1. Process costing collects costs by process (department) for a given period of time. Unit

costs are computed by dividing these costs by the department’s output measured for the

same period of time. Job-order costing collects costs by job. Unit costs are computed by

dividing the job’s costs by the units produced in the job. Process costing is typically used

for industries where units are homogeneous and mass-produced. Job-order costing is used

for industries that produce heterogeneous products (often custom-made).

4. The work-in-process account of the receiving department is debited, and the work-in-process

account of the transferring department is credited. The finished goods account is debited,

and the work-in-process account of the final department is credited upon completion

of the product.

5. Service firms generally do not have work-in-process inventories, and so equivalent units of

production are not needed. An important factor in process costing for services is determining

just what constitutes a unit of output.

8. In calculating this period’s unit cost, the weighted average combines beginning inventory costs

and work done with current-period costs and work to calculate this period’s unit cost. The FIFO

method excludes any costs and output carried over from this period’s unit cost computation,

hence, only current work and costs are used to calculate this period’s unit cost.

6PROCESS COSTING

DISCUSSION QUESTIONS

6-1

CHAPTER 6 Process Costing

10. The first step is the preparation of a physical flow schedule. This schedule identifies the

physical units that must be accounted for and provides an accounting for these units. The second

step is the equivalent unit schedule. This schedule computes the equivalent whole output for the

11.

A

production report summarizes the activities and costs associated with a process for a given

period. It shows the physical flow, the equivalent units, the unit cost, and the values of ending

work in process and goods transferred out. The report serves the same function as a job-order

cost sheet in a job-order costing system.

14. The weighted average method uses the same unit cost for all goods transferred out. The FIFO

method divides goods transferred out into two categories: units started and completed and

6-2

CHAPTER 6 Process Costing

6-1. d

6-2. c

6-10. d 100,000 + (0.4 × 25,000)

6-11. e 100,000 + (0.8 × 25,000)

