Forecasting Analysis (18)

⚫Evaluate the plausibility of the forecasting scenario

you provided in answer to the preceding question.

–We will defer the answer to this question until question 22

–Note that one particular challenge we face in this forecasting

will generate a substantial ‘cash float’ from its operations,

reducing the need for debt and equity financing. In reality,

we would expect Sirius to have a positive equity balance and

to ‘plug’ the balance sheet by holding excess financial assets

such as cash (insurance companies have similar financial

Forecasting Analysis (19)

⚫The ‘Revised Model’ (see Exhibit 2 of the model) assumes

that the diluted weighted average number of common stock

outstanding will remain constant at 1,628.3 million between

2006 and 2010. Compare these numbers to the number of

shares outstanding in your own eVal forecasting model and

explain any differences.

–This assumption is unreasonable. We know that Sirius has

Valuation Analysis (20)

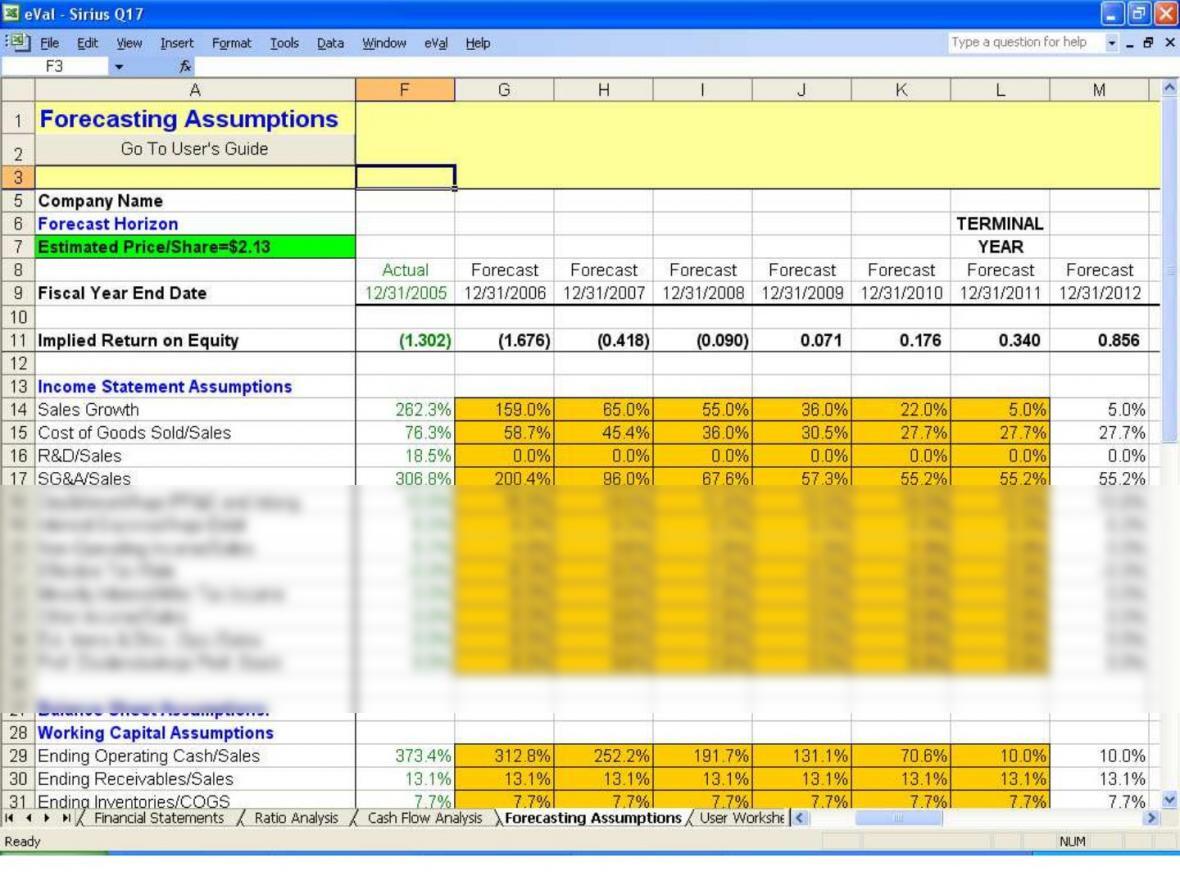

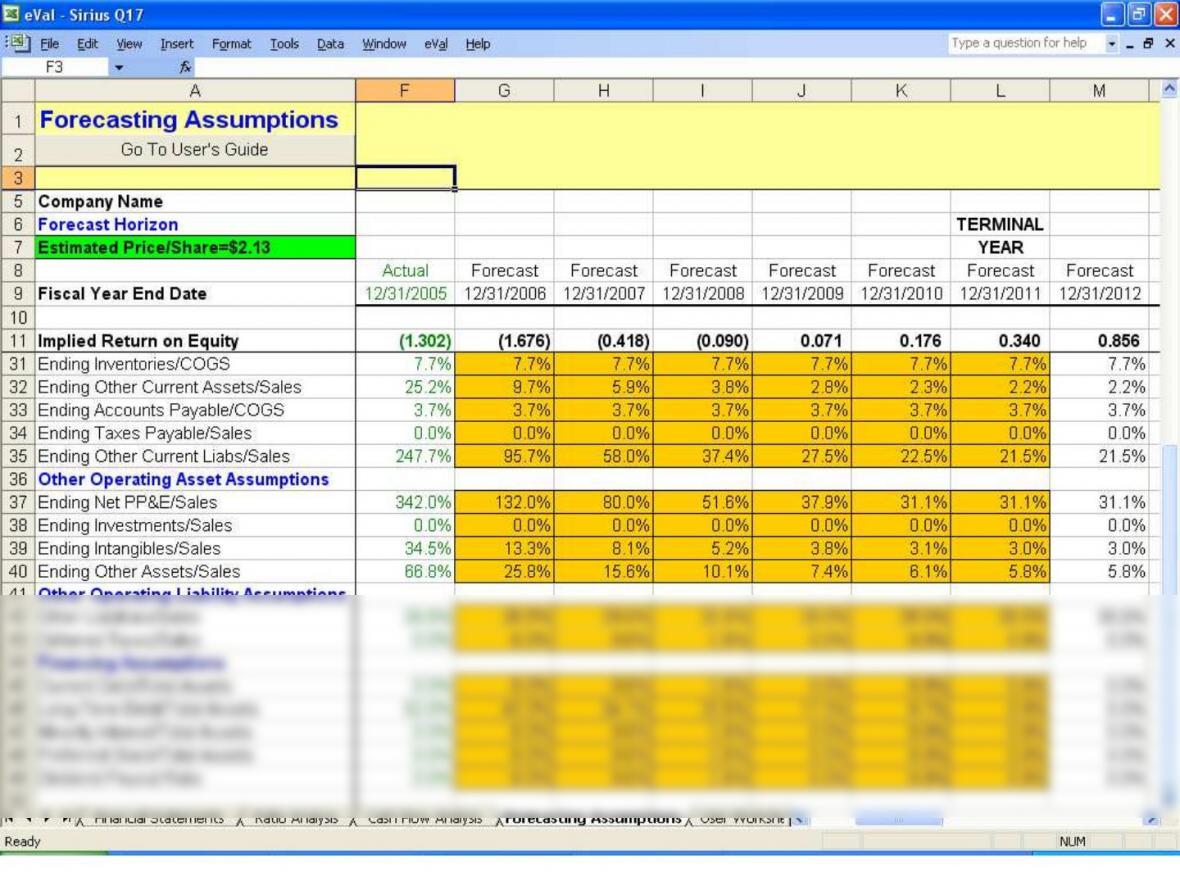

⚫The default valuation is less than -$20,000/share!

⚫The negative valuation arises because the default assumptions

support its unprofitable growth (look at equity and debt issues in

Cash Flow Analysis sheet).

⚫Note that the main causes of the negative valuation are the lack of

economies of scale built into the cost and operating asset

assumptions.

Valuation Analysis (21)

