Valuation Equations

or

what’s happening inside the

computer

for the period ending

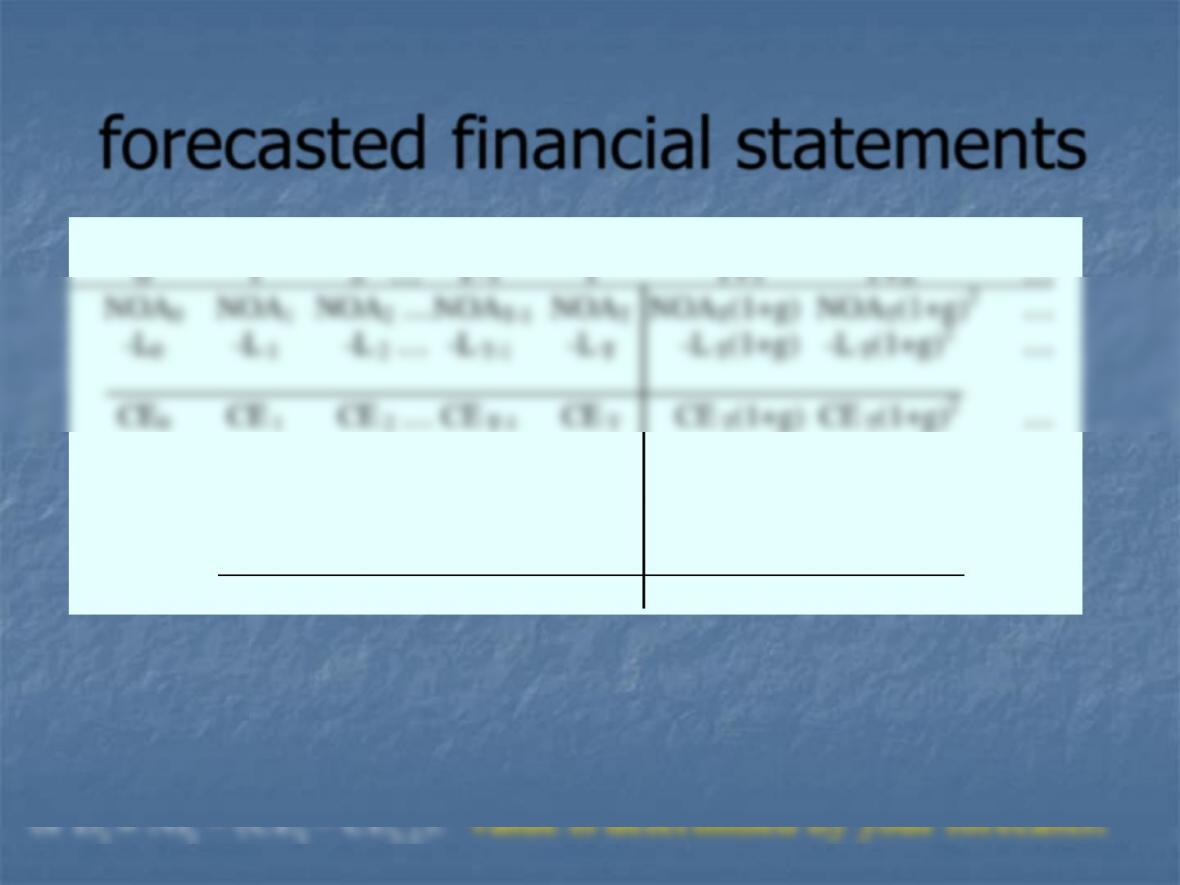

0 1 2 … T-1 T T+1 T+2 …

NOA0 NOA1 NOA2 …NOAT-1 NOAT NOAT(1+g) NOAT(1+g)2 …

-L0 -L 1 -L 2 … -L T-1 –L T -L T(1+g) -L T(1+g)2 …

CE0 CE 1 CE 2 … CE T-1 CE T CE T(1+g) CE T(1+g)2 …

NOI1 NOI2 …NOIT-1 NOIT NOIT(1+g) NOIT(1+g)2 …

-I1 -I2 … -IT-1 -IT -IT(1+g) -IT(1+g)2 …

Define net dividends Dtso that CEt= CEt-1 + NIt–Dt,

