, Grundvig can increase customer value by providing a lower price

(decreasing customer sacrifice) or by providing some extra product

features without increasing the price (increasing customer realization,

holding customer sacrifice constant). This is made possible by the

decreased cost of producing and selling the bolts.

7-28

CHAPTER 7 Activity Based Costing and Management

P 7-59

1. Supplier cost:

First, calculate the activity rates for assigning costs to suppliers:

Next, calculate the cost per engine by supplier:

Supplier cost:

Watson Johnson

Purchase cost:

$900 × 18,000………………………….…

…

$16,200,000

$1,000 × 4,000………………………….… $4,000,000

Replacing engines:

…

2. In the short run, buy 20,000 from Johnson and 2,000 from Watson. In the

long run, one possibility is to encourage Watson to increase its quality

7-29

CHAPTER 7 Activity Based Costing and Management

P 7-60

1. Activity-based management is a system-wide, integrated approach that focuses

management’s attention on activities. It involves two dimensions: a cost dimension

and a process dimension. Key elements in activity management are identifying

2. Setup………………………………………………

…

$125,000

Materials handling………………………………

…

180,000

Inspection…………………………………………

…

122,000

7-30

CHAPTER 7 Activity Based Costing and Management

P 7-60 (Continued)

Units produced and sold………………………………… 120,000 *

Potential unit cost reduction……………………………

…

$7.10 **

*$1,920,000/$16 (Total Cost/Unit Cost)

** $852,000/120,000 = $7.10

The consultant’s estimate of cost reduction was on target. Per-unit costs

can be reduced by at least $7, and further reductions may be possible if

improvements in value-added activities are possible.

We have identified $7.10 per unit of potential cost reduction. We don’t know

3. Unit cost to maintain sales = $14 – $4 = $10

Unit cost to expand sales = $12 – $4 = $8

4. Total potential reduction:

$ 852,000 (from Requirement 2)

150,000 (by automating)

$1,002,000

÷ Units………………………………

…

120,000

Unit savings………………………… $ 8.35

Costs can be reduced by at least $7, enabling the company to maintain

CHAPTER 7 Activity Based Costing and Management

P 7-60

(

Concluded

)

5. Current:

Sales………………………………………

…

$ 2,160,000 ($18 × 120,000 units)

Costs………………………………………

…

(1,920,000)

Income…………………………………

…

$ 240,000

P 7-61

1. Nonvalue-added usage and costs, 2013:

Nonvalue Usage Nonvalue Cost

AQ*

V

AQ**

A

Q – VAQ (AQ – VAQ)SP

2. Expected values for the coming year (2014):

Materials: EQ = 480,000 + 0.60(120,000) = 552,000 pounds

Engineering: EQ = 27,840 + 0.60(20,160) = 39,936 engineering hours

Excess Excess

Nonvalue Usage Nonvalue Cost

AQ EQ*

A

Q – EQ (AQ – EQ)SP

***

*

…

…

…

…

…

…

CHAPTER 7 Activity Based Costing and Management

P 7-61 (Concluded)

The company failed to meet the materials standard but beat the engineering

standard. The engineering outcome is of particular interest. The actual usage

of the engineering resource is 35,400 hours, and activity availability is 48,000.

P 7-62

1. Theoretical Velocity = 90,000/12,000 hours = 7.5 telescopes per hour

Theoretical Cycle Time = 60/7.5 telescopes = 8 minutes per telescope

P 7-63

a. Prevention (SD) i. Detection (SD)

b. Prevention (SD) j. External failure (societal)

7-33

CHAPTER 7 Activity Based Costing and Management

Case 7-64

1. Shipping and warehousing costs are currently assigned using tons of paper

produced, a unit-based measure. Many of these costs, however, are not driven by

2. The new method proposes assigning the costs of shipping and warehousing

separately for the low-volume products. To do so requires three cost assignments:

receiving, shipping, and carrying. The cost drivers for each cost are tons processed,

items shipped, and tons sold.

Pool rate, receiving costs:

CASES

CHAPTER 7 Activity Based Costing and Management

Case 7-64 (Continued)

3. Profit analysis:

Revised profit per ton (LLHC):

Loss…………………………………………………………………………

…

$ (35.41)

Original profit per ton:

The revised profit, reflecting a more accurate assignment of shipping and

warehousing costs, presents a much different picture of LLHC. The product is,

in reality, losing money for the company. Its earlier apparent profitability was

attributable to a subsidy being received from the high-volume products (by

spreading the special shipping and handling costs over all products, using

tons produced as the cost driver). The same effect is also true for the other

low-volume products. Essentially, the system is understating the handling

costs for low-volume products and overstating the cost for high-volume

products.

4. The decision to drop some high-volume products and emphasize low-volume

products could clearly be erroneous. As LLHC has demonstrated, its apparent

profitability is attributable to distorted cost assignments. A significant change in

5. Ryan’s strategy changed because his information concerning the individual

products changed. Apparently, the accounting system was undercosting the

CHAPTER 7 Activity Based Costing and Management

Case 7-65

1. Disagree. Chuck is expressing an uninformed opinion. He has not spent the

2. and 3.

At first glance, it may seem strange to even ask if Chuck’s behavior is unethical.

After all, what is unethical about expressing an opinion, albeit uninformed? While