1. Budgets are the quantitative expressions of plans. Budgets are used to translate the goals

and strategies of an organization into operational terms.

2. Control is the process of setting standards, receiving feedback on actual performance,

and taking corrective action whenever actual performance deviates materially from

planned performance. Budgets are standards, and they are compared with actual costs

and revenues to provide feedback.

5.

A

master budget is the collection of all individual area and activity budgets. Operating

budgets are concerned with the income-generating activities of a firm. Financial budgets

are concerned with the inflows and outflows of cash and with planned capital expenditures.

6. The sales forecast is a critical input for building the sales budget. However, it is not

necessarily equivalent to the sales budget. Upon receiving the sales forecast, management

Profit Planning

9

DISCUSSION QUESTIONS

CHAPTER 9 Profit Planning

11. Participative budgeting is a system of budgeting that gives subordinate managers a say in how the

budgets are established. Participative budgeting fosters creativity and communicates a sense of

responsibility to subordinate managers. It also creates a higher likelihood of goal congruence since

managers have more of a tendency to make the budget’s goals their own personal goals.

12.

A

gree. Individuals who are not challenged tend to lose interest and maintain a lower level of

performance. A challenging, but achievable, budget tends to extract a higher level of performance.

CHAPTER 9 Profit Planning

9-1. d

9-2. e

9-3. c

9-13. b

9-14. d

9-15. a

9-16. a

MULTIPLE-CHOICE QUESTIONS

CHAPTER 9 Profit Planning

CE 9-21

1st Quarter

February March Total

CE 9-22

1st Quarter

February March Total

Sales………………………

…

38,000 50,000 129,000

Desired ending

For the Coming Quarter

Patrick Inc.

Production Budget

41,000

January

January

CORNERSTONE EXERCISES

Patrick Inc.

