Royal Caribbean Cruises

Ratio Analysis and Forecasting

2

The Cruise

Experience

3

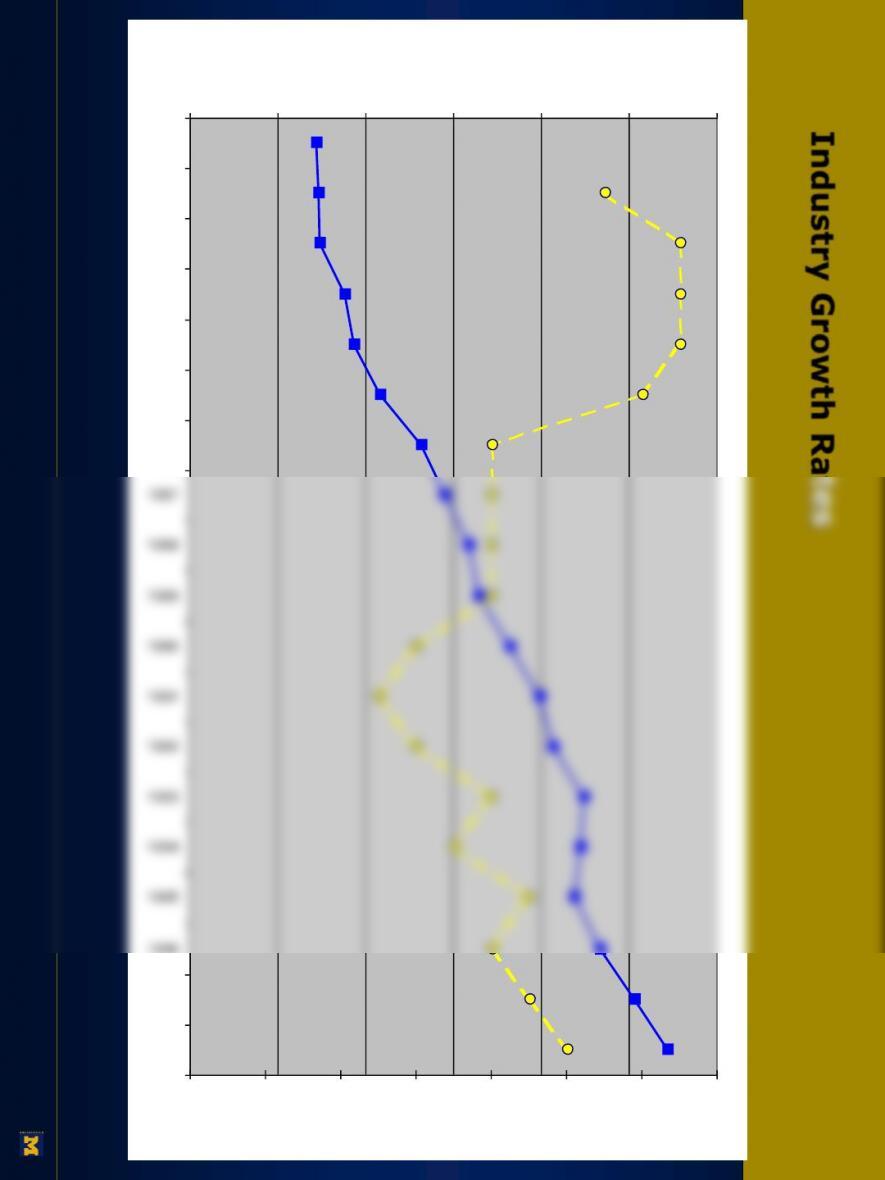

Industry Growth Rates

0

1000

2000

3000

4000

5000

6000

1980

1981

1982

1983

1984

1985

1986

1987

1996

1997

1998

annual cruise passengers (thousands)

5.6

5.8

6

6.2

6.4

6.6

6.8

7

average cruise length (days)

