CHAPTER 9 Profit Planning

P 9-47 (Continued)

d. Schedule 4: Direct Labor Budget

January February March Total

Units to be

produced

e. Schedule 5: Overhead Budget

January February March Total

Budgeted direct

9-21

CHAPTER 9 Profit Planning

P 9-47 (Continued)

f. Schedule 6: Selling and Administrative Expenses Budget

January February March Total

Planned sales

(Schedule 1)…………………

…

40,000 50,000 60,000 150,000

× Variable selling

and admistrative

CHAPTER 9 Profit Planning

P 9-47 (Continued)

g. Schedule 7: Ending Finished Goods Inventory Budget

Unit cost computation:

Direct materials:

Metal (10 lbs. × $8)…………………

…

$80

h. Schedule 8: Cost of Goods Sold Budget

Direct materials used (Schedule 3)

Metal (1,660,000 × $8)*…………………………………………

…

$13,280,000

Components (996,000 × $5)**…………………………………

…

4,980,000 $18,260,000

Direct labor used (Schedule 4)…………………………………

…

7,096,500

…

9-23

CHAPTER 9 Profit Planning

P 9-47 (Continued)

i. Schedule 9: Budgeted Income Statement

Sales (Schedule 1)…………………………………………………………………

…

$30,750,000

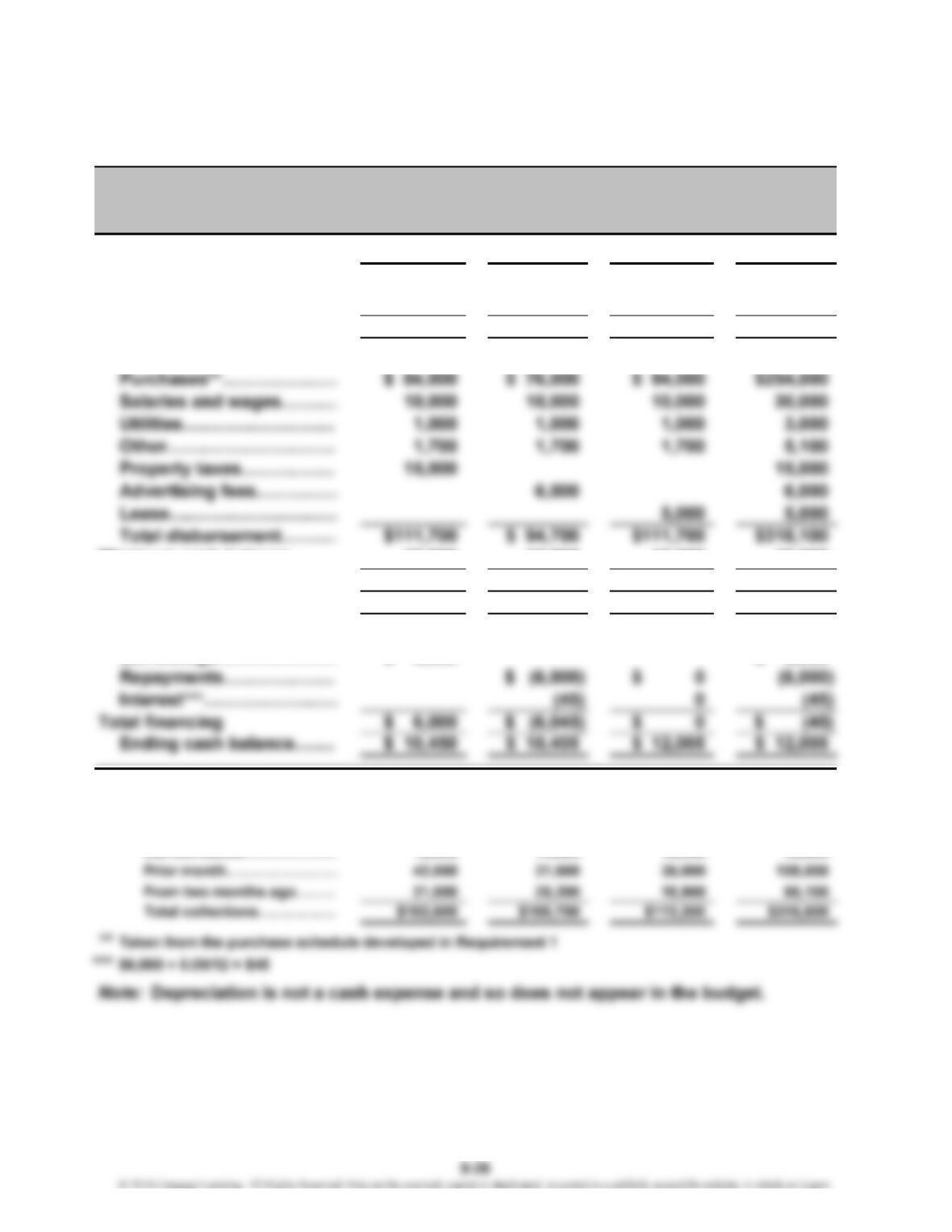

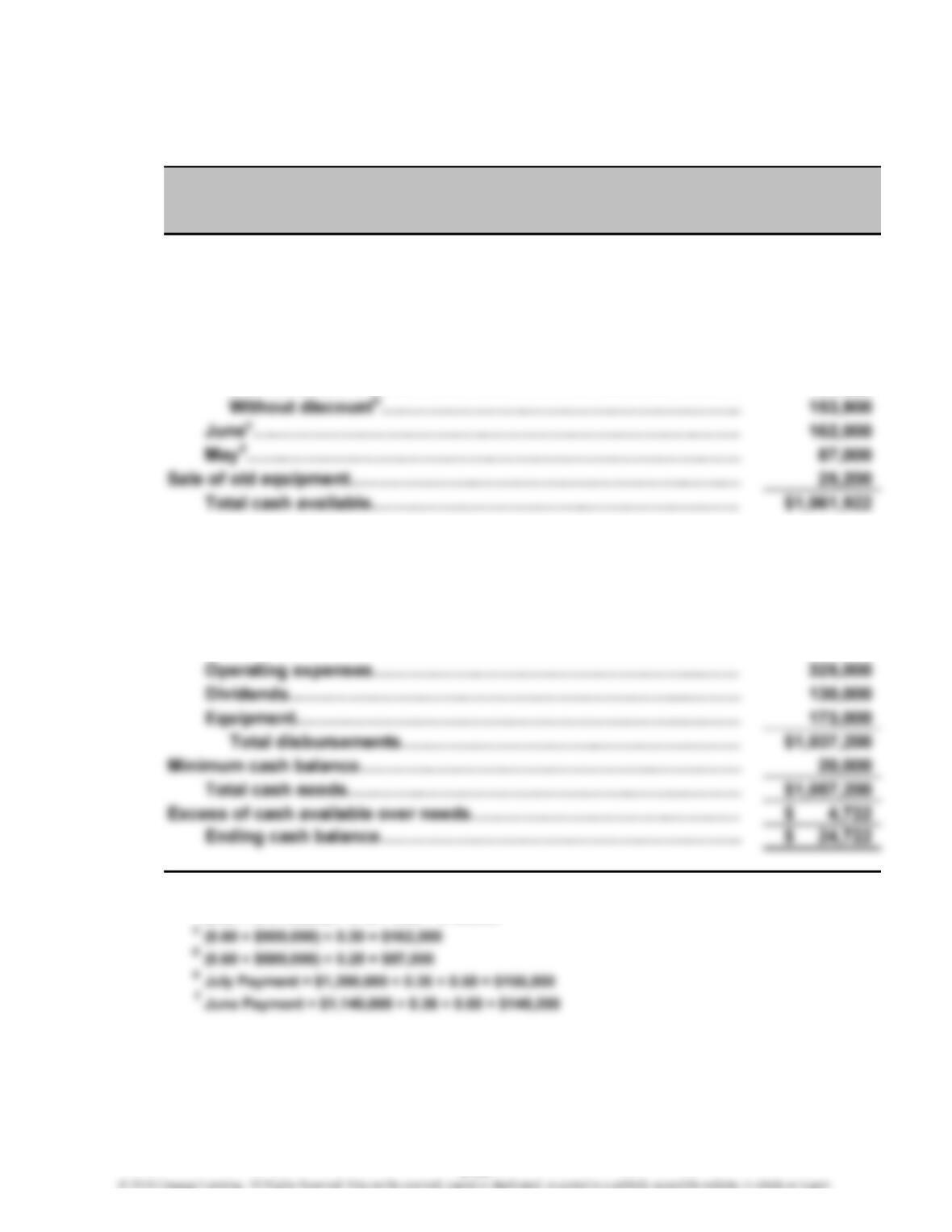

j. Schedule 10: Cash Budget

January February March Total

Beginning balance…… $ 400,000 $ 50,000 $ 495,004 $ 400,000

Cash receipts…………

…