Sales Budget

For the Coming Quarter

…

CHAPTER 9 Profit Planning

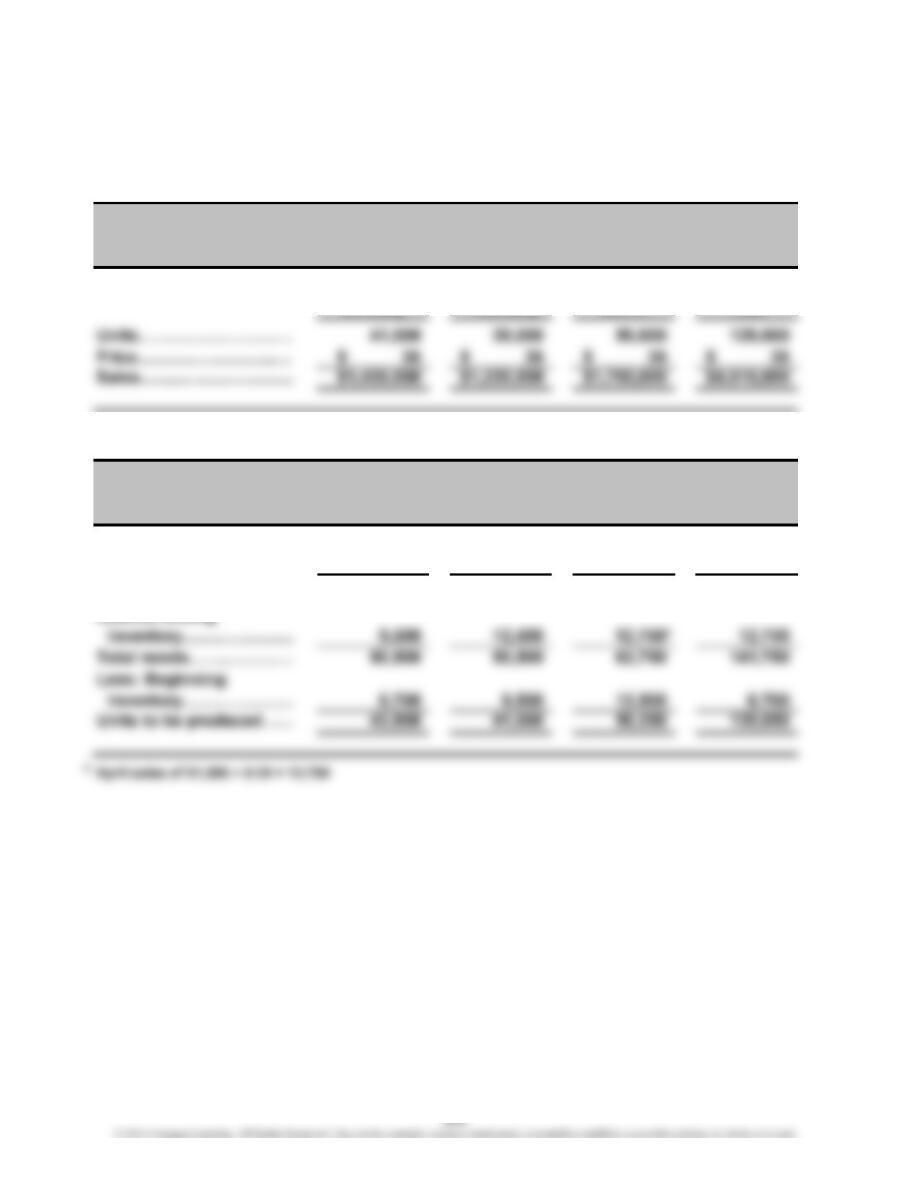

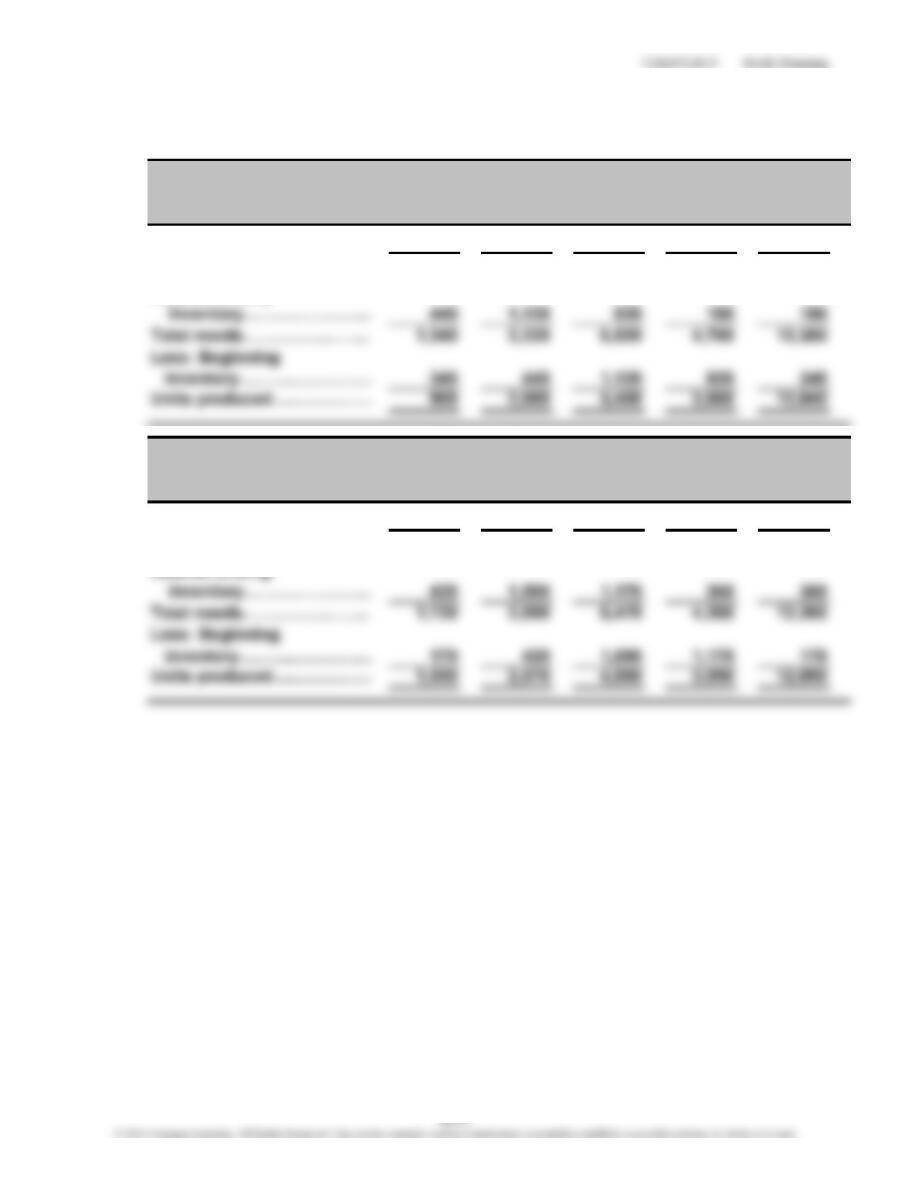

CE 9-23

1. Ending Inventory for December = 0.15 × 5.50 gal. of chemicals × 43,800 units

= 36,135

2. Direct materials purchases budget—chemicals in gallons:

January February

Production in units……………………………………

…

43,800 41,000

× Gallons per unit…………………………………

