Debt and Default

•Who cares about debt and default risk?

•Vfirm = Vequity + Vdebt

–If Vfirm > > Vdebt then use PV of respective future

pmts to value debt and equity

2

Predicting Default

•What does it

mean to

“default?”

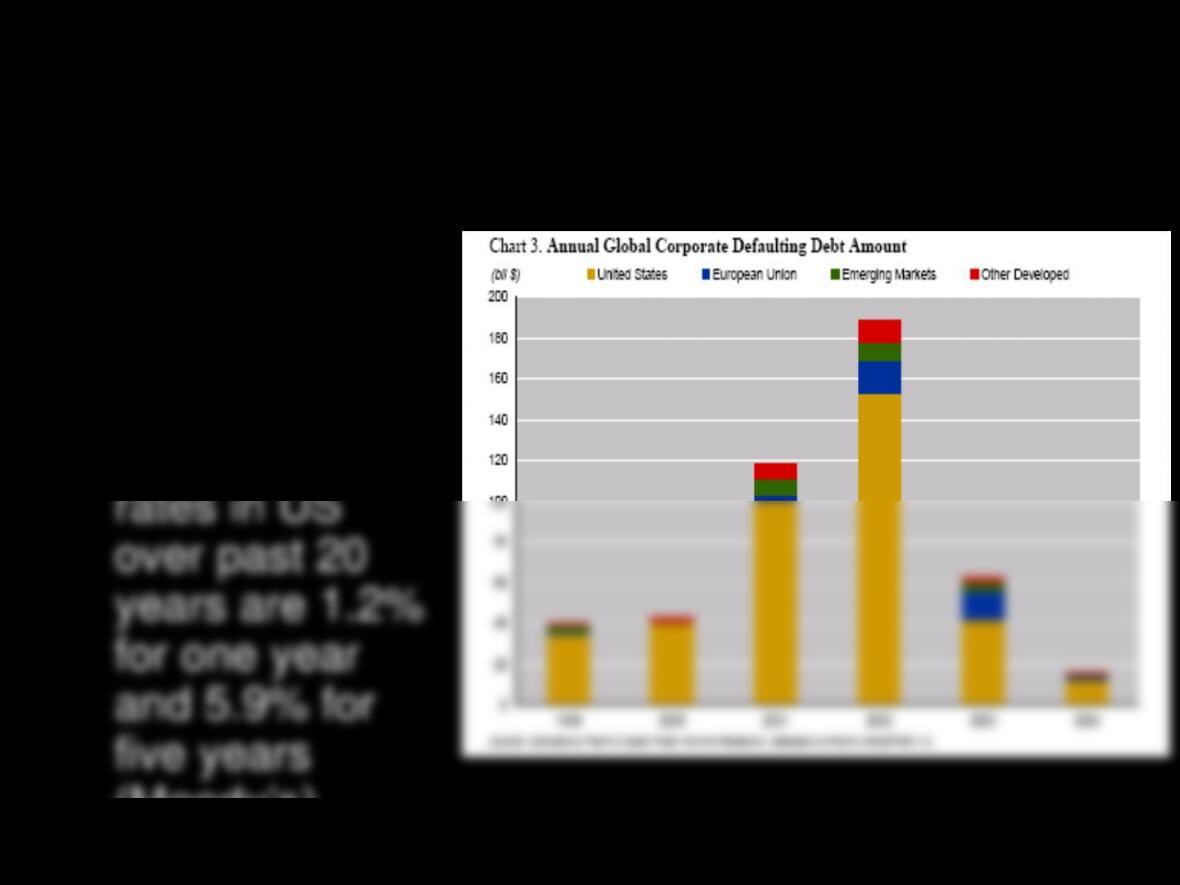

•Average default

(Moody’s).

$178B

3

Moody’s RiskCalc

http://riskcalc.moodysrms.com/

“Moody’s RiskCalc™ has been designed to act as an early

warning system to monitor changes in the credit quality

measuring, monitoring and managing portfolio credit

risk.”

What are the various determinants of Moody’s

RiskCalc?