8,200,000 10,250,000 12,300,000 30,750,000

Cash available………… $8,600,000 $10,300,000 $12,795,004 $31,150,000

Less disbursements:

Note: Depreciation is not a cash item and so does not appear in the cash budget.

2. Answers will vary.

CHAPTER 9 Profit Planning

P 9-48

1. To determine accounts payable as of June 30, a schedule of purchases will be

constructed. This schedule will also be used to build the cash budget.

Let X = Cost of Sales

*0.50 × Next Month’s Cost of Sales

Since purchases are paid for in the following month, accounts payable at the end

of June is $84,000. Inventory for June 30 is $36,000.

Accounts receivable for June 30 is computed as follows:

Assets L & OE

Cash…………………………………………………………………

…

$ 13,550

Accounts receivable………………………..……………………

…

88,200

Inventory…………………..………………………………………

…

36,000

CHAPTER 9 Profit Planning

P 9-48 (Continued)

2.

July

A

ugust September Total

Beginning cash balance……

…

$ 13,550 $ 10,450 $ 10,405 $ 13,550

Cash collections*……………

…

102,600 100,700 113,300 316,600

Total cash available……… $116,150 $111,150 $123,705 $330,150

Cash disbursements:

Minimum cash balance……

…

10,000 10,000 10,000 10,000

Total cash needs…………

…

$121,700 $104,700 $121,700 $328,100

Excess (deficiency)…………

…

$ (5,550) $ 6,450 $ 2,005 $ 2,050

Financing:

Borrowings………………

…

$ 6,000 $ 6,000

*Cash collections:

Cash sales…………………… $ 27,000 $ 30,000 $ 40,500 $ 97,500

Credit sales:

Current month………………

…

12,600 14,000 18,900 45,500

…

Grange Retailers

Cash Budget

For the Quarter Ending September 30, 2014

CHAPTER 9 Profit Planning

P 9-48 (Continued)

3.

Assets L & OE

Cash………………………………………………………………

…

$ 12,005

Accounts receivable a…………………………………………… 96,600

Inventory b…………………………………………………………

…

44,000

4. Cash budgets are important in loan decisions to help determine the company’s

ability to repay the loan. A statement of cash flows would also be helpful to see how

cash has been generated and used in the past. Another key report is the balance

Grange Retailers

Balance Sheet

September 30, 2014

CHAPTER 9 Profit Planning

P 9-49

When Eisenhower said “planning is everything,” he was no doubt referring to the

extensive planning process he undertook to plan the D-Day invasion of Normandy.

That plan was comprehensive and took into account the manpower needed,

9-28

CHAPTER 9 Profit Planning

P 9-50

Beginning cash balance………………………………………………………

…

$ 27,000

Collections:

Cash sales (0.40 × $1,140,000)………….……………………………… 456,000

Credit sales:

July:

With discounta…………………………………………………………

…

150,822

Less disbursements:

Raw materials:

Julye…………………………………………………………….………

…

June

f

…………………………………………………………….………

…

Direct labor………………………………………………………..………

…

…

a(0.60 × $1,140,000) × 0.45 × 0.50 × 0.98 = $150,822

b

(0.60 × $1,140,000) × 0.45 × 0.50 = $153,900

d

f

Feinberg Company

Cash Budget

For the Month of July

$ 156,000

148,200

105,000

9-29

CHAPTER 9 Profit Planning

P 9-51

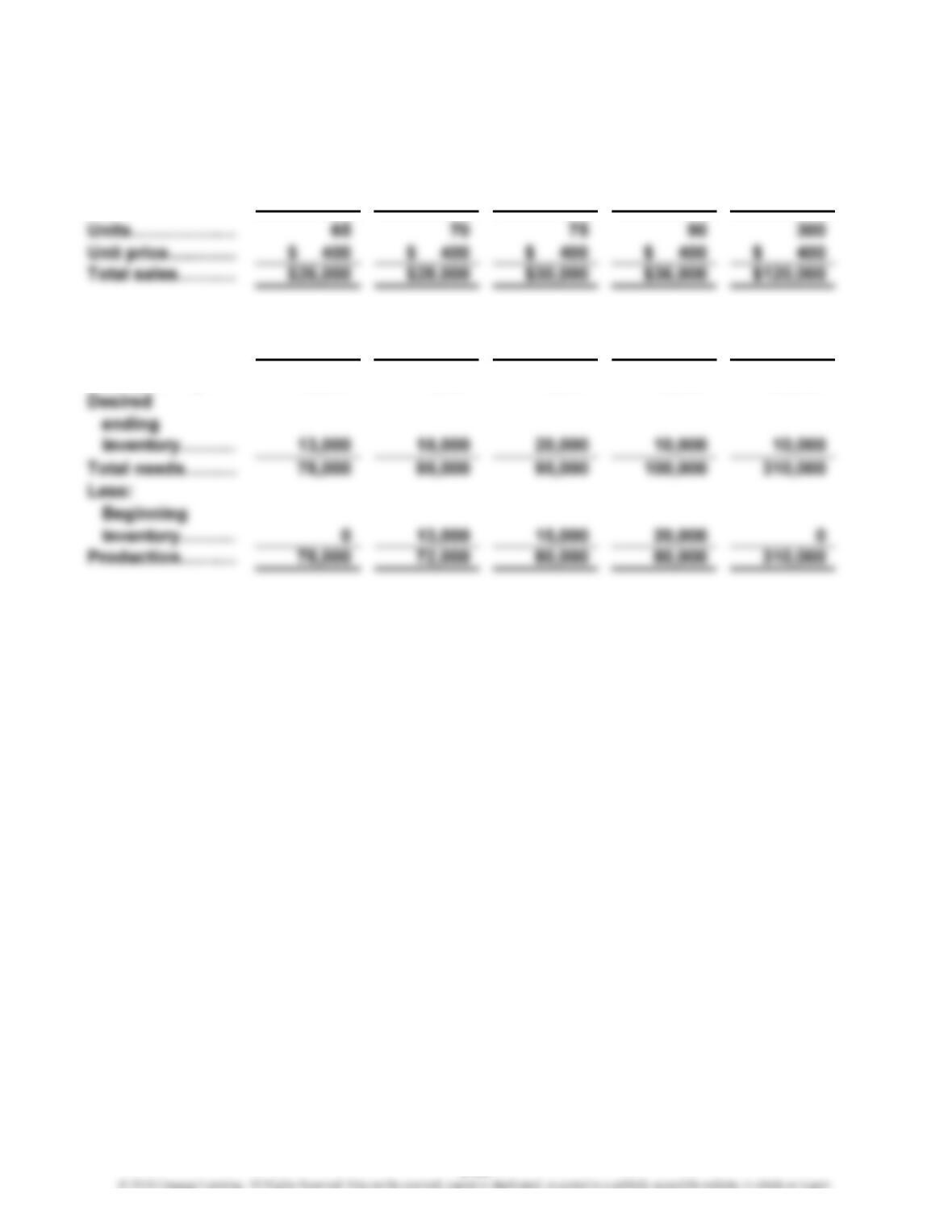

1. Schedule 1: Sales Budget (units and budgeted sales in thousands)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

2. Schedule 2: Production Budget

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Sales (Sch. 1)…… 65,000 70,000 75,000 90,000 300,000