33

16

96

39466

29800

69107

2045000

1841000

1542000

0%

20%

40%

60%

80%

100%

ships berths passengers

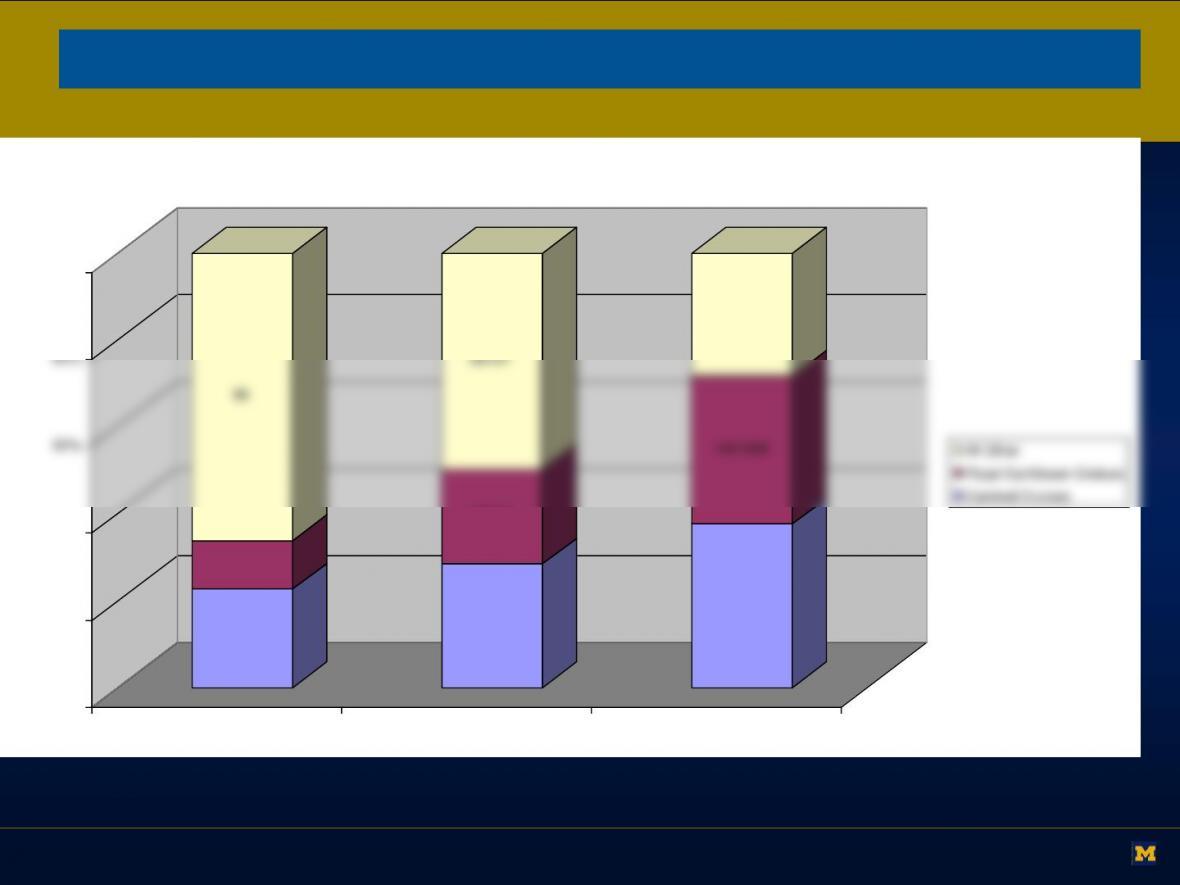

1998 Market Share

All Other

