CHAPTER 14 Capital Investment Decisions

P 14-37 (Continued)

Revenues……………………………………………………………

…

$ 1,650,000

2. Discount Facto

r

Present Value

1.00000 $(1,840,000)

3.60478 1,189,577

0.50663 91,193

P 14-38

2. Since I = P for the IRR:

3. For a life of 8 years:

6 180,000

10

$(1,840,000)

330,000

Cash Flow

0

1–5

Y

ea

r

14-16

CHAPTER 14 Capital Investment Decisions

P 14-38 (Continued)

The IRR is between 8% and 9%—greater than the 8% cost of capital. The company

4. Requirement 2 reveals that the estimates for cash savings can be off by as much as

$9,479 (over 15%) without affecting the viability of the new system. Requirement 3

P 14-39

1. First, calculate the expected cash flows:

Days of operation each year: 365 – 15 = 350

Revenue per day: $235 × 2 × 150 = $70,500

2. Revised Cash Flow = (0.80 × $24,675,000) – $3,250,000

=

$16,490,000

14-17

CHAPTER 14 Capital Investment Decisions

P 14-39 (Continued)

3. NPV = (7.46944)CF – $120,000,000 = 0

CF =

=

Annual Revenue = $16,065,461 + $3,250,000

4. Round-Trip Average Price = (2 × $235) × 1.1 = $517

Seats to Be Sold = = 107 (rounded up)