9-30

CHAPTER 9 Profit Planning

P 9-51 (Continued)

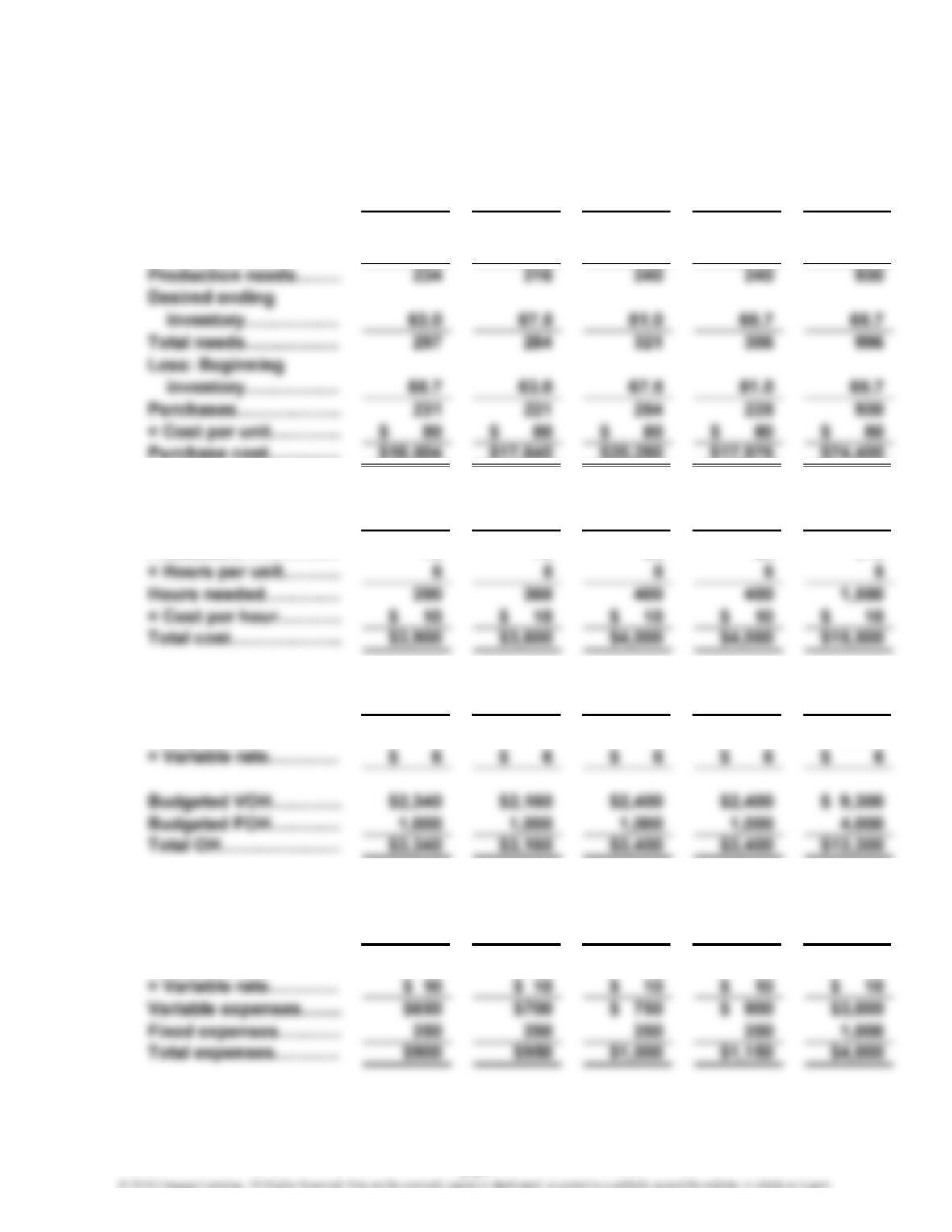

3. Schedule 3: Direct Materials Purchases Budget (in thousands)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Production……………

