1. A static budget is for a particular level of activity. A flexible budget is one that can be established

for any level of activity.

2. For performance reporting, it is necessary to compare the actual costs for the actual level of

activity with the budgeted costs for the actual level of activity. A flexible budget provides the

means to compute the budgeted costs for the actual level of activity, after the fact.

5. An after-the-fact flexible budget facilitates performance evaluation by allowing the calculation of

what spending should have been for the actual level of activity.

6. Part of a variable overhead spending variance can be caused by inefficient use of overhead

resources.

10. The volume variance occurs when the actual volume differs from the expected volume used to

compute the predetermined standard fixed overhead rate. An unfavorable volume variance

occurs when the actual volume is less than the expected volume. Thus, an unfavorable volume

variance means that actual production is less than expected.

DISCUSSION QUESTIONS

11 FLEXIBLE BUDGET AND

OVERHEAD ANALYSIS

11-1

CHAPTER 11 Flexible Budget and Overhead Analysis

12. The spending variance. This variance is computed by comparing actual expenditures with

budgeted expenditures. The volume variance simply tells whether the actual volume is different

from the expected volume.

13. An activity-based budget requires three steps: (1) identification of activities, (2) estimation of

activity output demands, and (3) estimation of the costs of resources needed to provide the

activity output demanded.

11-2

CHAPTER 11 Flexible Budget and Overhead Analysis

11-1. c

11-2. a

11-8. a

11-9. d

11-10. d

11-11. a

11-12. c

MULTIPLE-CHOICE QUESTIONS

11-3

CHAPTER 11 Flexible Budget and Overhead Analysis

CE 11-19

1.

Direct materials ($0.60 × 3 × 4,000)……………………

…

$ 7,200

2.

A

ctual Budgeted

V

ariance*

Units produced………………………

…

3,800 4,000 200 U

Direct materials………………………

…

$ 6,800 $ 7,200 $ (400) F

V

CE 11-20

2,500 units 3,000 units 3,500 units

Direct materials………………………

…

$ 4,500 $ 5,400 $ 6,300

V

Budgeted for 4,000 units

Performance Report

CORNERSTONE EXERCISES

11-4

V

CHAPTER 11 Flexible Budget and Overhead Analysis

CE 11-21

Actual Budgeted Variance*

Units produced………………

…

3,800 3,800

—

Direct materials………………

…

$ 6,800 $ 6,840 $ (40) F

CE 11-22

1. Actual Variable Overhead Rate

(AVOR)

3. Actual variable overhead……………………

…

$206,816

Applied variable overhead……………………

…

207,200

Total variable overhead variance……………

…

$ (384) F

Note: The total variable overhead variance can also be calculated using

Performance Report

Actual Variable Overhead

Actual Direct Labor Hours

=

11-5

V

CHAPTER 11 Flexible Budget and Overhead Analysis

CE 11-23

1. Columnar approach:

2.