⚫In mid 2006, Sirius was trading at around $4.50/share.

Using eVal, provide a set of forecasting assumptions

–Start with valuation from Q. 17

–Change terminal SG&A assumption to 47%

–Valuation = $4.45/share

Valuation Analysis (22)

⚫Based on your analysis above, evaluate the plausibility

of the $5.79 price target proposed in the sell-side

analyst model (see Exhibit 1 of the model).

implying RNOA of 137%

–This is just for the $4.45 valuation

⚫Sirius Reports Fourth Quarter and Full Year 2006 Results

– Achieves First-Ever Quarter of Positive Cash Flow from Operations and

Free Cash Flow

– 2006 Revenue Increases 163% to a Record $637 Million

– Highest Satellite Radio Subscriber Share in Company‘s History

– 2007 Outlook For More Than 8 Million Subscribers and Revenue

Approaching $1 Billion

company‘s history.

⚫“In 2006, SIRIUS added 2.7 million new subscribers, an annual record for satellite radio, and

captured 62% share of satellite radio subscriber growth. More importantly, SIRIUS achieved

positive free cash flow in the fourth quarter 2006 — four years after adding our first

subscriber,” said Mel Karmazin, CEO of SIRIUS. “The fourth quarter marked the fifth

–2006 Cost of Equity Grants = $438 million

–2006 Net Loss = $1.1 billion

Key Takeaways

⚫Both earnings and cash flows can be managed

⚫Economies of scale can make default ‘straight line’

sustainability of these business models is often

questionable