Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

The Deal with George Foreman

▪the old deal with George: 60% of gross profit

–approximately $64 million in 1999

▪Is this an accounting distortion?

▪correcting the balance sheet today versus forecasting the

correction in the future?

http://www.biggeorge.com/familyman/familyman.htm

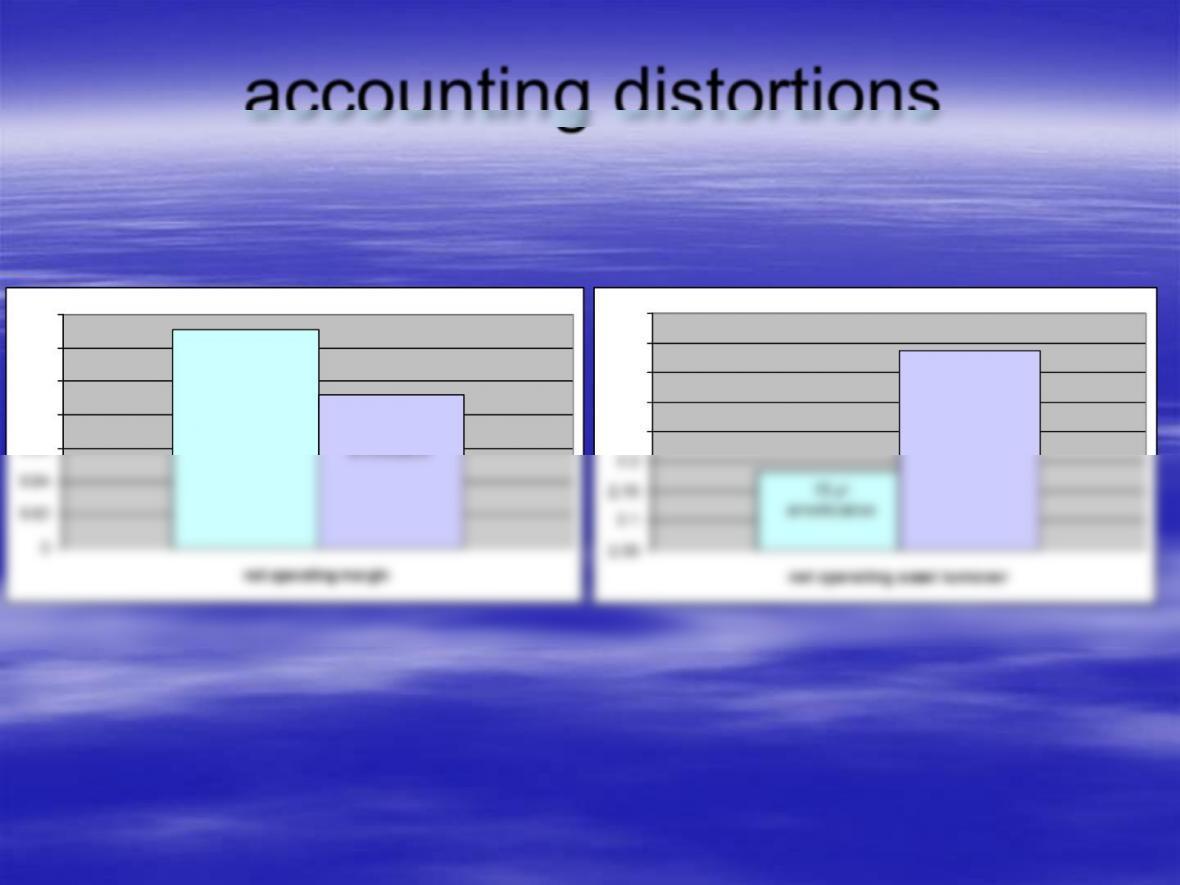

Suppose Foreman Trademark has a 3 year life.

