CHAPTER 6 Process Costing

P 6-50 (Continued)

Transferred

Costs accounted for: Out Total

Goods transferred out

P 6-51

1. Units to account for: Units accounted for:

Units in beginning WIP……

…

15,000 Transferred out……… 45,000

2. Equivalent

Units

…

5. To assign costs to spoiled units, they should appear as an item in the

equivalent units schedule:

Equivalent

Units

Transferred out…………………………………………………..………………

…

42,500

Work in Process

Ending

6-19

CHAPTER 6 Process Costing

P 6-51 (Continued)

The cost per equivalent unit is the same calculated without spoilage.

P 6-52

Units to account for: Units accounted for:

Units in beginning WIP……

…

24,000 Units completed………

…

70,000

Costs to account for:

Costs in beginning WIP………………………..………………………………

…

$285,520

Costs added by department…………………..………………………………

…

638,480

Total costs to account for…………………………………………………

…

$924,000

…

COST INFORMATION

Millie Company

Assembly Department

For the Month of June

(Weighted Average Method)

UNIT INFORMATION

Production Report

P 6-53

Units to account for: Units accounted for:

Units in beginning WIP……

.

24,000 Started and completed…

…

46,000

Units started……..…………

…

56,000 From beginning WIP……

…

24,000

Costs to account for:

Costs in beginning WIP…………………………..……………………………

…

$285,520

Costs added by department……………………..……………………………

…

638,480

Total costs to account for……………………..……………………………

…

$924,000

*Rounded

UNIT INFORMATION

COST INFORMATION

Millie Company

(FIFO Method)