…

5.5 5.5

…

3. Ending Inventory for December = 0.15 × 1 drum × 43,800 units = 6,570

4. Direct materials purchases budget—drums:

January February

Production in units……………………………………

…

43,800 41,000

× Drums per unit……………………………………

…

11

…

…

CHAPTER 9 Profit Planning

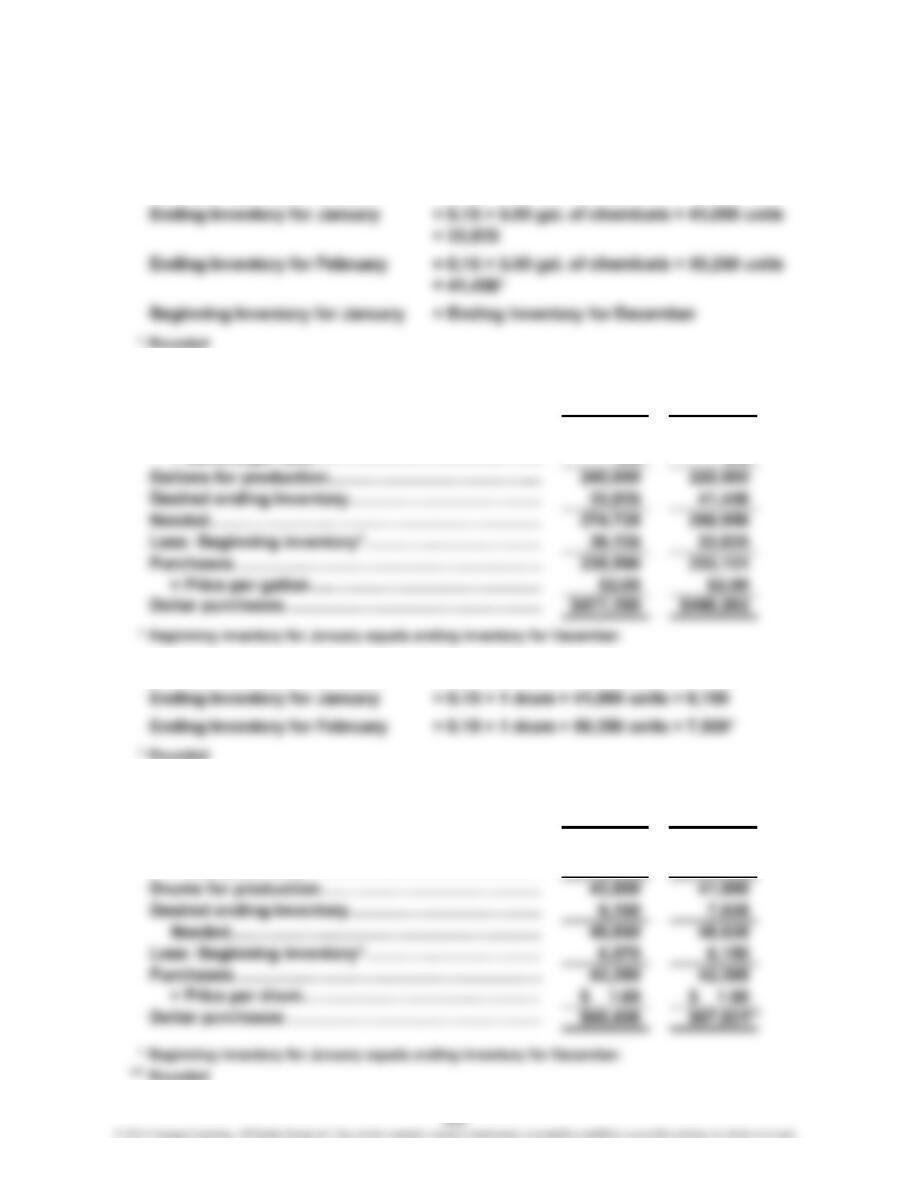

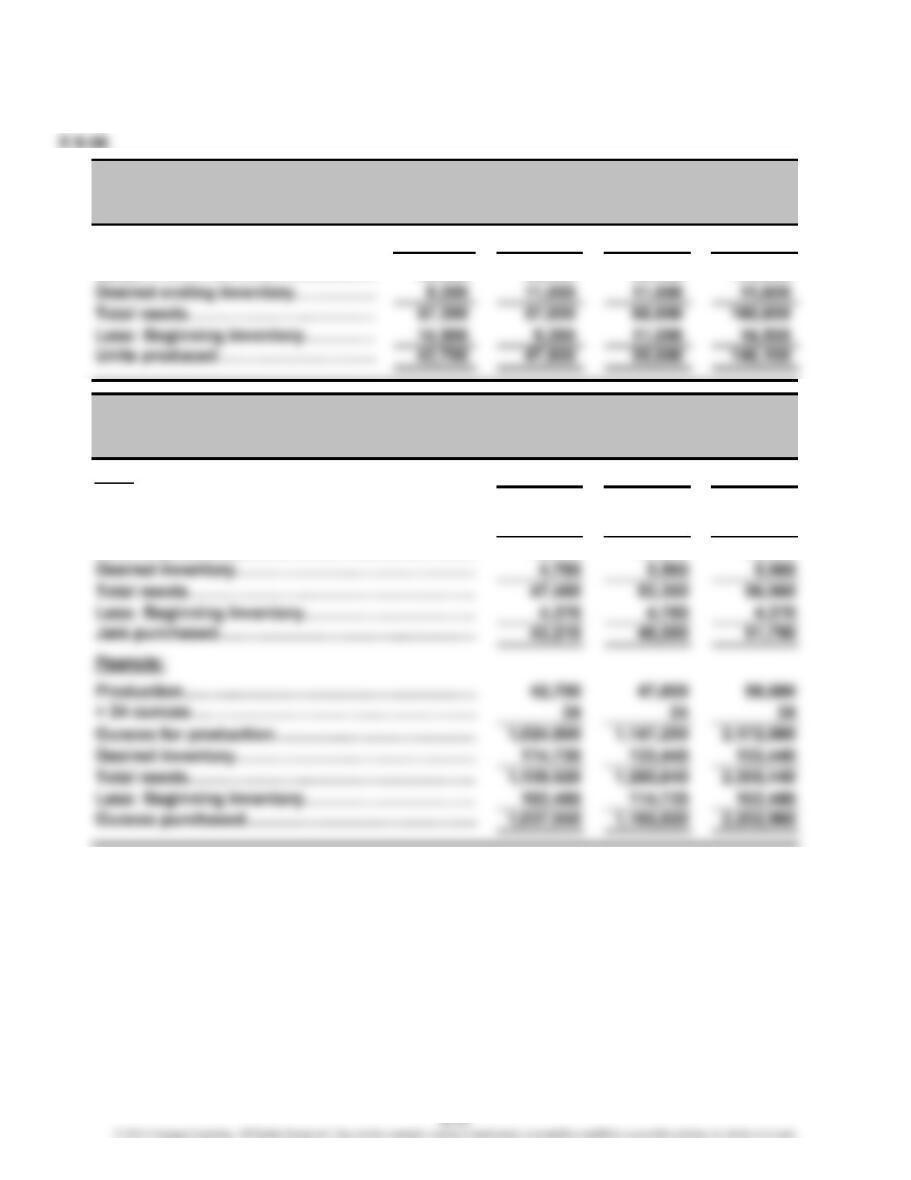

CE 9-24

