1. Cash equivalents such as money market funds and CDs are highly liquid investments that can be

readily converted into cash. They are treated as cash.

2. Operating activities are the ongoing, day-to-day, revenue-generating activities of an organization.

Investing activities involve the sale or purchase of long-term assets. Financing activities stem

from long-term liabilities and equity sources.

6. (1) Compute the change in cash for the period.

(2) Compute the cash flows from operating activities.

(3) Identify the cash flows from investing activities.

7. Accrual accounting allows a firm to recognize revenues before they are collected or to pay for

inputs before they are expensed. This practice creates the possibility of having a negative

operating cash flow while still reporting a positive net income.

8. Accrual accounting allows a firm to collect revenues that were recognized in a prior period and to

15 STATEMENT OF CASH FLOWS

DISCUSSION QUESTIONS

15-1

CHAPTER 15 Statement of Cash Flows

10. A decrease in a current liability means that cash payments to creditors were greater than the

expenses recognized during the period. An increase in a noncash current asset means that

more cash was paid than the expenses recognized. (As assets expire, they become expenses.)

13. Worksheets are an efficient, logical way of organizing the data needed to prepare a statement of

cash flows.

14. The worksheet approach is based on a transaction analysis. Using the beginning and ending

balances on the balance sheet, transactions are analyzed that impact cash flows. Debit and

15-2

CHAPTER 15 Statement of Cash Flows

15-1. c

15-2. b

15-11. e

15-12. c

MULTIPLE-CHOICE QUESTIONS

15-3

CHAPTER 15 Statement of Cash Flows

CE 15-17

a. Investing—use of cash

b. Financing—source of cash

CE 15-18

1. Change in cash: $1,130,000 – $700,000 = $430,000

CE 15-19

Net income……………………………………………………………………………

…

$ 900,000

Add (deduct) adjusting items:

CE 15-20

Sale of equipment…………………………………………………………………… $ 380,000

CORNERSTONE EXERCISES

CHAPTER 15 Statement of Cash Flows

CE 15-21

Issuance of bonds payable………………………………………………

…

$ 385,000

Payment of mortgage……………………………………..………………

…

(100,000)

CE 15-22

1.

Cash flows from operating activities:

Net income……………………………………..……

…

$ 900,000

Add (deduct) adjusting items:

Decrease in accounts receivable………………

…

167,500

…

2. The sum of the operating, investing, and financing cash flows must equal the

change in cash flow.

Blaylock Company

Statement of Cash Flows

For the Year Ended December 31, 201

4

15-5

…

CHAPTER 15 Statement of Cash Flows

CE 15-23

Income Cash

Statement Flows

Revenues……………………………………

…

$1,200,000 $ 68,500 * $1,268,500

Gain on sale of equipment………………

…

50,000 (50,000)

CE 15-24

2013 Debit

Assets:

Cash…………………………

…

$ 54,000 (1) $57,000 $111,000

Accounts receivable………

…

33,000 (2) 3,800 36,800

…

Liabilities and stockholders’ equity:

Accounts payable…………

…

$ 24,000 (7) 12,000 $ 36,000

…

Credit

Worksheet: Young Company

At December 31, 201

4

Adjustments

Transactions

2014

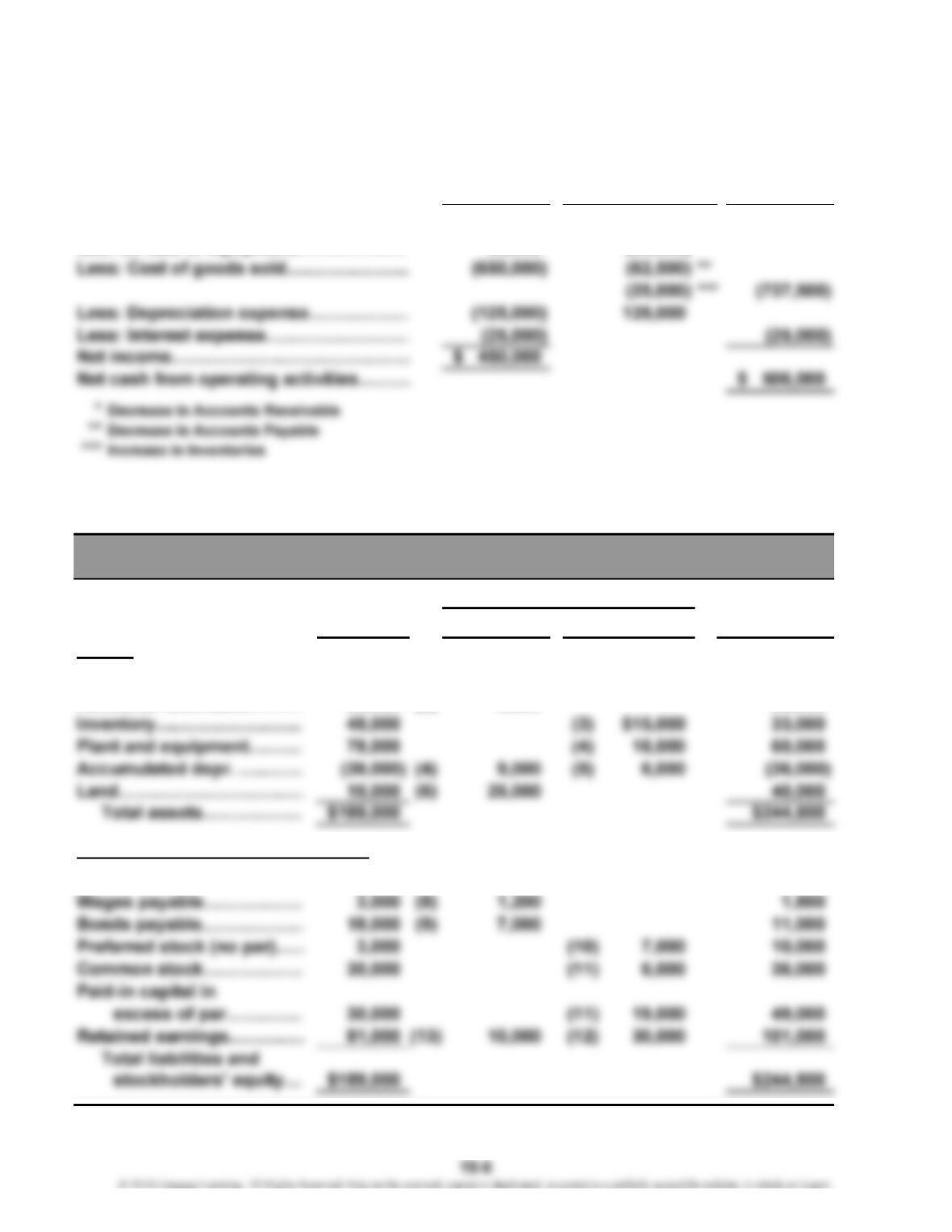

CE 15-24 (Continued)

Cash flows from operating activities:

Net income…………………………………………

…

(12) $30,000

…

…

…

Cash flows from investing activities:

Sale of equipment…………………………………

…

(4) 4,800

Cash flows from financing activities:

Reduction in bonds payable……………………

…

(9) 7,000

…

Debit Credit

Transactions

15-7

CHAPTER 15 Statement of Cash Flows

E 15-25

a. Investing—source of cash f. Investing—use of cash

E 15-26

a. Added to f. Added to

E 15-27

1. Note: Balances refer to prepaid rent account.

2. In determining operating cash flow under the indirect method, any increase in a

E 15-28

1. Cash flows from operating activities:

Net income……………………………………………………………………… $ 61,725

Add (deduct) adjusting items:

EXERCISES

15-8

CHAPTER 15 Statement of Cash Flows

E 15-28 (Continued)

2. From Requirement 1, the net operating cash without the change in accounts

payable is $8,475 ($18,600 – $10,125). Thus, the change in accounts payable

3. The operating cash flows are only $18,600, about half of what would be needed.

However, Hepworth has a large cash balance ($126,000) including this year’s

E 15-29

1. Cash flows from investing activities:

Purchase of bonds……………………………………………………………

…

$(200,000)

…

2. The negative cash flow from investing can be covered using cash from operating

and financing activities. Sources of cash for investment include operating cash

E 15-30

Cash flows from financing activities:

CHAPTER 15 Statement of Cash Flows

E 15-31

2013 2014

2.

Cash flows from operating activities:

Net income……………………………………………….…………………

…

$40,000

3. Change in Accounts Receivable = Operating Cash Flows without

Accounts Receivable

Indirect Method

Change

Oliver Company

Operating Cash Flows

15-10

CHAPTER 15 Statement of Cash Flows

E 15-32

Cash flows from operating activities:

Income Cash

Statement Flows

E 15-33

a. Financing activities

b. Operating activities—added to net income

c. Operating activities—deducted from net income

Adjustments

Oliver Company

Operating Cash Flows

Direct Method

E 15-34

Cash flows from operating activities:

Net income…………………………………….…………………………

…

$156,000

…

…

E 15-35

Cash flows from operating activities:

Income Cash

Statement Flows

Revenues…………………………

.