6-18. a

6-19. c

MULTIPLE-CHOICE QUESTIONS

6-3

CHAPTER 6 Process Costing

CE 6-21

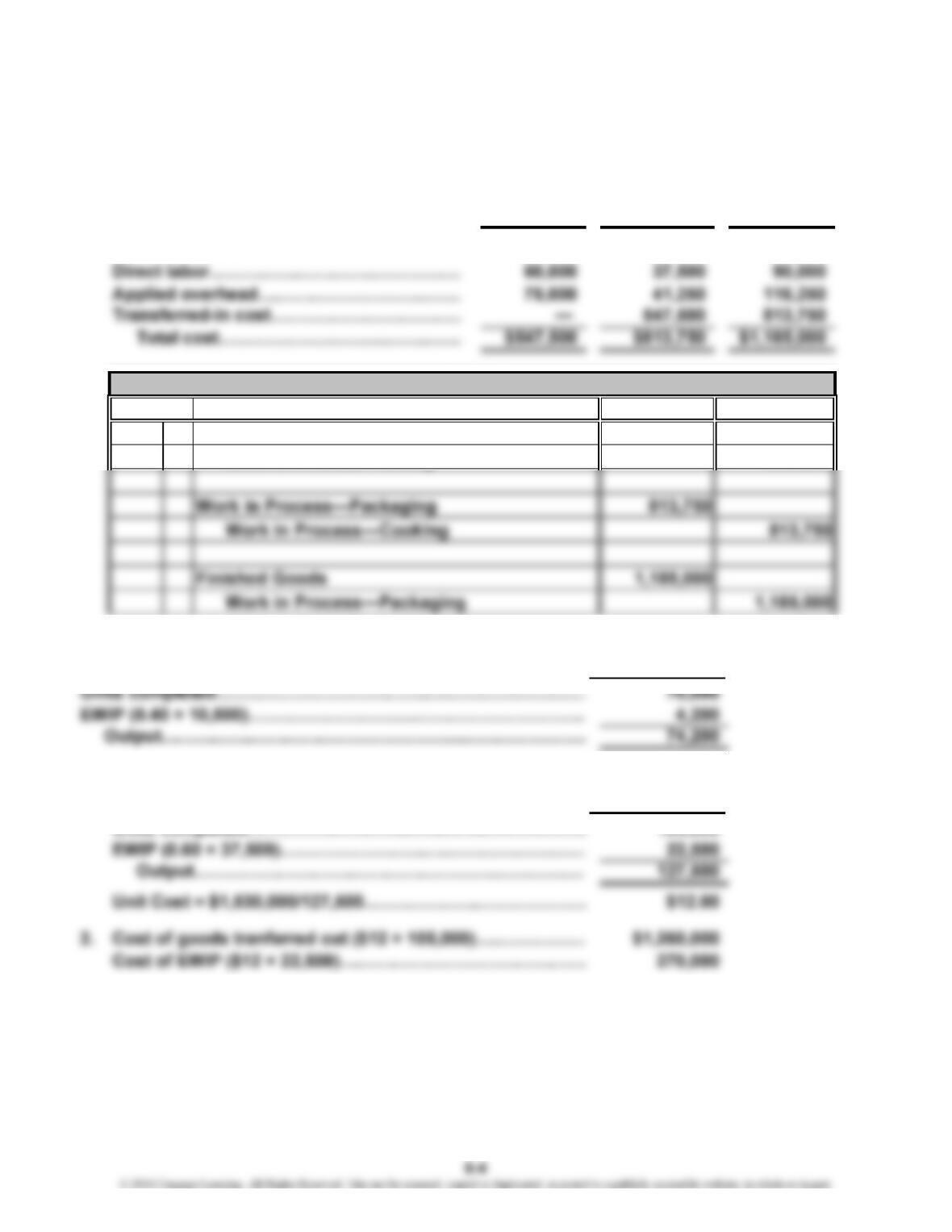

Mixing Cooking Packaging

1. Direct materials………………………………

…

$412,500 $187,500 $ 165,000

2.