Direct Labor Budget: January February March Total

Units to be produced………………

…

43,800 41,000 50,250 135,050

CE 9-25

Overhead: January February March Total

Total direct labor hrs. ………………

…

13,140 12,300 15,075 40,515

CE 9-26

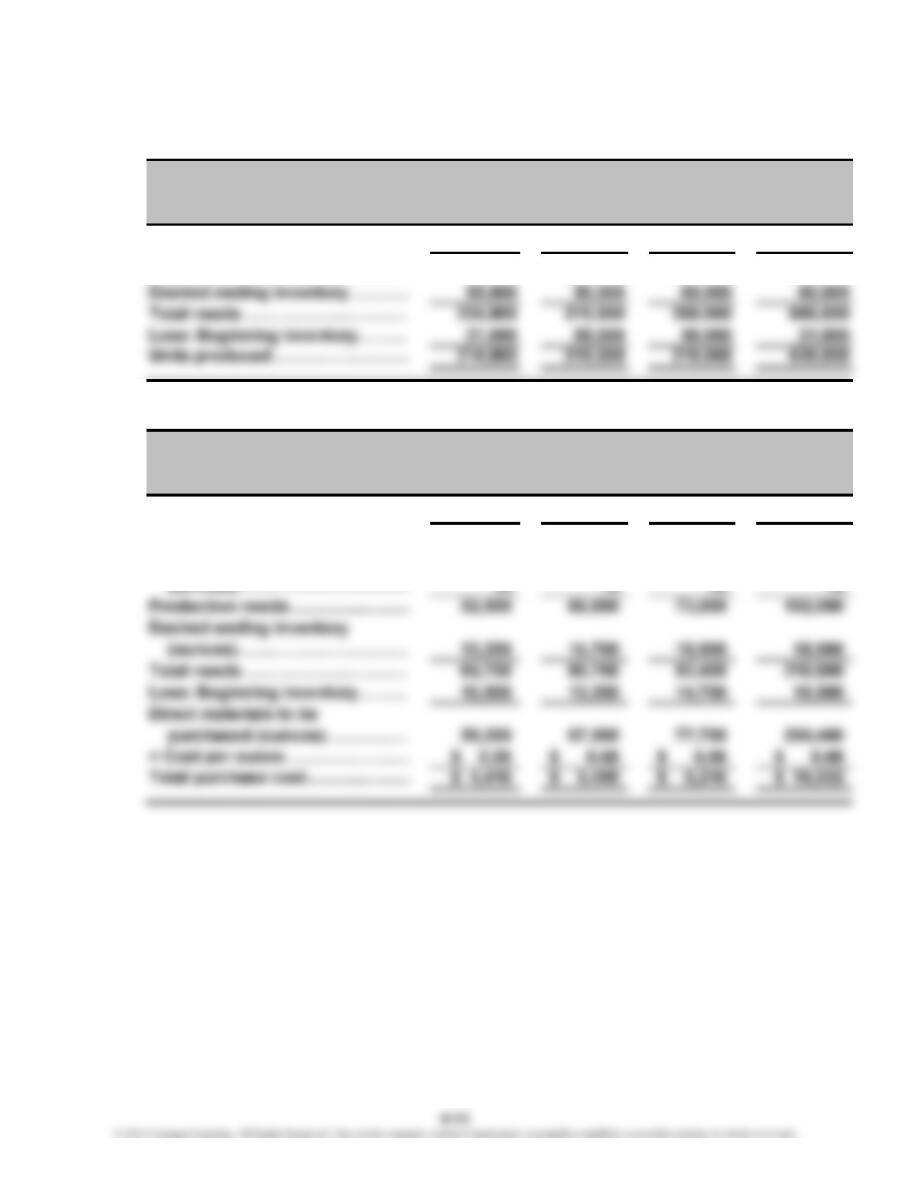

1. Direct materials…………………………………………………………………………

…

$14.00

Direct labor (1.9 hr × $16)…………………………….………………………………

…

30.40

…

…