V

ariable Overhead Spending Variance = (AVOR – SVOR) AH

= ($3.68 – $3.70)56,200

= $(1,124) F

CE 11-24

Cost Actual Actual

Formula Cost Hours

Inspection

…

$2.00 $112,300 $112,400 $(100) F $112,000 $400 U

…

CE 11-25

1. Standard Hrs for Actual Units = SH per Unit × Actual Units Produced

= 4 × 14,000

= 56,000

1. AH × AVOR 2. AH × SVOR

Cost Item

Overhead

3. SH × SVOR

Spending

V

ariance

Budget for

Budget for

V

ariance

EfficiencyAt Standard

Hours

11-6

V

V

V

CHAPTER 11 Flexible Budget and Overhead Analysis

CE 11-26

1. Columnar approach:

1. AH × AFOR

CE 11-27

Salaries (6 inspectors × $32,000)………………

…

$192,000

CE 11-28

40,000 units 60,000 units

Fixed

V

ariable 60,000 mhrs 90,000 mhrs

Maintenance…

…

$50,000 $1.80 $158,000 $212,000

Machining……

…

25,000 3.00 205,000 295,000

V

…

56,200 × $5.03

$282,686

Spending

56,200 × $5.00

Efficiency

$281,000

$1,686 U

2. AH × SFOR 3. SH × SFOR

$1,000 U

$280,000

56,000 × $5.00

11-7

CHAPTER 11 Flexible Budget and Overhead Analysis

CE 11-29

A

ctual Budgeted

V

ariance*

Units produced………………

…

40,000 40,000 —

Maintenance…………………

…

$158,300 $158,000 $ 300 U

Performance Report

11-8

CHAPTER 11 Flexible Budget and Overhead Analysis

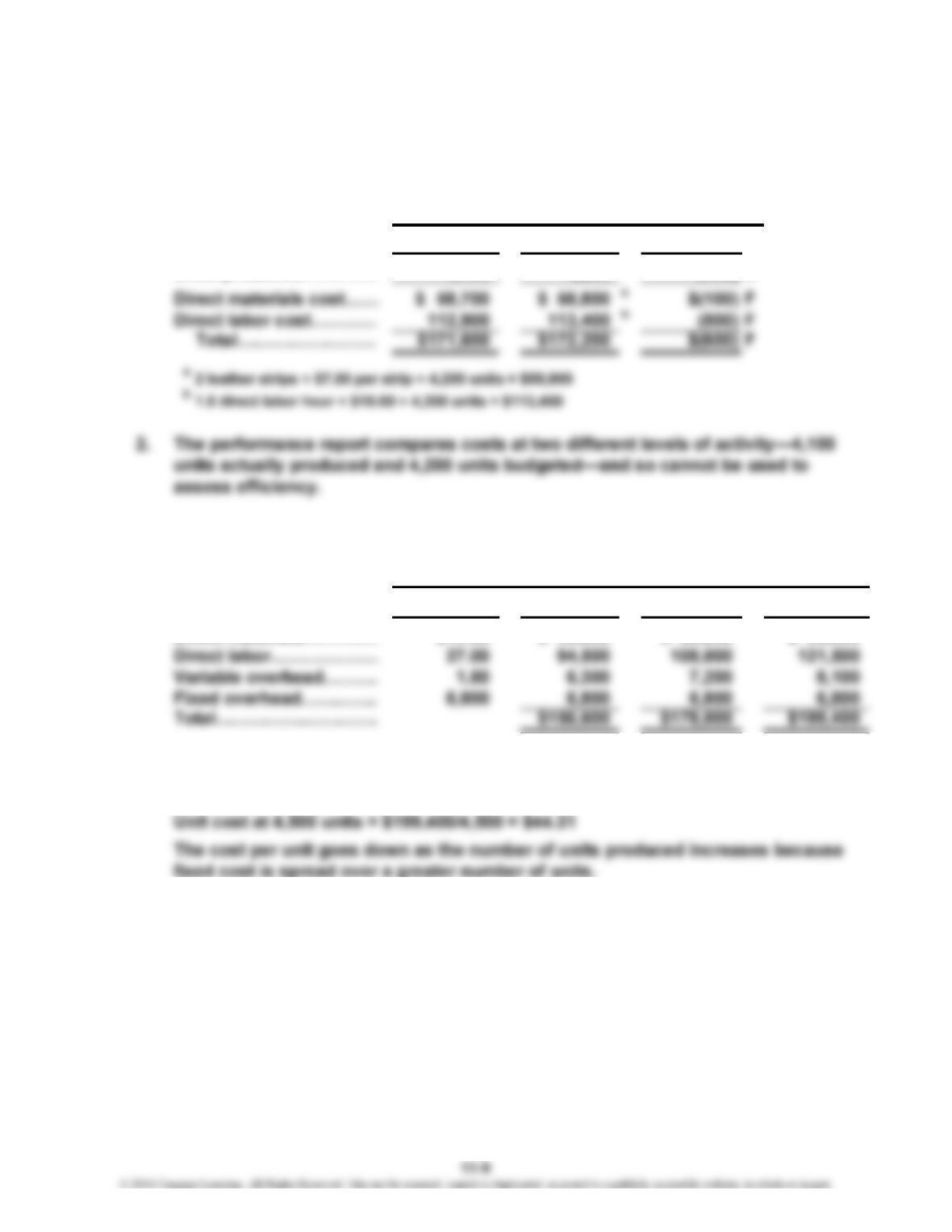

E 11-30

1.