forecasted financial statements

where

Dtis the net cash distributions to equity holders,

or free cash flow to common equity,

computed as NIt–(CEt–CEt-1), and

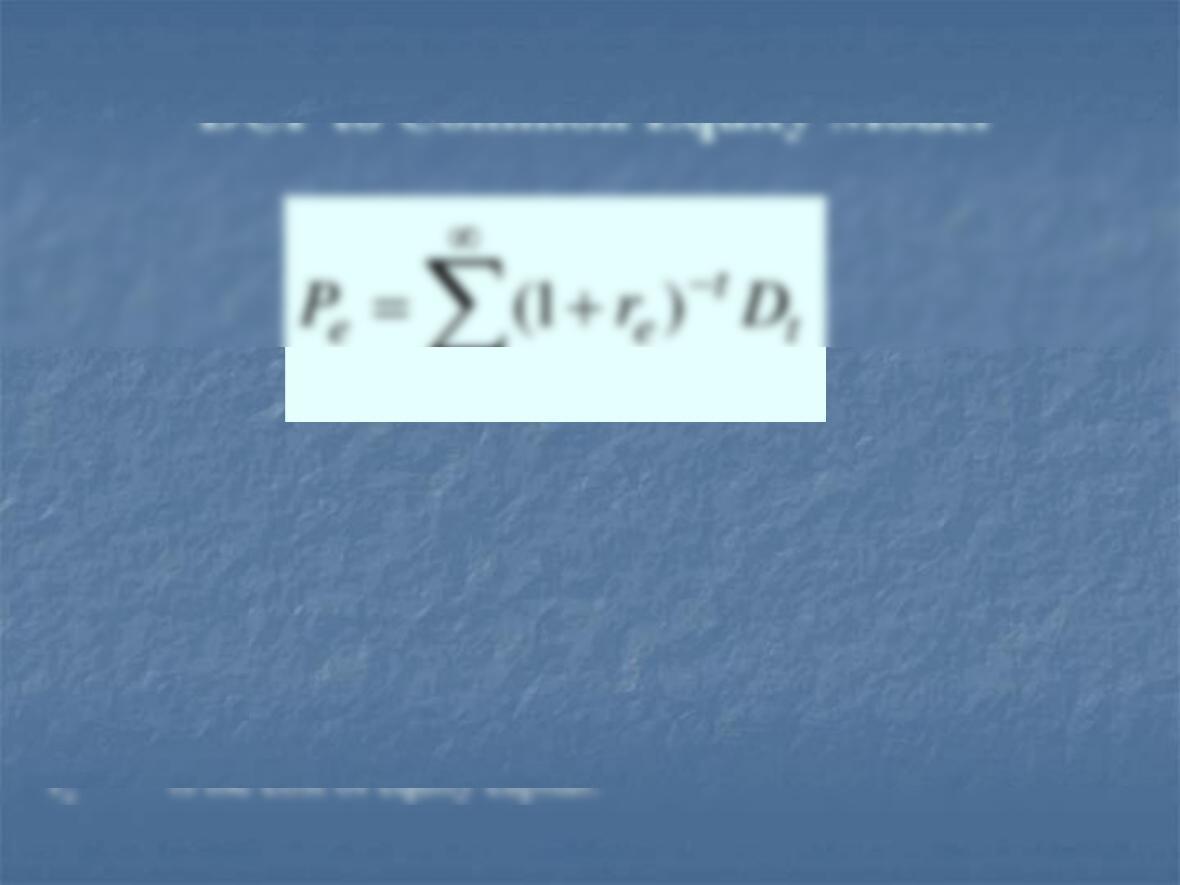

=

−

+=

1

)1(

t

t

t

ee DrP

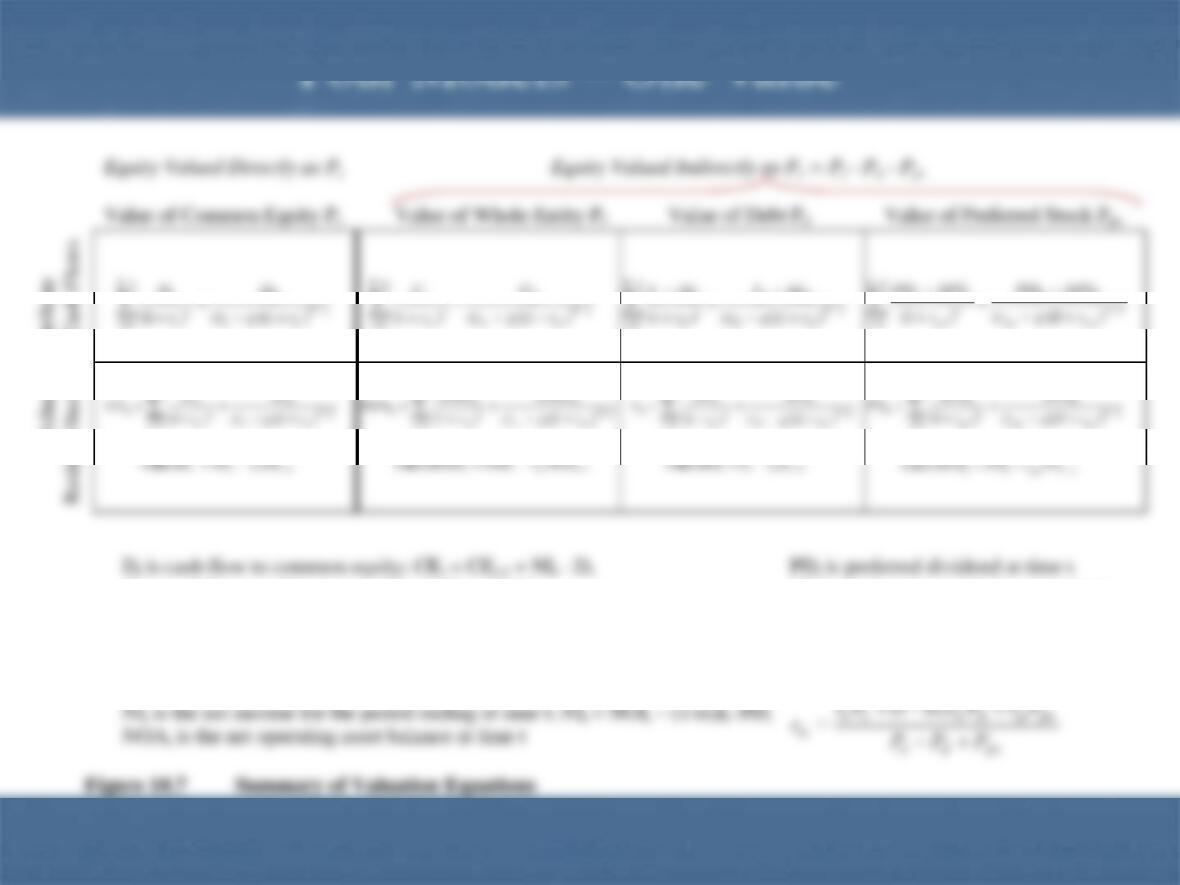

Equity Valued Directly as Pe Equity Valued Indirectly as Pe = Pf – Pd – Pps

Value of Common Equity Pe Value of Whole Entity Pf Value of Debt Pd Value of Preferred Stock Pps

1

1

ere wh

)1)(()1(

−

=

−=

+−

+

tett

ee

t

e

CErNIRI

rgr

r

1

1

ere wh

)1)(()1(

−

=

−=

+−

+

twtt

ww

t

w

NOArNOIRNOI

rgr

r

. ere w h

)1)(()1(

1

1

−

=

−=

+−

+

tdtt

t

dd

d

LrIRIT

rgr

r

. ere wh

)1)(()1(

1

1

−

=

−=

+−

+

tpstt

t

psps

ps

PSrPDRPD

rgr

r

Dt is cash flow to common equity; CEt = CEt-1 + NIt – Dt PDt is preferred dividend at time t