Assembly Department

Production Report

For the Month of June

6-21

CHAPTER 6 Process Costing

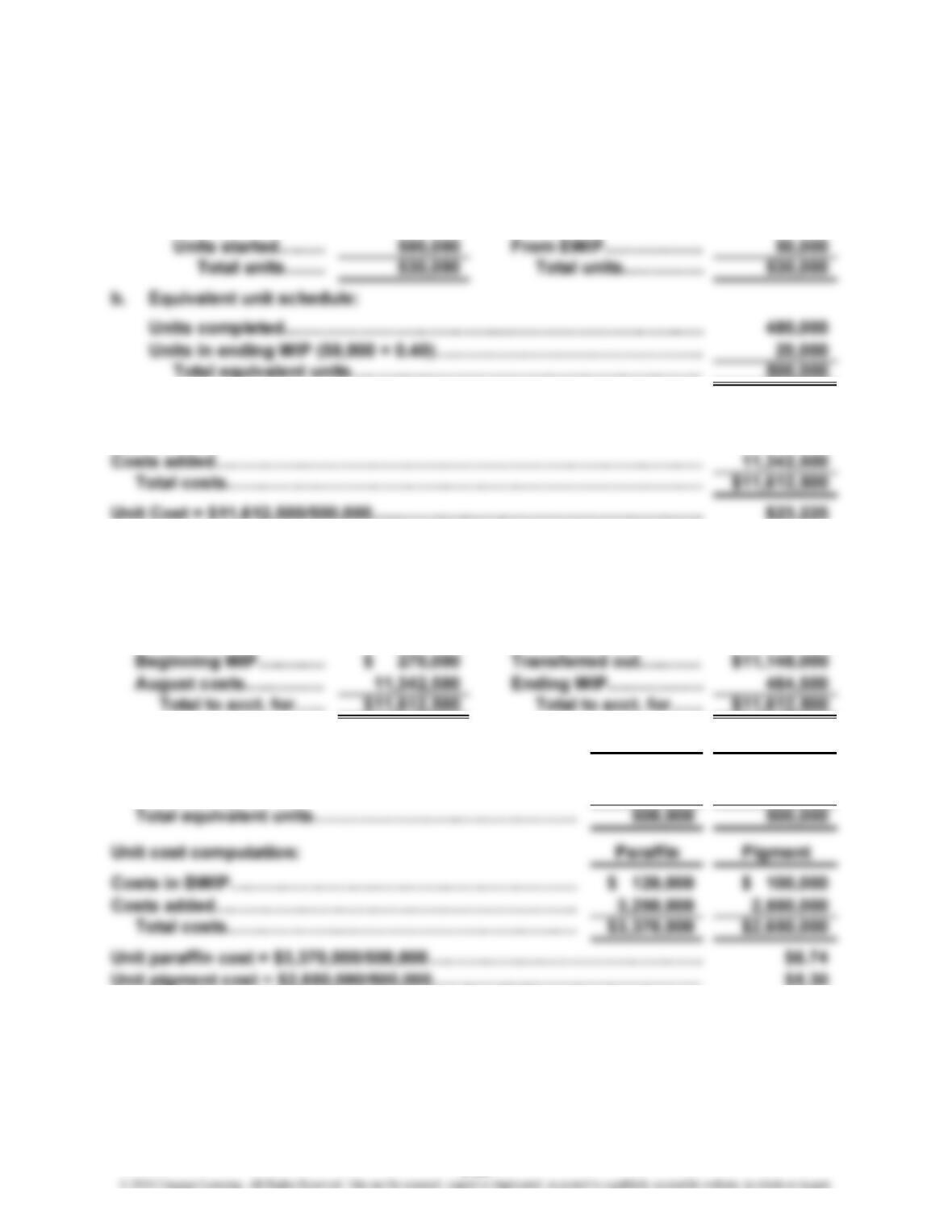

P 6-54

1. a. Physical flow schedule:

Units to account for: Units accounted for:

Units in BWIP……

…

30,000 Units completed………

…

480,000

2. Unit cost computation:

Costs in BWIP………………..……………………………………………………

…

$ 270,000

…

3. Ending work in process (20,000 × $23.225)…………………………………… $464,500

Goods transferred out (480,000 × $23.225)……..…..………………………… $11,148,000

4. Cost reconciliation:

Costs to account for: Costs accounted for:

5. Equivalent unit schedule: Paraffin Pigment

Units completed………………..………………………………

…

480,000 480,000

Units in ending WIP……………………..……………………… 20,000 20,000

6-22

CHAPTER 6 Process Costing

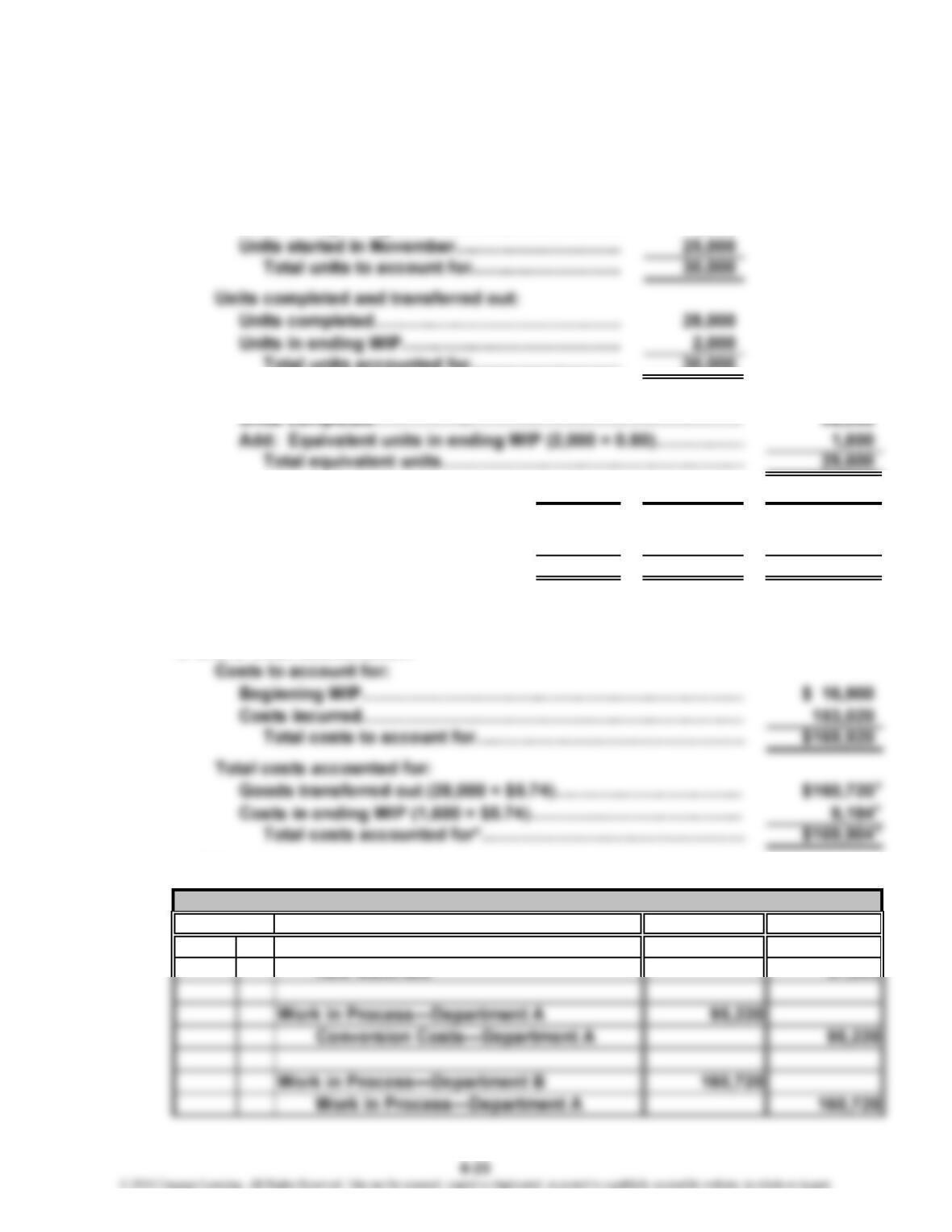

P 6-55

1. Department A

a. Physical flow schedule:

Units in beginning WIP…………..………………

…

5,000

Total units accounted for……………..………

…

30,000

b. Equivalent unit calculation:

c. Costs charged to the department: Materials Conversion Total

Beginning WIP…………..……………… $10,000 $ 6,900 $ 16,900

Incurred during November…………..

…

57,800 95,220 153,020

Total costs…………..………………

…

$67,800 $102,120 $169,920

Unit cost calculation:

Unit cost = $169,920/29,600………….…..…………………………

…

$5.74

d. and e. Cost reconciliation:

*Rounded

2.

Credit

Work in Process—Department A

Raw Materials 57,800

Journal

Date Description

57,800

Debit

CHAPTER 6 Process Costing

P 6-55 (Continued)

Answers may vary, but could (or should) include:

