CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-32

3. Total Ordering Cost = Number of Orders × Cost per Order

= 72 orders × $10

=

E 8-33

1. Reorder Point without Safety Stock = Average Daily Rate × Lead Time

= 80 motors × 5 days

= 400 units

√2 × 17,280 × $10

$6

$720

=

EOQ1.

8-13

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

E 8-34

1. Reorder Point without Safety Stock = Average Daily Rate × Lead Time

= 16 units × 6 days

=

4. There are many more weddings during the summer than in most other seasons of the

year. This could explain why sometimes the maximum number of boas used (50) is

96 units

8-14

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-35

1. Direct materials……………………….……………………

…

$2.85

Direct labor……………………….…………………………

…

1.92

2. Absorption-costing income:

Sales (204,300 units × $9)…….………….……………….………….………

…

$1,838,700

3. Direct materials……………………….……………………

…

$2.85

Direct labor……………………….…………………………

…

1.92

4. Variable-costing income:

Sales (204,300 units × $9)…….………….……………….………….………

…

$ 1,838,700

Less variable expenses:

…

PROBLEMS

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-35 (Continued)

5. Absorption-costing income:

Sales (196,700 units × $9)………………………………………………

…

$ 1,770,300

Less: Cost of goods sold (196,700 units × $7.27)…………………

…

1,430,009

Gross margin……………………………………………………………

…

$ 340,291

…

…

…

…

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-36

2. Variable-Costing Ending Inventory:

$4.25 per unit – $0.50 per unit = $3.75 per unit

Ending Inventory = 2,700 units × $3.75 = $10,125

Sales………………………………………………………………………………

…

$ 455,010

3.

Total

Sales………………………

…

$455,010 $116,000 $ 90,000 $ 661,010

Less variable expenses:

4. Only two segments are profitable, the drugstores & supermarkets and the beauty

shops. The discount stores are unprofitable. Sugarsmooth might consider

Drugstores &

Supermarkets

Discount

Stores

Beauty

Shops

Sugarsmooth Inc.