Adjusted amounts based on amortization over 3 years = 40.5M/yr or 32.4M

more than As Reported

15 yr

amortization

3 yr

amortization

2.05

2.1

2.15

2.2

2.25

2.3

2.35

2.4

2.45

net operating asset turnover

15 yr

amortization

3 year

amortization

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

net operating margin

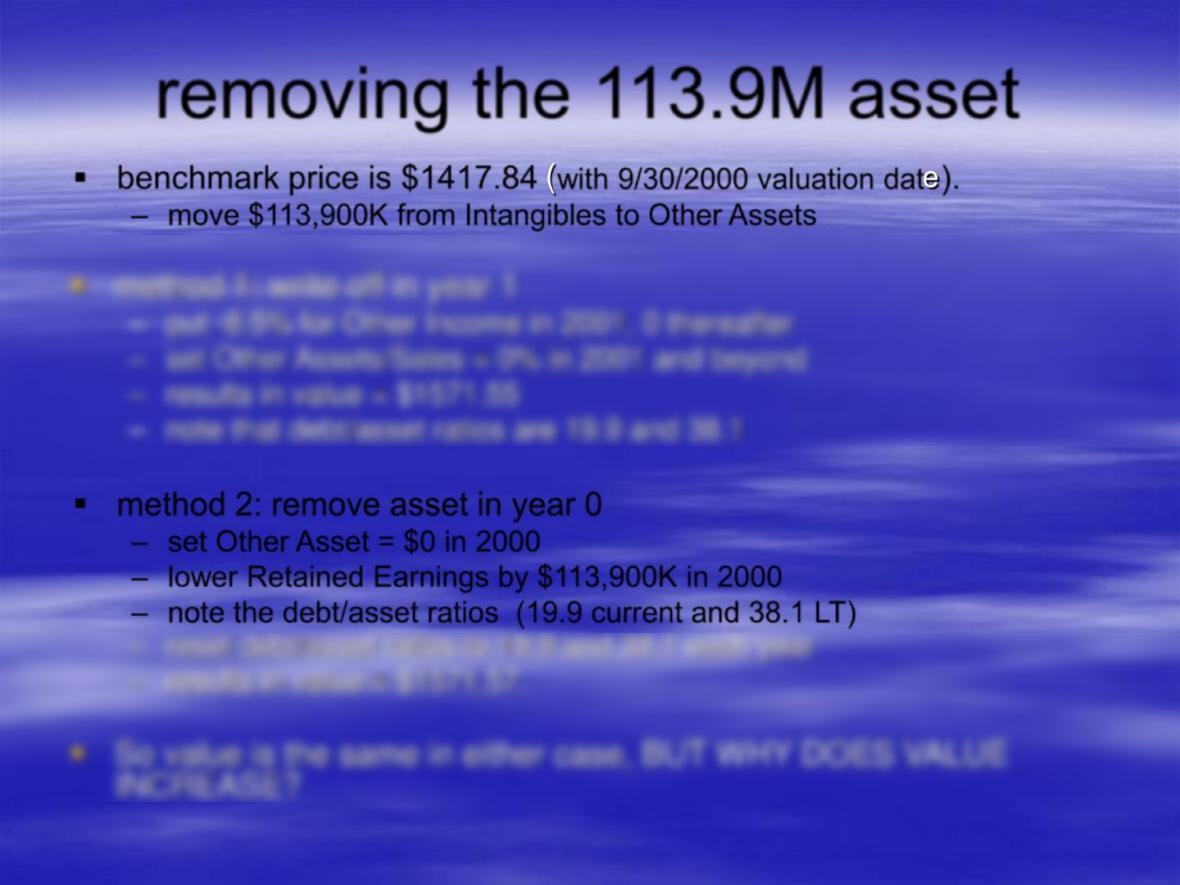

removing the 113.9M asset

▪benchmark price is $1417.84 (with 9/30/2000 valuation date).

