Archives: Solution Manual

978-0073526898 PowerPoint Session 15 – Intel Part 1

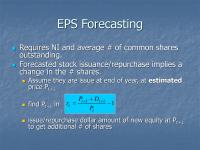

EPS Forecasting ◼Requires NI and average # of common shares outstanding. ◼Forecasted stock issuance/repurchase implies a change in the # shares. ◼Assume they are issue at end of year, at estimated price Pt+1. ◼issue/repurchase dollar amount of new equity at […]

978-0073526898 PowerPoint Session 13 – Valuation Equations Part 2

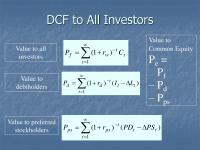

DCF to All Investors − += )1( t t wf CrP = 1 t Pe= Pf investors Value to = −−+= 1 )()1( t tt t dd LIrP tt psps PSPDrP stockholders = 1 […]

978-0073526898 PowerPoint Session 13 – Valuation Equations Part 1

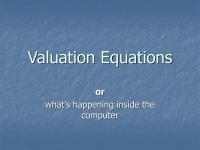

Valuation Equations or what’s happening inside the computer for the period ending 0 1 2 … T-1 T T+1 T+2 … NOA0 NOA1 NOA2 …NOAT-1 NOAT NOAT(1+g) NOAT(1+g)2 … -L0 -L 1 -L 2 … -L T-1 –L T -L […]

978-0073526898 PowerPoint Session 12 – 80 Minute Forecast Part 2

seasonality in SGA/Sales (HD)? 0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.5 8/2/09 8/3/08 7/29/07 7/30/06 7/31/05 8/1/04 8/3/03 8/4/02 7/29/01 7/30/00 sga/sales —- time —– seasonality in gross margin (HD)? 0 0.05 0.1 0.15 0.2 0.25 […]

978-0073526898 PowerPoint Session 12 – 80 Minute Forecast Part 1

The 80 Minute Forecast Forecasting the 3rd quarter for Tim Hortons for period ended 9/30/2012, to be announced November 8. But first, some facts about quarterly earnings and seasonality announced in press release with exchange press releases, blackout period, no […]

978-0073526898 PowerPoint Session 9 – Tale Of Two Movie Theaters Part 3

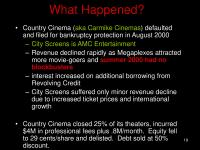

19 What Happened? •Country Cinema (aka Carmike Cinemas) defaulted and filed for bankruptcy protection in August 2000 –City Screens is AMC Entertainment –Revenue declined rapidly as Megaplexes attracted due to increased ticket prices and international growth •Country Cinema closed 25% […]

978-0073526898 PowerPoint Session 9 – Tale Of Two Movie Theaters Part 2

The Movie Industry 0 1000 2000 3000 4000 5000 6000 7000 8000 9000 1995 1996 1997 1998 1999 2000 box office gross sales (M) average attendance (M) $4.35/ticket $5.39/ticket 11 12 Multiplexes and Megaplexes average screens/theater 0 1 2 3 […]

978-0073526898 PowerPoint Session 9 – Tale Of Two Movie Theaters Part 1

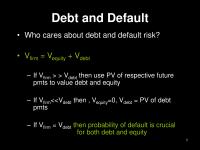

Debt and Default •Who cares about debt and default risk? •Vfirm = Vequity + Vdebt –If Vfirm > > Vdebt then use PV of respective future pmts to value debt and equity –If Vfirm<<Vdebt then , Vequity=0, Vdebt = PV […]

978-0073526898 PowerPoint Session 8 – HD Part 3

19 Next, forecasting CGS and SG&A: Are they also seasonal? 29.5% 29.6% 29.9% 30.0% 29.7% 30.2% 30.5% 30.4% 31.6% 32.0% 31.2% 31.3% 32.9% 33.4% 33.3% 33.5% 31.9% 30.8% 30.8% 32.0% 32.7% 34.2% 33.6% 33.2% 20.3% 18.6% 20.8% 21.5% 19.2% 20.7% […]