A

ctual Budgeted

V

ariance

Units produced…………

…

4,100 4,200 (100) U

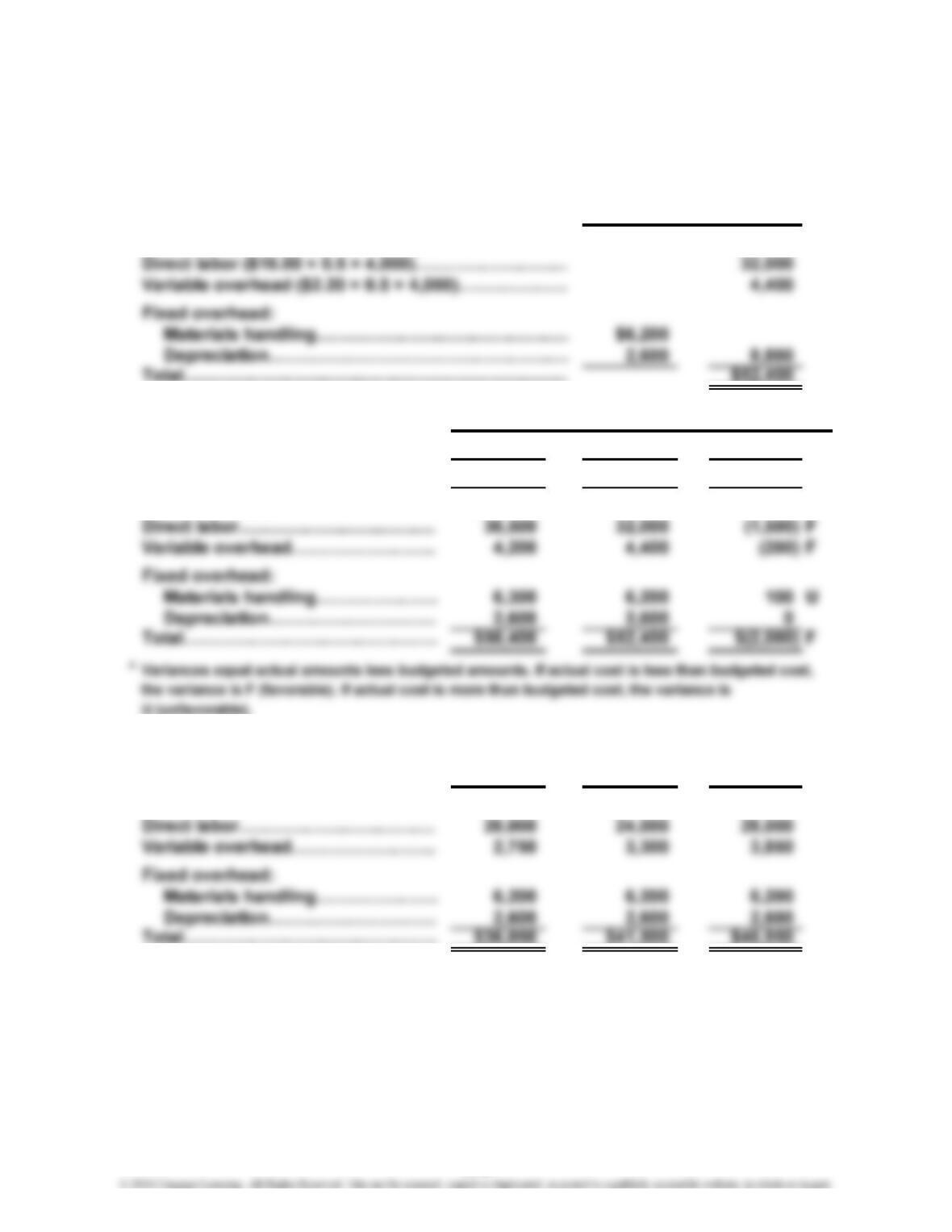

E 11-31

1.

Cost Formula 3,500 units 4,000 units 4,500 units

Direct materials…………

…

$14.00 $ 49,000 $ 56,000 $ 63,000

V

…

2. Unit cost at 3,500 units = $156,600/3,500 = $44.74

Unit cost at 4,000 units = $178,000/4,000 = $44.50

Performance Report

Flexible Budget for

EXERCISES

CHAPTER 11 Flexible Budget and Overhead Analysis

E 11-32

1.