NOIt is the operating income for the period ending at time t, net of tax rps is the cost of preferred stock capital

It is the interest expense for the period ending at time t, rw is the weighted average cost of capital:

NIt is the net income for the period ending at time t; NIt = NOIt – (1-tx)It–PDt

NOAt is the net operating asset balance at time t

Figure 10.7 Summary of Valuation Equations

Valuation Attribute

Residual Income Cash Flows

psde

pspddee

wPPP

PrPrtxPr

r++

+−+

=)1(

Four Models –One Value

Define residual income RIt= NIt–reCEt-1. (NIt= RIt+ reCEt-1)

Start with Dt= NIt –(CEt–CEt-1) and substitute in RI tto get

Dt= CEt-1 –CEt+ RIt+ reCEt-1.

Substitute this for all future Dtin the dividend discount model to get

=

−++−+=

1

t

t

…..

)1()1(

11

)1( 2

2

0

1

−

+

+

+

−

+

+

+

−++=

=

ee

ee

t

t

ee r

r

r

r

CERIrP

−

++=

t

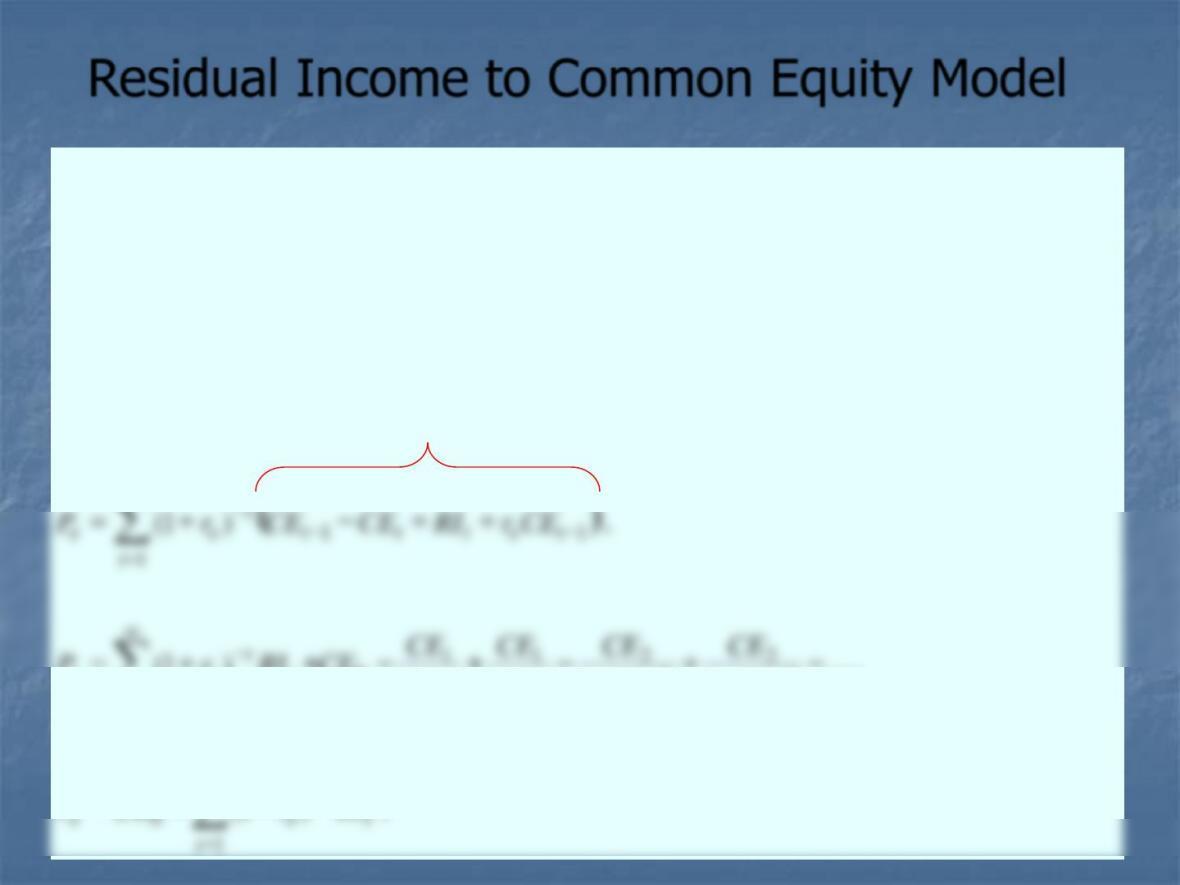

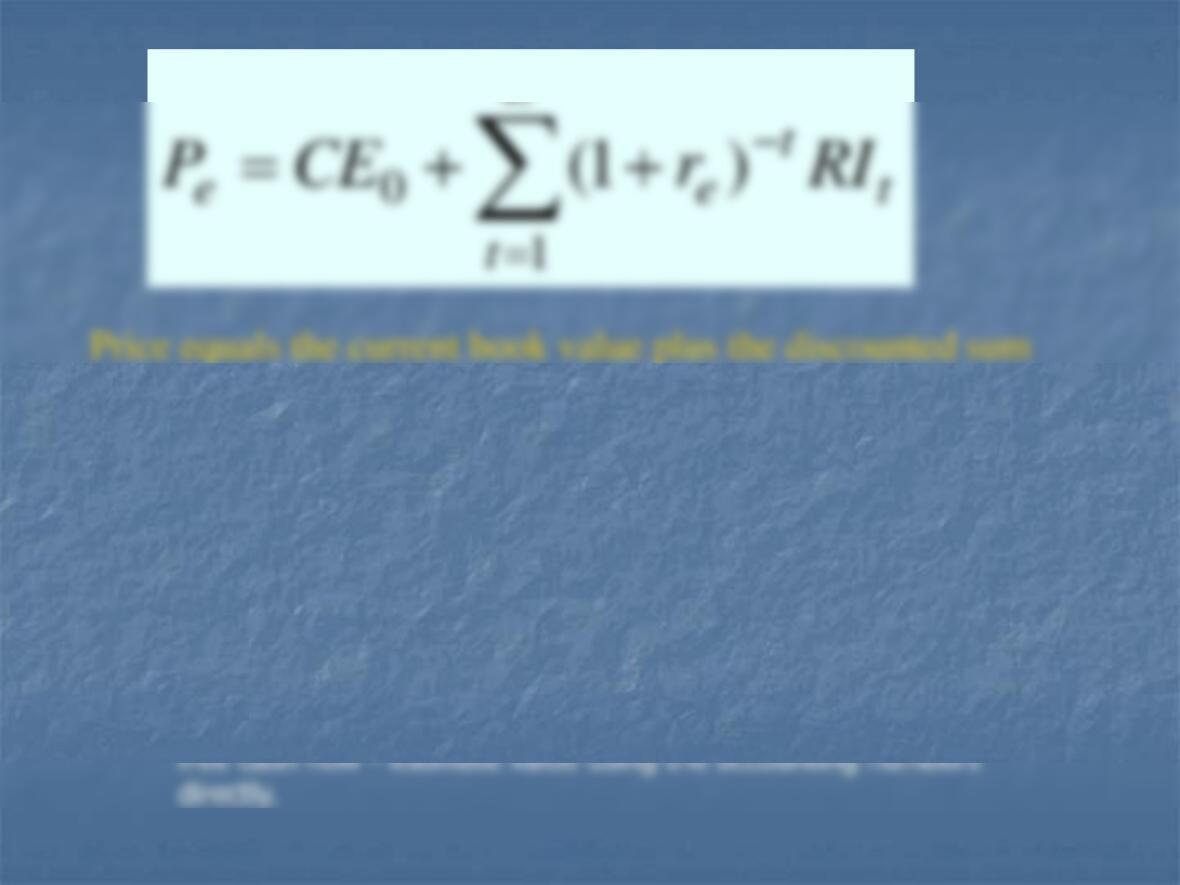

Residual Income to Common Equity Model

of expected future residual income (abnormal earnings).