978-0073526898 PowerPoint Session 8 – HD Part 2

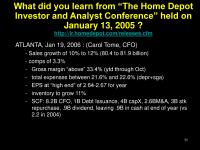

11 What did you learn from “The Home Depot Investor and Analyst Conference” held on January 13, 2005 ? http://ir.homedepot.com/releases.cfm 2.2 in 2004) ATLANTA, Jan 19,2006 : (Carol Tome, CFO) – Sales growth of 10% to 12% (80.4 to 81.9 […]

978-0073526898 PowerPoint Session 8 – HD Part 1

1 Financial Statement Analysis Forecasting Home Depot’s fourth quarter of 2005 financial statements super freak 2 products as well as other services. •Target individual homeowners, small contractors, and moving into commercial and industrial customers. Overview of business/industry • World’s largest […]

978-0073526898 PowerPoint Session 6 – RCL Forecasting Part 3

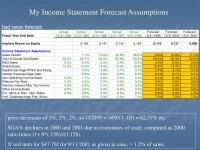

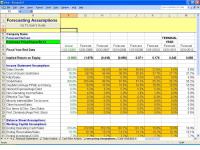

ratio times (1+.9*(.158))/(1.158). X’ord item for $47.7M for 9/11/2001 as given in case, = 1.2% of sales. My Income Statement Forecast Assumptions Actual Actual Actual Actual Actual Forecast Forecast Forecast Fiscal Year End Date 12/31/1994 12/31/1995 12/31/1996 12/31/1997 12/31/1998 12/31/1999 […]

978-0073526898 PowerPoint Session 6 – RCL Forecasting Part 2

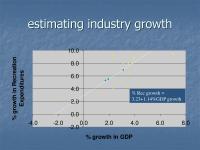

estimating industry growth -2.0 0.0 2.0 4.0 6.0 8.0 10.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0 % growth in GDP % growth in Recreation Expenditures % Rec growth = 3.23+1.14%GDP growth -5.0 0.0 5.0 10.0 15.0 20.0 25.0 1980 […]

978-0073526898 PowerPoint Session 6 – RCL Forecasting Part 1

what direction is this ship headed? Forecasting for the Love Boat Jackson 5 – The love you save firm sales unpredictable series based on past data forecast firm sales Figure 8.1 Estimating Industry and Firm Sales from Macroeconomic Data estimate […]

978-0073526898 PowerPoint Session 5 – RCL Ratios Part 2

11 Advance Dupont breakdown Royal Caribbean Carnival RNOA= 498,639/4,757,629 893,398/5,298,064 Net Operating Margin (NOI/Sales) 498,639/2,636,291 = 18.9% 893,398/3,009,306 = 29.7% x NOA Turnover (Sales/NOA) 2,636,291/4,757,629 = 0.554 3,009,306/5,298,064 = 0.568 + Spread (RNOA – NBC) 10.5% – 6.7% = 3.8% […]

978-0073526898 PowerPoint Session 5 – RCL Ratios Part 1

Royal Caribbean Cruises Ratio Analysis and Forecasting loveboat 1 2 The Cruise Experience 3 Industry Growth Rates 0 1000 2000 3000 4000 5000 6000 1980 1981 1982 1983 1984 1985 1986 1987 1996 1997 1998 1988 1989 1990 1991 1992 […]

978-0073526898 PowerPoint Session 4 – Overstock Acctg And Ratios Part 3

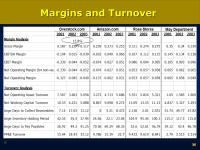

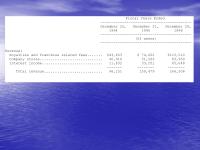

18 Margins and Turnover 12.8% 9% Boston Chicken, 1996 Fiscal Years Ended ——————————————————- December 25, 1994 December 31, 1995 December 29, 1996 —————– —————– —————– <S> <C> <C> <C> Cash Flows from Operating Activities: Net income……………………………………………… $ 16,173 $ 33,559 […]

978-0073526898 PowerPoint Session 4 – Overstock Acctg And Ratios Part 2

Next, Financial Analysis Framework for of Business Analysis and Valuation Financial Statements Analysis Tools competitor financials, bond ratings, beta factors, security prices etc. Other Public Data: industry data, analyst reports, Strategy Analysis Accounting Analysis Financial Analysis Prospective Analysis Business Application […]