7.46944

$120,000,000

$55,187

$16,065,461

$517

CHAPTER 14 Capital Investment Decisions

P 14-40

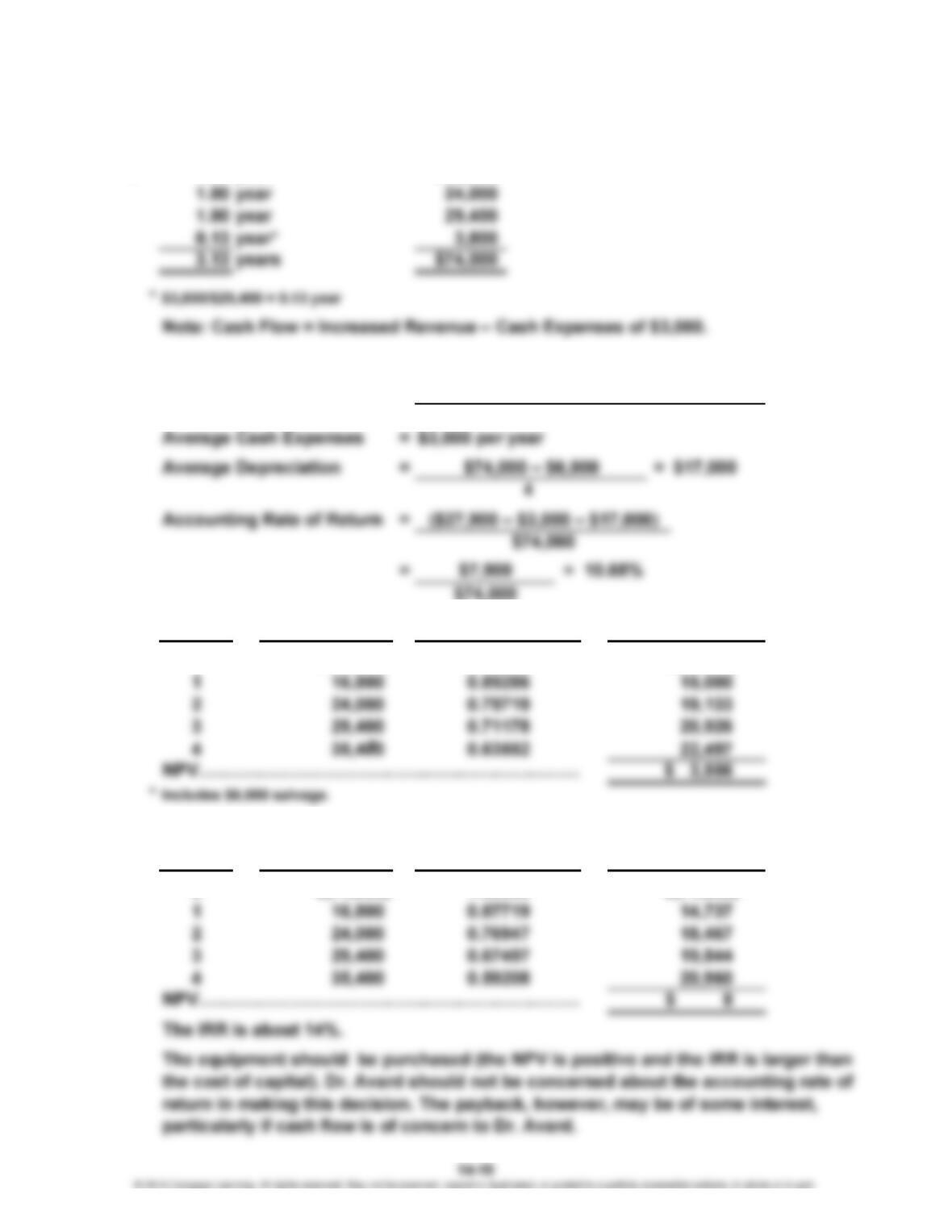

1. 1.00 year $16,800

2. Accounting rate of return:

Average Cash Revenue = = $27,900

3.

Y

ea

r

0

IRR (by trial and error): Using 14% as the first guess:

Y

ea

r

0

Discount Facto

r

Present Value

$(74,000) 1.00000 $(74,000)

Cash Flow

1.00000

($19,800 + $27,000 + $32,400 + $32,400)

4

Cash Flow

$(74,000)

Discount Facto

r

Present Value

$(74,000)

CHAPTER 14 Capital Investment Decisions

P 14-40 (Continued)

4. Year Cash Flow

0 $(74,000) 1.00000 $(74,000)

1 11,200 0.89286 10,000

P 14-41

1. Annual CF (rebuild alternative) = ($295.00 – $274.65)10,000 = $203,500

NPV = (CF × df) – I = ($203,500 × 3.79079) – $600,000 = $171,425

2. For the rebuild alternative, df = $600,000 = 2.94840. The IRR ≈ 20%.

$203,500

For the scrap alternative, df × CF = 0 implies that the IRR is infinite (CF is

Discount Factor Present Value

14-20

CHAPTER 14 Capital Investment Decisions

P 14-42

1.

A

llocation

(1) Substance abuse wing……

…

$1,500,000

2. With unlimited capital, the substance abuse wing and the laboratory would be chosen.

With limited capital, the laboratory and outpatient surgery wing would be chosen.

3. Answers may vary, but three qualitative considerations that should generally be

considered in capital budgeting evaluations include:

P 14-43

2.

Y

ea

r

Present Value

0 $(3,500,000)

Cash Flow

Project

Investment

$1,500,000

Discount Facto

r

1.00000

$(3,500,000)

14-21

CHAPTER 14 Capital Investment Decisions

P 14-43 (Continued)

P = CF(df) = I for the IRR, thus,

For 5 years and a discount factor of 3.88889, the IRR is about 9%.

3.

Y

ea

r

Discount Facto

r

Present Value

It is very important to adjust cash flows for inflationary effects. Since the required rate

of return for capital budgeting analysis reflects an inflationary component at the time

decision.

P 14-44

1. Bond Cost = $3,000/$60,000 = 0.05

Cost of Capital = 0.05(0.60) + 0.175(0.40)

= 0.03 + 0.07

= 0.10

2.

