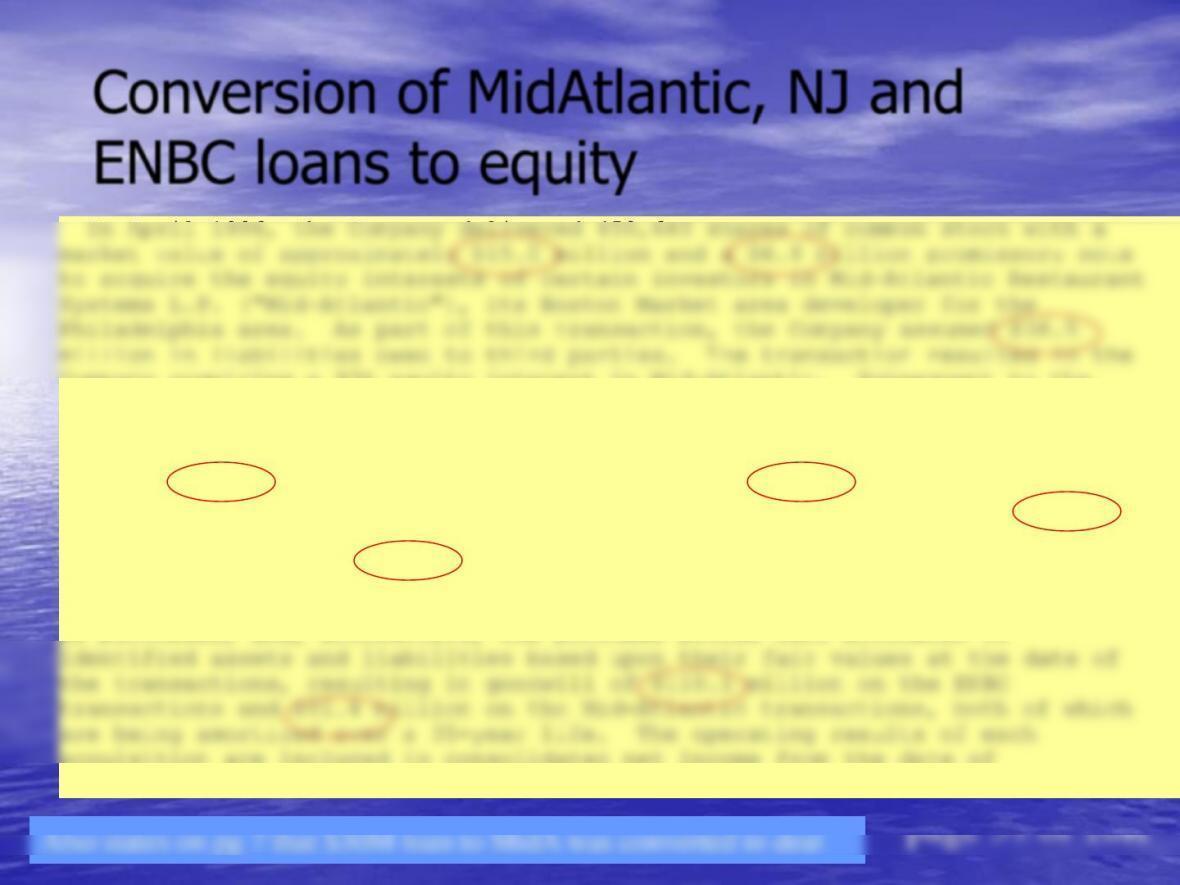

In April 1996, the Company delivered 450,640 shares of common stock with a

market value of approximately $15.0 million and a $6.8 million promissory note

to acquire the equity interests of certain investors in Mid–Atlantic Restaurant

Systems L.P. (“Mid–Atlantic”), its Boston Market area developer for the

developer for the southern New Jersey area (“New Jersey Rose”) for a purchase

price of $13.4 million, including the assumption of $1.1 million in liabilities

owed to third parties. Also, in June 1996, the Company converted its $120.0

million loan to ENBC into shares of common stock of ENBC and subsequently

invested an additional $45.9 million in ENBC common stock, resulting in an

ownership interest of approximately 53% of the outstanding shares of common