978-0073526898 PowerPoint Session 4 – Overstock Acctg And Ratios Part 1

1 Financial Statement Analysis Overstock.com War 2 Overstock.com Overview of Business What do they do? www.overstock.com Performance? http://finance.yahoo.com/q/bc?s=OSTK&t=5y&l=on&z=l&q=l&c= 3 Overstock.com: Overview of Business Key success factors? Key risks factors? 4 1. Revenue Recognition Major switch from commission basis to gross […]

978-0073526898 PowerPoint Session 3 – PPD Acctg Part 2

What happens if the member quits before 3 years are up? •could account for as a write–off commission expense (+) xx commission advance (–) xx •or could do nothing! So what’s the big accounting issue in the press release? “Even […]

978-0073526898 PowerPoint Session 3 – PPD Acctg Part 1

The Four Tops – Its the Same Old Song Pre–Paid Legal Services – Q3 1999 ? An HMO for legal expenses •The Service –30 minutes on phone etc. –15.75 million individuals enroll –PPD has 603 thousand, or 3.8% of market […]

978-0073526898 PowerPoint Session 2 – BC Acctg Part 3

⚫ ⚫ ⚫ ⚫ ⚫ ⚫ ⚫ ⚫ Operating Accruals = (NI –CFO)/TA ⚫ ⚫ ⚫ -5 -4 -3 -2 -1 0 1 2 3 4 5 0 0.05 […]

978-0073526898 PowerPoint Session 2 – BC Acctg Part 2

In April 1996, the Company delivered 450,640 shares of common stock with a market value of approximately $15.0 million and a $6.8 million promissory note to acquire the equity interests of certain investors in Mid–Atlantic Restaurant Systems L.P. (“Mid–Atlantic”), its […]

978-0073526898 PowerPoint Session 2 – BC Acctg Part 1

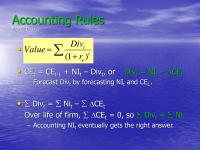

Accounting Rules Finance Drools • •CEt= CEt–1 + NIt–Divt, or Divt= NIt–DCEt + =t e t r Div Value )1( –Forecast Divtby forecasting NItand CEt.. •Divt= Nit– DCEt Over life of firm, DCEt= 0, so Divt= Nit –Accounting NIteventually […]

978-0073526898 PowerPoint Session 1 – BC Strat Part 3

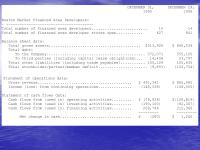

DECEMBER 31, DECEMBER 29, 1995 1996 Boston Market Financed Area Developers: – ————————————— Total number of financed area developers……………………. 15 14 Total number of financed area developer stores open………… 627 841 Balance sheet data: Total gross assets………………………………….. $513,926 $ 640,534 […]

978-0073526898 PowerPoint Session 1 – BC Strat Part 2

Fiscal Years Ended —————————————— December 25, December 31, December 29, 1994 1995 1996 —————————————— (53 weeks) —————————————— Revenue: Royalties and franchise related fees……. $43,603 $ 74,662 $115,510 Company stores……………………….. 40,916 51,566 83,950 Interest income………………………. 11,632 33,251 65,048 ——- ——– ——– […]

978-0073526898 PowerPoint Session 1 – BC Strat Part 1

Business Strategy Analysis •why won’t the company’s products/services become a commodity priced at the marginal cost of production? Rivalry Among Threat of Threat of Existing Firms New Entrants Substitute Products fixed/variable costs excess capacity PROFITABILITY Bargaining Power Bargaining Power of […]

978-0073526898 Case Suggested Solution To 4 Valuations Case W Compucorp

Suggested Solution to Four Valuation Models – One Value Case Part A: by hand computations 1) FCF to equity (i.e. net dividends) is computed as NIt – CEt. This gives 2001 2002 2003 2004 NI 3780 3834 4026 4227 chg […]

