1. The two major types of financial statement analysis discussed in this chapter are common-size

analysis and ratio analysis.

2. Horizontal analysis expresses line items of financial statements as a percentage of a prior-

period amount. Vertical analysis expresses the line item as a percentage of some other line item

4. Liquidity ratios measure the ability of a firm to meet its short-term obligations. Leverage ratios

measure the ability of a firm to meet both long- and short-term obligations. Profitability ratios

measure the earning ability of a firm.

5. Two types of standards used in ratio analysis are historical and industrial standards. Historical

standards allow one to assess trends over time. Industrial standards allow one to assess a

7. It may indicate a need to modify credit and collection policies to speed up the conversion of

receivables to cash.

8.

A

high inventory turnover ratio does not necessarily provide evidence of stockouts and disgruntled

10. The purchase alternative would increase the liabilities reported on the balance sheet. Increasing

liabilities may cause the company to violate some existing debt covenants. The lease payment,

however, had an immediate impact on the income statement rather than the balance sheet.

16 FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

16-1

12. For someone retiring, an annual income would be needed. Accordingly, companies that have

high yields and moderate payout ratios would be preferred to those that have a lower yield.

13. The price-earnings ratio can be compared with an investor’s expectation of future growth. If it is

low (high) based on this expectation, then the price is too low (high) and the price will change

based on the bidding that results.

16-2

CHAPTER 16 Financial Statement Analysis

16-1. b

16-5. d

16-6. c

MULTIPLE-CHOICE QUESTIONS

16-3

CHAPTER 16 Financial Statement Analysis

CE 16-11

Year 1 is the base year. Therefore, every dollar amount in Year 1 is 100% of itself.

Percent Year 1 Net Sales = $1,000,000/$1,000,000 = 100%

Dollars Percent Dollars Percent Dollars Percent

Net sales…………

…

$1,000,000 100% $1,100,000 110% $1,300,000 130%

Less: Cost of

…

Note: Percents are rounded to the nearest whole percent.

Dollar Amount of Line Item

CORNERSTONE EXERCISES

Year 1 Year 2 Year 3

Dollar Amount of Base Year Line Item

=Percent for a Line Item

16-4

CHAPTER 16 Financial Statement Analysis

CE 16-12

Since the analysis is based on net sales, net sales in each year equals 100% of itself.

Then, every line item on the income statement is expressed as a percent of that

year’s net sales.