stock of ENBC as of March 7, 1997. These transactions have been accounted for

as purchases, and, accordingly, the purchase prices were allocated to

identified assets and liabilities based upon their fair values at the date of

the transactions, resulting in goodwill of $110.1 million on the ENBC

transactions and $81.4 million on the Mid–Atlantic transactions, both of which

are being amortized over a 35–year life. The operating results of each

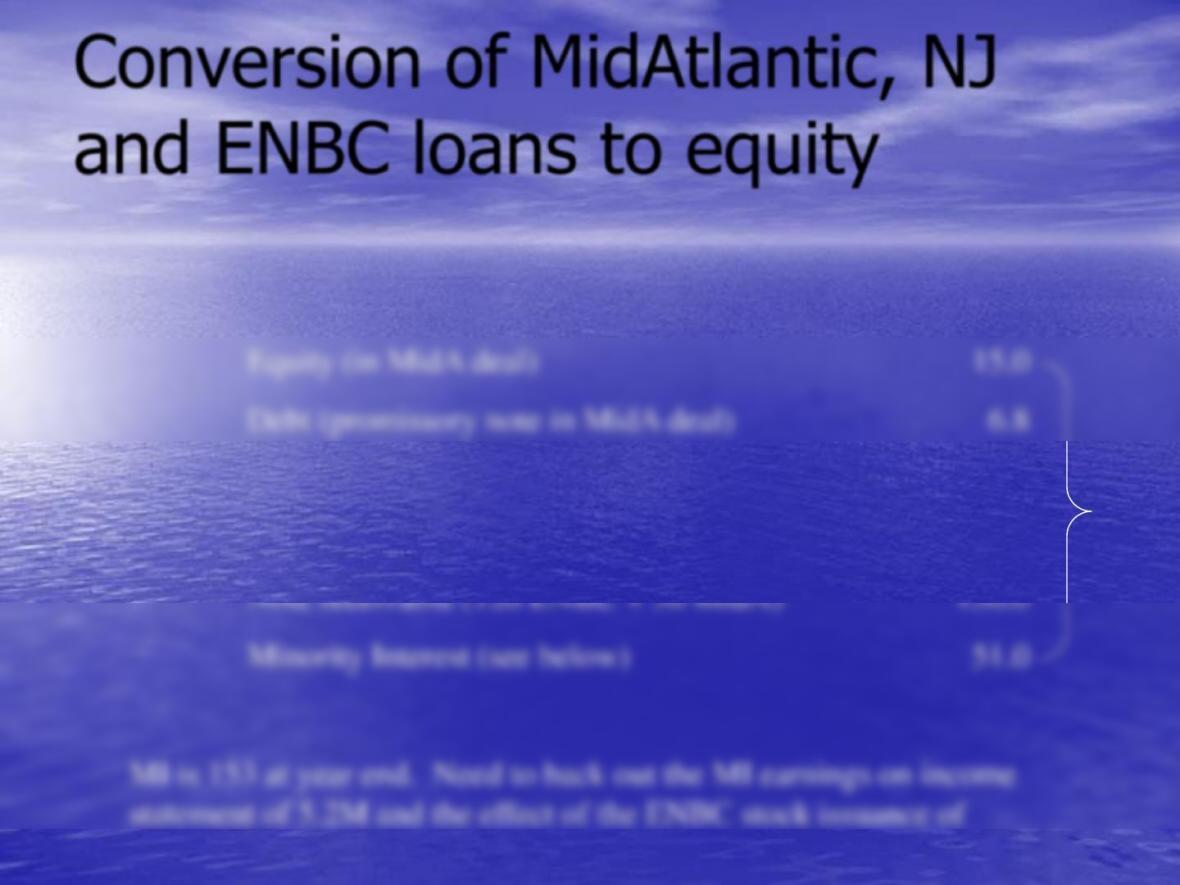

Conversion of MidAtlantic, NJ and

ENBC loans to equity

Conversion of MidAtlantic, NJ

and ENBC loans to equity

goodwill (81.4+110) 191.5M

Assets (plug) 130.2M

3rd party debt (38.5 MidA +1.1 NJ) 39.6

Cash (13.4 in NJ and 45.9 in ENBC) 59.3

97.2M.