4

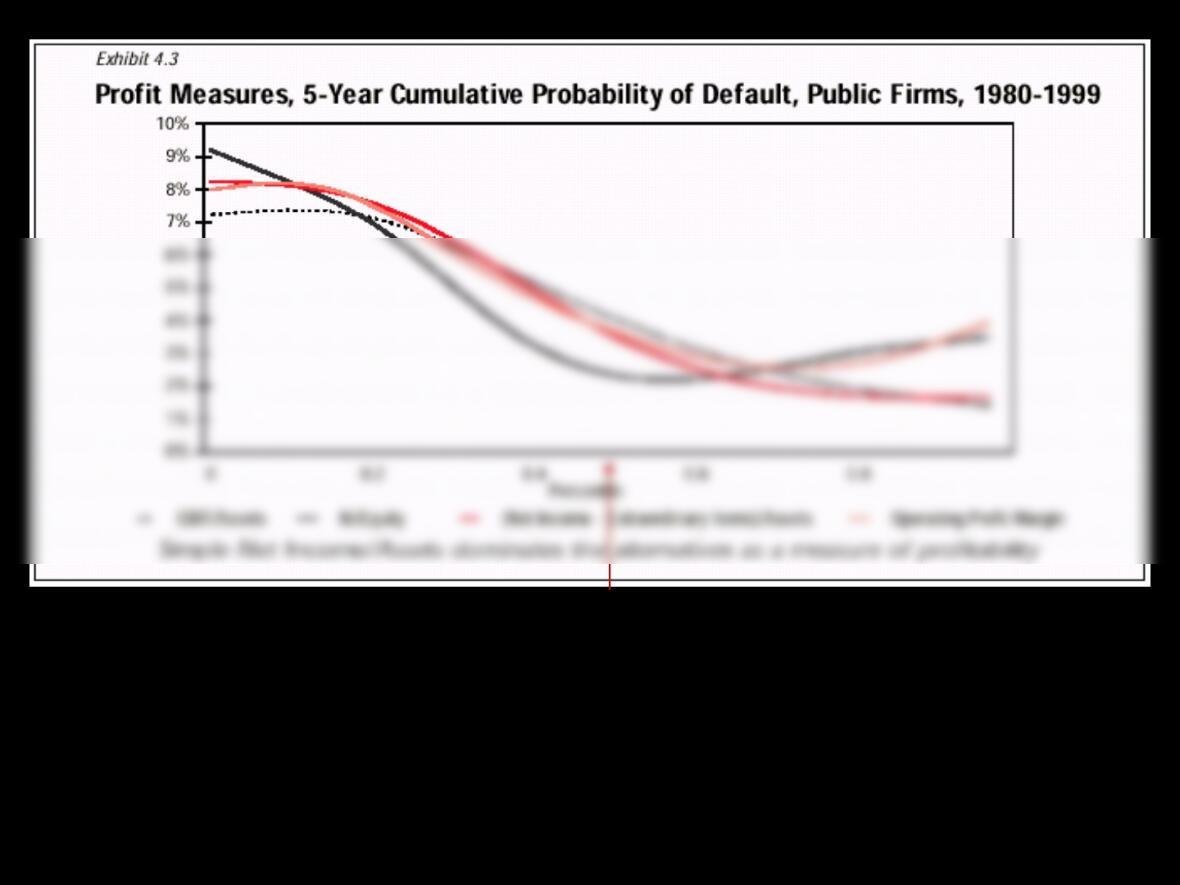

NI/Assets = .022

5

2.21

6

7

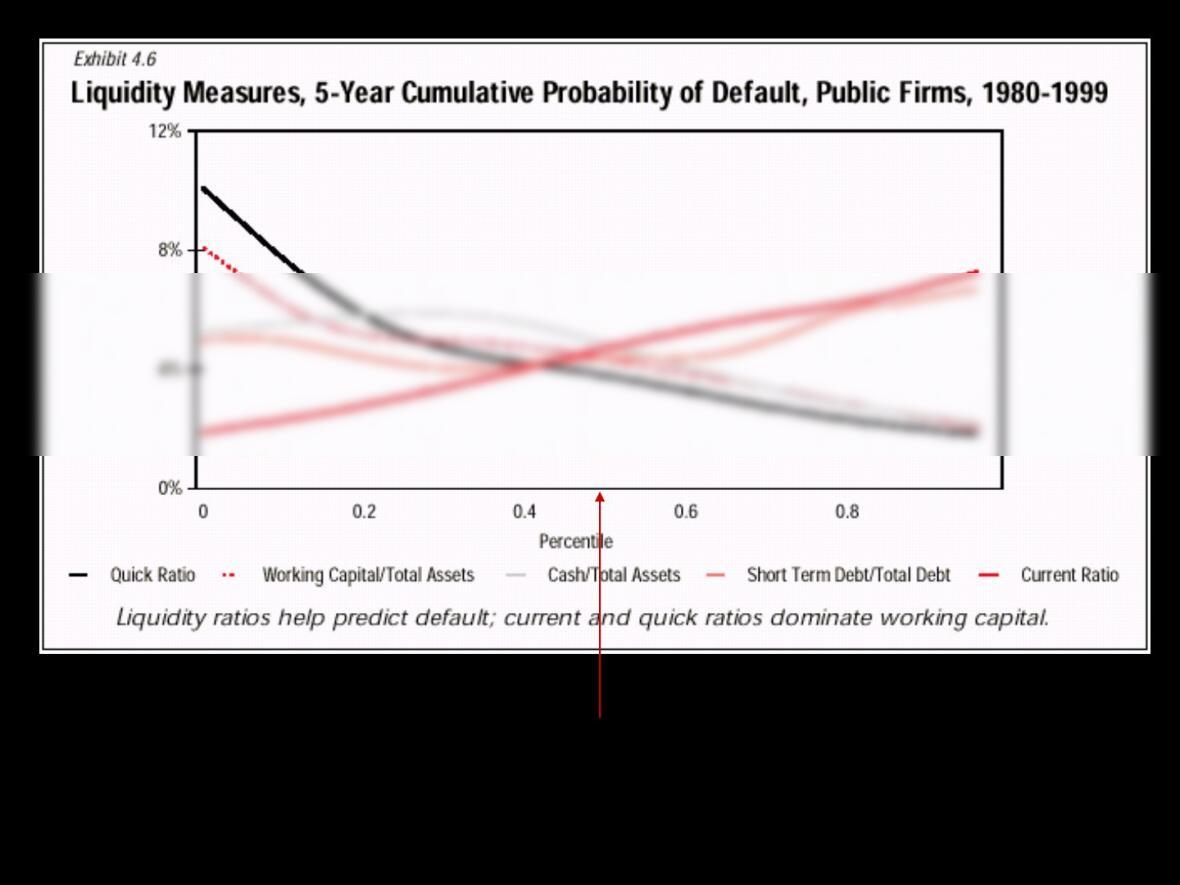

(CA –Inv)/CL = 1.2

8

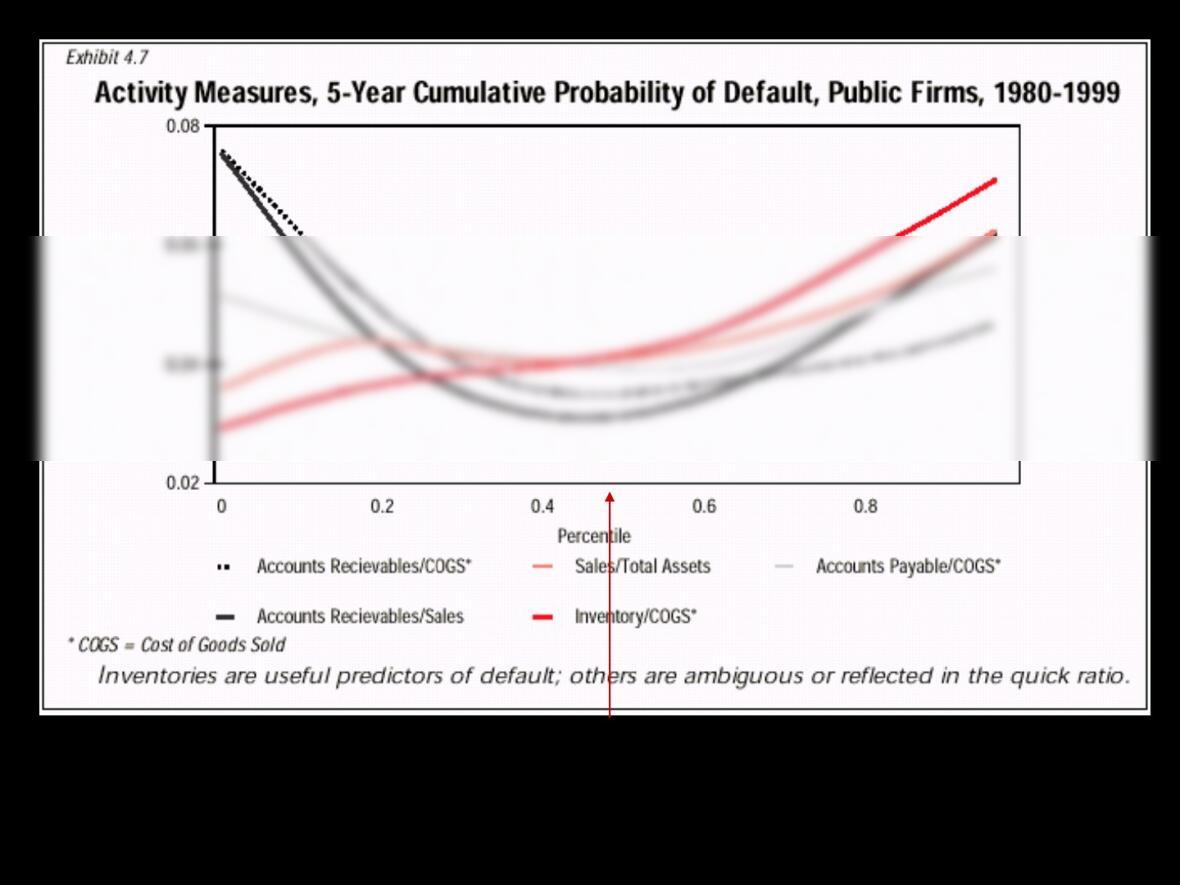

Inv/CGS = .137