Percent Year 1 Net Sales = $1,000,000/$1,000,000 = 100%

Percent Dollars Percent Dollars Percent

Net sales…………

…

100% $1,100,000 100% $1,300,000 100%

Less: Cost of

…

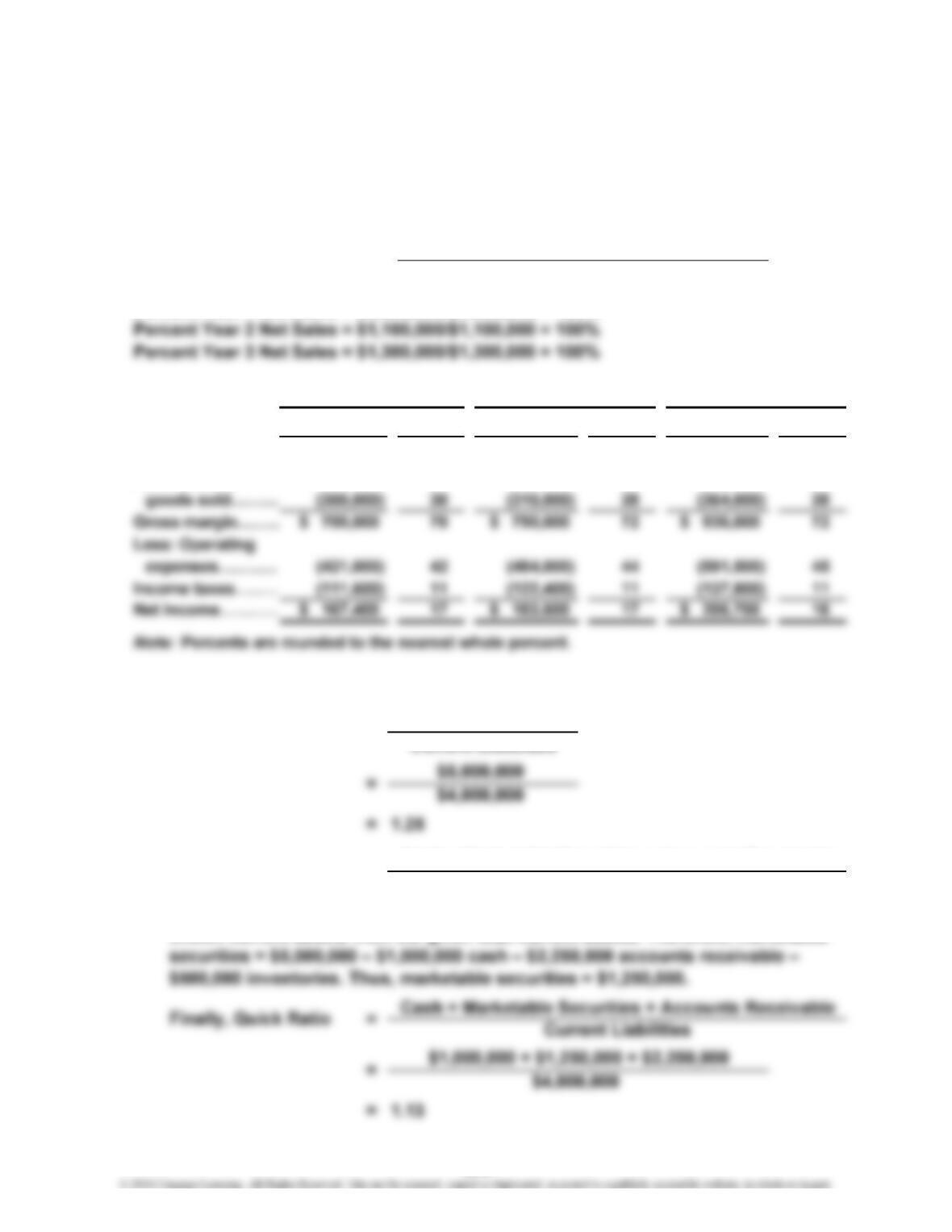

CE 16-13