Royal Caribbean Cruises

Carnival Cruises

Cruise Industry Market Shares

5

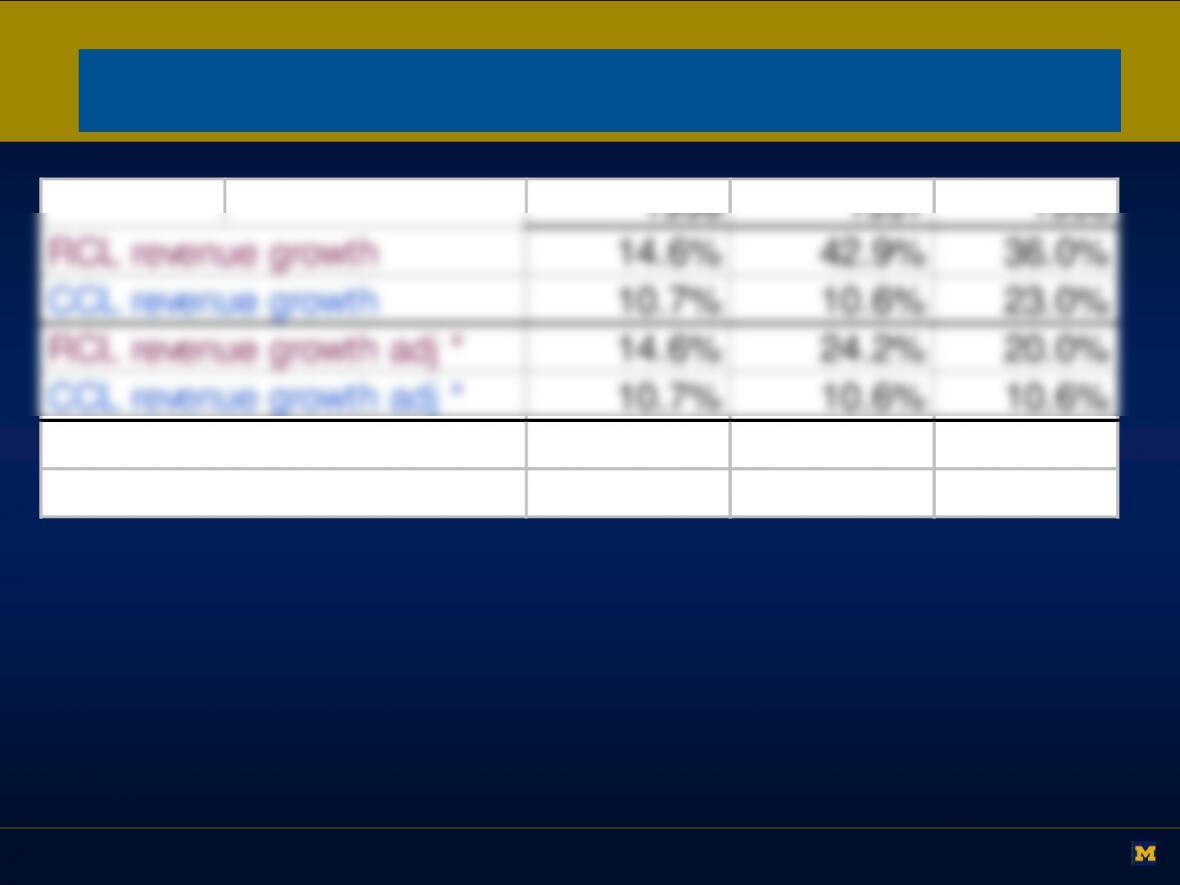

1996 1997 1998

RCL revenue growth 14.6% 42.9% 36.0%