321.7

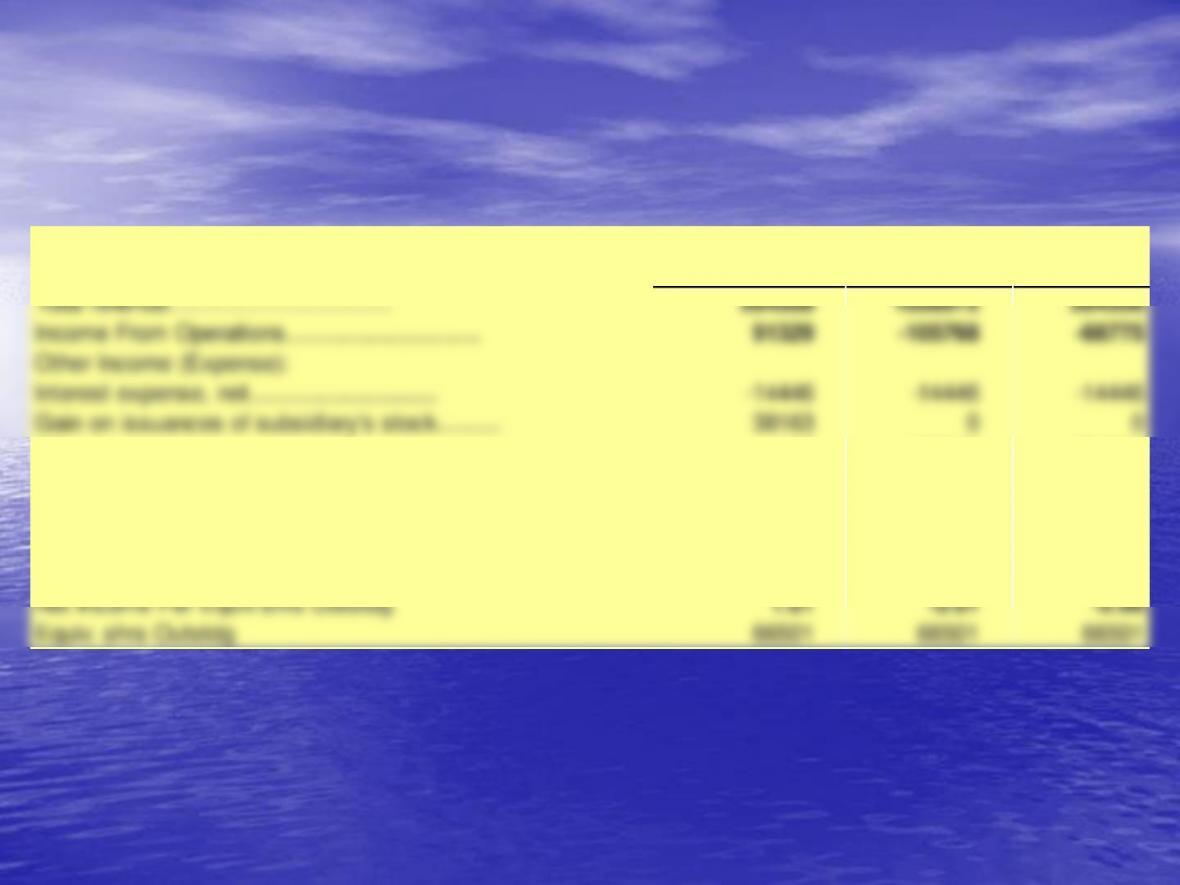

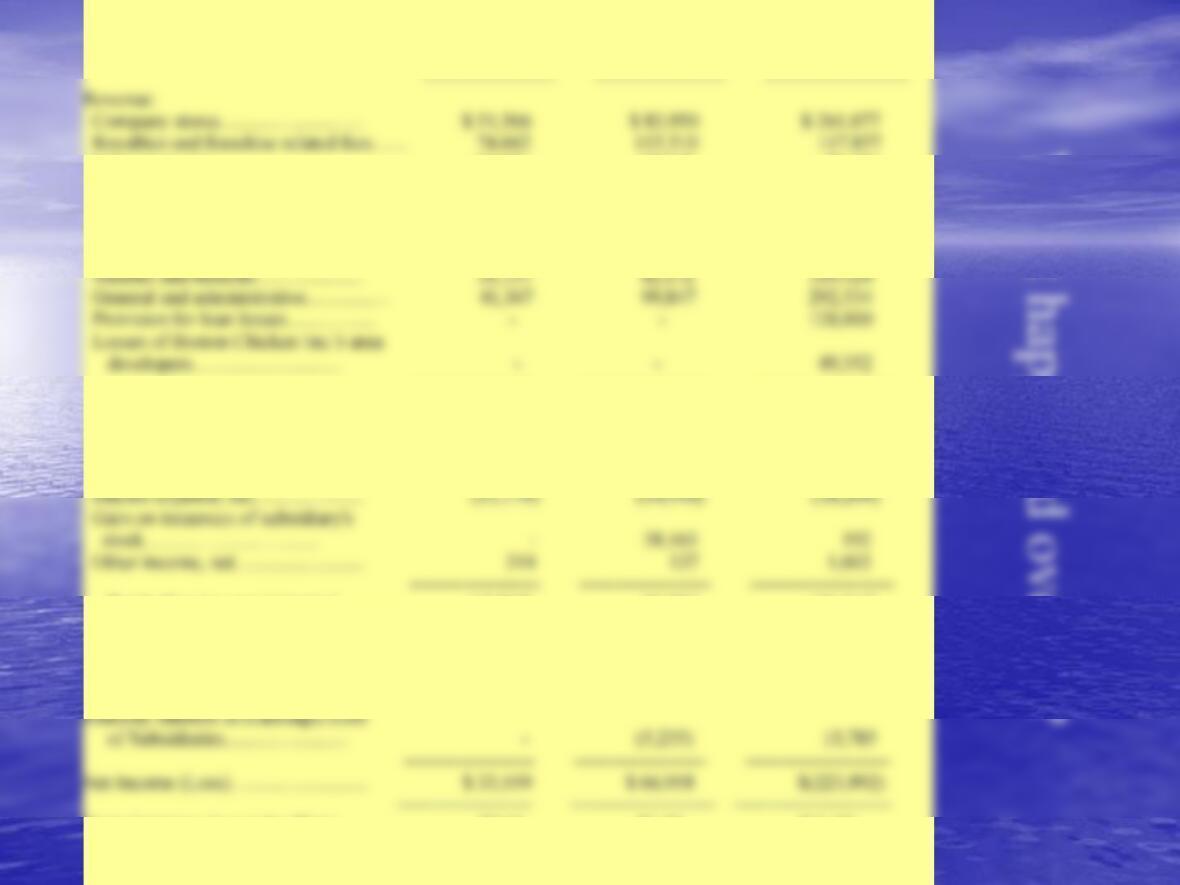

As Reported Consolidate AD Allowance

Total revenue………………………….. 264508 1058972 264508

Income From Operations………………………. 91329 –105768 –68775

Other Income (Expense):

Interest expense, net........................... –14446 –14446 –14446

Gain on issuances of subsidiary‘s stock......... 38163 0 0

Other income, net…………………………. 137 –191000 –191000

Income Before Income Taxes and Minority Interest................

115183 –311214 –274221

Income Taxes (37.3% ETR)……………………………….. 42990 –116083 –102284

Minority Interest in (Earnings) of Subsidiary..........................

BOSTON CHICKEN INC 1996 Income Statement Restated

Remove the gain on sale of ENBC stock and write off $191 in

goodwill from conversions/acquisitions.