2. Cost of ending inventory ($49.72 × 675)……………………………………………

…

$33,561

CE 9-27

Direct materials ($14 × 20,000)………………………………………………………

…

$280,000

Direct labor (1.9 hr × $16 × 20,000)………..……………………..…………………

…

608,000

…

…

Cost of Goods Sold Budget

For the Coming Year

Andrews Company

…

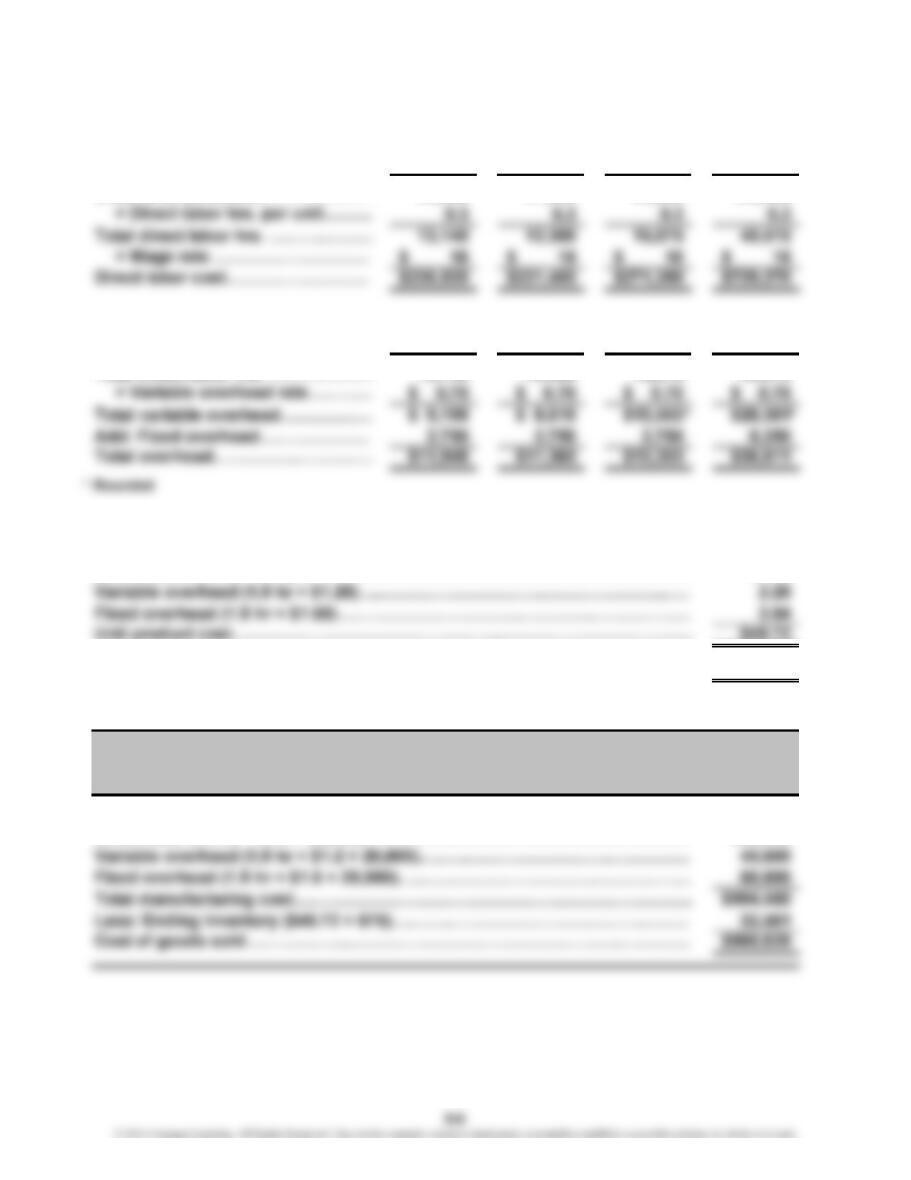

CE 9-28

V

ariable selling expenses (0.03 × $19,730,000)…………

…

$ 591,900

Fixed expenses:

Salaries………………………………………………………

…

$ 960,000

…

…

…

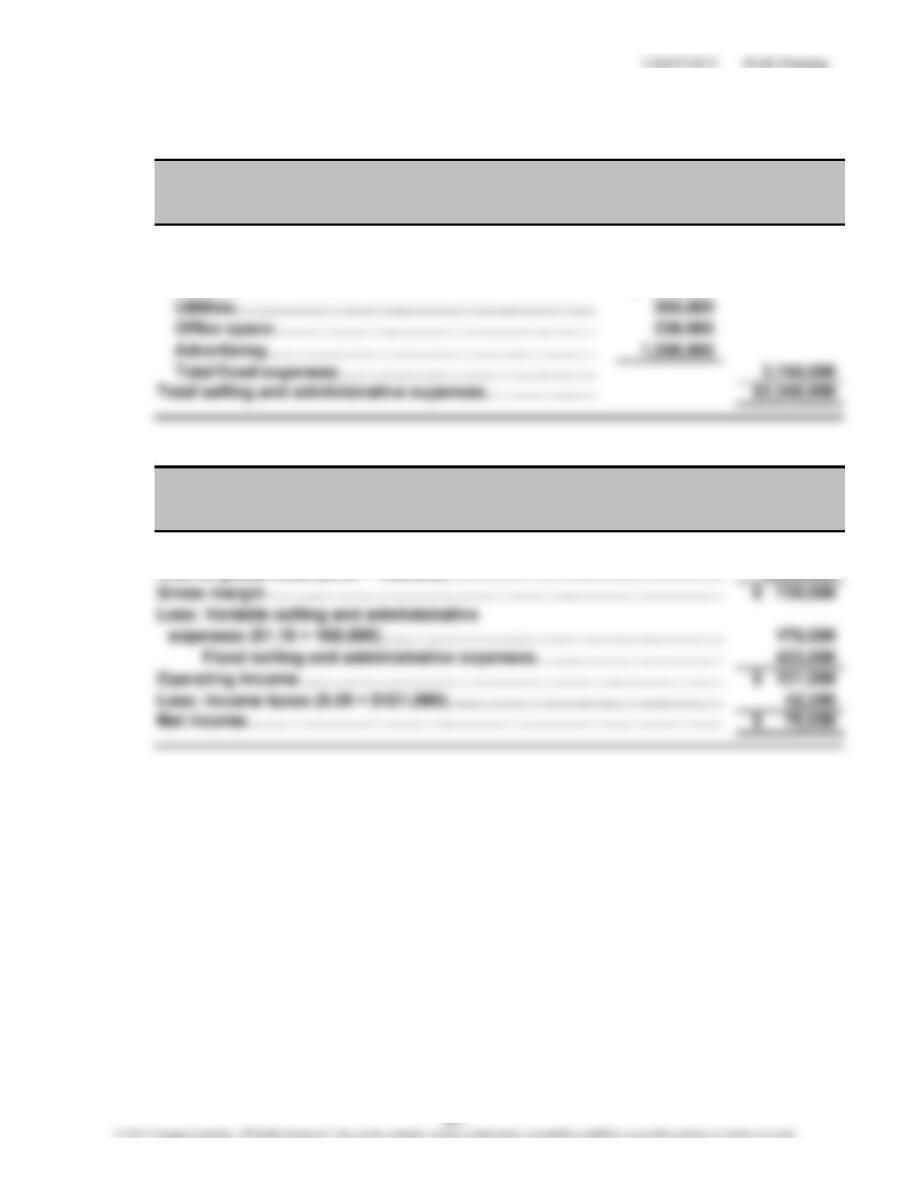

CE 9-29

Sales ($10.80 × 160,000)….……………..…………….…………………………… $1,728,000

Cost of goods sold ($6.30 × 160,000)….……………..…………….……………

…

1,008,000

For the Coming Year

Fazel Company

Selling and Administrative Expenses Budget

For the Coming Year

Oliver Company

Budgeted Income Statement

CHAPTER 9 Profit Planning

CE 9-30

August September

June:

($100,800 × 0.25)………………………………….…………

…

$25,200 —

CE 9-31

1. Payments for purchases from:

2. Payments for purchases from:

…

CHAPTER 9 Profit Planning

CE 9-32

1. Cash receipts in October from:

Cash sales ($157,000 × 0.85)………………………………………………

…

$133,450

2. Payments for food and supplies purchases from:

3. Beginning balance………………………………………………………………

…

$ 2,147

Cash receipts……………………………………………………………………

…

157,558

Cash available……………………………………………………………………

…

$159,705

Less:

Payments for food and supplies purchases……………………………

…

$126,500

Owners’ draw…………………………………………………………………

…

6,000

CHAPTER 9 Profit Planning

E 9-33

1. h, i 6. f

E 9-34

1.