Using a conversion cost control account is more commonly used because direct

P 6-56

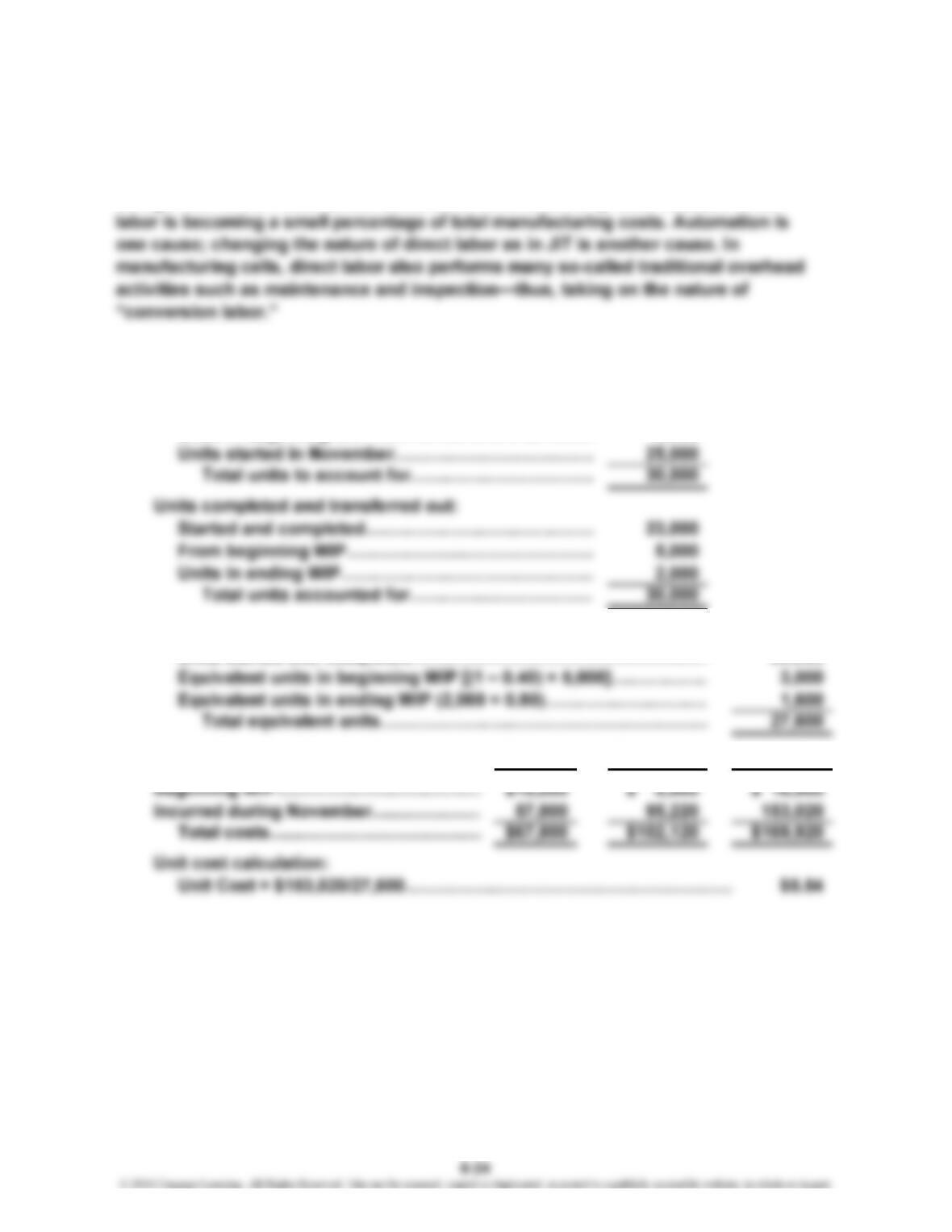

1. Department A

a. Physical flow schedule:

Units in beginning WIP……………..…………………

…

5,000

b. Equivalent unit calculation:

Units started and completed……..……………………………………

…

23,000

c. Costs charged to the department: Materials Conversion Total

CHAPTER 6 Process Costing

P 6-56 (Continued)

d. and e. Cost reconciliation:

Costs of unit started and completed (23,000 × $5.54)……………….

…

$127,420

Costs of unit in beginning WIP:

*Difference due to rounding.

2.