978-0073526898 Case Sirius Q17 Part 3

Model Summary Sensitivity Analysis Historical Data For: Forecast Horizon 10 Years SIRIUS SATELLITE RADIO Most Recent Fiscal Year End: 12/31/2005 This Year’s ROE (%) -167.62% Average ROE (last five years) -695.11% Sales Growth (last five years) #DIV/0! Terminal Year’s ROE […]

978-0073526898 Case Sirius Q17 Part 2

Annual Dividend Yield 4.00% Value of Contingent Claim Per Share #NAME? Number of Shares Subject to Claim (000s) 1,000 Total Value of Contingent Claim ($000s) #NAME? Residual Income Valuation ($000) Company Name SIRIUS SATELLITE RADIO Most Recent Fiscal Year End […]

978-0073526898 Case Sirius Q17 Part 1

Financial Statements ($000s) inactive Ticker Industry Code Sector Code Company Name SIRI MG724 MG7 Common Shares Outstanding 1,346,227 (in 000s at most recent fiscal year end) Estimated Price/Share=$2.13 Actual Actual Actual Actual Actual Forecast Forecast Forecast Forecast Forecast Forecast Forecast […]

978-0073526898 Case Sirius Part 3

Forecasting Analysis (18) ⚫Evaluate the plausibility of the forecasting scenario you provided in answer to the preceding question. –We will defer the answer to this question until question 22 –Note that one particular challenge we face in this forecasting will […]

978-0073526898 Case Sirius Part 2

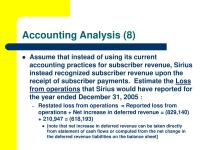

Accounting Analysis (8) ⚫Assume that instead of using its current accounting practices for subscriber revenue, Sirius instead recognized subscriber revenue upon the receipt of subscriber payments. Estimate the Loss from operations that Sirius would have reported for the year ended […]

978-0073526898 Case Sirius Part 1

Sirius Satellite Radio, Inc. Case Overview ⚫Comprehensive analysis of a growth company that requires economies of scale to attain profitability ⚫Company spends aggressively to increase subscriber growth in an attempt to achieve scale economies ⚫Subscriber growth falls short of target […]

978-0073526898 Case Salton Part 2

The Deal with George Foreman ▪the old deal with George: 60% of gross profit –approximately $64 million in 1999 ▪Is this an accounting distortion? ▪correcting the balance sheet today versus forecasting the correction in the future? http://www.biggeorge.com/familyman/familyman.htm ▪the new deal […]

978-0073526898 Case Salton Part 1

Accounting Analysis ▪Identifying accounting distortions –caused by estimation error, bad GAAP, or management manipulation ▪But you have to know the distortion exists! ▪From a valuation perspective, – Correcting the distortion = Forecasting the distortion’s reversal the RI model and accounting […]

978-0073526898 Case Ratio Case Notes

Instructor Notes for Interpreting Margin and Turnover Ratios* Overview: The objective of this case is to illustrate the determinants of margin and turnover ratios. Textbooks frequently recommend comparing margin and turnover ratios over time and across firms to identify the […]

978-0073526898 Case Overstock Slides Part 5

Analyst Valuation Method ⚫Analyst report uses comparable enterprise value to revenue multiples with ‘discount retailing peers’ and ‘internet bellwethers’ as comparisons ⚫Argues that OSTK deserves a premium because of superior top-line growth prospects ⚫Note that enterprise value equals market value […]

978-0073526898 Case Overstock Slides Part 4

Key Insights from Analysis ⚫Overstock’s turnover looks a little slow –High balance of cash and marketable securities slows down aggregate turnover ratios –Aggressive use of fulfillment partners combined with gross- basis accounting for sales revenue should lead to higher turns […]

978-0073526898 Case Overstock Slides Part 3

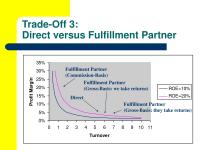

Trade-Off 3: Direct versus Fulfillment Partner 0% 5% 10% 15% 20% 25% 30% 35% 0 1 2 3 4 5 6 7 8 9 10 11 Turnover Profit Margin ROE=20% ROE=10% (Gross-Basis: we take returns) Direct Fulfillment Partner (Gross-Basis: they […]