Y

ea

r

Discount Facto

r

Present Value

Cash Flow

Cash Flow*

14-22

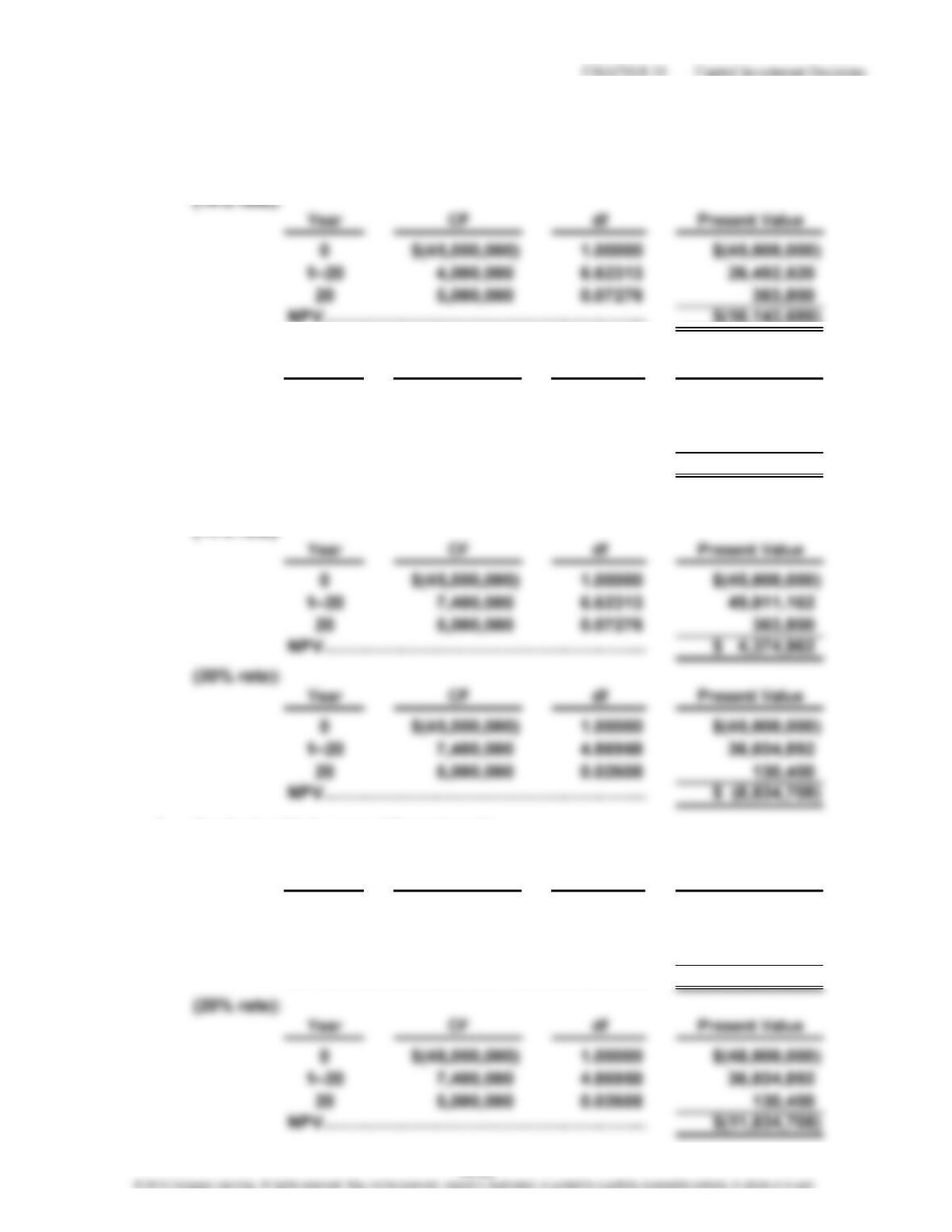

P 14-45

1. Original savings and investment:

Y

f

NPV………………………………………………

…

$(18,143,680)

(20% rate):

Y

ear CF d

f

Present Value

0 $(45,000,000) 1.00000 $(45,000,000)

1–20 4,000,000 4.86958 19,478,320

20 5,000,000 0.02608 130,400

NPV………………………………………………

…

$(25,391,280)

2. Total benefits: ($4,000,000 + $1,000,000 + $2,400,000)

(14% rate):