Debit Credit

Work in Process—Department A

Raw Materials 57,800

Journal

Date Description

57,800

6-25

CHAPTER 6 Process Costing

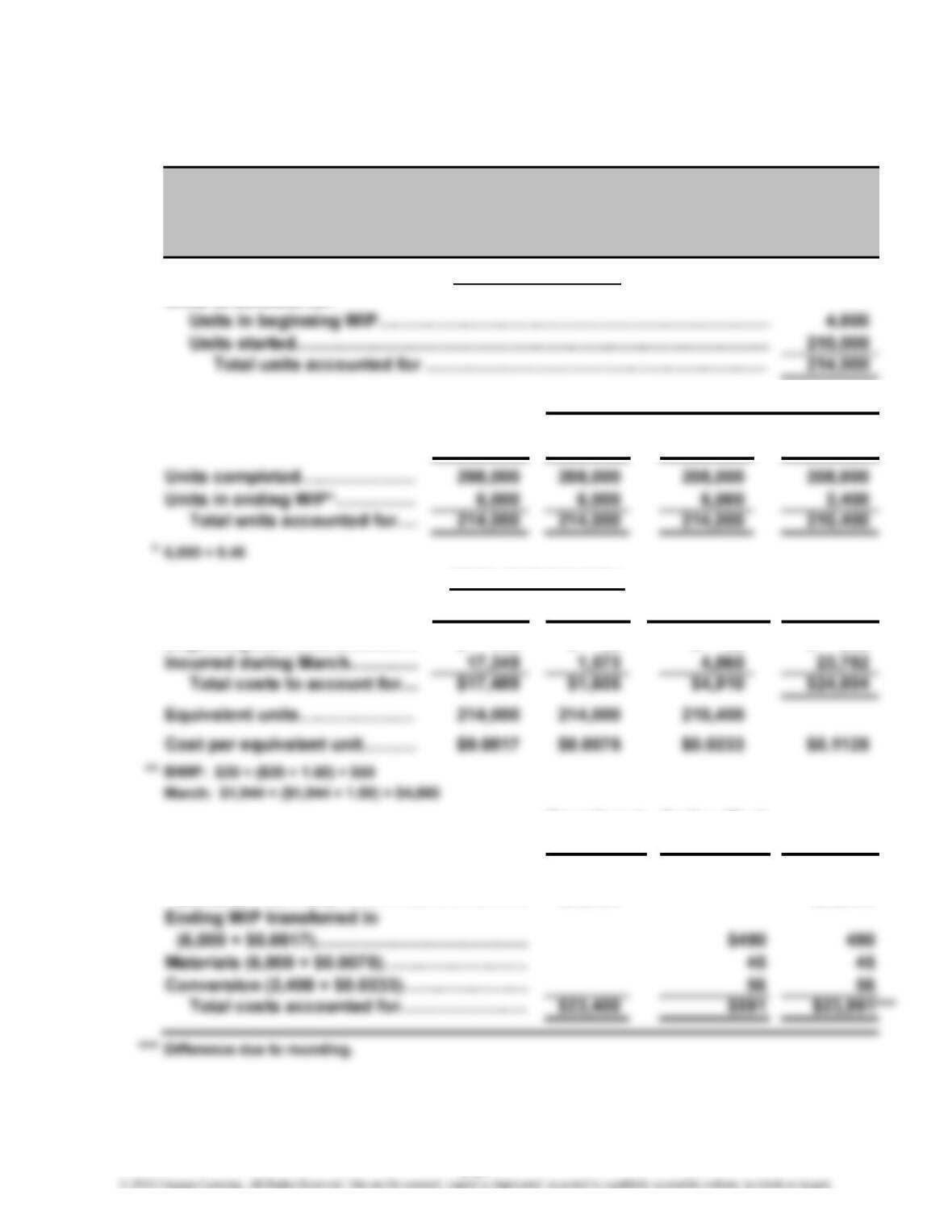

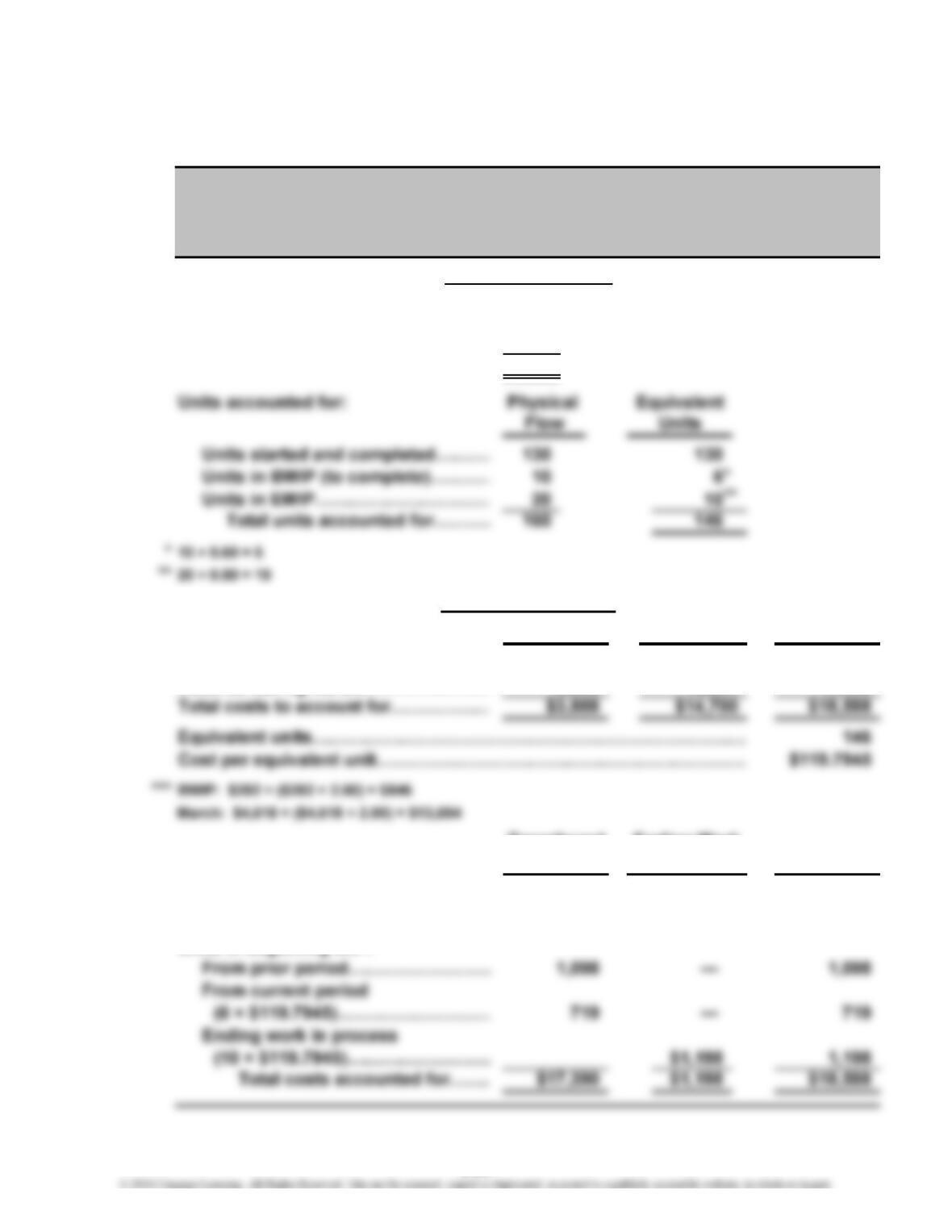

P 6-57

1.

Units to account for:

Units in beginning WIP……………………………………………………… 10

Costs to account for: Materials Conversion* Total

Beginning WIP……………………………

…

$ 252 $ 846 $ 1,098

Transferred Ending Work

Costs accounted for: Out Total

Goods transferred out

in Process

Benson Pharmaceuticals

Mixing Department Production Report

For the Month of March

(Weighted Average Method)

UNIT INFORMATION

COST INFORMATION

6-26

CHAPTER 6 Process Costing

P 6-57 (Continued)

2.

Units to account for:

Units accounted for: Flow Trans. In Materials Conversion

Costs to account for: Trans. In Materials Total

Beginning WIP…………………

…

$ 140 $ 32 $ 50 $ 222

Costs accounted for: Total

Goods transferred out

(208,000 × $0.1125)……………………………

…

$23,400 $23,400

Out

Transferred Ending Work

in Process

Equivalent Units

COST INFORMATION

Physical

Conversion

UNIT INFORMATION

Benson Pharmaceuticals

Encapsulating Department Production Report

For the Month of March

(Weighted Average Method)

**

6-27

CHAPTER 6 Process Costing

P 6-57 (Continued)