…

78 72 80 80 310

× Materials/unit………

…

33333

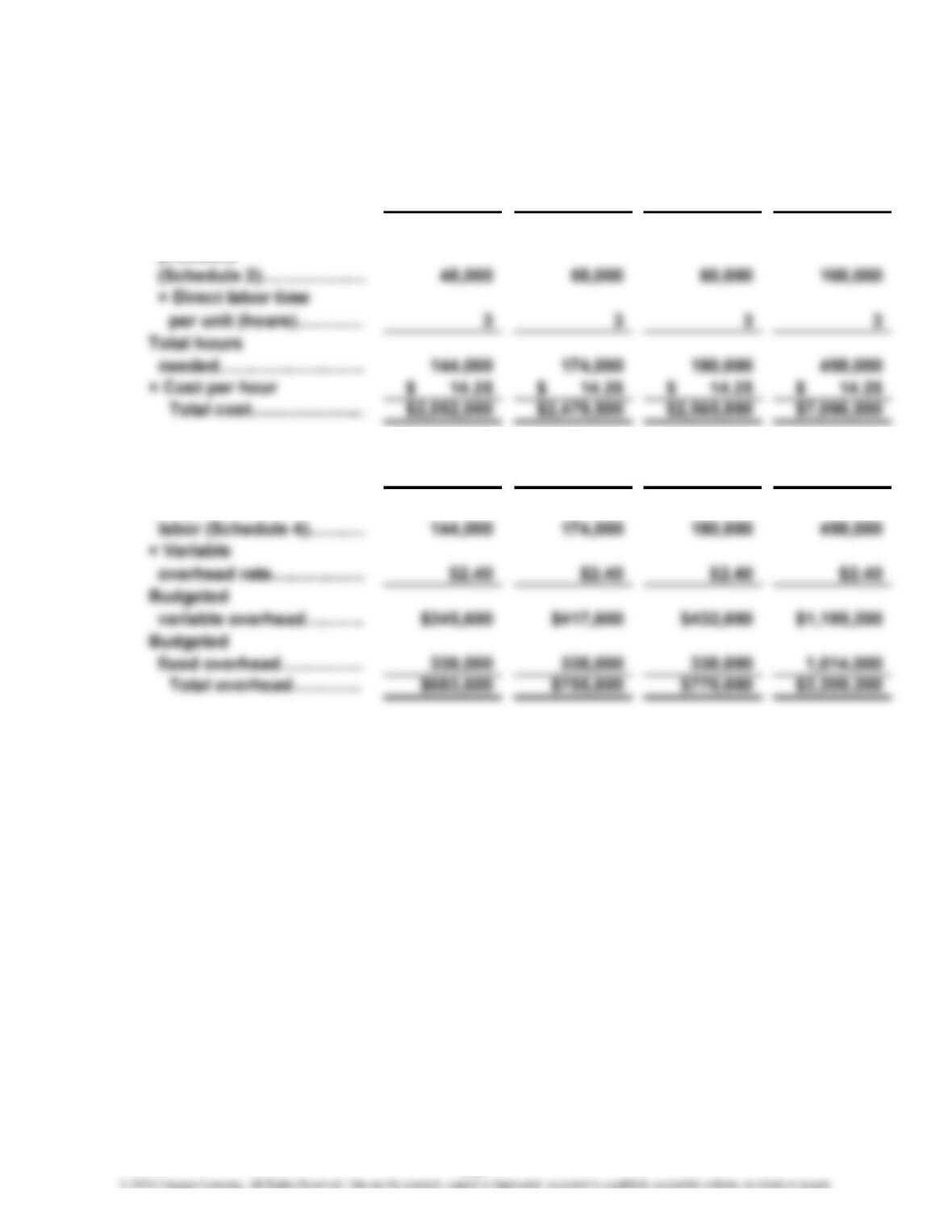

4. Schedule 4: Direct Labor Budget (in thousands, except per unit/hour data)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Production……………

…

78 72 80 80 310

…

5. Schedule 5: Overhead Budget (in thousands, except per unit/hour data)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Budgeted hours………