CCL revenue growth 10.7% 10.6% 23.0%

RCL revenue growth adj * 14.6% 24.2% 20.0%

CCL revenue growth adj * 10.7% 10.6% 10.6%

RCL passenger day growth 44.7% 32.5%

CCL passenger day growth 12.5% 9.2%

Growth at RCL and CCL

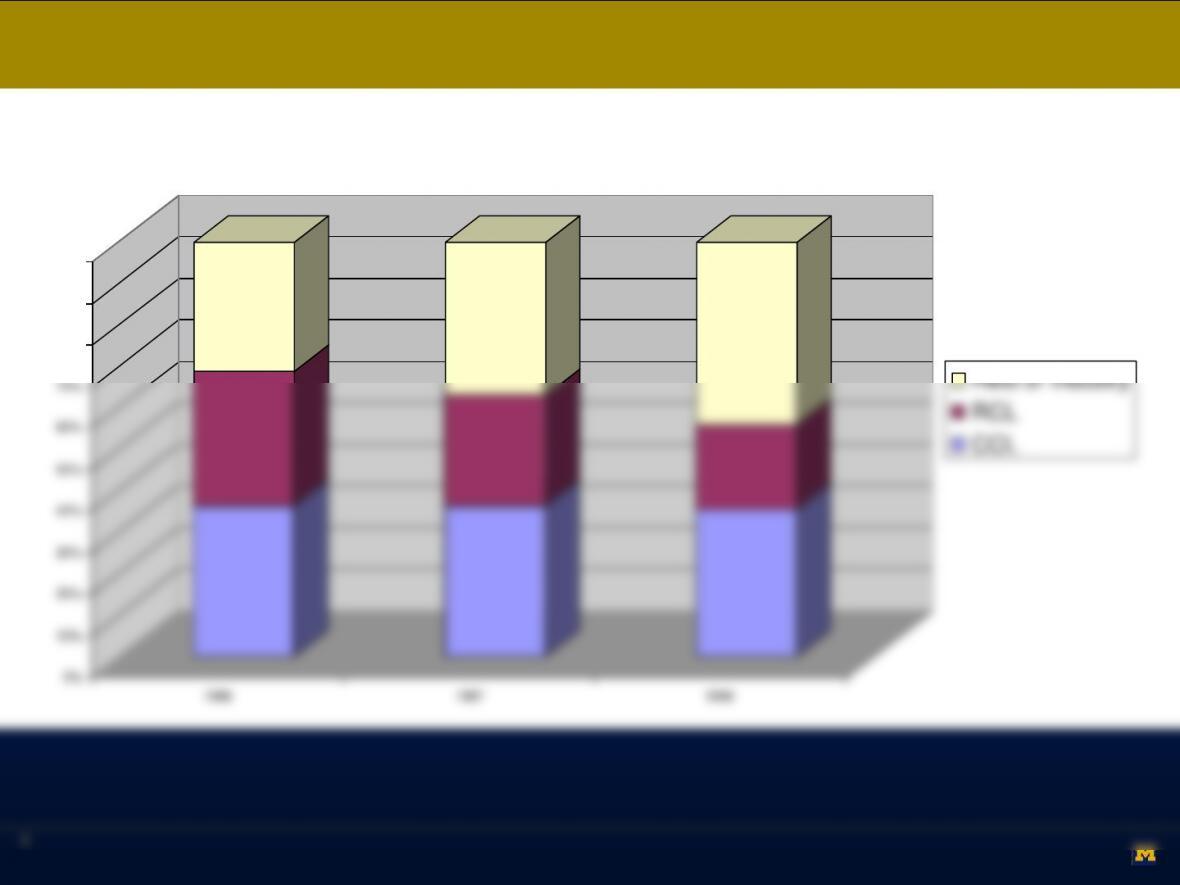

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1998 1997 1996

share of passenger cruise days

Rest of Industry