=

−

++=

1

0)1(

t

t

t

ee RIrCEP

Advantages over cash flow models:

1) business, accounting and financial analysis are all in terms of

accounting numbers.

2) avoids having to “undo” the accounting to get to dividends or

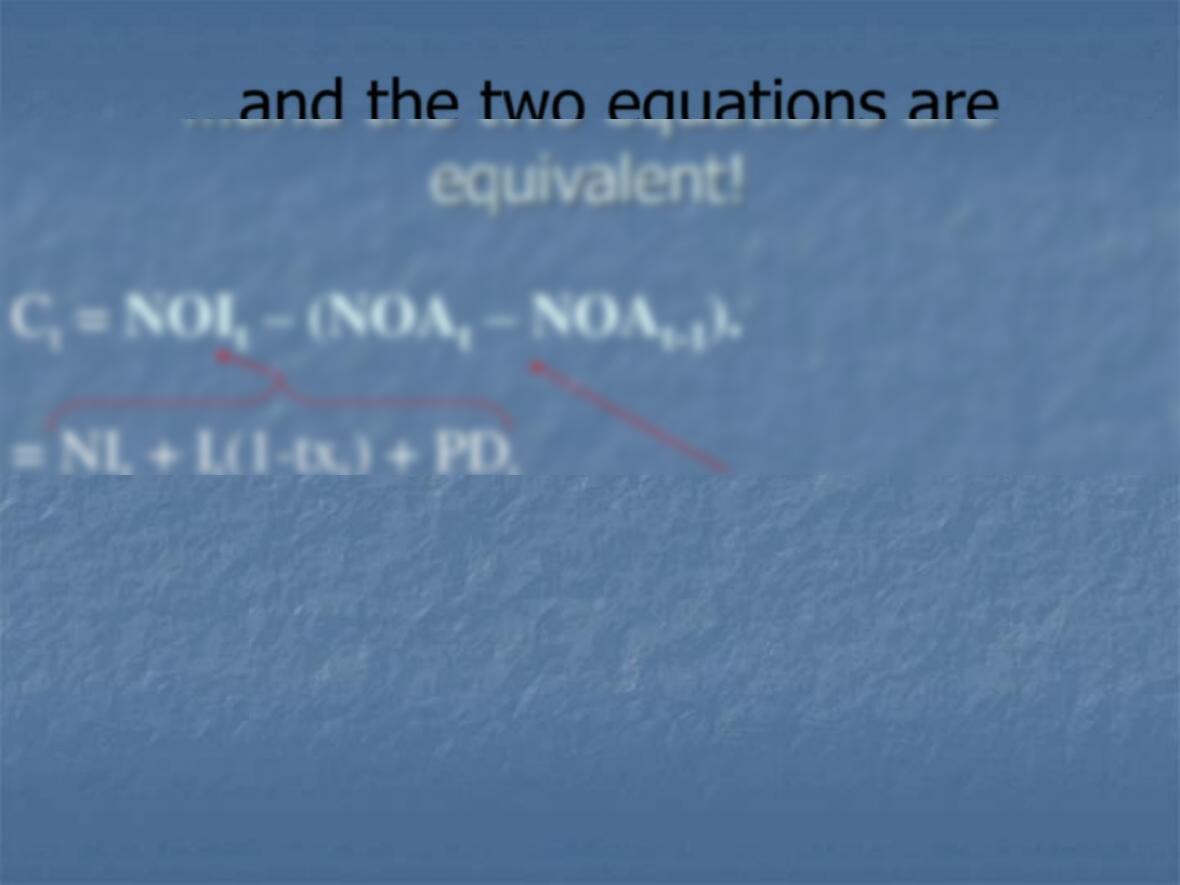

Ct= NOIt–(NOAt–NOAt-1).

Ct= Dt+ It(1-txt) –Lt+ PDt–PSt.