1st Qtr. 2nd Qtr. 3rd Qtr. 4th Qtr.

Y

ea

r

S12L7

Units……

…

800 2,200 5,600 4,600 13,200

…

…

…

2. Stillwater Designs will use the sales budget in planning as the basis for the production

EXERCISES

Stillwater Designs

Sales Budget

For the Year Ended December 31, 2014

E 9-35

1st Qtr. 2nd Qtr. 3rd Qtr. 4th Qtr.

Y

ea

r

Sales………………….………

…

800 2,200 5,600 4,600 13,200

Desired ending

…

…

1st Qtr. 2nd Qtr. 3rd Qtr. 4th Qtr.

Y

ea

r

Sales………………….………

…

1,300 1,400 5,300 3,900 11,900

Desired ending

…

…

Stillwater Designs

Production Budget for S12L5

For the Year Ended December 31, 2014

Stillwater Designs

Production Budget for S12L7

For the Year Ended December 31, 2014

CHAPTER 9 Profit Planning

1.

January February March Total

Sales……………………………………

…

48,000 46,000 55,000 149,000

2.

Jars: January February Total

Production……………………………………………

…

42,700 47,800 90,500

× 1 jar…………….……………………………………

…

111

Jars for production…………………………………

…

42,700 47,800 90,500

…

Direct Materials Purchases Budget

For January and February

Peanut-Fresh Inc.

Production Budget

For the First Quarter of the Year

Peanut-Fresh Inc.

CHAPTER 9 Profit Planning

E 9-37

A

pril May June Total

Sales………………………………… 180,000 220,000 200,000 600,000

E 9-38

July

A

ugust Septembe

r

Total

Units to be produced……………

…

3,500 4,400 4,900 12,800

× Direct materials per unit

(ounces)…………………………

…

15 15 15 15

…

Aqua-pro Inc.

Production Budget

For the Second Quarter

Langer Company

Direct Materials Purchases Budget

For July, August, and September

…

…

CHAPTER 9 Profit Planning

E 9-39

March

A

pril May Total

Units to be produced………… 4,000 13,000 14,400 31,400

E 9-40

Units Price Total Sales

LB-1………………………………………………

…

36,750 $32.00 $1,176,000

LB-2………………………………………………

…

18,900 20.00 378,000

Evans Company

Direct Labor Budget

For March, April, and May

Model

Alger Inc.

Sales Budget

For the Coming Year

E 9-41

1.

Septembe

r

Octobe

r

Novembe

r

Decembe

r

Sales………………………………………

…

250 200 230 380

…

…

2.

Fruit Septembe

r

Octobe

r

Novembe

r

Production……………………………………………

…

247 202 237

× Pounds of fruit ……………………………………

…

11 1

…

3. December includes the holiday season and is a time when many gifts are given. Jani

Jani’s Flowers and Gifts

Production Budget for Gift Baskets

For September, October, November, and Decembe

r

For September, October, and Novembe

r

Jani’s Flowers and Gifts

Direct Materials Purchases Budget

CHAPTER 9 Profit Planning

E 9-42

1. Credit Sales in May = $290,000 × 0.85 = $246,500

2.

July August

Cash sales…………………………………………………………

…

$ 44,250 $ 45,000

Payments on account:

From May credit sales:

(0.05 × $246,500)……………………………………………

…

12,325 0

…

…

…

…

…

E 9-43

1.

Payments on account:

From May credit sales:

(0.23 × $248,000)………………………………………………………………

…

$ 57,040

…

…

Schedule of Cash Receipts

For July

Bennett Inc.

Schedule of Cash Receipts

For July and August

Roybal Inc.

CHAPTER 9 Profit Planning

E 9-43 (Continued)

2.

Payments on account:

From June credit sales:

E 9-44

Payments on accounts payable:

From July purchases (0.80 × $77,000)…………………………………..…

…

$ 61,600

From August purchases (0.20 × $73,000)…………………………………..

…

14,600

Schedule of Cash Receipts

For August

Roybal Inc.