RCL

CCL

7

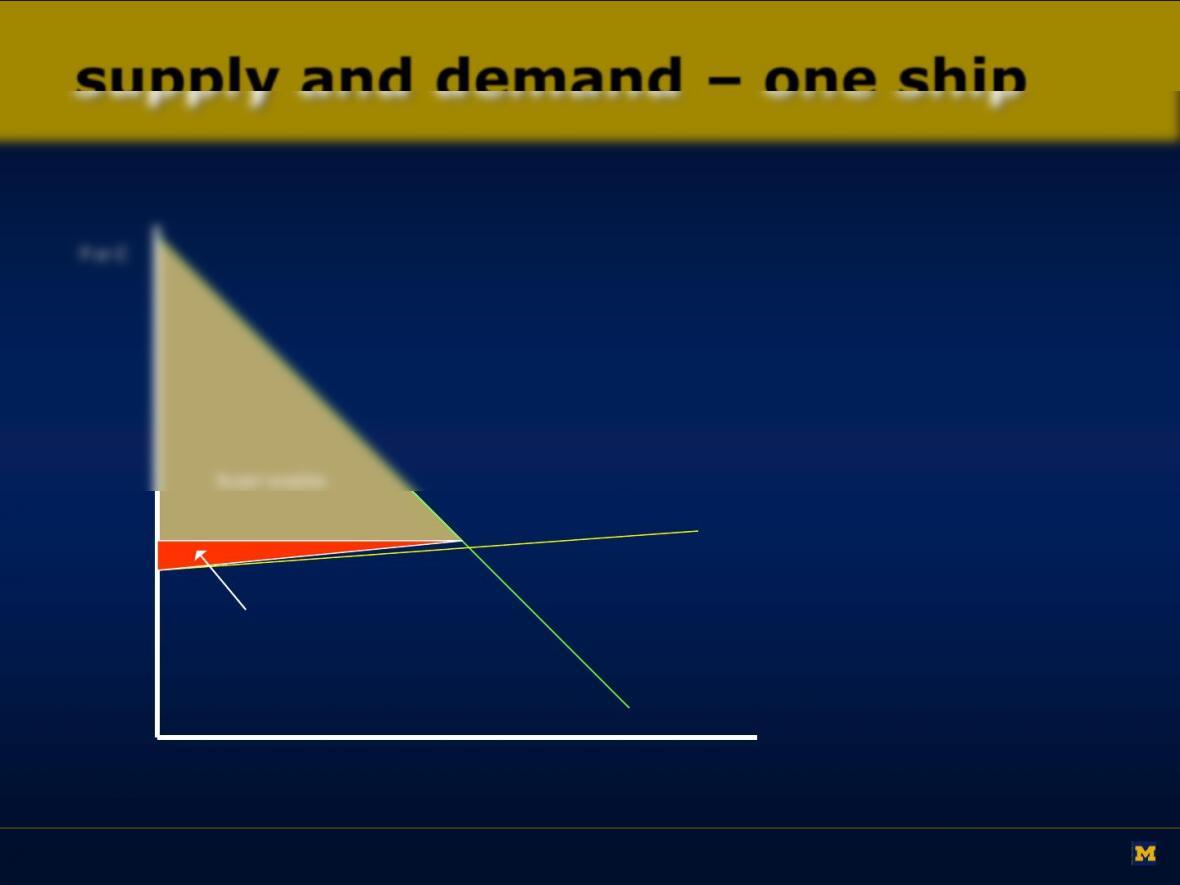

mc = 0

seller surplus

buyer surplus

P or C

Q

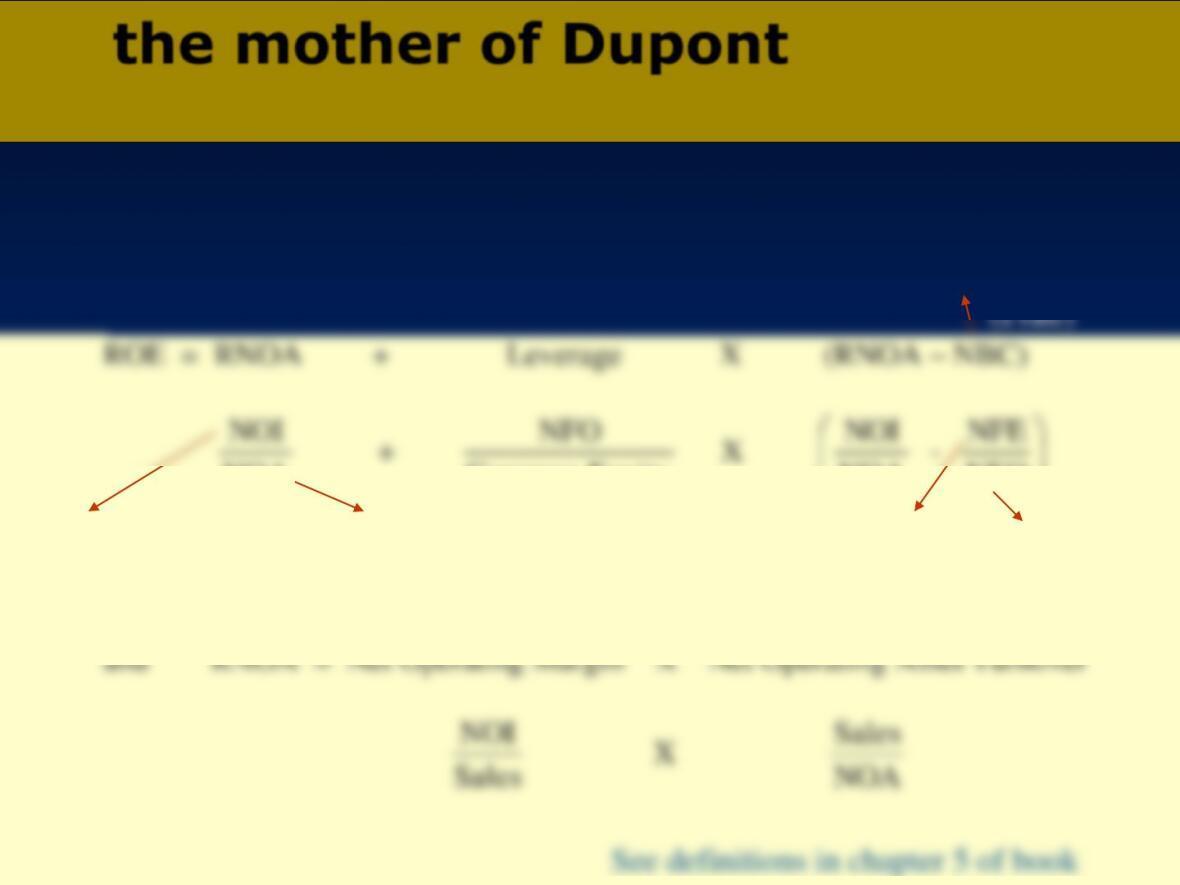

ROE = RNOA + Leverage X (RNOA – NBC)