You first need to calculate marketable securities by subtracting the specific

known current assets from the given total current assets. Therefore, marketable

$1,000,000

Dollar Amount of Line Item

Dollar Amount of Base Year Line Item

Year 2 Year 3

=Percent for a Line Item

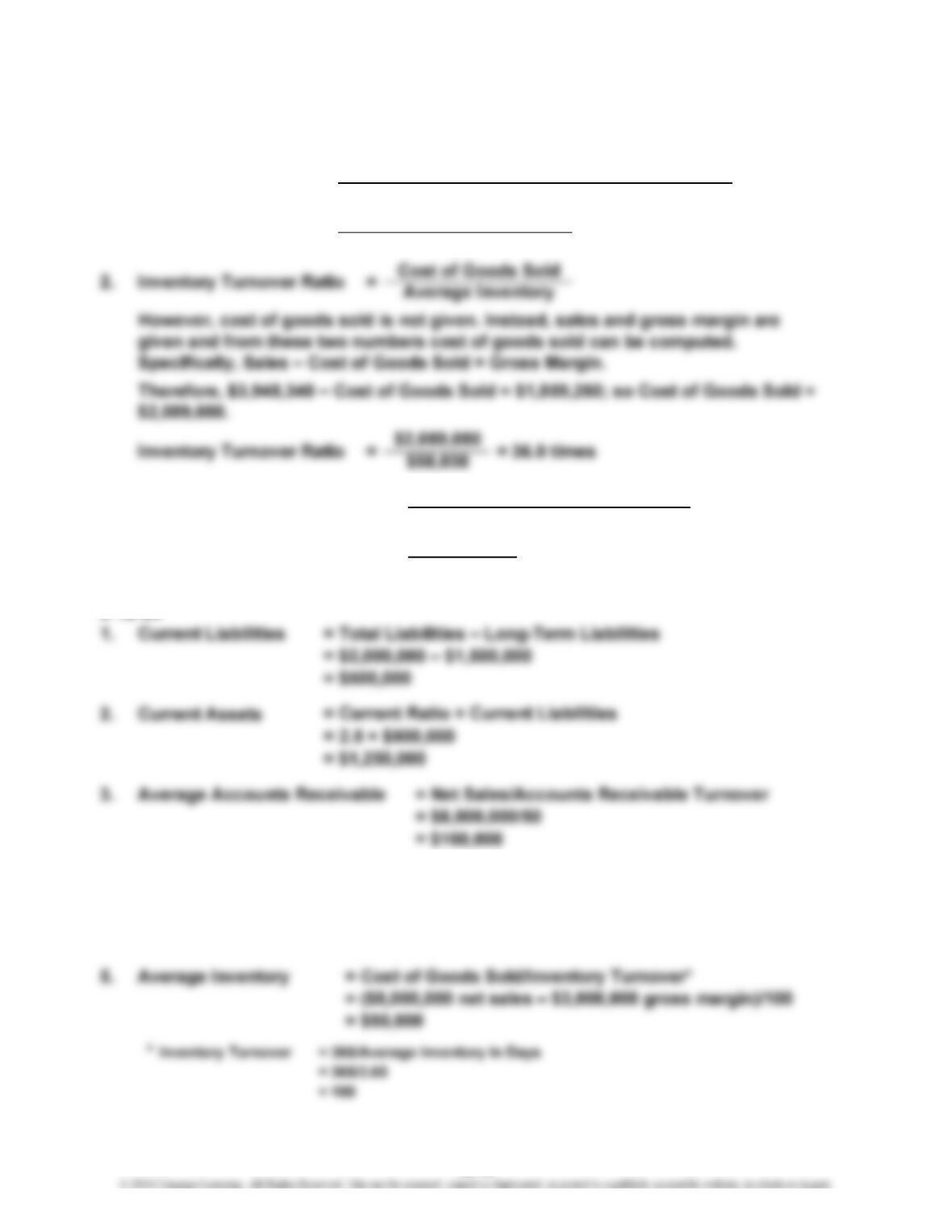

=Current Ratio

Year 1

Dollars

=

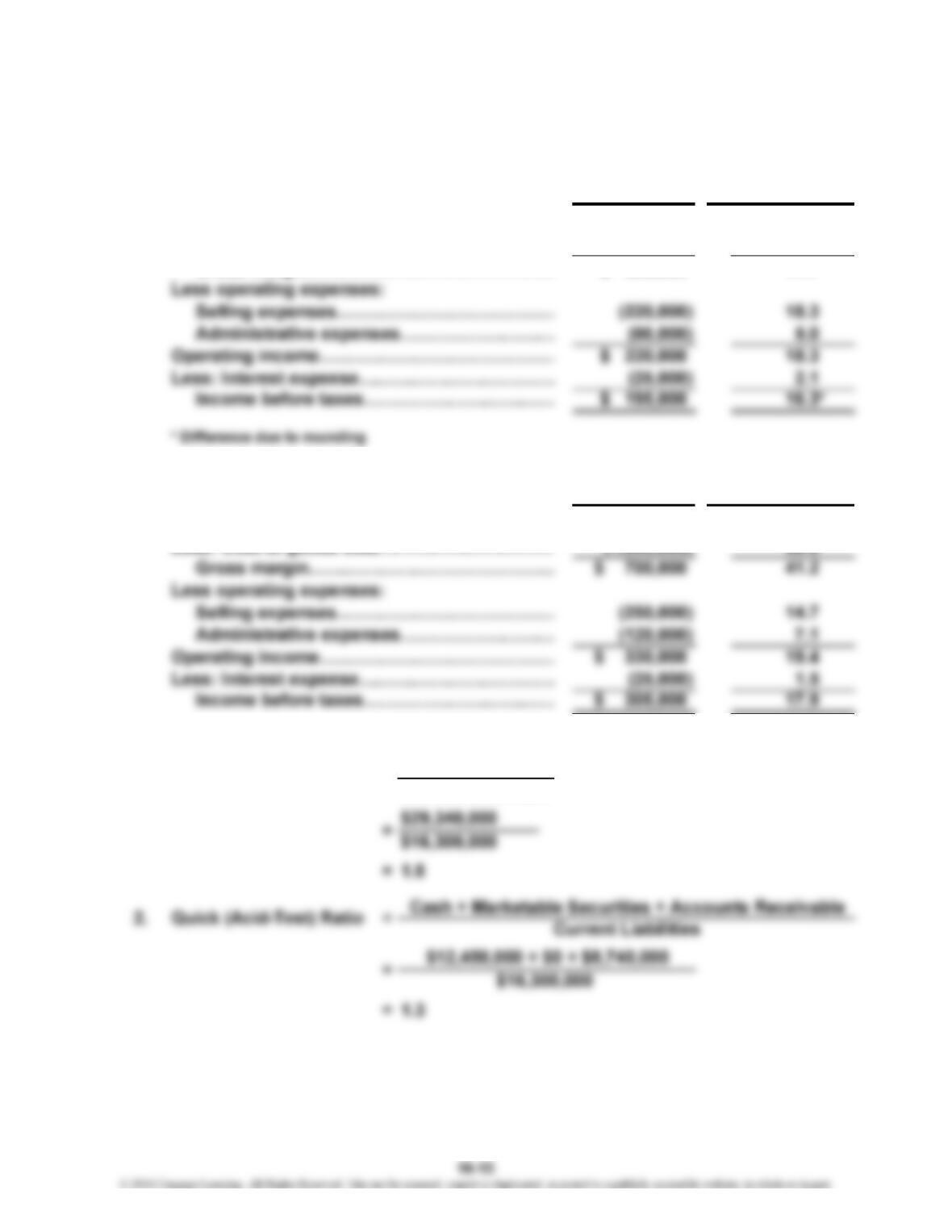

Cash + Marketable Securities + Accounts Receivable

Current Liabilities

Current Assets

Current Liabilities

Quick Ratio

2.

1.