Fein Company

Schedule of Cash Payments

For August

…

CHAPTER 9 Profit Planning

E 9-45

Beginning cash balance……………………………..…………

…

$ 736

Collections:

Cash sales………………………………………………………

…

18,600

Credit sales:

Current month ($54,000 × 0.40)…………………………

…

21,600

May credit sales ($35,000 × 0.30)………………………

…

10,500

2. Yes, the business does show a negative cash balance for the month of June. A

Cash Budget

For June

…

CHAPTER 9 Profit Planning

P 9-46

A

ugus

t

September

Cash fees……………………………………………..………

…

$ 48,500 $ 60,000

Received from sales in:

June (0.75 × 0.26 × $200,000 × 1.03)………

…

40,170 —

P 9-47

1.

a. Schedule 1:Sales Budget

January February March Total

Units…………………

…

40,000 50,000 60,000 150,000

PROBLEMS

Allison Manufacturing

For the Quarter Ended March 31

Aragon and Associates

Schedule of Cash Receipts

For August and Septembe

r

…

CHAPTER 9 Profit Planning

P 9-47 (Continued)

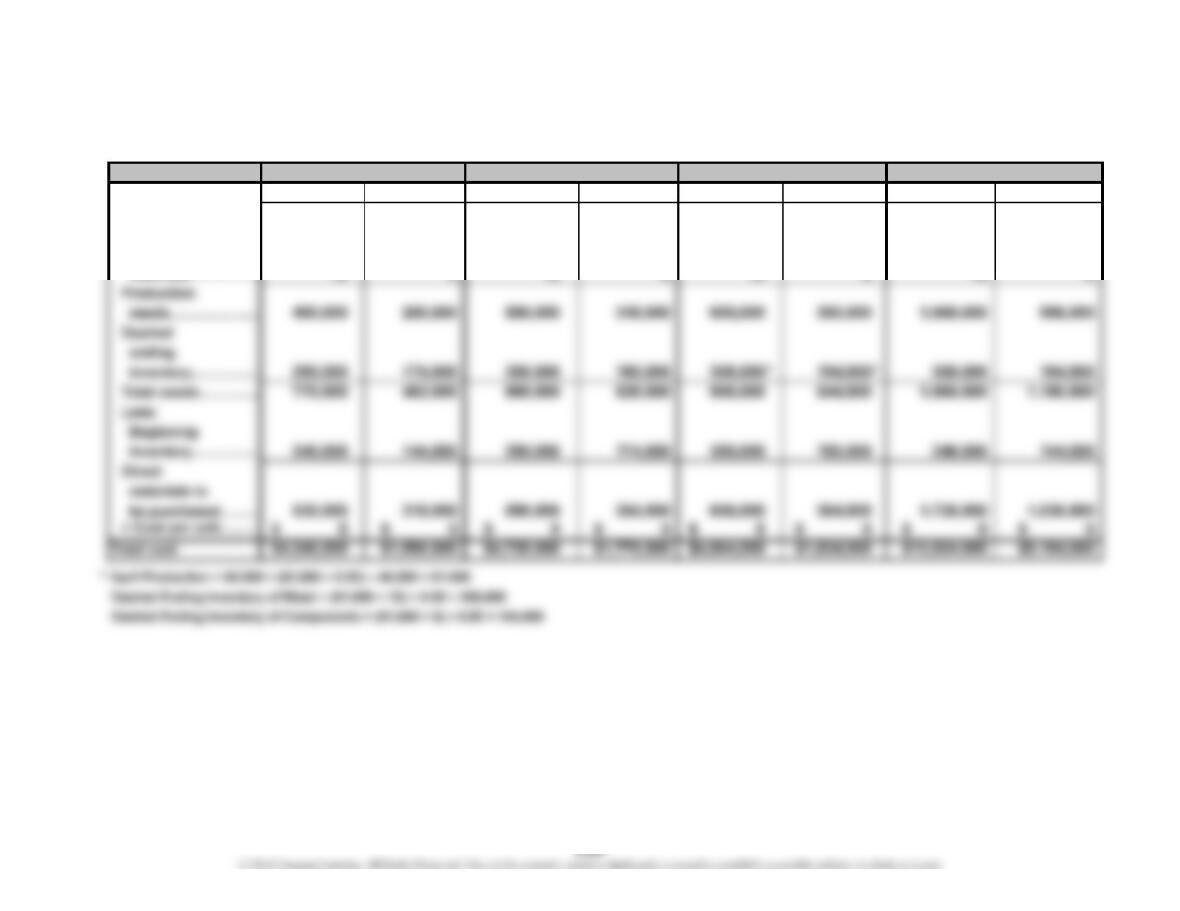

c. Schedule 3: Direct Materials Purchases Budget

Component

Units to

be produced………

…

48,000 60,000 60,000 166,000

× Direct

materials…………… 10 10 6 6

TotalMarch

Metal

Component

January

48,000

6

Metal

February

ComponentMetalMetal

58,000

10

Component

58,000

6

166,000

10

…