or 50 days

9

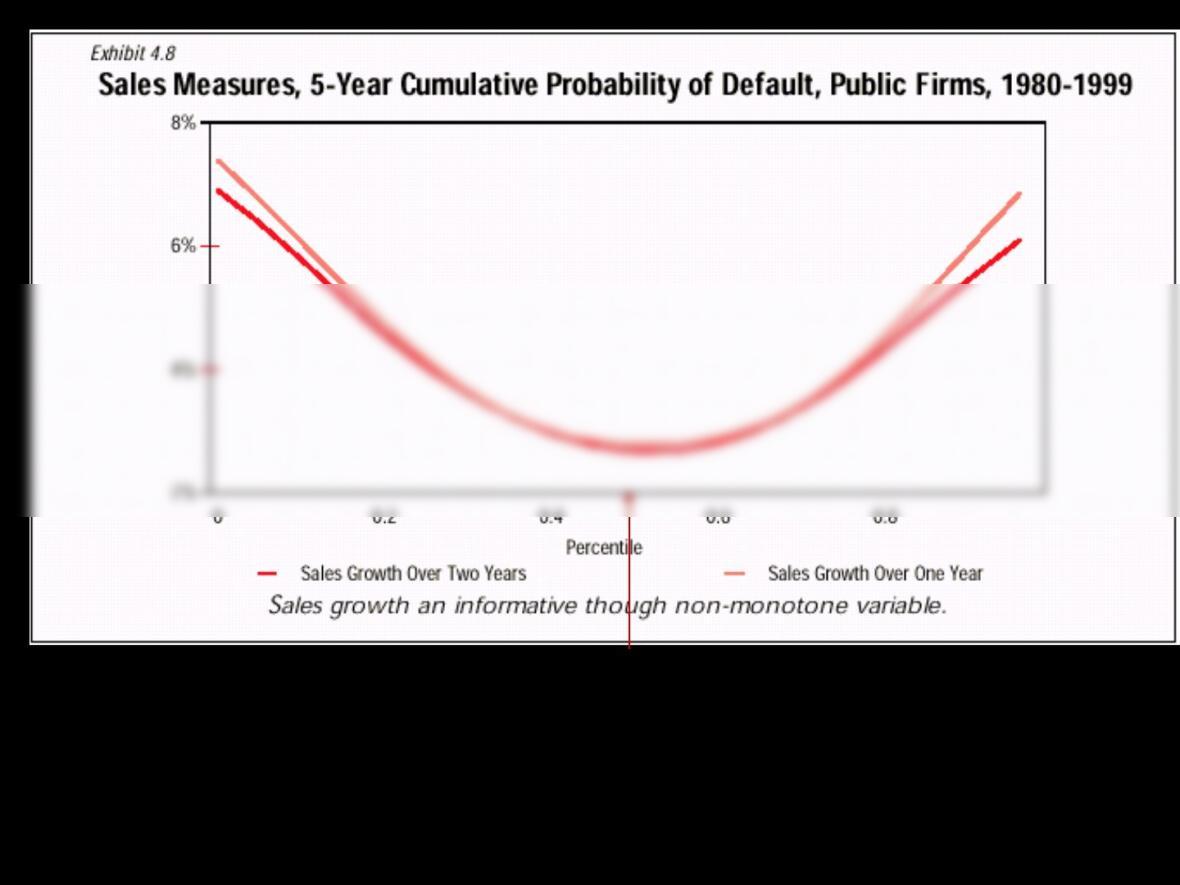

Sales growth =

.098

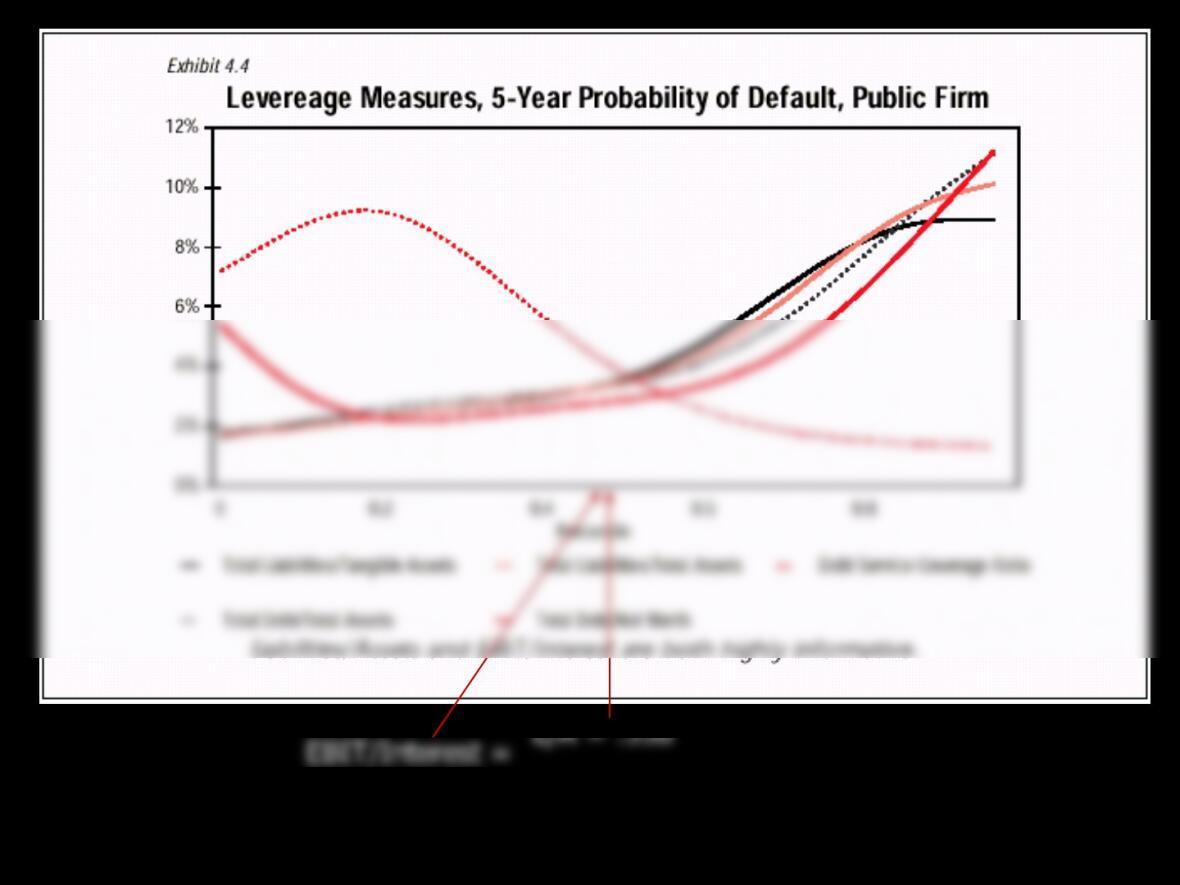

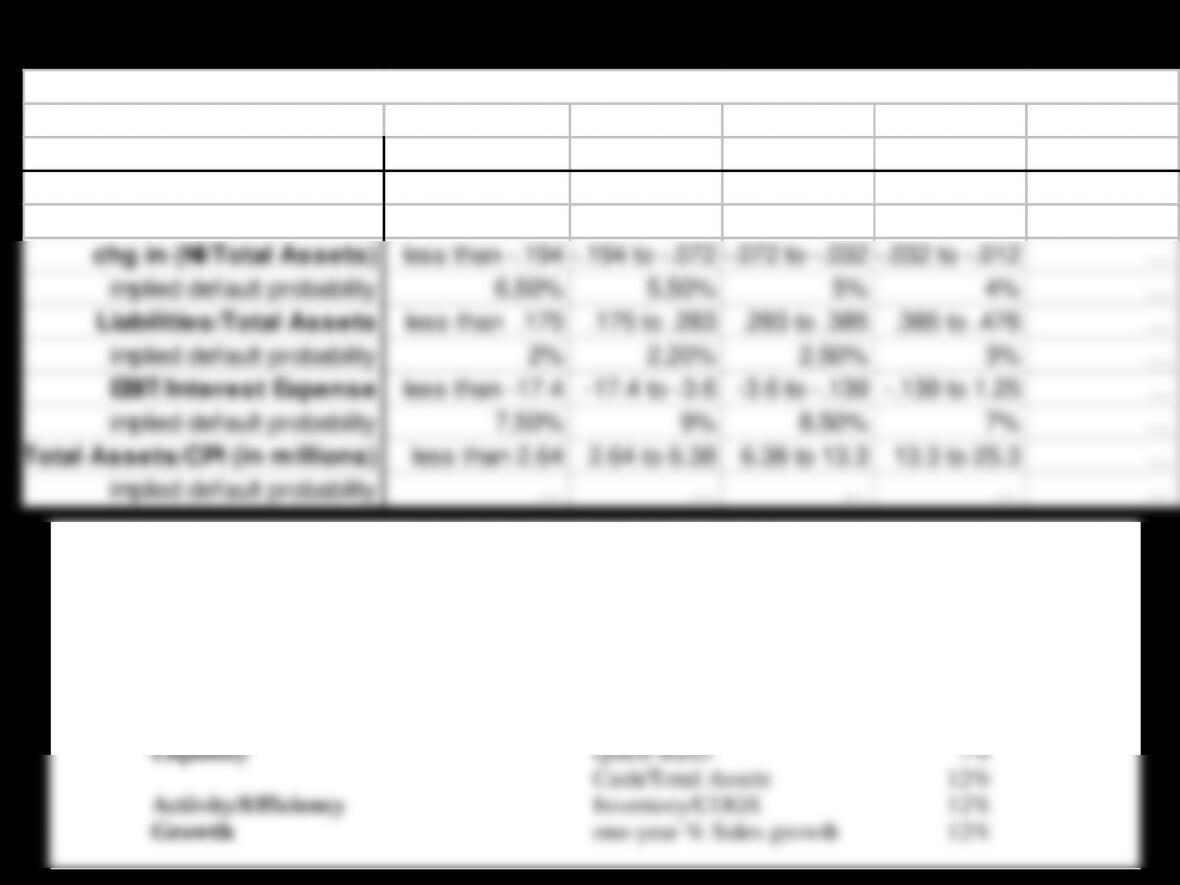

Table 1: Distribution of Financial Statement Ratios and Implied Default Probabilities

decile 0 to .10 .10 to .20 .20 to .30 .30 to .40 …

NI/Total Assets less than –.448 -.448 to –.161 -.161 to -.049 –.049 to .001 …

implied default probability 8.30% 8% 7.20% 5.50% …

chg in (NI/Total Assets) less than –.194 -.194 to –.072 -.072 to -.032 –.032 to –.012 …

implied default probability 6.50% 5.50% 5% 4% …

Liabilities/Total Assets less than .175 .175 to .283 .283 to .385 .385 to .476 …

implied default probability 2% 2.20% 2.50% 3% …

EBIT/Interest Expense less than –17.4 –17.4 to –3.6 –3.6 to –.139 -.139 to 1.25 …