–move $113,900K from Intangibles to Other Assets

▪method 2: remove asset in year 0

–set Other Asset = $0 in 2000

–lower Retained Earnings by $113,900K in 2000

–note the debt/asset ratios (19.9 current and 38.1 LT)

Salton Redux

▪what was the point again?

–accounting distortions influence on valuation

▪when we correct doesn’t matter

▪naïve extrapolation of past sales growth

▪overstatement of profitability

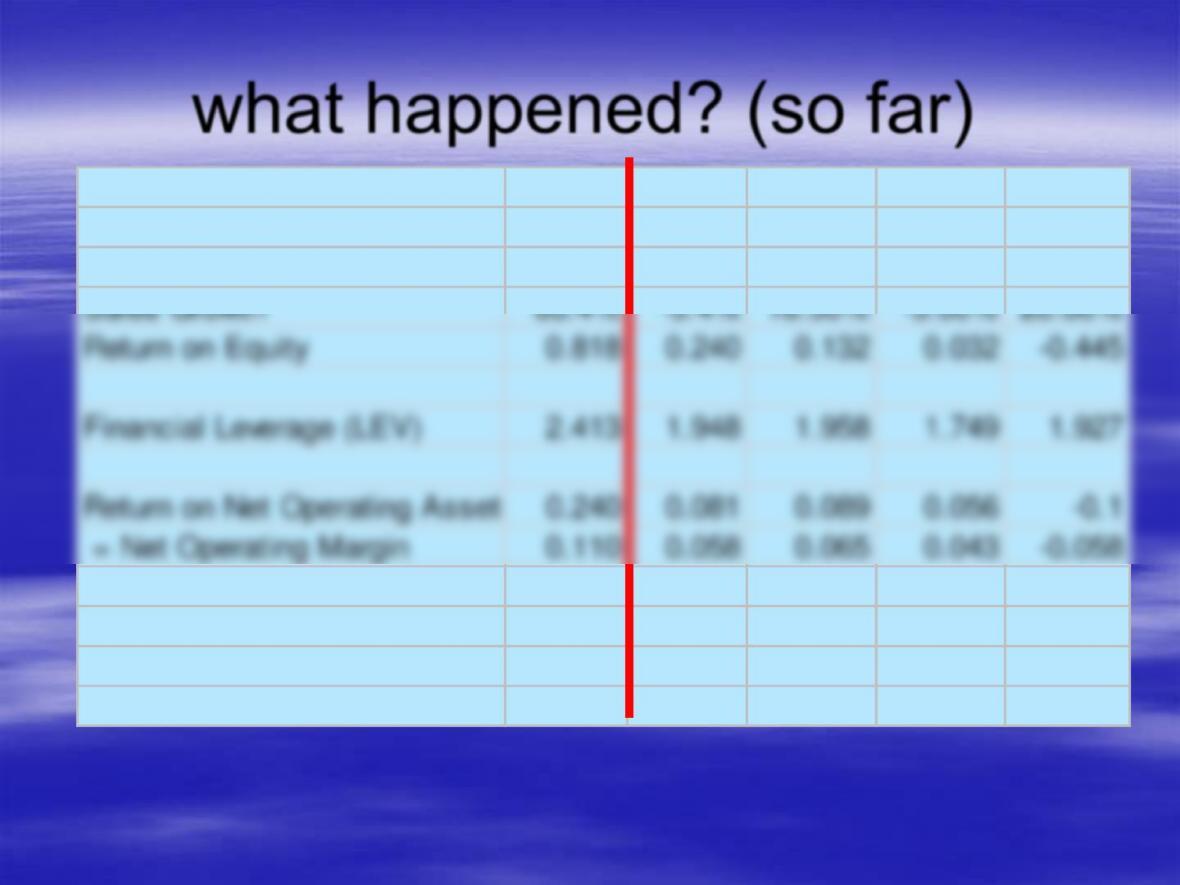

what happened? (so far)

