1. Tactical decisions are short run in nature; they involve choosing among alternatives with an

immediate or limited end in view. Strategic decisions involve selecting strategies that yield a

long-term competitive advantage.

5. The salary of the supervisor of an assembly line with excess capacity is an example of an

irrelevant future cost for an accept-or-reject decision.

6. Yes. Suppose, for example, that sufficient materials are on hand for producing a part for 2 years.

After 2 years, the part will be replaced by a newly engineered part. If there is no alternative use

for the materials, then the cost of the materials is a sunk cost and not relevant in a make-or-buy

decision.

10. Yes. The incremental revenue is $1,400, and the incremental cost is only $1,000, creating a

net benefit of $400.

13

DISCUSSION QUESTIONS

SHORT-RUN DECISION MAKING:

RELEVANT COSTING

13-1

CHAPTER 13 Short-Run Decision Making

13-1. e

13-2. b

13-8. b

MULTIPLE-CHOICE QUESTIONS

13-2

CHAPTER 13 Short-Run Decision Making

CE 13-13

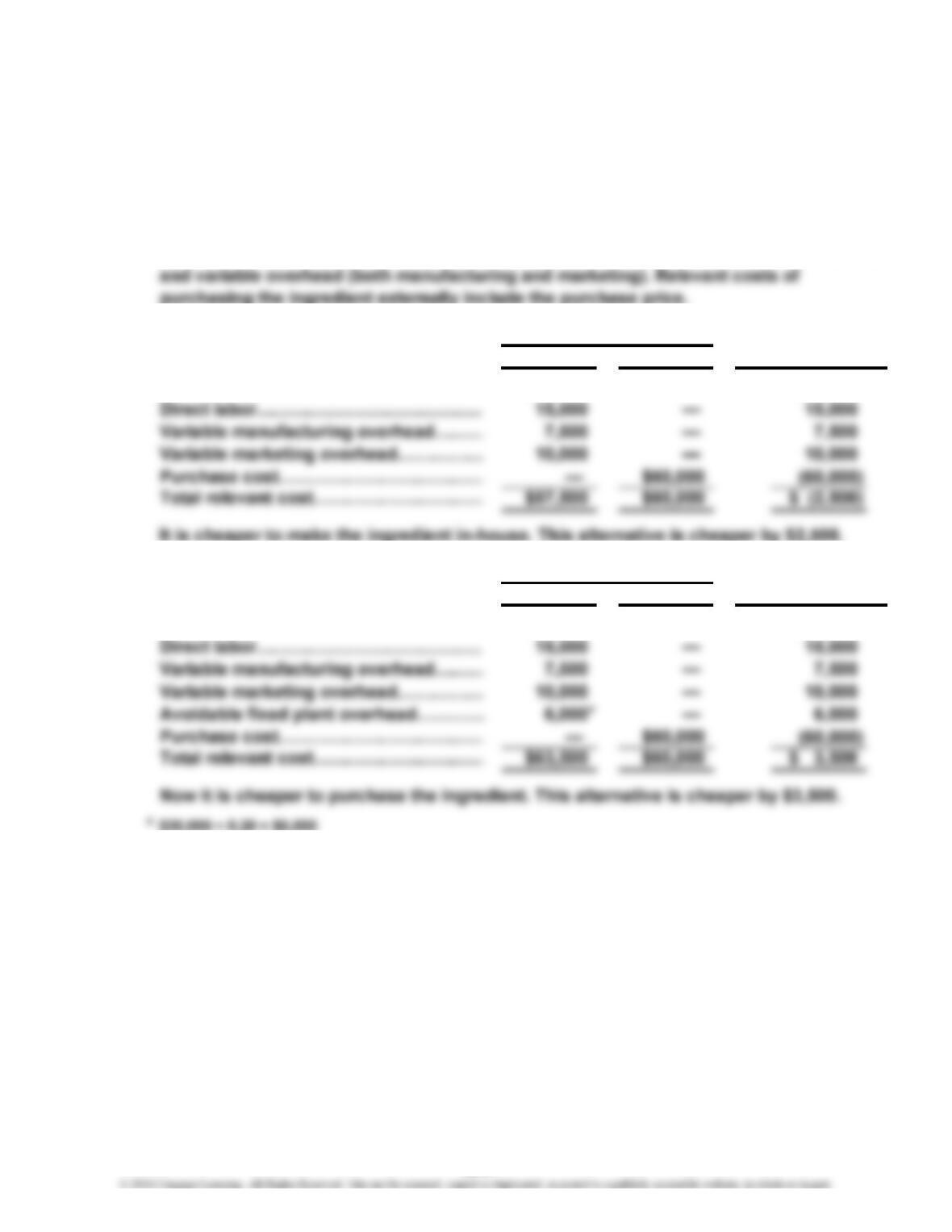

1. There are two alternatives: make the ingredient in-house or purchase it externally.

2. Relevant costs of making the ingredient in-house include direct materials, direct labor,

3.