$ 1,500,000 $ (20,000) * $1,480,000

Adjustments

Direct Method

Piura Merchandising Corporation

Cash Flows from Operating Activities

For the Year Ended December 31, 2013

15-12

CHAPTER 15 Statement of Cash Flows

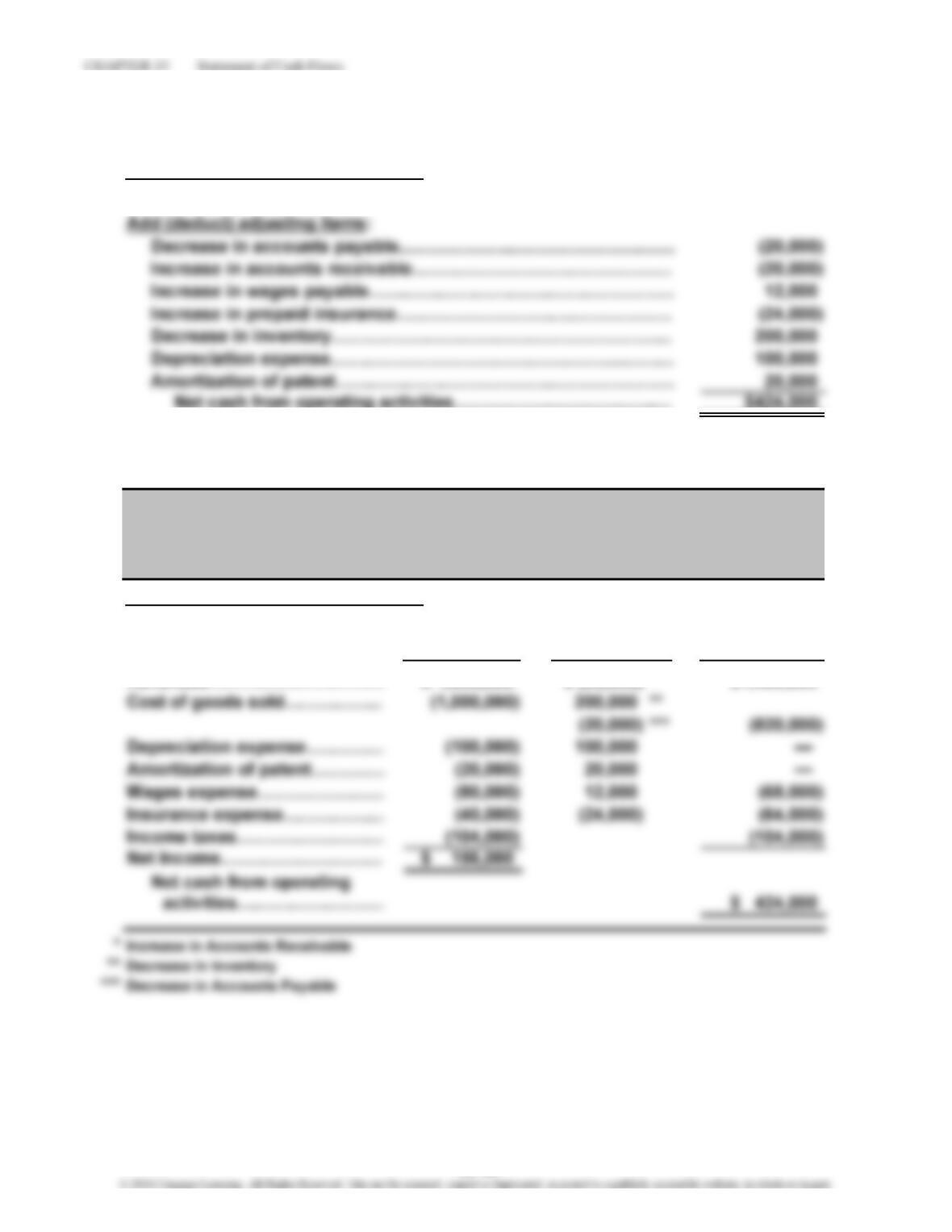

P 15-36

Cash flows from operating activities:

Net income………………………………………………… $ 63,000

Add (deduct) adjusting items:

Decrease in accounts receivable……………………

…

27,000

P 15-37

Income Cash

Cash flows from operating activities:Statement Flows

Revenues……………………………………

…

$ 297,000 $ 27,000 * $324,000

Cost of goods sold………………………

…

(175,500) (27,000) **

(39,600) *** (242,100)