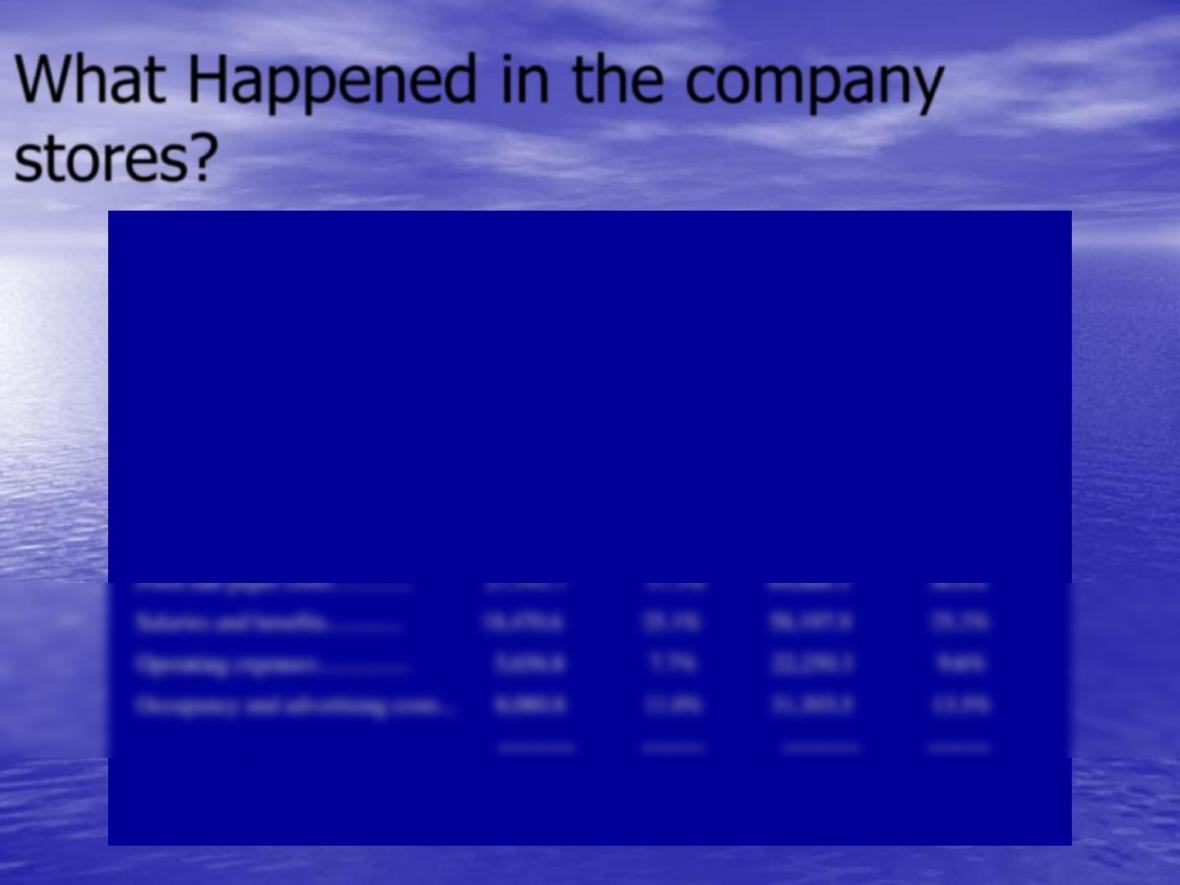

What Happened in the company

stores?

December 29, 1996 December 28, 1997

———-————-—— ——–—–—————-–

Number of Company stores

at year end……….………… 104 306

Net weekly revenue per store for the year. $ 23,643 $ 20,181

Net sales…………..……….. $ 73,512.7 100.0% $231,248.4 100.0%

Store cash flow………………. $ 13,862.8 18.9% $ 34,830.4 15.1%

========== ======== ========== ========

DECEMBER 31, DECEMBER 29, DECEMBER 28,

1995 1996 1997

Interest income………………….…… 33,251 65,048 83,434

——-————- ——————– ———————-

Total revenue……………………… 159,479 264,508 462,368

Costs and Expenses:

Cost of products sold…………………. 19,737 31,160 94,736

—————–— ——————– ———————-

Total costs and expenses……………. 92,241 173,179 674,046

————-——- ——————– ———————-

Income (Loss) from Operations……………. 67,238 91,329 (211,678)

Other Income (Expense):

Total other income (expense)………… (12,865) 23,854 (36,414)

————-——- ——————– ———————-

Income (Loss) Before Income Taxes

and Minority Interest………………. 54,373 115,183 (248,092)

Income Taxes (Benefit)………………….. 20,814 42,990 (8,415)

Basic Earnings (Loss) Per Share.…………. $0.71 $1.07 $(3.32)

Exploiting Information in

Accruals

•Accruals represent the difference between

earnings and cash flows, so earnings consists

are susceptible to manipulation.

Measuring Operating Accruals

•Operating Accruals =

total assets, so

Operating Accruals

manipulation?