16-5

CHAPTER 16 Financial Statement Analysis

CE 16-14

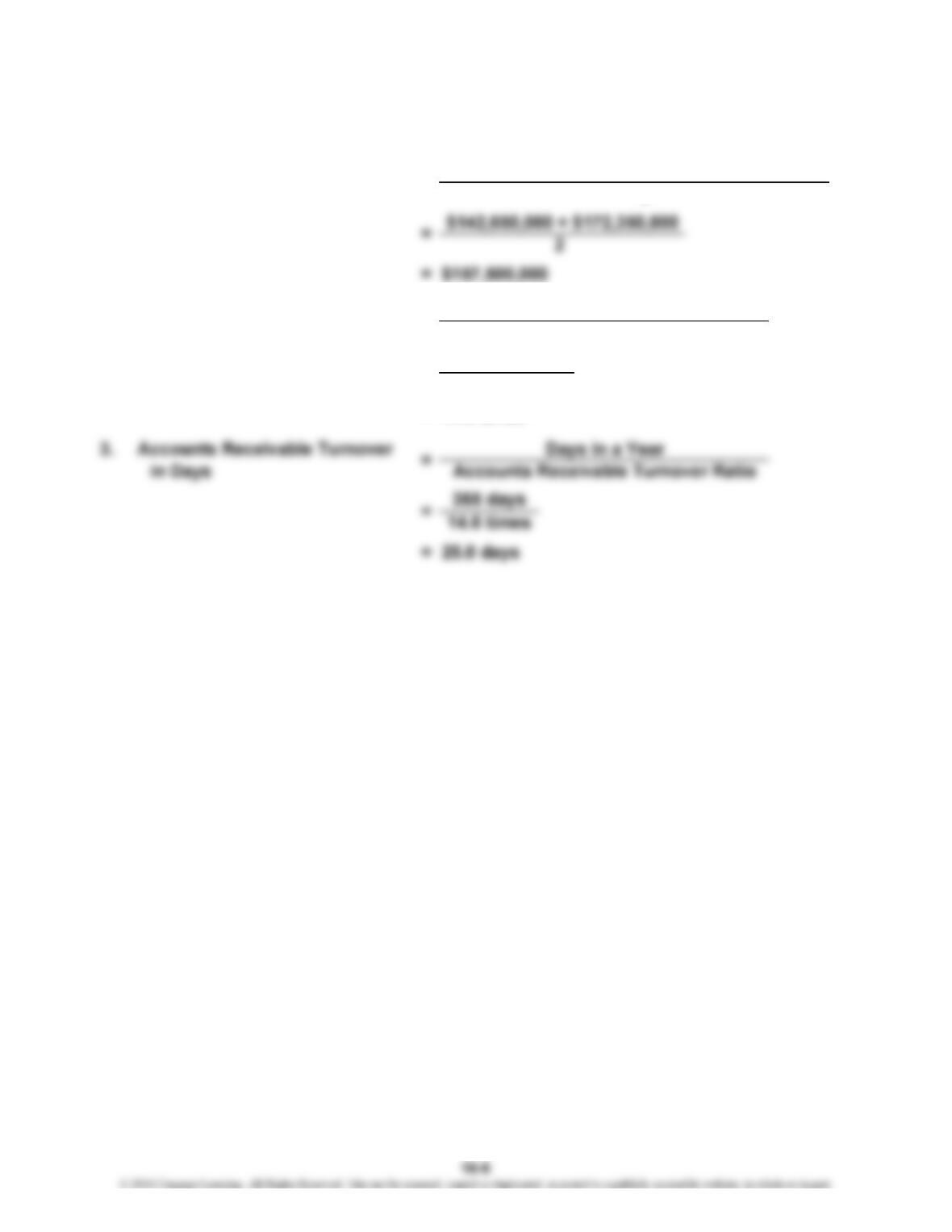

2. Accounts Receivable Turnover

Ratio

= 14.6 times

Net Sales

Average Accounts Receivables

$2,299,500,000

$157,500,000

Beginning Receivables + Ending Receivable

s

2

=

1. Average Accounts Receivables =

=

CHAPTER 16 Financial Statement Analysis

CE 16-15

4. Nikkola’s inventory turnover ratio is 30 times, which indicates that, on average,

the company converts finished goods inventory into sales 30 times a year.

Nikkola’s inventory turnover in days is 12.2, which indicates that, on average, the

company turns over finished goods inventory about every 12 days, which is

Beginning Inventory + Ending Inventory

2

2

=

= $58,500,000

=

$54,374,200 + $62,625,800

Average Inventory

1.

CHAPTER 16 Financial Statement Analysis

CE 16-16

CE 16-17

CE 16-18

CE 16-19

Interest Expense

Income Before Taxes + Interest Expense

$875,400

$4,635,750 + $875,400

Beginning Total Assets + Ending Total Assets

2

$6,521,576 + $8,121,576

$8,281,989

2

=

=

=

= 6.3 times

= $7,321,576

=

Times-Interest-Earned Ratio

Average Total Assets

1.