NOA

NOI

+

EquityCommon

NFO

X

NFO

NFE

–

NOA

NOI

the mother of Dupont

Return on equity = return on net operating assets + leverage X spread

net operating income net operating assets

net borrowing cost

net financial

obligations

net financial

expense

9

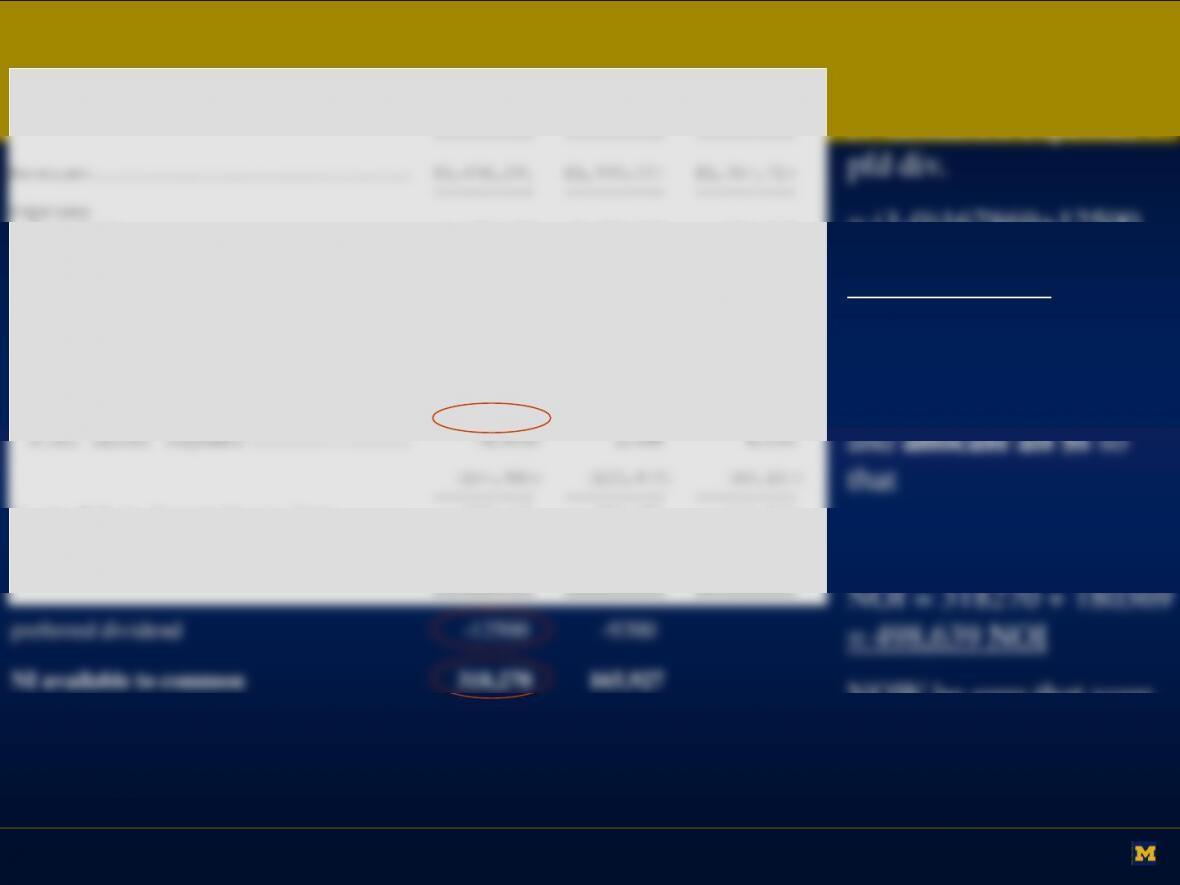

YEAR ENDED DECEMBER 31,

————————————

1998 1997 1996

———- ———- ———-

———- ———- ———-

Expenses

Operating……………………….. 1,593,728 1,219,268 854,478

Marketing, selling and administrative. 359,214 272,368 194,629

Depreciation and amortization……… 194,614 143,816 91,185

———- ———- ———-

2,147,556 1,635,452 1,140,292

———- ———- ———-

Operating Income…………………… 488,735 303,555 217,033

———- ———- ———-

Other Income (Expense)

Interest income………………….. 15,912 4,666 2,278

Income Before Extraordinary Item…….. 330,770 182,685 150,866

Extraordinary Item…………………. — (7,558) —

———- ———- ———-

Net Income………………………… $ 330,770 $ 175,127 $ 150,866

========== ========== ==========

NetFinancingExpense =

(1-t)(interest expense) +

= (1-0)167869+12500

=180,369 NFE.

NetOperatingIncome =

(1-t)OperatingIncome

NOI –NFE = NI

NOW be sure that your

allocations on BS.