Y

f

…

Y

f

…

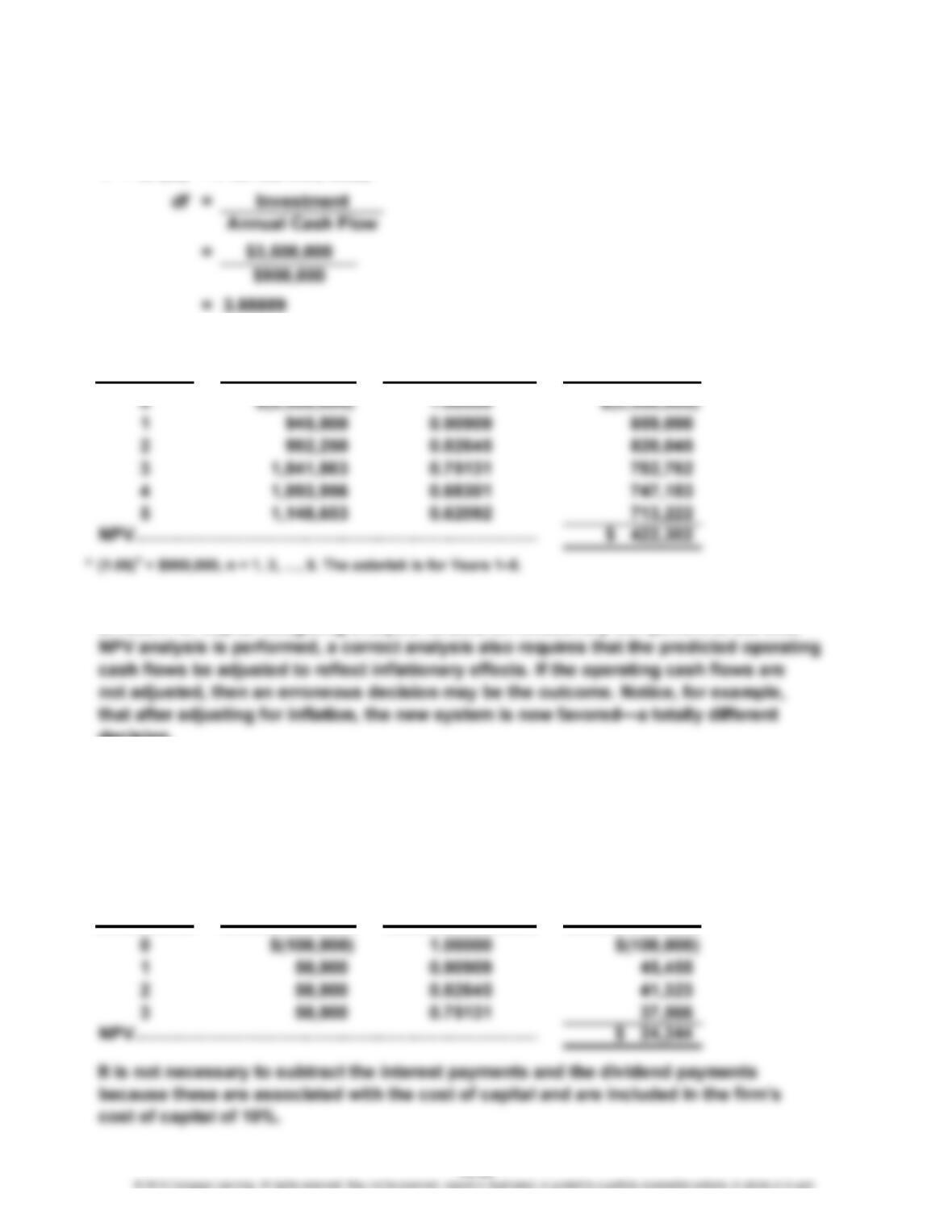

3. Analysis with increased investment:

(14% rate):

Y

ear CF d

f

Present Value

0 $(48,000,000) 1.00000 $(48,000,000)

1–20 7,400,000 6.62313 49,011,162

20 5,000,000 0.07276 363,800

NPV………………………………………………

…

$ 1,374,962

Y

f

…

14-23

CHAPTER 14 Capital Investment Decisions

P 14-45 (Continued)

4. The automated plant is an attractive investment when the additional

benefits are considered—it promises to return at least the cost of capital

P 14-46

1.