Debit

Work in Process—Cooking 547,500

Work in Process—Mixing 547,500

CE 6-22

Equivalent Units

CE 6-23

1. Equivalent Units

Units completed…………………………………………………

…

CORNERSTONE EXERCISES

Journal

CreditDate Description

105,000

CE 6-24

1. Equivalent

Units

Units completed………………………………………………………………………

…

240,000

…

CE 6-25

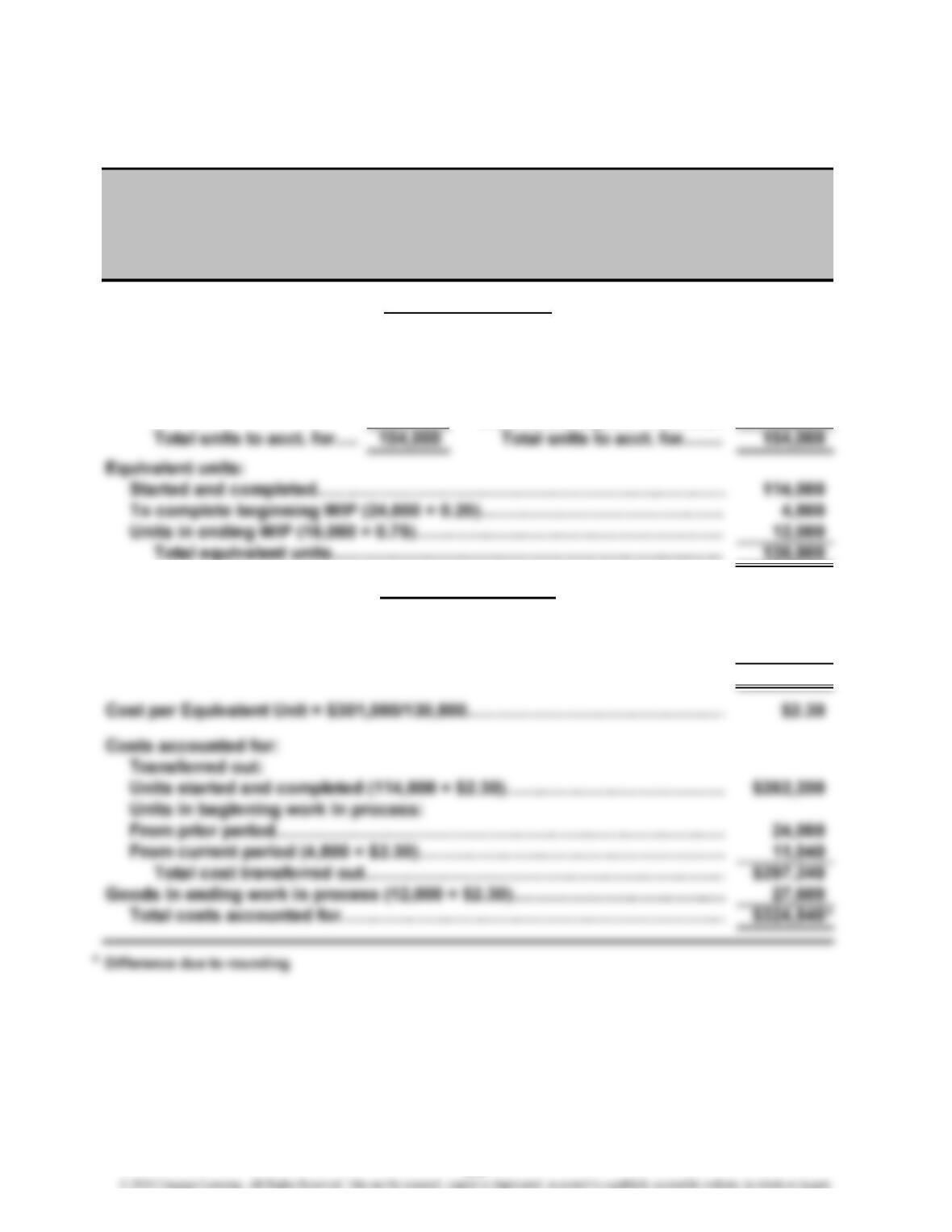

Physical flow schedule:

Units in BWIP (80% complete)…………………………………

…

100,000

CE 6-26

Physical flow:

Units to account for: Units to account for:

UNIT INFORMATION

Cutting Department

Production Report

For the Month of October

Weighted Average Method

CE 6-26 (Continued)

Costs to account for:

Beginning work in process…………………………………………………

…

$ 80,000

Transferred Ending

Out Work in Process Total

Goods transferred out

CE 6-27

1. Materials Conversion

Units completed……………………………………………

…

32,600 32,600

Units in ending WIP ×

…

3. Cost transferred out (32,600 × $5.45)…………………

…

$177,670

Cost of ending WIP:

Add:

COST INFORMATION

CHAPTER 6 Process Costing

CE 6-28

1. Physical flow schedule:

Units in beginning work in process………………………………

…

60,000

Units started during the period……………………………………

…

240,000

2. Units completed…………………………………..……………………… 262,500

Units in EWIP……………………………………………………………… 37,500

Equivalent units (transferred-in materials)………………………

…

300,000

3. Unit-Transferred-In Cost = ($213,000 + $687,000)/300,000………

…

$3.00

CE 6-29

…

2. Unit Cost = $301,000/130,800…………………………………………………………

…

$2.30

3. Cost of units transferred out:

BWIP costs……………………………………………………………………………

…

24,000

Equivalent

Units

6-7

CHAPTER 6 Process Costing

CE 6-30

Physical flow:

Units to account for: Units to account for:

Units in beginning WIP……

…

24,000 Units started and completed

…

114,000

Units started………………… 130,000 From beginning WIP…………

…

24,000

Units in ending WIP…………

…

16,000

Costs to account for:

Costs in beginning WIP…………………………………………………………… $ 24,000

Costs added by department………………………………………………………

…

301,000

Total costs to account for……………………………………………………

…

$325,000

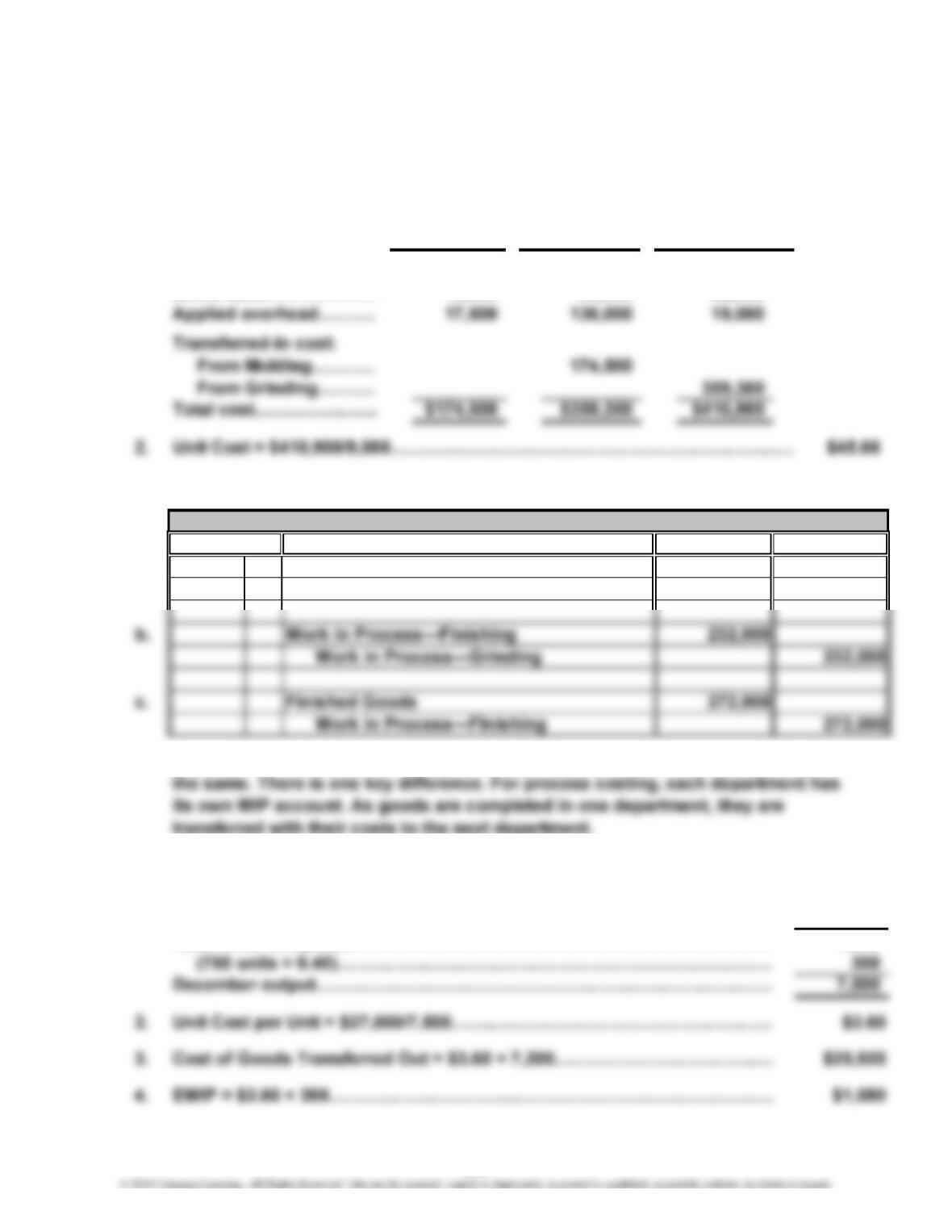

Inca Inc.

Mixing Department

Production Report

For the Month of July

(FIFO Method)

COST INFORMATION

UNIT INFORMATION

6-8

CHAPTER 6 Process Costing

E 6-31

1.

Direct materials…………

…

$ 9,800

Direct labor………………

…

22,800

E 6-32

1.

a. Work in Process—Grinding

Work in Process—Molding

2. The journal entries for the job-order and process-costing systems are generally

E 6-33

1. Equivalent

Units

7,200 units completed………………………………………………………………

…

7,200

Finishing

Department

EXERCISES

Description

Journal

Date

Department

Molding

Department

Grinding

Credit

Debit

128,000

128,000

$143,200

13,800

$ 15,200

33,600

6-9

CHAPTER 6 Process Costing

E 6-34

E 6-35

1. Unit Cost = $174,000/75,000 = $2.32 per unit

E 6-36

1. Unit Cost = $1,100,000/220,000…………………………………………………

…

$5.00

2. Cost of units transferred out (196,000 × $5.00)………………………………

…

$ 980,000

3. The weighted average method is simpler to use than FIFO, but it does not reflect

the unit cost as well if costs are changing significantly from one period to the next.