implied default probability 7.50% 9% 8.50% 7% …

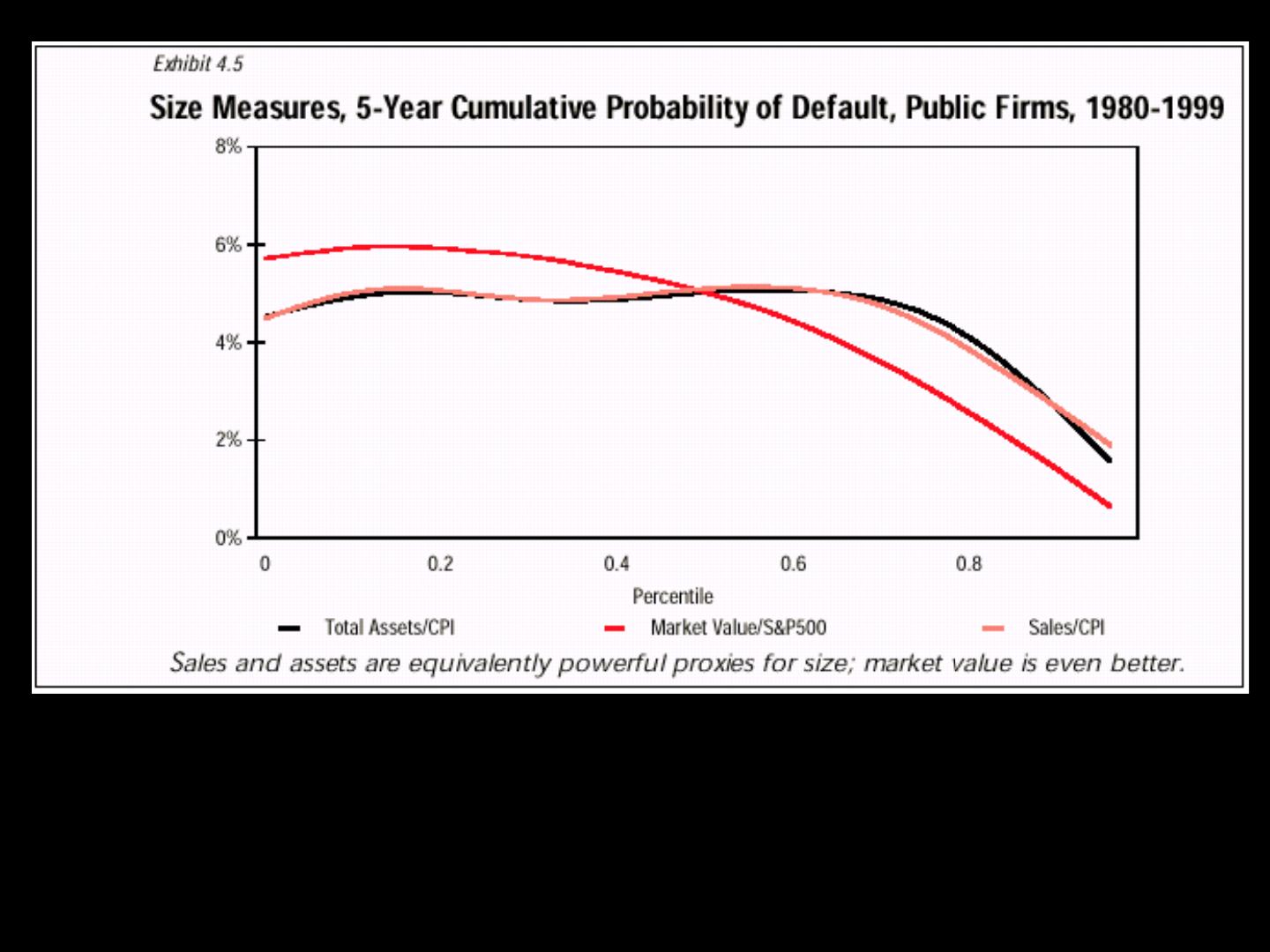

Total Assets/CPI (in millions)

less than 2.64 2.64 to 6.38 6.38 to 13.3 13.3 to 25.3 …

implied default probability … … … … …

Table 2: Modified RiskCalc Model

(apply these weights to the individual default probabilities from the graphs)

Profitability NI/Total Assets 9%

Moody’s RiskCalc Model