…

390 360 400 400 1,550

…

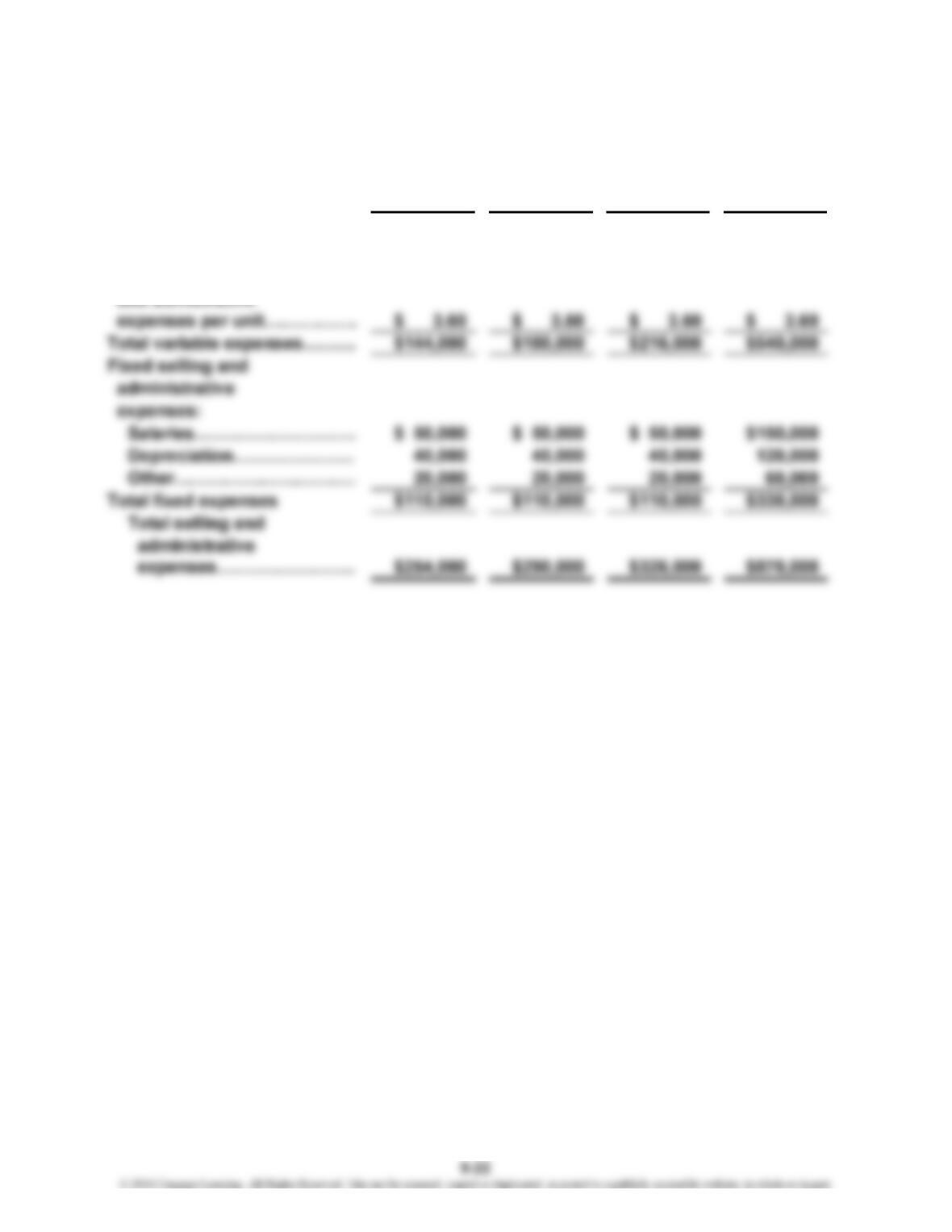

6. Schedule 6: Selling and Administrative Expenses Budget

(in thousands, except per unit/hour data)

Qtr. 1 Qtr. 2 Qtr. 3 Qtr. 4 Total

Planned sales…………

…

65 70 75 90 300

…

9-31