Cash flows from operating activities:

Net income………………………………………………….. $ 30,210 $ 17,523 $ 10,263

by operating activities:

Provision for stock grant, stock transfer and associate stock

options………………………………………………… – 644 1,122

Provision for deferred income taxes………………………….. 11,122 12,293

Depreciation and amortization……………………………….. 2,944 2,026 533

Net changes in asset and liability accounts, net of effects of

purchase of UFL:

Increase in accrued Membership income………………………. (1,196) (689) (672)

Increase in commission advances……………………………. (28,142) (22,891) (18,381)

Increase in other assets………………………………….. (304) (678) (1,360)

Increase in inventories…………………………………… (472) (489) (1,270)

Decrease (increase) in prepaid product commissions…………… 752 (513) (622)

(Decrease) increase in deferred revenue…………………….. (805) 771 1,390

Increase in Membership benefits……………………………. 1,159 787 315

(Decrease) increase in accounts payable and accrued expenses….. (5,373) 5,688 1,914

——– ——–

Prepaid legal SCF 1998 1997

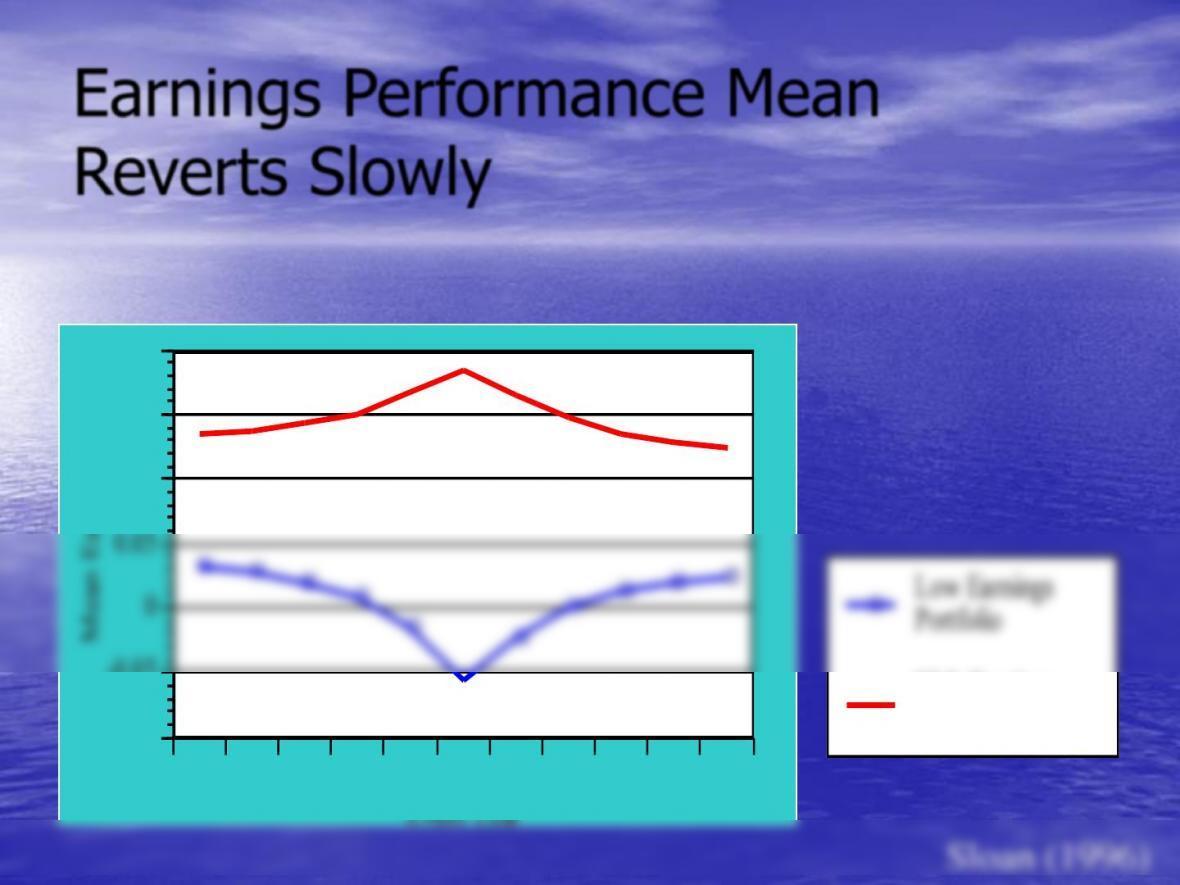

Earnings Performance Mean

Reverts Slowly

⚫⚫⚫⚫

⚫

⚫

⚫

⚫

⚫⚫⚫

-5 -4 -3 -2 -1 0 1 2 3 4 5

-0.1

0

0.05

0.1

0.15

0.2

Event Year

Low Earnings

⚫High Earnings

Portfolio