Y

ea

r

CF df Present Value

0 $(860,000) 1.00000 $(860,000)

1–8 225,000 4.34359 977,308

NPV……………………………………………… $ 117,308

Y

r

4. A postaudit can help ensure that a firm’s resources are being used wisely.

It may reveal that additional resources ought to be invested or that

CHAPTER 14 Capital Investment Decisions

P 14-47

1. Standard (Rate = 18%):

Year CF df Present Value

0 $(500,000) 1.00000 $(500,000)

1 300,000 0.84746 254,238

2 200,000 0.71818 143,636

3–10 100,000 2.92845 * 292,845

NPV……………………………………………

…

$ 190,719

*d

f

for Years 1

–

10 minus df for Years 1

–

2 (from Exhibit 14B.2)

2. Standard (Rate = 10%):

Year CF df Present Value

0 $(500,000) 1.00000 $(500,000)

1 300,000 0.90909 272,727

2 200,000 0.82645 165,290

3–10 100,000 4.40903 440,903

NPV……………………………………………

…

$ 378,920

…

–

14-25

…

CHAPTER 14 Capital Investment Decisions

P 14-47 (Continued)

3. Notice how the cash flows using a 10% rate in Years 8–10 are weighted compared

to the 18% rate. The difference in present value is significant. Using an excessive

P 14-48

1. Standard (Rate = 14%):

Year CF df Present Value

0 $(500,000) 1.00000 $(500,000)

1 300,000 0.87719 263,157

2 200,000 0.76947 153,894

3–10 100,000 3.56946 356,946

NPV…………………………………………………………… $ 273,997

2. Standard (Rate = 14%):

Year CF df Present Value

0 $(500,000) 1.00000 $(500,000)

14-26

CHAPTER 14 Capital Investment Decisions

Case 14-49

The statement that Manny would normally have taken the first bid without

hesitation implies that the bid met all of the formal requirements outlined

by the company. If Manny’s friend had met the bid as requested, then

presumably Manny would have offered the business to his friend. The

The fact that Manny was tempted by Todd’s enticements and appeared to

be leaning toward accepting Todd’s original offer compounds the

difficulty of the issue. If Manny actually accepts Todd’s offer and grants

the business at the original price and accepts the gifts, then his behavior

is unquestionably unethical. Some parts of the Statement of Ethical

Professional Practice that would be violated are listed below.

II. Confidentiality

1. Keep information confidential except when disclosure is authorized or

III. Integrity

2. Refrain from engaging in any conduct that would prejudice carrying

out duties ethically.