Variable-Costing Income Statement

For the Coming Year

8-17

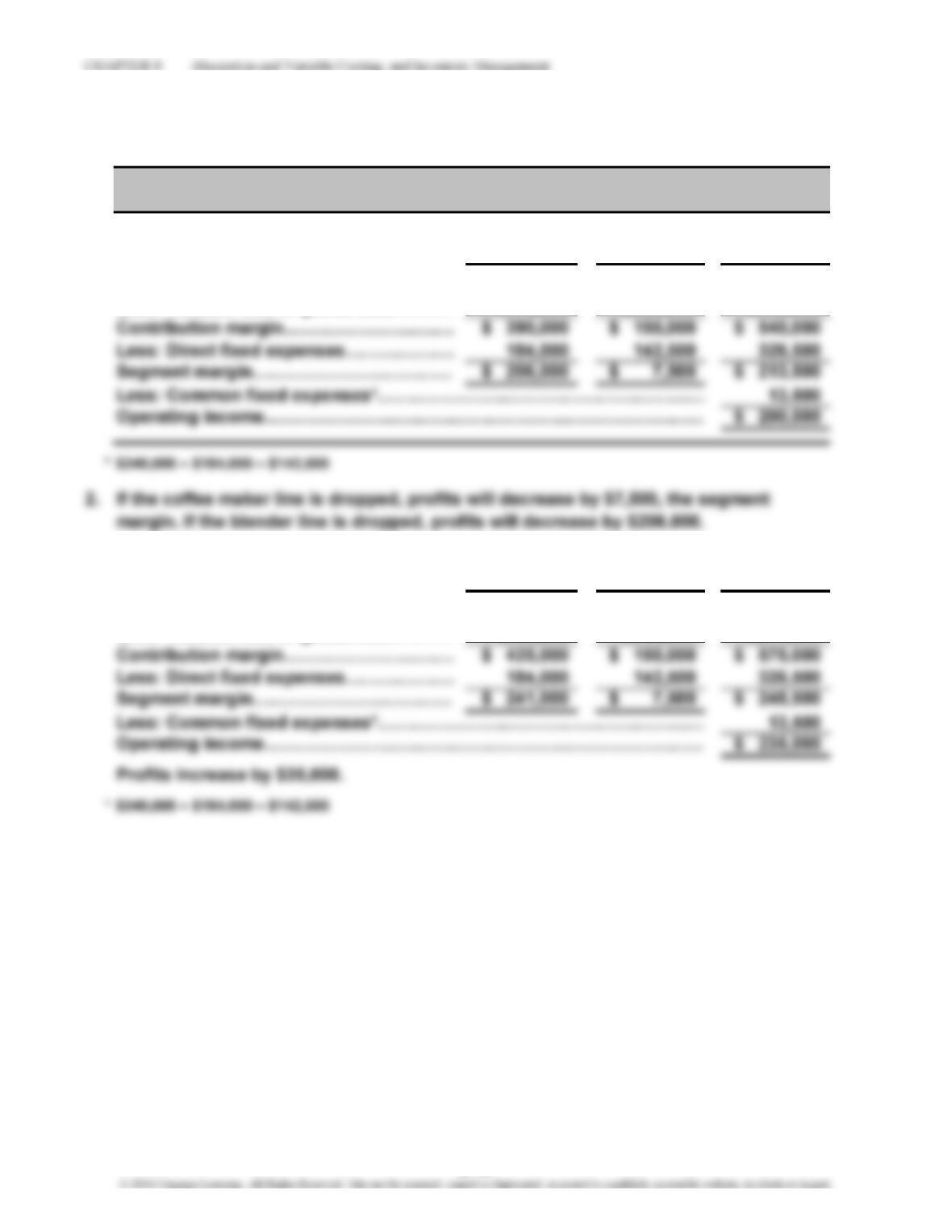

P 8-37

1.

Coffee

Blenders Makers Total

Sales…………………………………………… $1,560,000 $2,175,000 $3,735,000

Less: Variable cost of goods sold………

…

1,170,000 2,025,000 3,195,000

3. Coffee

Blenders Makers Total

Sales…………………………………………… $1,775,000 $2,175,000 $3,950,000

Less: Variable cost of goods sold………

…

1,350,000 2,025,000 3,375,000

Alard Company

Segmented Income Statement

8-18

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-38

1. Absorption costing:

Direct materials………………………………………………

…

$1.68

2. Variable costing:

Direct materials………………………………………………

…

$1.68

V

3. Selling price…………………………………………………… $ 6.95

Less:

V

4. Sales ($6.95 × 29,500)………………………………………

…

$205,025

Less variable expenses:

V

ariable cost of goods sold……………………………

…

$72,865

8-19

V

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-39

Scented Musical Regula

r

Total

1. Sales…………………………………

…

$13,000 $19,500 $25,000 $57,500

Less: Variable expenses…………

…

9,100 15,600 12,500 37,200

Contribution margin………………

…

$ 3,900 $ 3,900 $12,500 $20,300

2. Regular:

Sales…………………………………………………

…

$20,000

Less: Variable expenses…………………………

…

10,000

…

3. Combinations would be beneficial. Dropping the musical line (which

shows the greatest segment loss) and keeping the scented line while

increasing advertising yields a profit (the optimal combination).

Scented Regula

r

Total

8-20

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-40

1. Ordering Cost = 36,000 units/3,000 units × $15 = 12 orders × $15 = $180

5. Ordering Cost at EOQ = 36,000 units/600 units × $15 = $900

Carrying Cost at EOQ = $3 × (600 units/2) = $900

6. Total Cost of EOQ Policy = $900 + $900 = $1,800

Savings if EOQ Is Used = $4,680 – $1,800 = $2,880

8-21

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

P 8-41

3. Rate of Usage = 7 days per week × 50 weeks (that the pizza shop is open) = 350 days

= 14,000 units/350 days = 40 blocks per day

4. The order quantity would have to be 600 instead of 800 (the EOQ). If so, the

following inventory costs would be incurred:

Ordering Cost = $40 × (14,000 units/600 units)

5. The most cheese that should be kept on hand given the 10-day constraint is

8-22

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

Case 8-42

1. Many legitimate reasons support the creation of inventory (e.g., the

need to avoid stockouts and the need to ensure on-time delivery). Paul

2. Since the decision to produce for inventory was not motivated by any

sound economic reasoning, and Ruth knows the real motive behind the

decision, she should feel discomfort in the role she has been asked to

assume. If she decides to appeal to higher-level management, the

3. The following standards may apply:

Integrity. Refrain from engaging in any conduct that would prejudice

CASES

8-23

CHAPTER 8 Absorption and Variable Costing, and Inventory Management

Case 8-43

1. By discussing the amount by which his company and Piura have reduced costs, Mac

may have violated the confidentiality standard. Specifically, Mac should: “keep

2. Mac would violate a host of standards: disclosing confidential information, accepting

8-24