16-8

CE 16-20

1. Average Common

2. Return on Stockholders’

Equity

CE 16-21

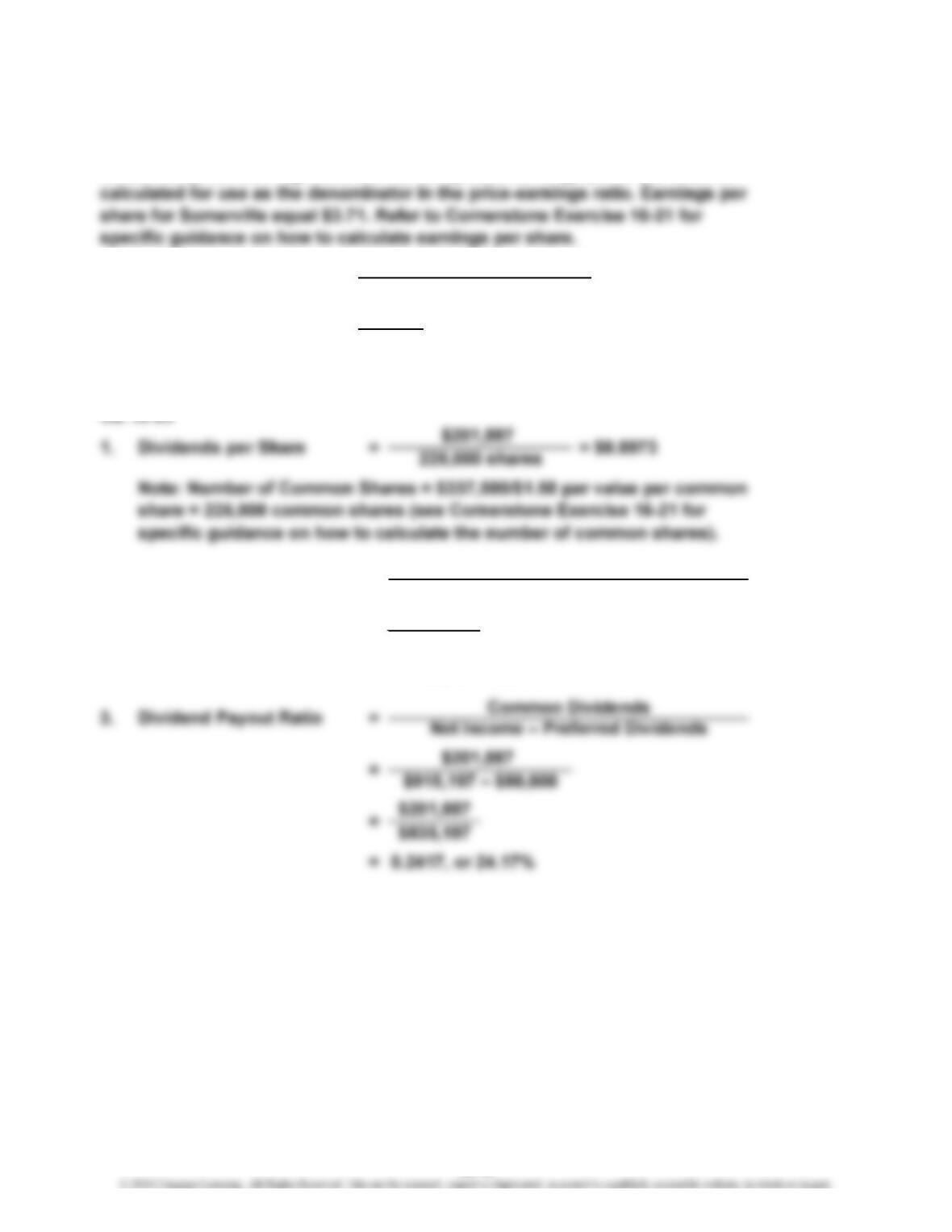

1. Preferred Dividends = $1,000,000 × 0.08 = $80,000

(Recall that the preferred shares pay a dividend of 8% as shown in

Somerville Company’s balance sheet.)

= $3.71, or $3.71 of earnings per share

Average Common Stockholders’ Equity

$4,316,655 + $4,949,965

Net Income – Preferred Dividends

$4,949,965.

=

CHAPTER 16 Financial Statement Analysis

CE 16-22

Before the price-earnings ratio can be computed, earnings per share must be

= 2.18329, or 2.18

CE 16-23

= 0.1108, or 11.08%

Market Price per Common Share

Dividend per Common Share

$8.10

$3.71

0.8973

$8.10

Market Price per Share

Earnings per Share

=

=

=

=

Price-Earnings Ratio

Dividend Yield2.