…

PROBLEMS

Adjustments

Solpoder Corporation

Statement of Cash Flows

For the Year Ended December 31, 201

4

Statement of Cash Flows

For the Year Ended December 31, 2014

Direct Method

Solpoder Corporation

15-13

…

CHAPTER 15 Statement of Cash Flows

P 15-38

Cash flows from operating activities:

Net loss…………………………………………………

…

$ (800)

Add (deduct) adjusting items:

Depreciation expense…………………………………

…

6,000

P 15-39

Income Cash

Cash flows from operating activities: Statement Flows

For the Year Ended September 30, 2014

Roberts Company

Statement of Cash Flows

Adjustments

Roberts Company

Operating Cash Flows

For the Year Ended September 30, 2014

…

CHAPTER 15 Statement of Cash Flows

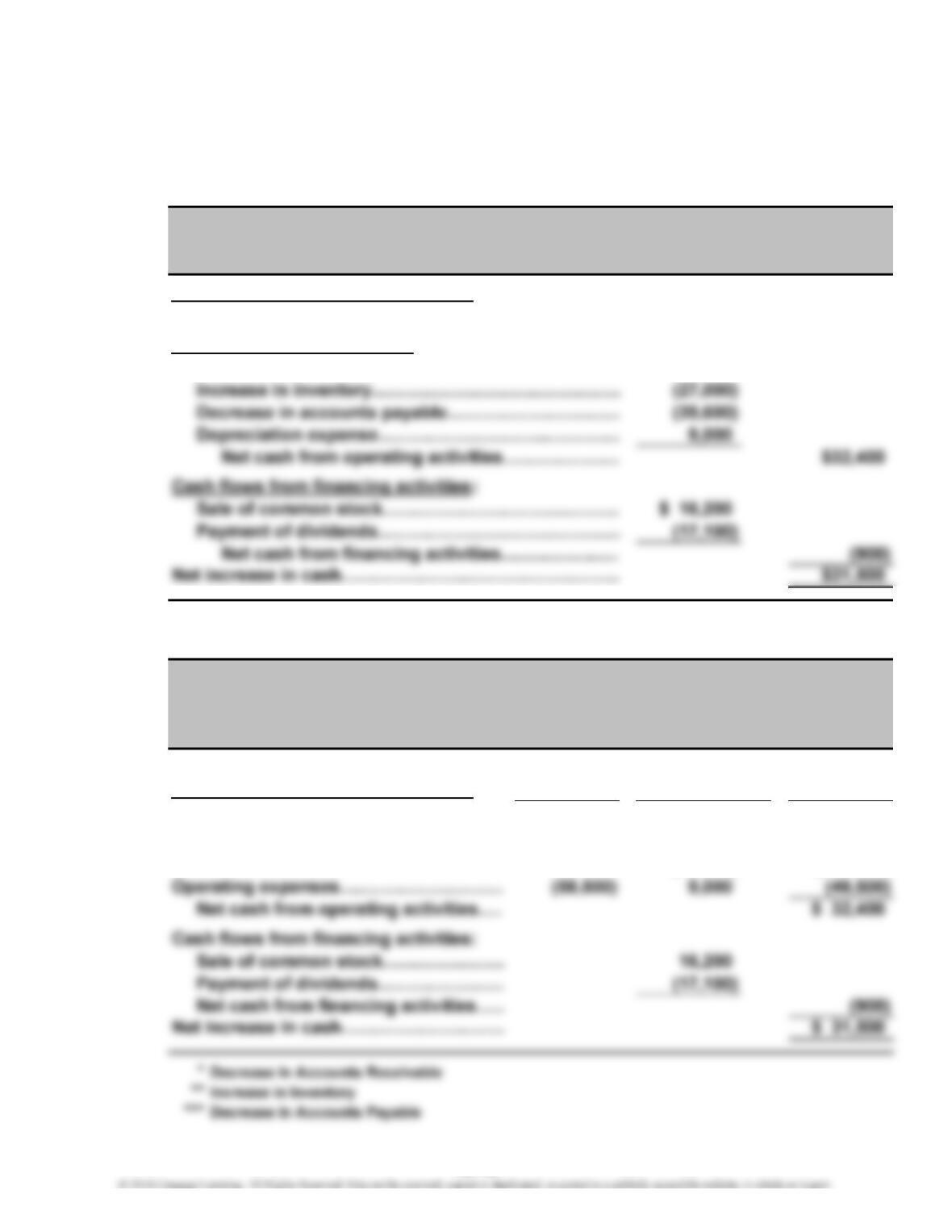

P 15-40

1. and 2.