978-0073526898 Case Overstock Slides Part 2

Sales Growth ⚫Growth rate in GAAP basis sales = 238.9/91.8 = 160% ⚫Growth rate in gross basis sales = 278.8/142.8 = 95% Source: Nissim and Penman (2001) GAAP Basis vs. Gross Basis Gross Profit Income Statement – Annual Overstock.com Inc. […]

978-0073526898 Case Overstock Slides Part 1

Overstock.com: Business Strategy Analysis Case Overview ⚫Comprehensive case that we will use throughout the course ⚫Rapidly growing “e–tailer” ⚫Strong sales growth and high stock price valuation ⚫But struggling to report a profit Overview of Business ⚫Close-out Internet retailer –http://www.overstock.com ⚫Revenues […]

978-0073526898 Case OSTK Q3 05 Part 2

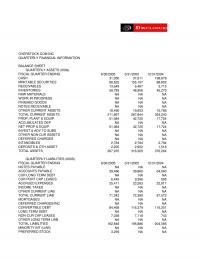

OVERSTOCK COM INC QUARTERLY FINANCIAL INFORMATION BALANCE SHEET QUARTERLY ASSETS (000s) FISCAL QUARTER ENDING 6/30/2005 3/31/2005 12/31/2004 CASH 31,350 37,611 198,678 MRKTABLE SECURITIES 88,625 155,157 88,802 RECEIVABLES 13,649 6,467 5,715 INVENTORIES 59,783 48,956 45,279 RAW MATERIALS NA NA NA WORK […]

978-0073526898 Case OSTK Q3 05 Part 1

OVERSTOCK COM INC Consolidated Statements of Income In Thousands Except Per Share Amounts For Period Ended Jun 30, 2005 09/30/05 3m Notes Revenue Direct 61,499 40% Growth Fulfillment partner 98,797 66% Growth Total revenue $160,296 55% Growth Cost of goods […]

978-0073526898 Case Netflix Part 3

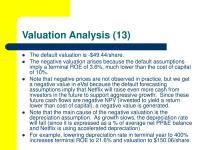

Valuation Analysis (13) ⚫The default valuation is -$49.44/share. ⚫The negative valuation arises because the default assumptions imply a terminal ROE of 3.6%, much lower than the cost of capital of 10%. lower than cost of capital), a negative value is […]

978-0073526898 Case Netflix Part 2

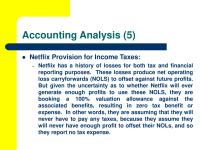

Accounting Analysis (5) ⚫Netflix Provision for Income Taxes: –Netflix has a history of losses for both tax and financial reporting purposes. These losses produce net operating loss carryforwards (NOLS) to offset against future profits. never have to pay any taxes, […]

978-0073526898 Case Netflix Part 1

Netflix, Inc. Case Overview ⚫Comprehensive analysis of a growth company experiencing growing pains. ⚫Management claims them to be temporary growing pains ⚫Stock market senses more chronic problems ⚫Case involves evaluation of competing perspectives and conclusion regarding company’s prospects and valuation […]

978-0073526898 Case NFLX 14 Part 7

23 24 14.22% 14.22% 5.00% 5.00% 1029973 1081472 150119 76890 47121 -31257 5262 -3173 23 24 14.22% 14.22% 5.00% 5.00% 2039436 2141408 297248 152249 93304 -61892 10420 -6284 23 24 14.22% 14.22% 5.00% 5.00% 7989232 8388694 1164430 596415 365507 -242454 […]

978-0073526898 Case NFLX 14 Part 6

Equity Value 1621977 Equity Value at Current Date 1731933 Less Contingent Claims 0 Adjusted Value 1731933 Shares Out. 52,732 Price/Share 32.84404907 Numbers below are inputs for dropdown list in Quick ‘n’ Dirty 5 Years 10 Years 20 Years 10 11 […]

978-0073526898 Case NFLX 14 Part 5

25 26 27 29 30 32 33 35 37 38 40 42 44 47 345 362 380 399 419 440 462 485 509 535 561 589 619 650 (3) (3) (3) (3) (3) (4) (4) (4) (4) (4) (5) (5) […]