16-10

CHAPTER 16 Financial Statement Analysis

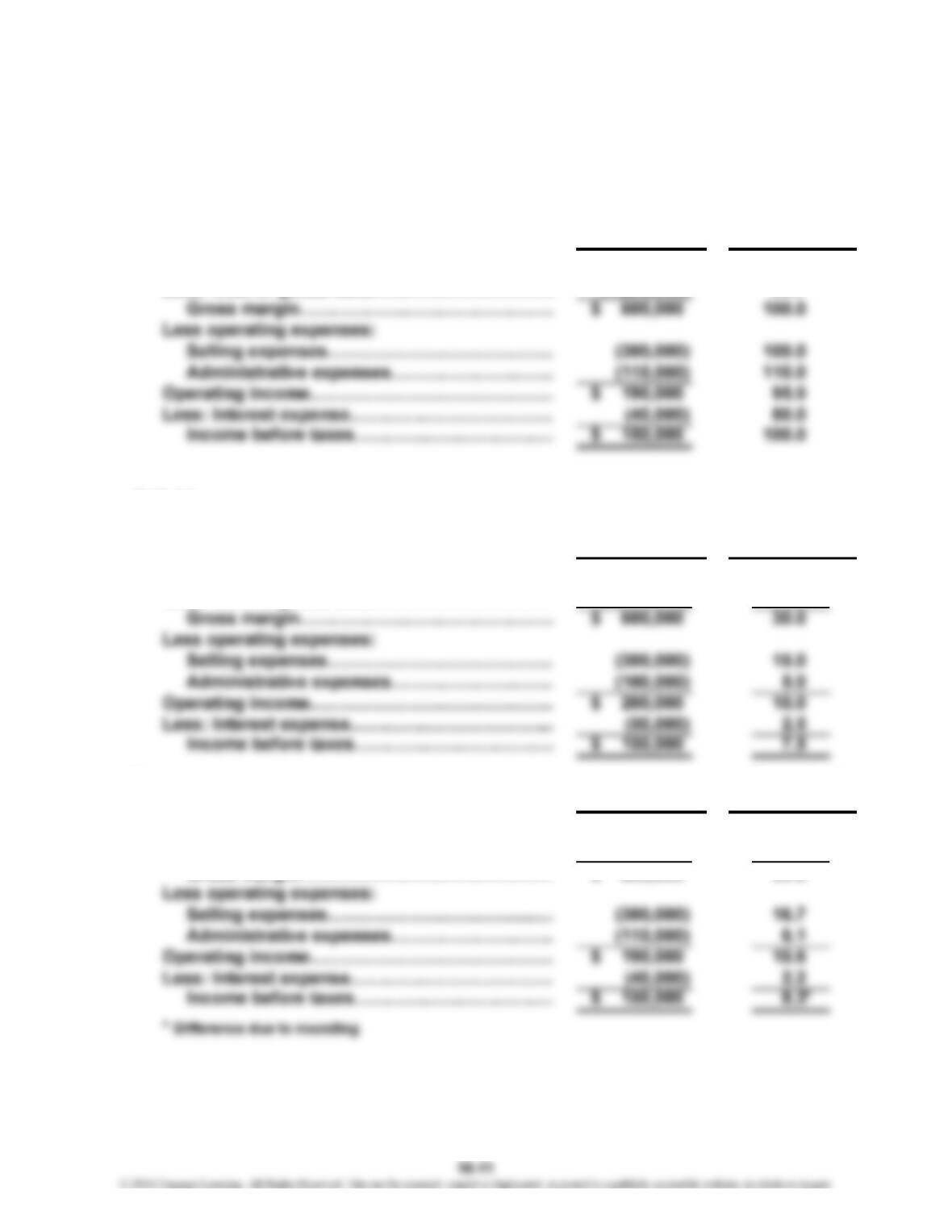

E 16-24

Sales…………………………………………………

…

$ 1,800,000 90.0%

Less: Cost of goods sold…………………………

…

(1,200,000) 85.7

E 16-25

1.