Cash flows from operating activities:

Net income…………………………………………… $ 450,000

Add (deduct) adjusting items:

Decrease in accounts receivable………………

…

68,750

Cash flows from financing activities:

Mortgage received………………………………….

…

$ 250,000

Dividends…………………………………………….

…

(225,000)

Booth Manufacturing

Statement of Cash Flows

For the Year Ended December 31, 201

4

15-15

…

…

CHAPTER 15 Statement of Cash Flows

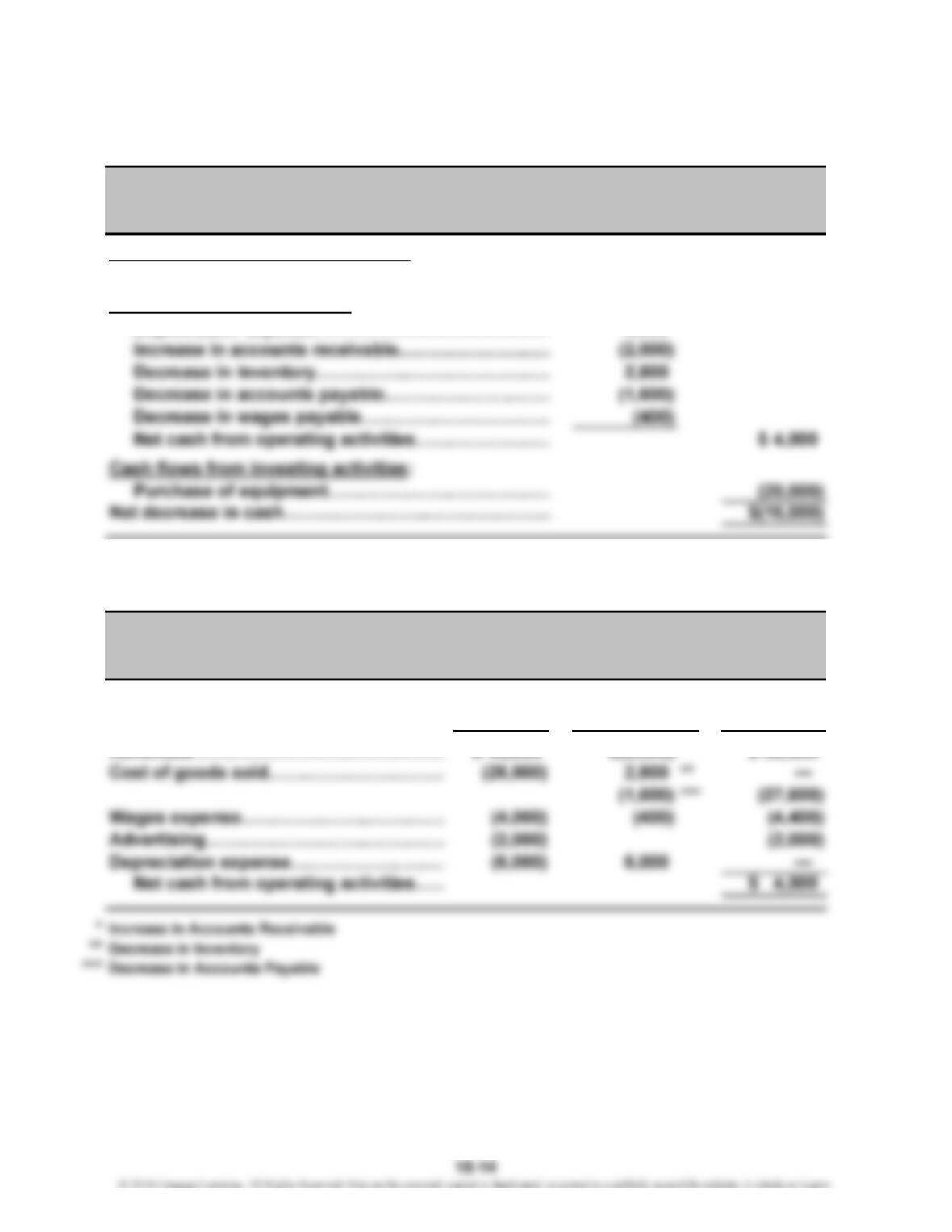

P 15-41

1. and 2.

Income

Statement Adjustments Cash Flows

Cash flows from operating activities:

Revenues…………………………….……

…

$1,200,000 $ 68,750 a$1,268,750

Gain on sale of equipment………………

…

50,000 (50,000) —

Booth Manufacturing

Operating Cash Flows

For the Year Ended September 30, 2014

15-16

…