3. Weighted average is easier to use than FIFO because it does not require separate

tracking for units in BWIP. FIFO requires that prior-period work and costs be

accounted for separately. The weighted average method commingles prior-period

6-28

CHAPTER 6 Process Costing

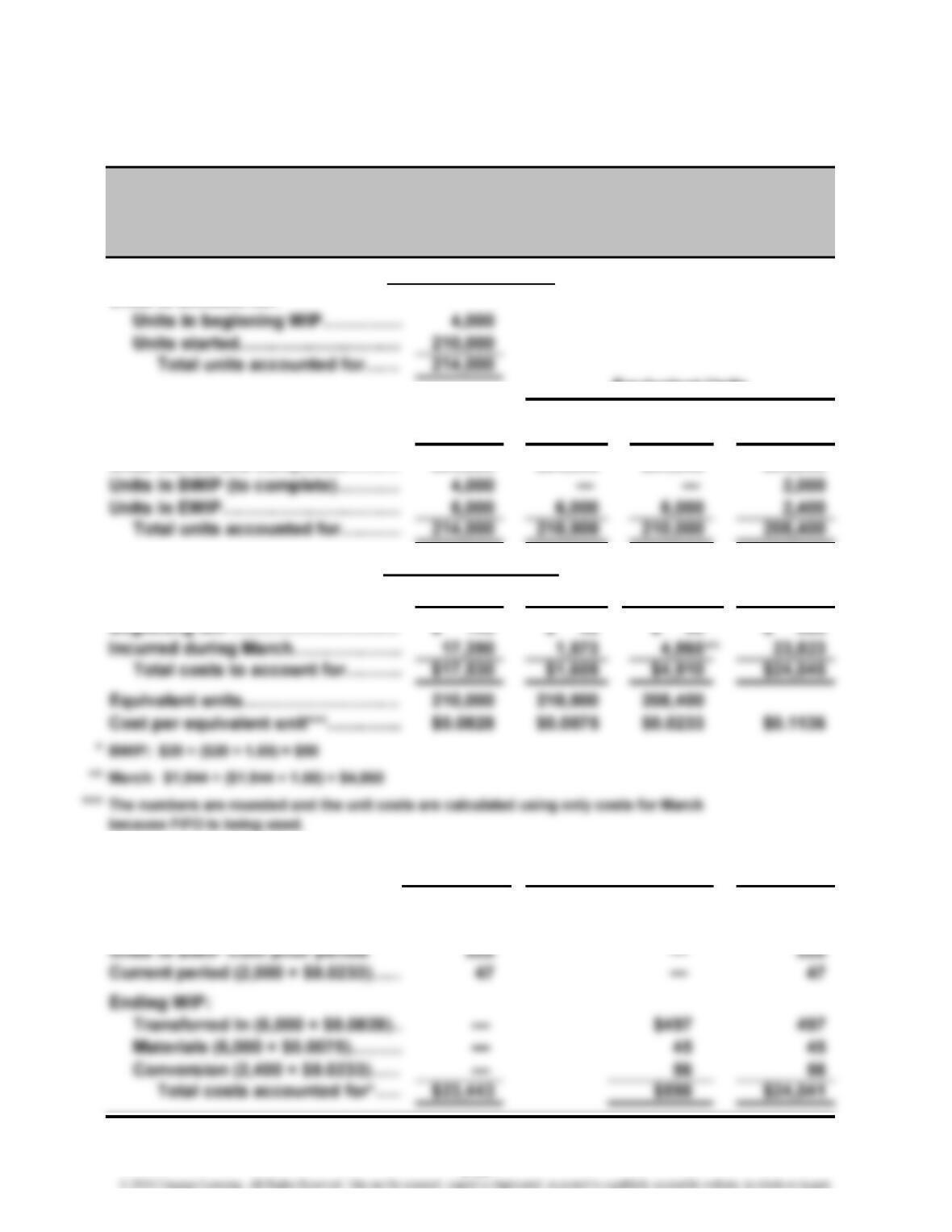

P 6-58

1.

Units to account for:

Units in beginning WIP……………

…

10

Units started…………………………

…

150

Total units ………………………

…

160

Costs to account for: Total

Beginning WIP…………………………… $ 1,098

Incurred during March…………………

…

17,490

Costs accounted for: Total

Units started and completed

(130 × $119.7945)………………………

…

— $15,573

Units in beginning WIP:

Ending Work

Conversion

$ 846

13,854

Materials

$15,573

Out

$ 252

3,636

in Process

Benson Pharmaceuticals

Mixing Department Production Report

(FIFO Method)

COST INFORMATION

UNIT INFORMATION

For the Month of March

Transferred

***

6-29

…

CHAPTER 6 Process Costing

P 6-58 (Continued)

2.

Units to account for:

Physical

Units accounted for: Flow Trans. In Materials Conversion

Units started and completed………

…

204,000 204,000 204,000 204,000

Costs to account for: Trans. In Materials Total

Ending

Costs accounted for: Work in Process Total

Units started and completed

(204,000 × $0.1136)………………… $23,174 — $23,174

*Difference due to rounding.

Transferred

Out

Conversion

COST INFORMATION

Equivalent Units

Benson Pharmaceuticals

UNIT INFORMATION

Encapsulating Department Production Report

(FIFO Method)

For the Month of March

6-30

CHAPTER 6 Process Costing

Case 6-59

1. Unit cost computation:

Physical flow schedule:

Units, beginning work in process…………………………………………

…

0

Direct Conversion

Costs charged to the department: Materials Cost Total

Costs in BWIP………………………………

…

$0$0 $0

Costs added by department*………………

…

114,000 82,201 196,201

Total costs………………………………… $114,000 $82,201 $196,201

*$45,667 + (0.80 × $45,667)

Direct Conversion

Equivalent units calculation: Materials Cost

Units completed………………………………………………

…

2,500 2,500

2. Since conversion activity is the same for both bows, only the materials cost will

differ. Thus, the unit materials cost is computed and then added to the unit

conversion cost obtained in Requirement 1.