FIFO calculates the unit cost using only costs of the current period and output of the

E 6-37

Units to account for:

Units in beginning work in process……………………………

…

91,500

…

6-10

CHAPTER 6 Process Costing

E 6-38

Units to account for:

Units in beginning WIP……………………………………………………………

…

25,000

E 6-39

Physical flow:

Units to account for: Units to account for:

Units in beginning WIP……

…

20,000 Units completed……………

…

50,000

Costs to account for:

Costs in beginning WIP…………………………………………………………… $ 93,600

UNIT INFORMATION

COST INFORMATION

Cooking Department

Production Report

For the Month of April

(Weighted Average Method)

CHAPTER 6 Process Costing

E 6-39 (Continued)

Costs accounted for:

Transferred

Out Total

Goods transferred out

E 6-40

Materials Conversion

Units completed……………………..……………

…

60,000 60,000

E 6-41

1. Unit materials cost [($147,000 + $1,053,000)/240,000]………………………

…

$5.00

…

2. Cost transferred out (180,000 × $6.13)…………………………………….….

…

$1,103,400

Cost of ending WIP:

E 6-42

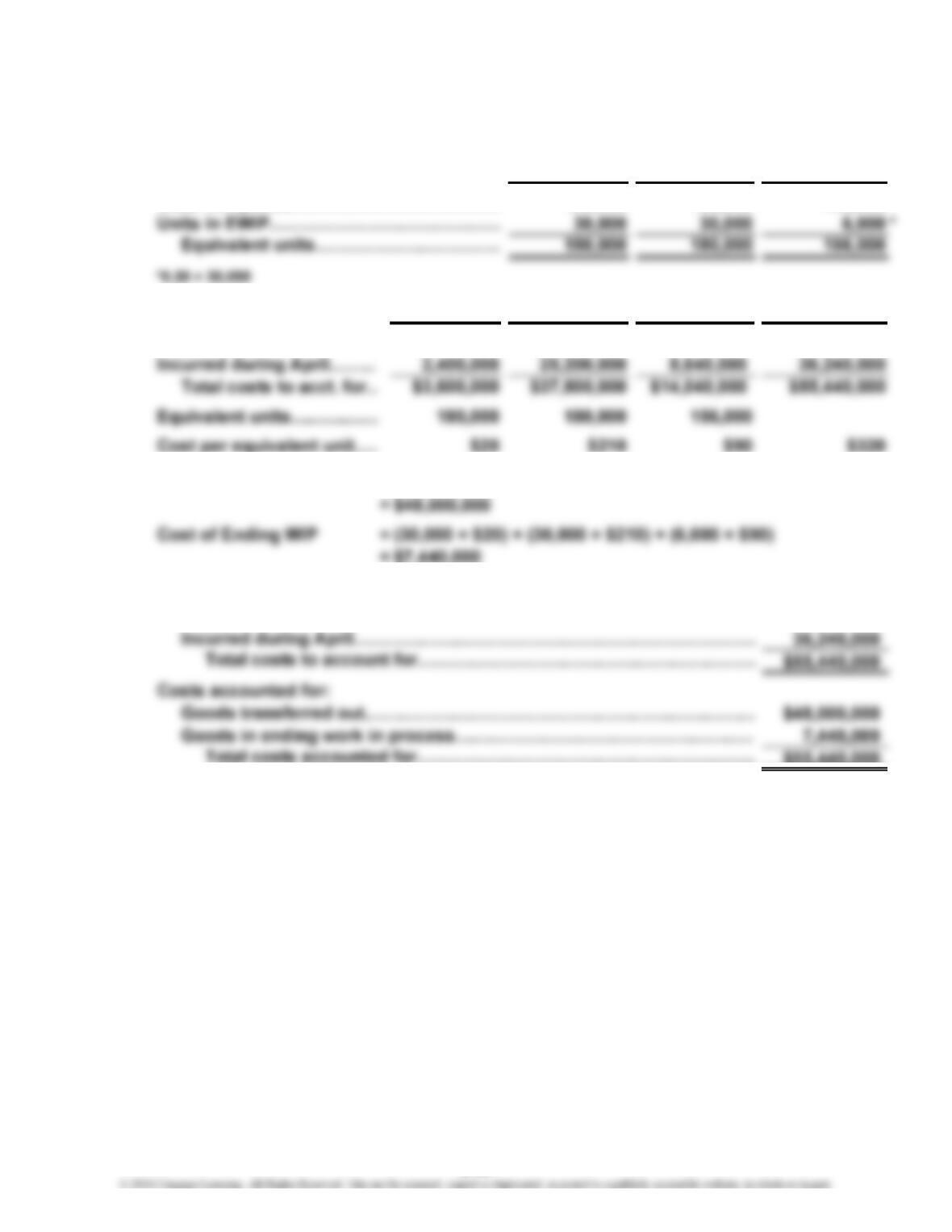

1. Units to account for: Units accounted for:

Ending

Work in Process

CHAPTER 6 Process Costing

E 6-42 (Continued)

*Calculation:

2. Transferred-In Materials Conversion

Units transferred out……………

…

120,000 120,000 120,000

E 6-43

1. Unit transferred-in cost [($2,100 + $30,900)/75,000]……..…………

…

$0.44

…

…

E 6-44

Units started and completed……..……………………………………

…

27,000

…

…

E 6-45

1. Unit Cost = $14,000/7,840……………………………………….………

…

$1.79

2. Cost of ending work in process ($1.79 × 2,400)……………..………

…

$ 4,296

6-13

CHAPTER 6 Process Costing

P 6-46

1. Mixing department:

a. Units Transferred to Tableting = Total Units* – Ending WIP

2. Tableting department:

3. The solution is to convert the transferred-in units to the same unit of measure as

the output for the tableting department. Each bottle has eight ounces of transferred-

P 6-47

1. Units to account for:

Units in beginning work in process………..…………………

…

60,000

Units started during the period……………..…………………

…

120,000

PROBLEMS

CHAPTER 6 Process Costing

P 6-47 (Continued)