CASES

CHAPTER 14 Capital Investment Decisions

Case 14-50

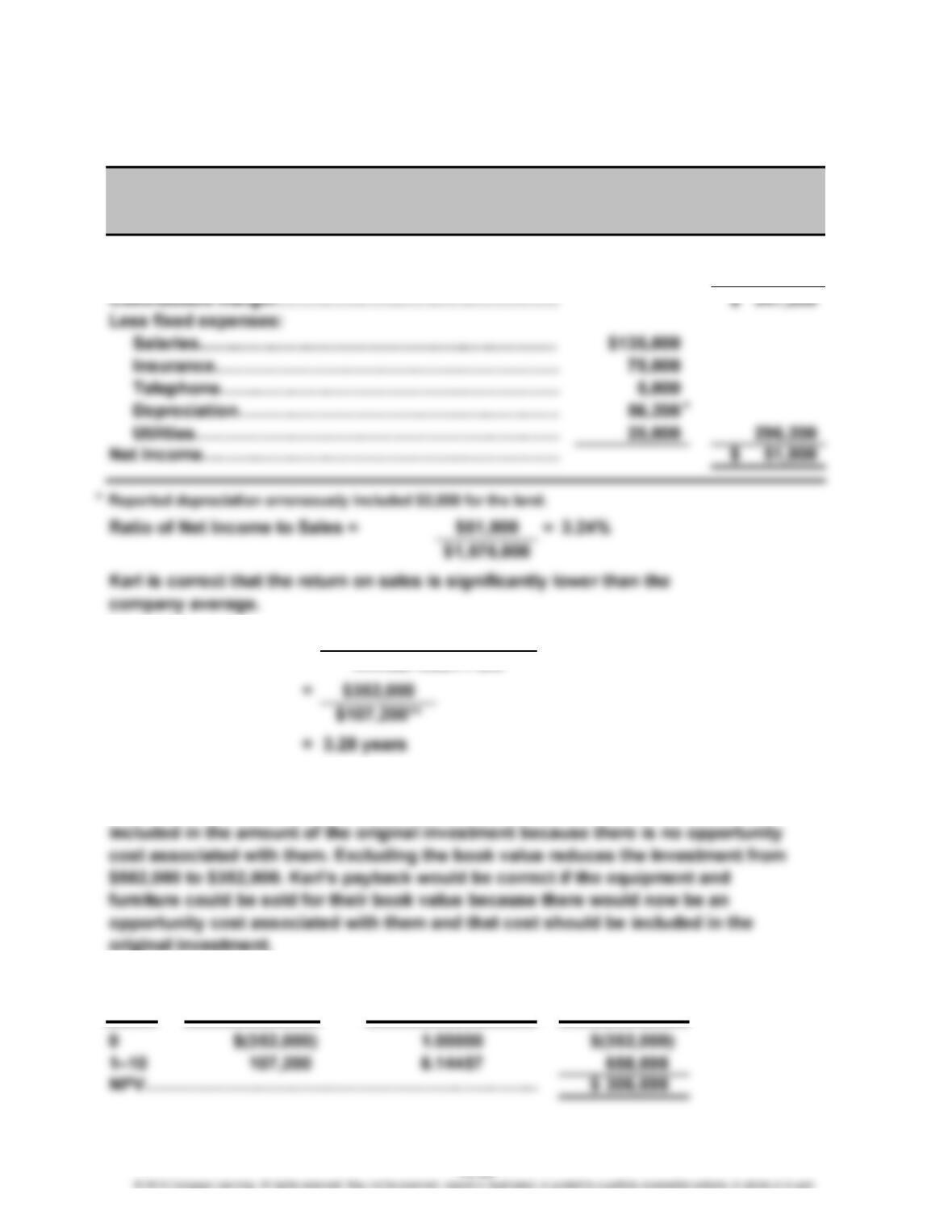

1.

Sales (35,000 × $45)…………………………………………

…

$1,575,000

Less: Variable expenses ($35.08 × 35,000).……………

…

1,227,800

2. Payback Period =

** Net income of $51,000 + depreciation of $56,200

Karl is wrong. The book value of the equipment and the furniture should not be

3. NPV:

Y

ea

r

Shaftel Ready Mix

Income Statement

For the Proposed Plant

Present Value

Cash Flow

Original Investment

Annual Cash Flow

Discount Facto

r

14-28

CHAPTER 14 Capital Investment Decisions

Case 14-50 (Continued)

If the furniture and equipment can be sold for book value:

NPV:

Y

ea

r

Discount Facto

r

Present Value

0 $(582,000) 1.00000 $(582,000)

4. Breakeven:

= $35.08X + $296,200

= $296,200

= 29,859 cubic yards

NPV (using break-even amount):

Y

ea

r

Discount Facto

r

Present Value

0 $(352,000) 1.00000 $(352,000)

X

Cash Flow

$9.92X

$45X

Cash Flow

Case 14-50 (Continued)

5. Cost of Capital = 10% for 10 years, so df = 6.14457

df =I

CF

Net Income = Sales – Variable Expenses – Fixed Expenses

= $45X – $35.08X – $296,200

$1,086