Econo Model

…

CASES

Case 6-59 (Continued)

Units completed and transferred out:

Started and completed…………………..……………………………………… 1,500

…

…

…

Direct materials cost charged to the department: Direct

Materials

Costs in beginning work in process……..………………………………………

…

$0

Costs added by department………………..……………………………………… 30,000

Total costs…………………………………..……………………………………

…

$30,000

Equivalent units calculation: Direct

Materials

Units completed……………………………..………………………………………

…

1,500

Add: Equivalent units in ending work in process…………..………………… 100

Total equivalent units…………………………………………..………………

…

1,600

Unit cost calculation:

…

Total units to account for…………………………………..………………

…

1,200

Units completed and transferred out:

Started and completed……………………………………..…………………… 1,000

From beginning work in process…………………………..…………………

…

0

Units, ending work in process……………………………..…………………

…

200

Total units accounted for…………………………………..………………

…

1,200

…

…

6-32

CHAPTER 6 Process Costing

Case 6-59 (Continued)

Equivalent units calculation: Direct

Materials

3. Unit cost for Econo model……………………………..……………………………

…

$ 48.75

Unit cost for Deluxe model…………………………..………………………………

…

100.00

Unit cost for both together……………………………..……………………………

…

$148.75

4. The profitability of the Econo line was being understated by nearly $22 while that of

the Deluxe line was overstated by over $29 producing an erroneous $51 difference

in profitability under the current process-costing system. This easily could be enough

…

CHAPTER 6 Process Costing

Case 6-60

1. Physical flow schedule:

Units, beginning work in process……………………………………………

…

10,000

Units started (transferred in)…………………..………………………………

…

51,000

Total units to account for……………………..…………………………

…

61,000

Units completed and transferred out:

*Assumes that overhead is used in the same proportion as direct labor

Direct Conversion

Equivalent units calculation: Materials Costs

Units started and completed……………………………………

…

40,000 40,000

Units completed from beginning work in process…………… 4,000

*Rounded

Value of ending work in process:

Direct materials (11,000 × $1.70)…..…………..……………………………… $18,700

Conversion costs (6,600 × $8.12)…..…………..……………………………

…

53,592

Total cost of units in ending work in process………………..…………

…

$72,292

Assumptions: Overhead is used at the same rate as direct labor.

…

CHAPTER 6 Process Costing

Case 6-60 (Continued)

2. Units, beginning work in process…………………..……………………………

…

8,000

Units started (transferred in)………………………………………………………

…

50,000

Total units to account for………………………………………………………

…

58,000

Units completed and transferred out:

Direct Conversion Transferred

Equivalent units calculation: Materials Costs In

Units started and completed…..…………………

…

42,000 42,000 42,000

Costs:

Transferred-in cost (50,000 × $9.82)*…………………………

…

$491,000

…

*Assumes that all units transferred out, including those finished from beginning work in process, have

a cost of $9.82 per unit. In essence, this assumes that the unit cost of this period equals the unit cost

of the prior period.

Unit Cost = Unit Direct Materials Cost + Unit Conversion Costs + Unit Tranferred-In

Cost

$16.84

Units, ending work in process:*

CHAPTER 6 Process Costing

Case 6-60 (Continued)

In addition to the same assumptions made for the first department, we had to assume

Case 6-61

1. Gary’s proposal requires Donna to falsify the equivalent unit calculation so that

income and assets can be inflated and reported incorrectly. Falsification of the

2. Donna has an obligation to report Gary to a superior only if an actual ethical problem

exists. If Gary decides that the course of action he is suggesting is not really in his or

the company’s best interests, then no ethical problem exists and no action by Donna

is needed.

3. If Gary insists on his idea of falsification of the division’s reports, Donna should

attempt to resolve the conflict by appealing to Gary’s immediate supervisor (and on

4. In this situation, the ethical dilemma is complicated by two factors: Donna’s age

and a low likelihood of resolution by appealing to higher-level authorities. Donna’s