Sales…………………………………………………

…

$ 2,000,000 100.0%

Less: Cost of goods sold………………..………… (1,400,000) 70.0

2.

Sales…………………………………………………… $ 1,800,000 100.0%

Less: Cost of goods sold…………………………

…

(1,200,000) 66.7

Gross margin……………………………………

…

$ 600,000 33.3

EXERCISES

Year 1 Year 1 Sales

Percent o

f

Percent o

f

Y

ear 2

Y

ear 2 Sales

Year 1 AmountYear 2 Amount

Percent o

f

CHAPTER 16 Financial Statement Analysis

E 16-26

1.

Y

ear 2

Sales…………………………………..……………

…

$1,200,000 120.0%

Less: Cost of goods sold………………………

…

(700,000) 100.0

Gross margin……………………………………

…

$ 500,000 166.7

2.

Y

ear 3

Sales……………………………………………..…

…

$ 1,700,000 170.0%

Less: Cost of goods sold………………………

…

(1,000,000) 142.9

E 16-27

1.

Y

ear 1

Sales…………………………………………..……

…

$1,000,000 100.0%

Less: Cost of goods sold………………………

…

(700,000) 70.0

Percent of

Sales in Year 1

Percent of

Y

ear 1

Percent of

Y

ear 1

16-12

CHAPTER 16 Financial Statement Analysis

E 16-27 (Continued)

2.

Y

ear 2

Sales………………………………….………………

…

$1,200,000 100.0%

Less: Cost of goods sold………………………… (700,000) 58.3

Gross margin……………………………………

.

$ 500,000 41.7

3.

Y

ear 3

Sales………………………………….………………

…

$ 1,700,000 100.0%

Less: Cost of goods sold………………………… (1,000,000) 58.8

.

E 16-28

Percent of

Sales in Year 2

Percent of

Sales in Year 3

Current Assets

Current Liabilities

=

1.

Current Ratio

CHAPTER 16 Financial Statement Analysis

E 16-29

=

E 16-30

=

$408,550

+ Ending Accounts Receivables

2

=

=$419,000 + $398,100

2

Beginning Accounts Receivables

1.20

$3,000,000

$3,600,000

=

Average Accounts Receivable1.

Current Assets

Current Liabilities

Current Ratio1. =

CHAPTER 16 Financial Statement Analysis

E 16-31

=

E 16-32

=

$335,000,000 + $350,000,000

Beginning Accounts Receivable +

2

$342,500,000

2

$1,100,400 + $965,800

$1,033,100

2

=

=

Average Inventory1.

1. Average Accounts Receivable = Ending Accounts Receivable

2

=

Beginning Inventory + Ending Inventory

16-15

CHAPTER 16 Financial Statement Analysis

E 16-33

= 10.1 days

E 16-34

4. Marketable Securities = (Quick Ratio × Current Liabilities) – (Cash + Receivables)

= (2.0 × $500,000) – ($600,000 + $160,000)

= $1,000,000 – $760,000

= $240,000

365 days

36 times

Inventory Turnover Ratio

Days in a Yea

r

=

=

Inventory Turnover in Days3.

1. Average Inventory Beginning Inventory + Ending Inventory

2

$53,420 + $62,640

2 = $58,030

=

=

16-16

E 16-35

= 12.0 times

E 16-36

3. The debt ratio and debt-to-equity ratio are commonly used measures of a

company’s financial riskiness. As calculated in Requirement 1, Busch’s debt ratio

is 0.80, which indicates that for every $1.00 of assets, Busch has taken on debt

of $0.80. Stated a bit differently, Busch has chosen to finance 80% of its assets

with debt. As calculated in Requirement 2, Busch’s debt-to-equity ratio is 4.05,

which indicates that for every $1.00 of equity, Busch has taken on $4.05 of

liabilities. Taken together, it appears as though Busch has chosen to pursue a

=

Income Before Taxes + Interest Expense

Interest Expense

$5,500,000 + $500,000

=Times-Interest-Earned Ratio

$500,000

16-17