Make Buy

Direct materials……………………………

…

$25,000 — $ 25,000

V

V

4.

Make Buy

Direct materials……………………………

…

$25,000 — $ 25,000

V

V

CORNERSTONE EXERCISES

Cost to Make

A

lternatives Differential

Cost to Make

A

lternatives Differential

13-3

CHAPTER 13 Short-Run Decision Making

CE 13-14

1. Relevant costs and benefits of accepting the special order include the sales price of

2. If the problem is analyzed on a unit basis:

A

ccept Reject

Price……………………………………

…

$ 5.00 — $ 5.00

V

…

—

CE 13-15

1. The two alternatives are to keep the parquet flooring line or to drop it.

2. The relevant benefits and costs of keeping the parquet flooring line to include sales

of $300,000, variable costs of $250,000, machine rent cost of $40,000*, and

3.

Keep Drop

Sales……………………………………

…

$ 300,000 —$ 300,000

Less: Variable expenses……………

…

(250,000) — (250,000)

…

—

Amount to

Accept

Differential

Benefit to

Accept

Differential

13-4

CHAPTER 13 Short-Run Decision Making

CE 13-16

1. Previous contribution margin of the strip line was $175,000. A 10% decrease in

sales implies a 10% percent decrease in total variable costs, so the contribution

2.

Keep Drop

Contribution margin…………… $305,000 $233,500 $ 71,500

Less: Machine rent……………

…

(75,000) (35,000) (40,000)

CE 13-17

1. Revenue from Logs = (8,000 × $495) = $3,960,000

Differential

Amount to Keep

*

13-5

CHAPTER 13 Short-Run Decision Making

CE 13-18

1. Swoop Rufus

Contribution margin per unit……………………………… $ 5.00 $15.00

2. Since the Swoop sweatshirt yields $50 of contribution margin per hour of machine

time (which is higher than the $45 contribution margin per hour of machine time

3. Total Contribution Margin of Optimal Mix = 70,000 units Swoop × $5

= $350,000

Note: Cornerstone Exercise 13-18 (as well as Cornerstone 13-6) clearly illustrates

a fundamentally important point involving relevant decision making with a

CHAPTER 13 Short-Run Decision Making

CE 13-19

1. Swoop Rufus

Contribution margin per unit………………………………… $ 5.00 15.00$

2. Since Swoop yields $50 of contribution margin per hour of machine time,

the first priority is to produce all of the Swoop sweatshirts that the the

market will take (i.e., demands). Machine time required for maximum amount

of Swoop = 40,000 maximum units × 0.10 hours of machine time required per

3. Total Contribution Margin of Optimal Mix = (40,000 units Swoop × $5) +

(9,091 units Rufus × $15)

= $336,365

CE 13-20

Price = Cost + Markup Percentage × Cost

CE 13-21

1. Desired Profit = 0.25 × Target Price

60 minutes

60 minutes

13-7

CHAPTER 13 Short-Run Decision Making

E 13-22

E 13-23

Steps in Austin’s decision:

Step 1: Define the problem. The problem is whether to continue studying at his

present university or to study at a university with a nationally recognized

engineering program.

Step 4: Total the relevant costs and benefits for each feasible alternative. No specific

event is listed for this step, although we can assume that it was done, and

that three schools were selected as feasible since Event j mentions that two

of three applications met with success.