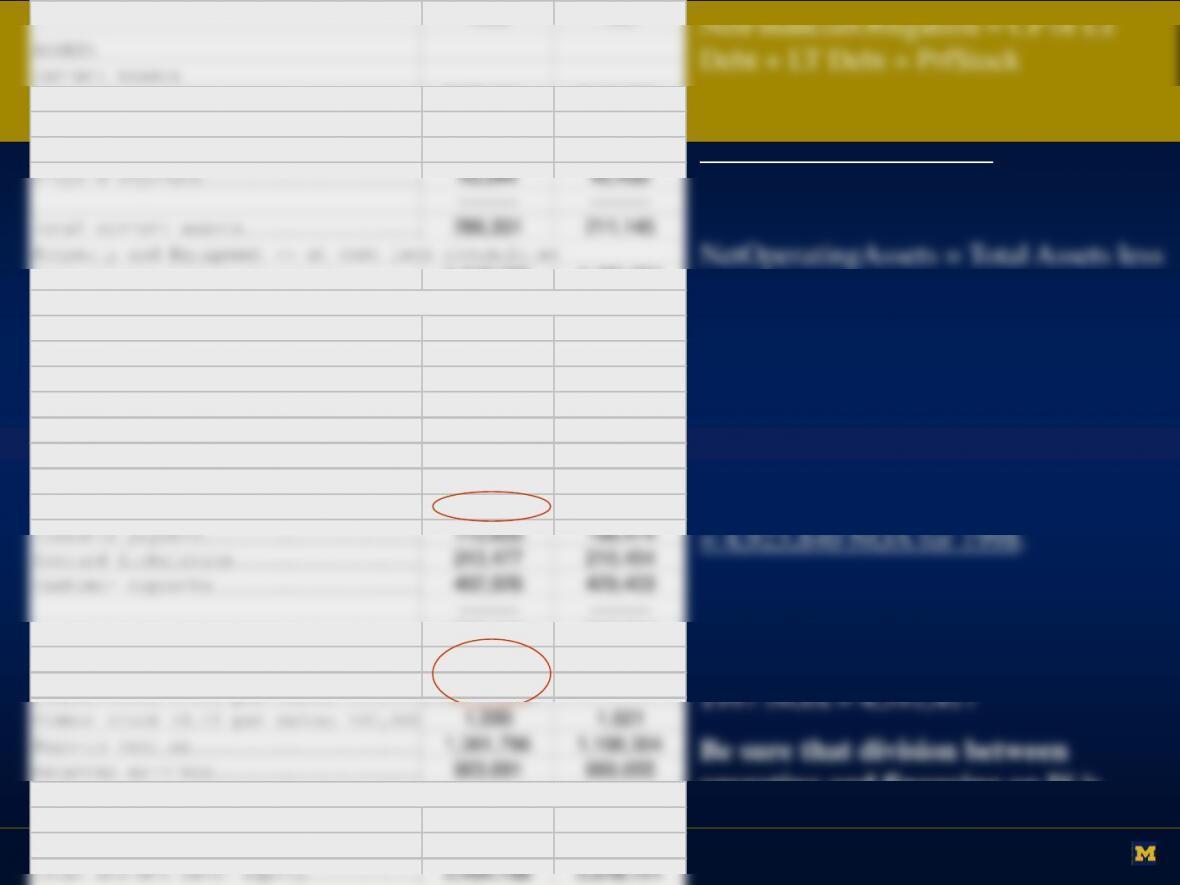

10

1998 1997

———- ———-

ASSETS

Current Assets

Cash and cash equivalents……………………………

$172,921 $110,793

Trade and other receivables, net…..…………………

36,532 22,628

Inventories……………………..…………………

31,834 37,274

Prepaid expenses……………………………………

Total current assets……………..………….

depreciation and amortization……..…………………

5,073,008 4,785,291

Goodwill — less accumulated amortization of $107,365 and

$96,952, respectively…………….…………………

309,801 320,214

Other Assets…………………….…………………..

16,936 23,098

———- ———-

$5,686,076 $5,339,748

========== ==========

LIABILITIES AND SHAREHOLDERS’ EQUITY

Current Liabilities

Current portion of long-term debt….…………………

$127,919 $141,013

Accounts payable……………………………………

Accrued liabilities…………………………………

Total current liabilities…………………….

890,155 889,344

Long-Term Debt…………………..…………………..

2,341,163 2,431,683

Preferred Stock…. 172,500 172,500

Common stock ($.01 par value; 500,000,000 shares

Retained earnings………………..…………………

923,691 660,655

Treasury stock (354,492 and 314,148 common shares at

cost)…………………………..………………

–4,919 -4,359

———- ———-

Total shareholders’ equity………..………….

2,454,758 2,018,721

NetFinancialObligation = CP of LT

Debt + LT Debt + PrfStock

= 127,919 + 2,341,163 + 172,500 =

2,641,582 NFO for 1998

Operating Liabilities.

Allocate all $s such that

NOA –NFO = CE.

NOA = CE + NFO = (2,454,758 –

172,500) + 2,641,582

1997 NFO = 2,745,196

operating and financing on IS is

consistent with division on BS!