Actual Actual Actual Actual Actual

Fiscal Year End Date 7/1/2000 7/1/2001 6/29/2002 6/29/2003 6/30/2004

Sales Growth 65.4% -5.4% 16.50% -3.00% 20.00%

Return on Equity 0.818 0.240 0.132 0.032 -0.445

Financial Leverage (LEV) 2.413 1.948 1.958 1.749 1.927

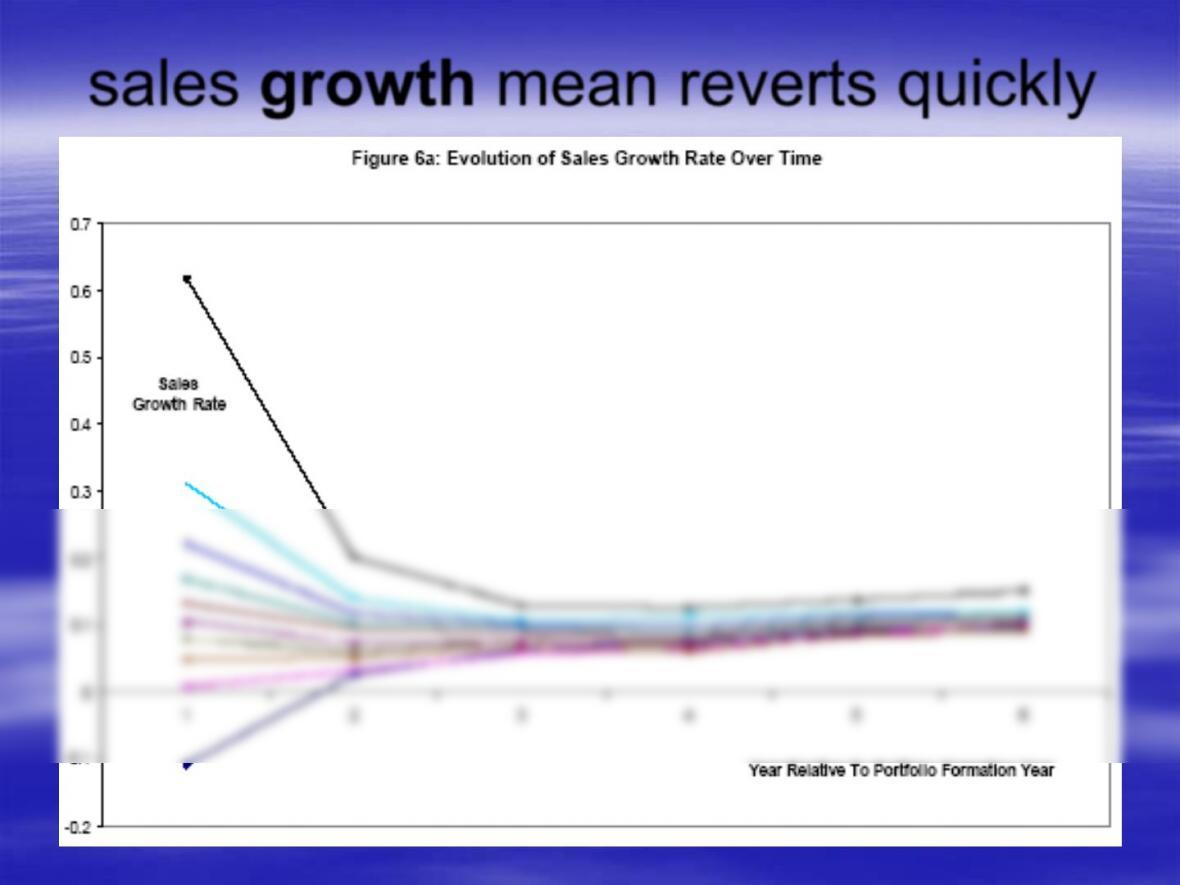

sales growth mean reverts quickly