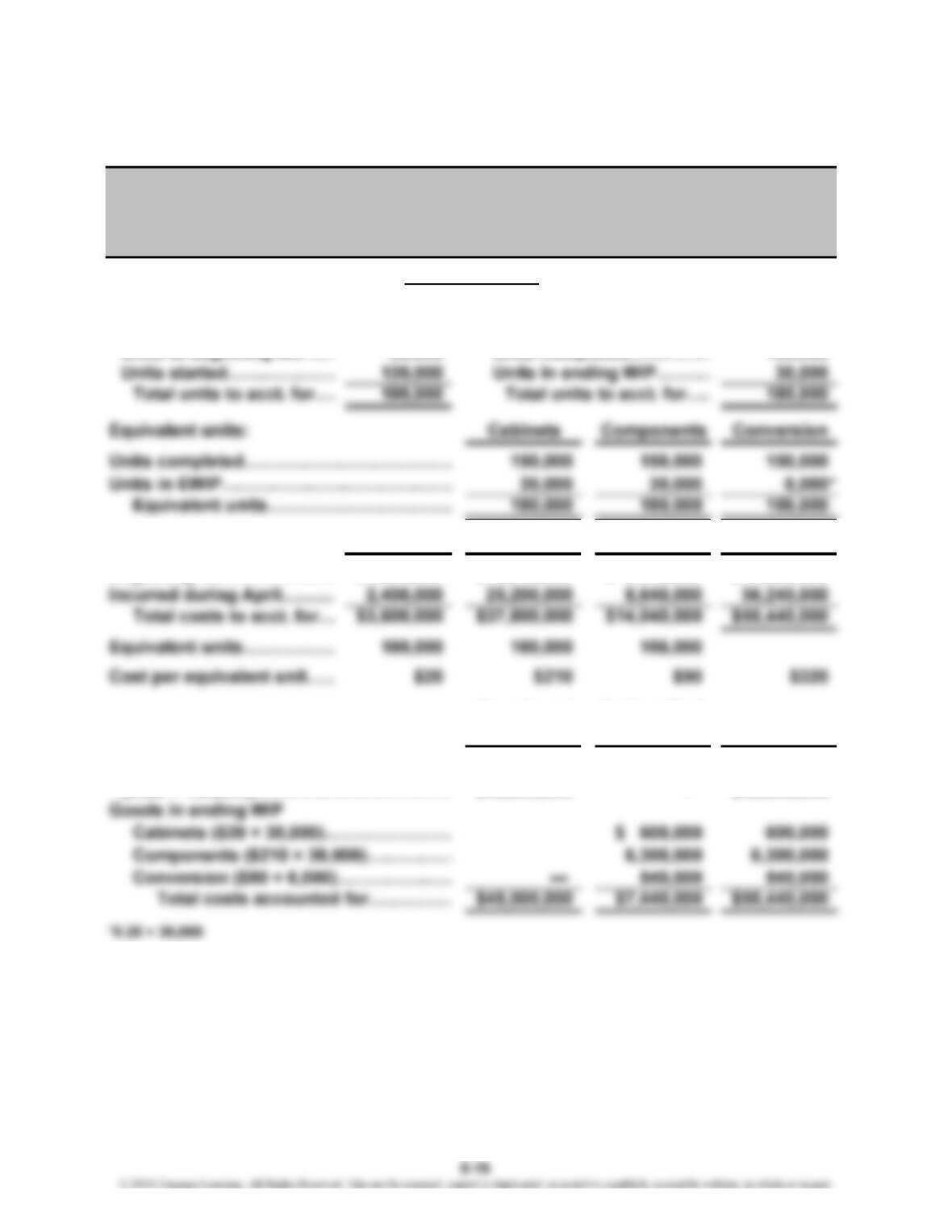

2. Cabinets Components Conversion

Units completed……………………………… 150,000 150,000 150,000

3. Costs to account for: Cabinets Components Conversion Total

Beginning WIP……………

…

$1,200,000 $12,600,000 $ 5,400,000 $19,200,000

4. Costs Transferred Out = 150,000 × $320

5. Costs to account for:

Beginning work in process………..…………………………………………

…

$19,200,000

…

6-15

CHAPTER 6 Process Costing

P 6-48

1.

Physical flow:

Units to account for: Units accounted for:

Units in beginning WIP…

…

60,000 Units completed…………

…

150,000

Costs to account for: Cabinets Components Conversion Total

Beginning WIP……………… $1,200,000 $12,600,000 5,400,000$ $19,200,000

Transferred Ending Work

Costs accounted for: Out in Process Total

Goods transferred out

($320 × 150,000)……………………………

…

$48,000,000 — $48,000,000

Unit Information

Assembly Department

Production Report

For the Month of April

(Weighted Average Method)

CHAPTER 6 Process Costing

P 6-48 (Continued)

2. Although the answers may vary, some essential elements should be mentioned in

the report. The job cost sheet summarizes the manufacturing activity for a job,

whereas the production report summarizes the manufacturing activity in a process

P 6-49

1. Units to account for:

Units in beginning work in process (60% complete)………….

.

40,000

Units started during the period………………..…………………

…

120,000

2. Units completed…………………………………………..……………

…

120,000

Add: Units in Ending WIP × Fraction Complete

6-17

CHAPTER 6 Process Costing

P 6-49 (Continued)

4. First, calculate the cost per unit for the equivalent units in beginning

inventory (0.60 × 40,000 = 24,000 equivalent units in BWIP) = 24,000

Prior Period Unit Cost = $144,000/24,000…………………………………………… $6.00

Next, calculate the current-period (FIFO) cost per unit:

P 6-50

Physical flow:

Units to account for: Units accounted for:

Units in beginning WIP……

…

40,000 Units completed……………

…

120,000

…

Throw-Rug Department

Production Report

For the Month of August

(Weighted Average Method)

UNIT INFORMATION

6-18