V

ariable costs: $ 18,000

Maintenance…………………………………

…

40,500

Power…………………………………………

…

189,000

2. Direct Labor Hours for 15% Higher Production = 90,000 + 0.15(90,000)

= 103,500

Direct Labor Hours for 15% Lower Production = 90,000 – 0.15(90,000)

= 76,500

Formula

V

ariable costs:

Maintenance……………

…

$0.20 $ 15,300

Power……………………… 0.45 34,425

…

$ 20,700

46,575

Palladium Inc.

Overhead Budget

For the Coming Year

Formula

Activity Level

90,000 Hours

$0.20

0.45

2.10

103,500 Hours 76,500 Hours

A

ctivity Level

…

CHAPTER 11 Flexible Budget and Overhead Analysis

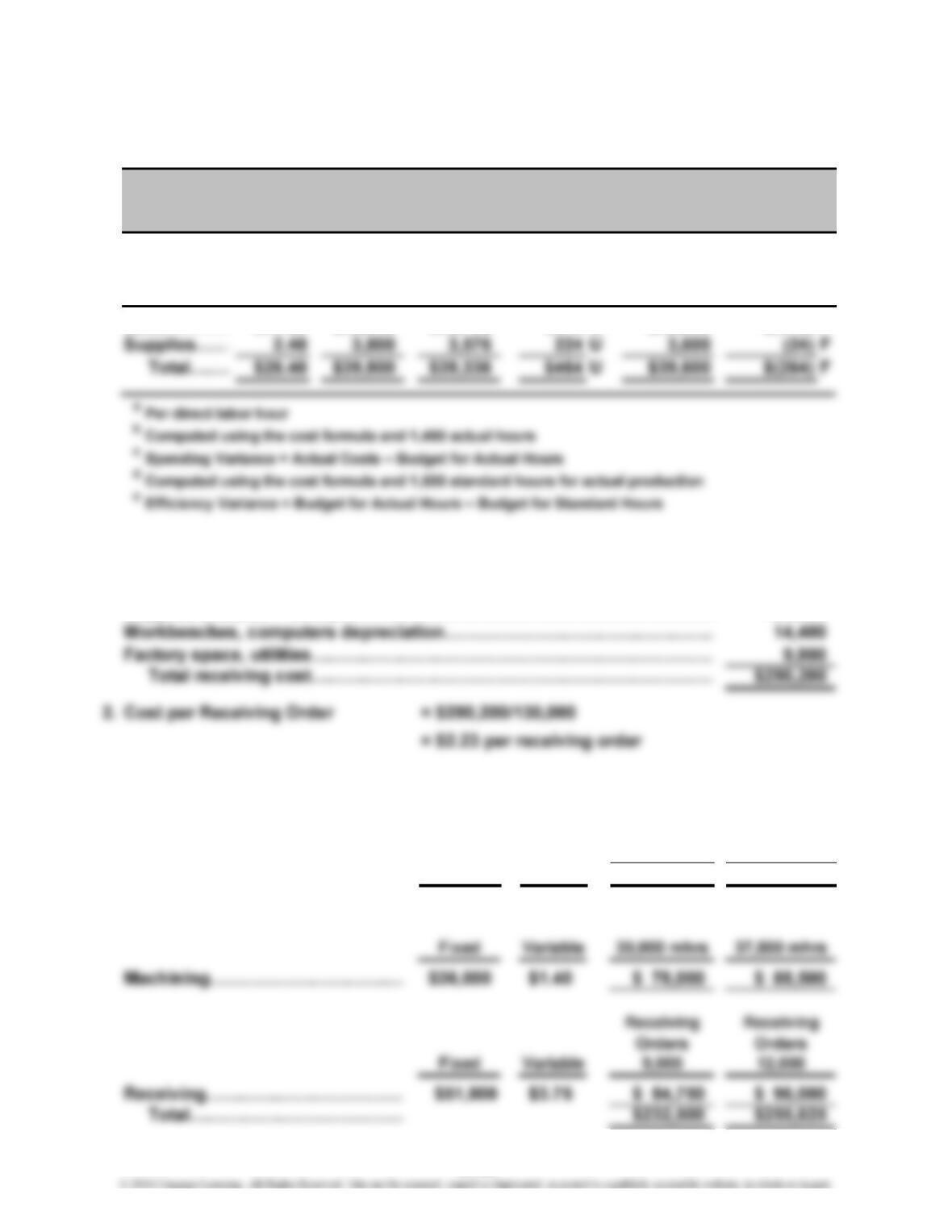

E 11-33

Direct labor hours

based on actual……

…

Variable overhead:

Maintenance………

…

U

E 11-34

1. Standard direct labor hrs required:

= Actual Deliveries × Standard Direct Labor Hours

= 38,600 × 0.80

= 30,880 direct labor hours

2.

