1. The only difference between absorption costing and variable costing is the way in which fixed

overhead costs are assigned. Under variable costing, fixed overhead is a period cost; under

absorption costing, it is a product cost.

2.

A

bsorption-costing income is greater because some of the period’s fixed overhead is placed in

inventory and not recognized as part of Cost of Goods Sold on the absorption-costing income

statement.

5. Ordering costs are the costs of placing and receiving an order. Examples include clerical

costs, documents, insurance, and unloading. Carrying costs are the costs of carrying

inventory. Examples include insurance, taxes, handling costs, and the opportunity cost of

capital tied up in inventory.

8. Reasons for carrying inventory include the following:

(a) to balance setup and carrying costs

(b) to satisfy customer demand

8ABSORPTION AND VARIABLE

COSTING, AND INVENTORY

MANAGEMENT

DISCUSSION QUESTIONS

A

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

10. The economic order quantity is the amount that should be ordered to minimize the

sum of ordering and carrying costs.

8-1. b

8-2. e

–

8-8. c ($15

–

$10)(20,000)

–

$75,000

MULTIPLE-CHOICE QUESTIONS

8-2

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

CE 8-13

1. Units Ending Inventory = Units Beginning Inventory + Units Produced –

Units Sold

CE 8-14

1. Units Ending Inventory = Units Beginning Inventory + Units Produced –

Units Sold

…

…

3. Value of Ending Inventory = 2,600 units × $92 = $239,200

CE 8-15

1. Direct materials………………………

…

$9

Direct labor……………………………

…

6

2.

Sales ($47 × 9,300)………………………………………………………………

…

$437,100

…

CORNERSTONE EXERCISES

Osterman Company

Income Statement Under Absorption Costing

For the Most Recent Yea

r

8-3

…

…

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

CE 8-16

1. Direct materials………………………… $ 9

Direct labor……………………………… 6

2.

Sales ($47 × 9,300)………………………….……………

…

$437,100

Less: Variable costs……………………………………

…

176,700

CE 8-17

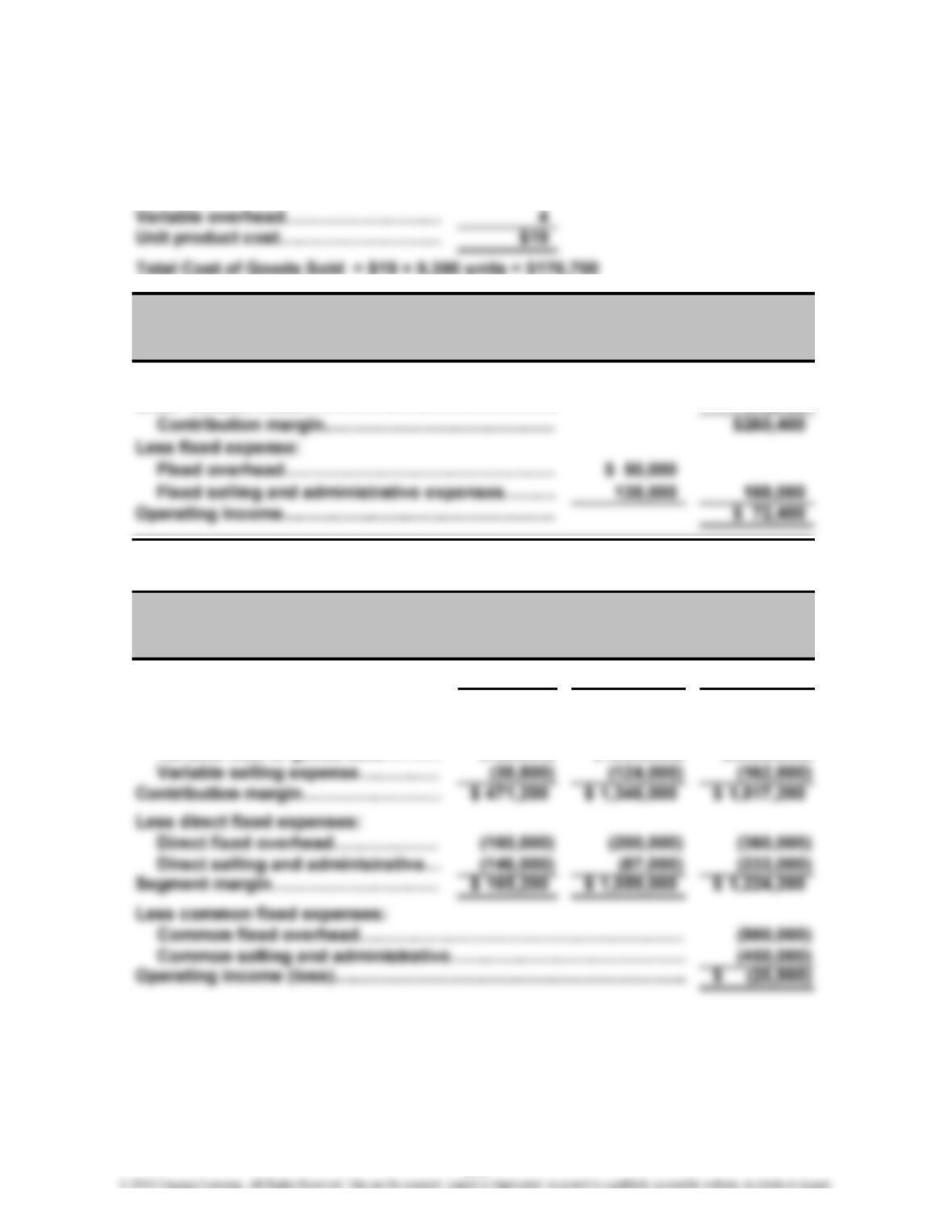

Poinsettias Fruit Trees Total

Sales……………………………………… $ 970,000 $ 3,100,000 $ 4,070,000

Less variable expenses:

V

ariable cost of goods sold………

…

(460,000) (1,630,000) (2,090,000)

V

Segmented Income Statement

For the Coming Year

Income Statement Under Variable Costing

For the Most Recent Yea

r

Gorman Nurseries Inc.

Osterman Company

8-4

V

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

CE 8-18

= 16 orders per year

=

=8,000 pounds

500 pounds

1. Number of Orders Annual Number of Pounds Used

Number of Pounds in an Order

8-5

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

CE 8-19

1. EOQ =

EOQ =

√

(2 × 8,000 × $5)/$2

= 200 pounds

4. Total Annual Carrying Cost under the EOQ Policy = ($200/2) × $2

= $200

CE 8-20

Reorder Point = Daily Usage × Lead Time

Reorder Point = 30 × 5 days = 150 pounds

CE 8-21

1. Safety Stock = (Maximum Daily Usage – Average Daily Usage) × Lead Time

Reorder Point = (30 pounds × 5 days ) + 25 pounds = 175 pounds

√2 × D × CO

CC

8-6

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-22

1. Unit Direct Materials Cost = $80,000/20,000 units = $4.00

2. Unit direct materials cost…………………………………………………

…

$ 4.00

Unit direct labor cost………………………………………………………

…

5.07

…

3. Ending Inventory in Units = 20,000 – 18,900 = 1,100 units

E 8-23

1. Unit direct materials cost ($123,000/50,000 units)……………………

…

$2.46

2. Variable-Costing Ending Inventory = $5.62 × (50,000 – 47,300) = $15,174

E 8-24

1. Unit direct materials cost ($596,000/80,000 units)……………………

…

$ 7.45

Unit direct labor cost ($104,000/80,000 units)…………………………

…

1.30

2. Unit direct materials cost (596,000/80,000 units)……………………… $7.45

…

3. Absorption-Costing Ending Inventory = $12.71 × 1,000 units* = $12,710

EXERCISES

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-25

1. Unit direct materials cost………………………

…

$ 9.95

Unit direct labor cost……………………………

…

2.75

2. Unit direct materials cost………………………

…

$ 9.95

…

3. Absorption-costing income:

Sales ($32 × 28,700)…………………………………………… $918,400

Less: Cost of goods sold ($16.85 × 28,700)………………

…

483,595

4. Variable-costing income:

Sales ($32 × 28,700)…………………………………………… $918,400

Less variable expenses:

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-26

1. Unit direct materials cost………………

…

$ 8.00

Unit direct labor cost……………………

…

4.00

2. Unit direct materials cost………………

…

$ 8.00

Unit direct labor cost……………………

…

4.00

E 8-27

1. Absorption-costing income:

Sales ($27 × 23,700)…………………………………………… $639,900

2. Variable-costing income:

Sales ($27 × 23,700)…………………………………………… $639,900

Less variable expenses:

8-9

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-28

1. Number of Units in Ending Inventory = Units Produced – Units Sold

= 16,000 – 15,200

= 800 units

2. Fixed Overhead Rate = Total Fixed Overhead ÷ Units Normal Production

= $23,000/20,000 units

3. Absorption-costing income…………… 45,000$

V

ariable-costing income………………

…

42,500

Difference……………………….………

…

2,500$

8-10

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-29

1.

Sweaters Jackets Total

Sales……………………….…………………

…

$ 210,000 $ 450,000 $ 660,000

Less variable expenses:

V

ariable cost of goods sold……………

…

(145,000) (196,000) (341,000)

V

ariable selling expense………………

…

(10,500) (22,500) (33,000)

2. For the company as a whole, an increase of $10,000 in fixed expense will

result in a decrease in operating income to $74,000 ($84,000 – $10,000). If

the equipment is for the sweaters line, then that line’s segment margin will

E 8-30

1. Small

Consumer Business

Computers Computers

Direct materials……………………………… $490 $1,180

V

…

V

and administrative expense.

Knitline Inc.

Segmented Income Statement

For the Coming Year

…

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-30 (Continued)

2.

Small

Consumer Business

Computers Computers Total

Sales……………………….………

…

$ 40,960,000 $ 134,000,000 $ 174,960,000

Less variable expenses:

E 8-31

1. Orders per Year = 17,280 units/864 units per order = 20 orders

2. Total Ordering Cost = $10 × 20 orders = $200

Paulson Computers Inc.

Segmented Income Statement

For the Coming Year