EXERCISES

13-8

CHAPTER 13 Short-Run Decision Making

E 13-24

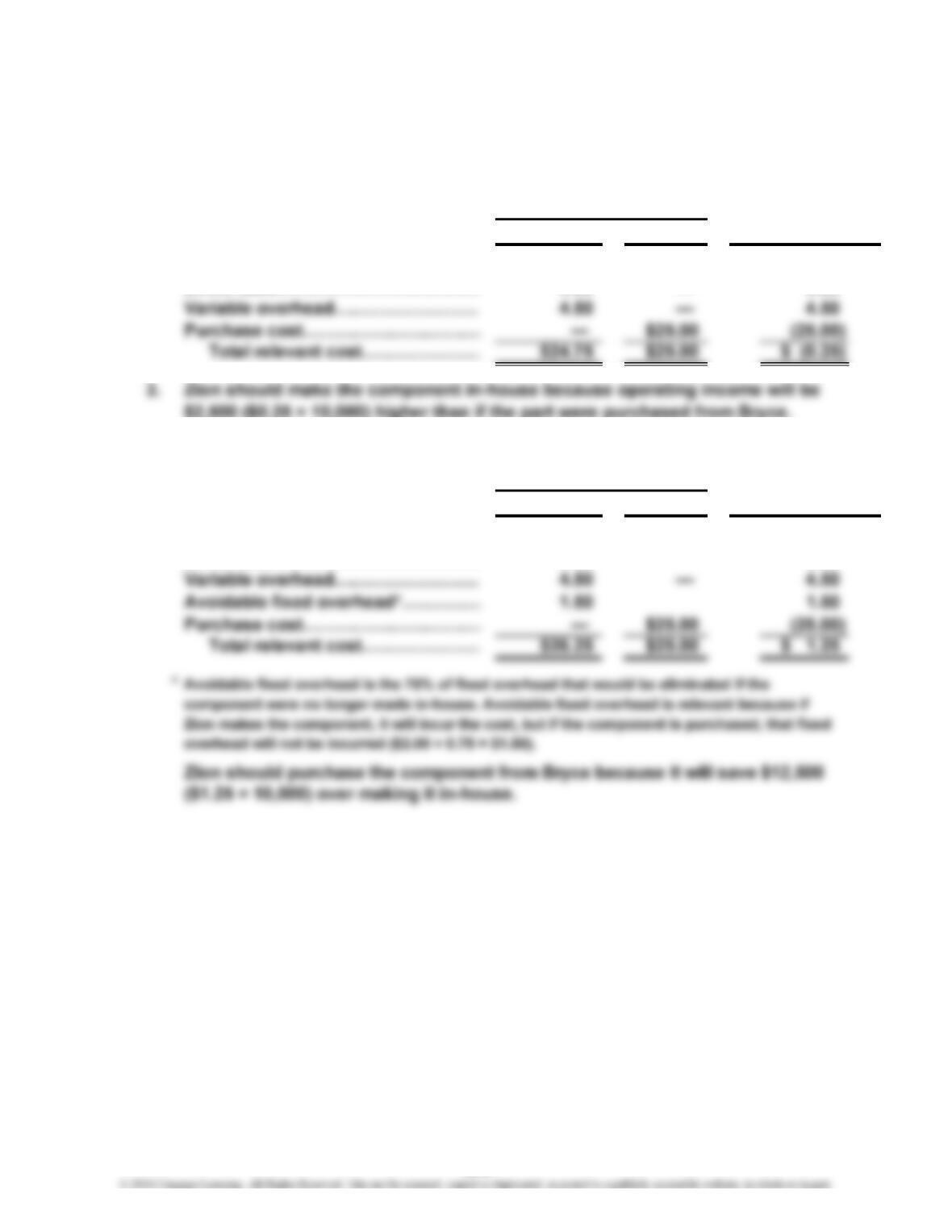

1. The two alternatives are to make the component in-house or to buy it from Bryce.

2.

Make Buy

Direct materials………………………

…

$12.00 — $ 12.00

Direct labor……………………………

…

8.25 — 8.25

E 13-25

1.

Make Buy

Direct materials………………………

…

$12.00 — $ 12.00

Direct labor……………………………

…

8.25 — 8.25

V

…

A

lternatives Differential

A

lternatives Differential

Cost to Make

Cost to Make

13-9

V

CHAPTER 13 Short-Run Decision Making

E 13-25 (Continued)

2. As the percentage of avoidable fixed cost increases (above 75%), total relevant

costs of making the component increases, causing the “purchase” decision to

be more financially appealing (compared to the “make” option) than it was when

3. Total relevant avoidable fixed cost would need to decrease by $12,500. Total

relevant make costs of $262,500 need to decrease to $250,000 to equal the total

relevant buy costs. Holding all other relevant make costs constant, this decrease

of $12,500 ($262,500 – $250,000) in fixed cost would reduce the total relevant

13-10

CHAPTER 13 Short-Run Decision Making

E 13-26

1. The two alternatives are:

2. Direct materials…………………

…

$3.10

Direct labor………………………

…

2.25

3. The statement that “existing sales will not be affected” indicates that there will be

E 13-27

In this case, it may be easier to deal with the total costs and revenues of the special

order:

E 13-28

If Petoskey drops Conway, overall profit will decrease by $75,000 as a result of the

CHAPTER 13 Short-Run Decision Making

E 13-29

If Petoskey drops Conway, overall profit will increase by $5,000. Contribution margin will

decrease by $75,000 as a result of the lost contribution margin ($300,000 – $225,000).

E 13-30

If Petoskey drops Conway, profit will decrease by $28,000. There will be a decrease of

$75,000 as a result of the lost Conway contribution margin ($300,000 – $225,000). Note

that the direct fixed expense for depreciation is a sunk cost and not relevant to the

E 13-31

1. Contribution Margin if HS Is Sold at Split-Off = $9 × 14,000 pounds

= $126,000

2. Contribution margin if HS is processed into CS

Revenue ($45 × 4,000)……………………………

…

$180,000

13-12

CHAPTER 13 Short-Run Decision Making

E 13-32

1. Reno Tahoe

2. Assuming no other constraints, the optimal mix is zero units of Reno and 820

units of Tahoe. Total painting department time is 2,460 hours per year; if all of

E 13-33

1. If 500 units of each product can be sold, then the company will first make and

sell 500 units of Tahoe (the product with the higher contribution margin per hour