V

ariable overhead analysis:

E 11-35

= $400,000/32,000 DLH

= $12.50

2. Fixed overhead analysis:

Budgeted Fixed Overhead

Practical Capacity

=Standard Fixed Overhead Rate (SFOR)

Actual Budgeted

93,000

$104,600

93,000

$107,000

1.

Performance Report

Variance

—

$2,400

11-11

…

CHAPTER 11 Flexible Budget and Overhead Analysis

E 11-36

1.

V

ariable overhead analysis:

2. Fixed overhead analysis:

E 11-37

1. Fixed Overhead Rate = $832,500/450,000* = $1.85 per DLH

2. Fixed overhead analysis:

3.

V

ariable OH Rate = ($1,777,500 – $832,500)/450,000 hours

= $2.10 per DLH

4. Variable overhead analysis:

Spending Efficiency

Actual FOH

Actual VOH Budgeted VOH

Budgeted FOH

Applied FOH

Actual FOH Budgeted FOH

Applied VOH

Actual VOH Budgeted VOH

Applied VOH

Applied FOH

11-12

CHAPTER 11 Flexible Budget and Overhead Analysis

E 11-38

1. Total Applied Fixed Overhead = (Standard Hours per Unit × Actual Units) × SFOR

= (0.9 × 143,000) × $11 = $1,415,700

4. Total Applied = (Standard Hours per Unit × Actual Units) × SVOR

Variable Overhead

= (0.9 × 143,000) × $6.36 = $818,532

CHAPTER 11 Flexible Budget and Overhead Analysis

E 11-39

Actual Actual Spending Efficiency

Cost Hours

b

V

ariancec

V

ariancee

Labor………

…

$24.00 $36,000 $35,760 $240 U $(240) F

E 11-40

1. Salaries (6 workers × $27,000)…………………………………………………

…

Supplies (130,000 × $0.80)………………………………………………………

…

E 11-41

Fixed Variable

Engineering…………………………

…

$67,000 $5.50

V

V

Performance Report

For the Year Ended December 31

Cost

Budget for Budget for

Standard

Cost Formulaa

$36,000

Hoursd

50,000 units

750 eng. hrs.

$ 71,125

$ 69,750

500 eng. hrs.

40,000 units

A

nker Company

$162,000

104,000

Required for

11-14

CHAPTER 11 Flexible Budget and Overhead Analysis

E 11-42

A

ctual Budgeted

V

ariance

Maintenance………………………

…

$179,600 $176,700 $2,900 U

Performance Report

11-15

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-43

1. Direct Labor Hours = (80,000 bags × 0.20 hours) +

(80,000 bags × 0.30 hours)

2.

Formula

V

ariable costs:

Maintenance………………………

…

$0.50 $20,000

Power………………………………

…

0.40 16,000

…

PROBLEMS

40,000 Hours*

Activity Level

Healthy Pet Company

Overhead Budget

For the Coming Year

CHAPTER 11 Flexible Budget and Overhead Analysis

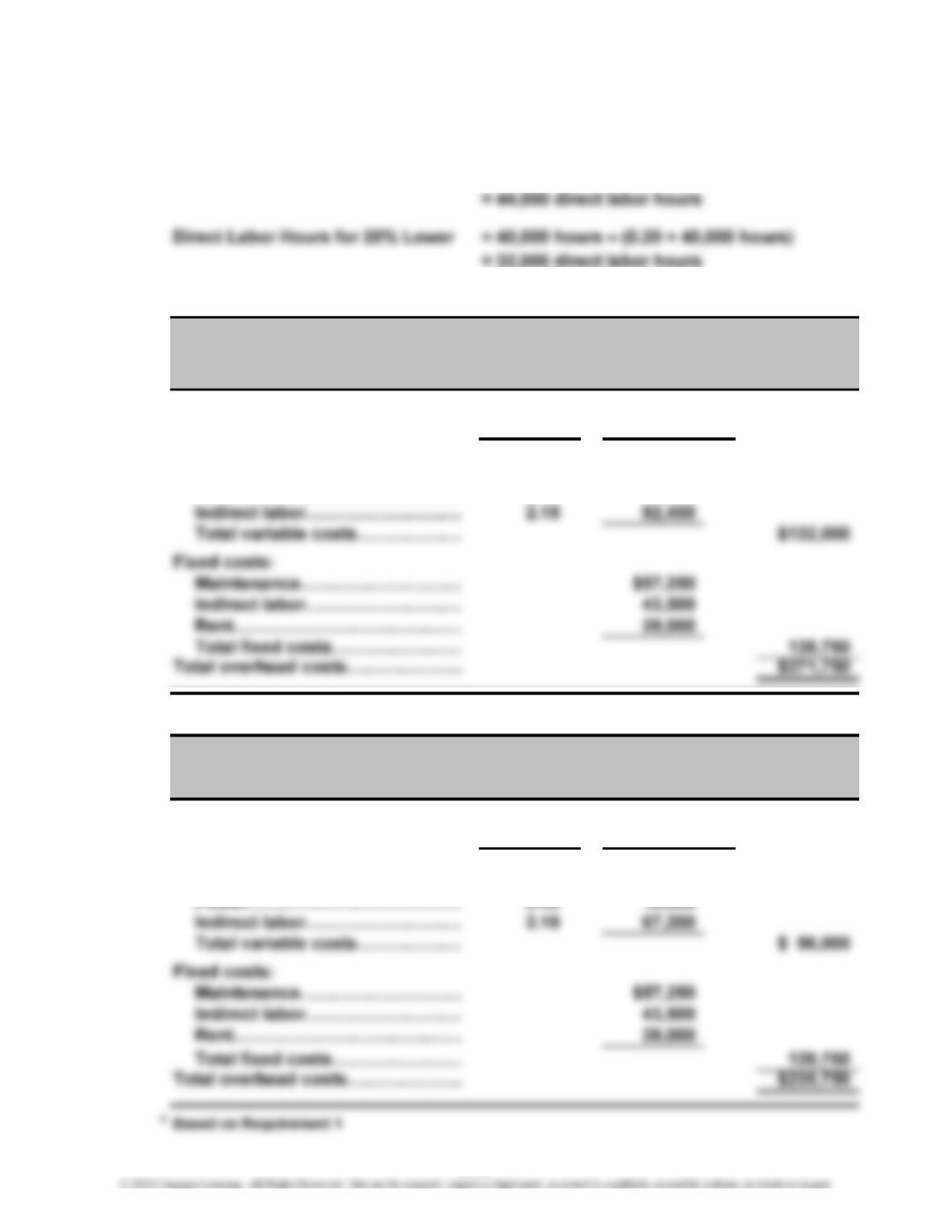

P 11-44

1. Direct Labor Hours for 10% Higher = 40,000 hours + (0.10 × 40,000 hours)

2. 10% higher:

Formula

V

ariable costs:

Maintenance………………………

…

$0.50 $22,000

Power………………………………

…

0.40 17,600

…

20% lower:

Formula

V

ariable costs:

Maintenance………………………

…

$0.50 $16,000

…

…

44,000 Hours*

Healthy Pet Company

Overhead Budget

For the Coming Year

A

ctivity Level

Healthy Pet Compan

y

Overhead Budget

For the Coming Year

A

ctivity Level

32,000 Hours*

11-17

CHAPTER 11 Flexible Budget and Overhead Analysis

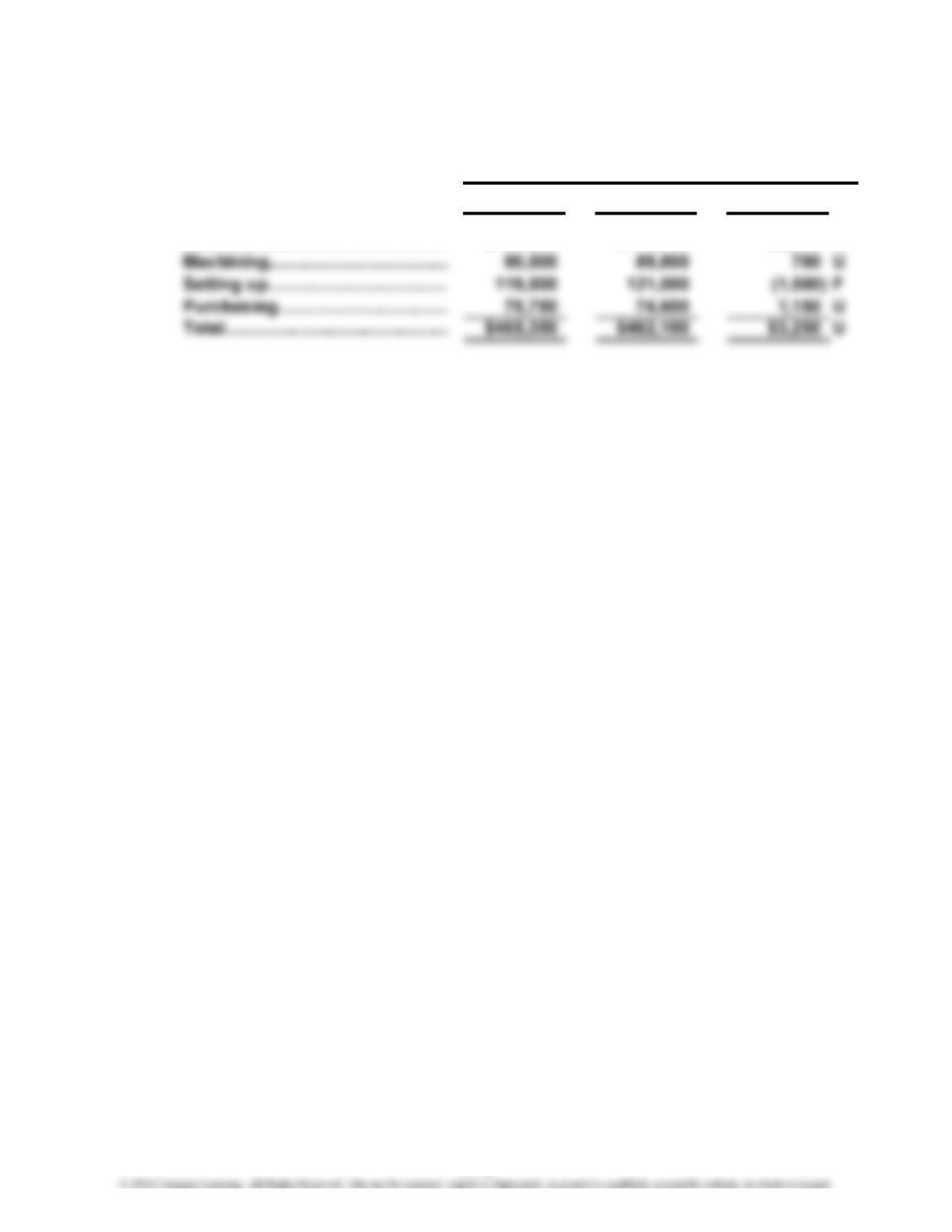

P 11-45

2.

A

ctual Budgeted*

V

ariance

Units produced………………………… 190,000 190,000 0

Production unit:

Maintenance………………………

…

$ 81,300 $ 80,750 $ 550 U

3. All of the variances are small (less than 2% of budgeted amounts). Most would

probably view the variances as immaterial. Reasons for variances are numerous.

Healthy Pet Compan

y

Performance Report

For the Current Year

11-18

CHAPTER 11 Flexible Budget and Overhead Analysis

P 11-46

1. Car W23 = 12/60(30,000) = 6,000 direct labor hours

2.

A

ctivity Level

Formula 30,000 Hours*

Variable costs:

Maintenance……………………

…

$3.80 $114,000

Supplies…………………………

…

4.25 127,500

…

P 11-47

1.

V

ariable*

Acquisition………………………

…

$600

Freight……………………………

…

60

…

2. Most Likely Optimistic

Sales (@ $760)…………………

…

$114,000,000 $190,000,000

V

…

Spelzig Company

Overhead Budget

For the Month of November

Fixed

$54,720,000

Pessimistic

11-19