To common

To debt holders

To preferred

Free Cash Flow to All Investors can be computed from

Statement of cash flow data as

–(CEt+Lt+PSt–CEt-1 –Lt-1–PSt-1)

= NIt –(CEt–CEt-1) + It(1–txt) –Lt + PDt –PSt

= Dt+ It(1-txt) –Lt+ PDt–PSt.

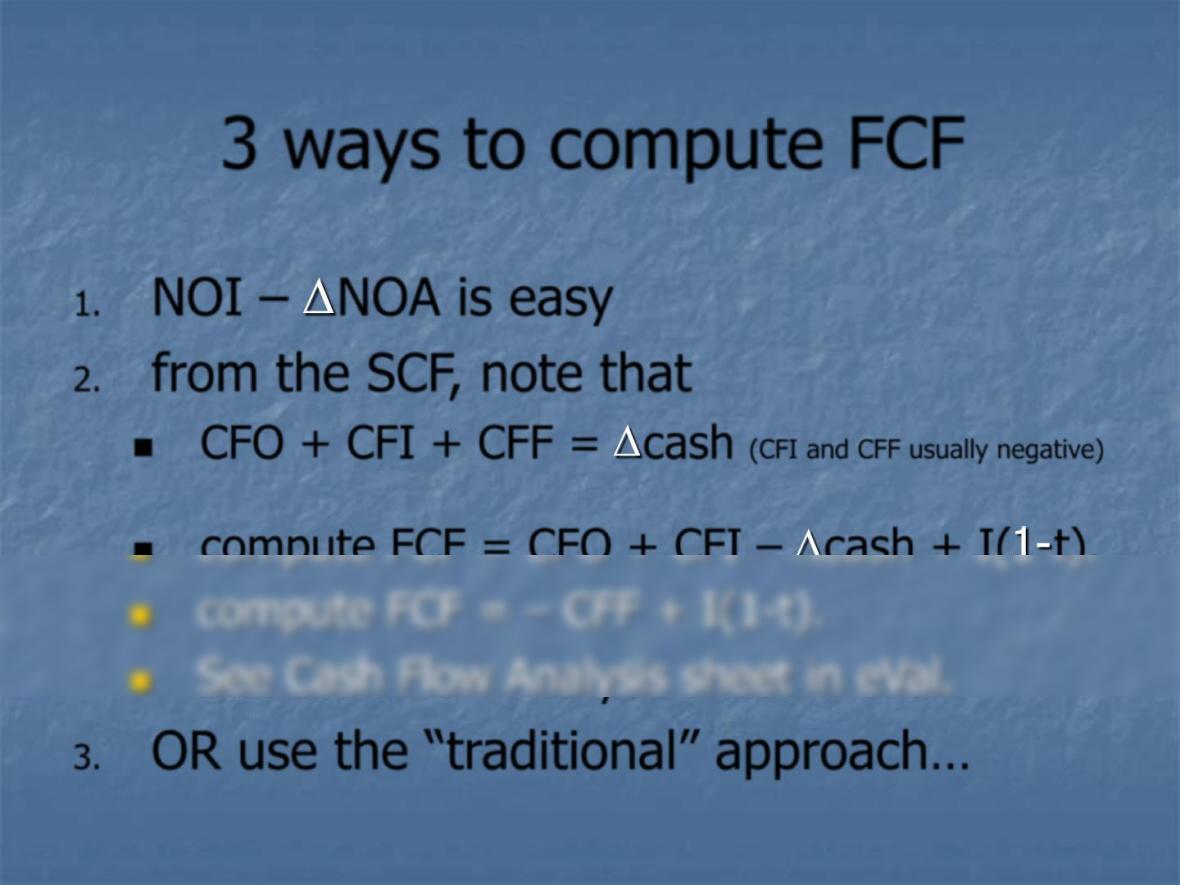

3 ways to compute FCF

1. NOI –NOA is easy

2. from the SCF, note that

◼CFO + CFI + CFF = cash (CFI and CFF usually negative)

3. OR use the “traditional” approach…

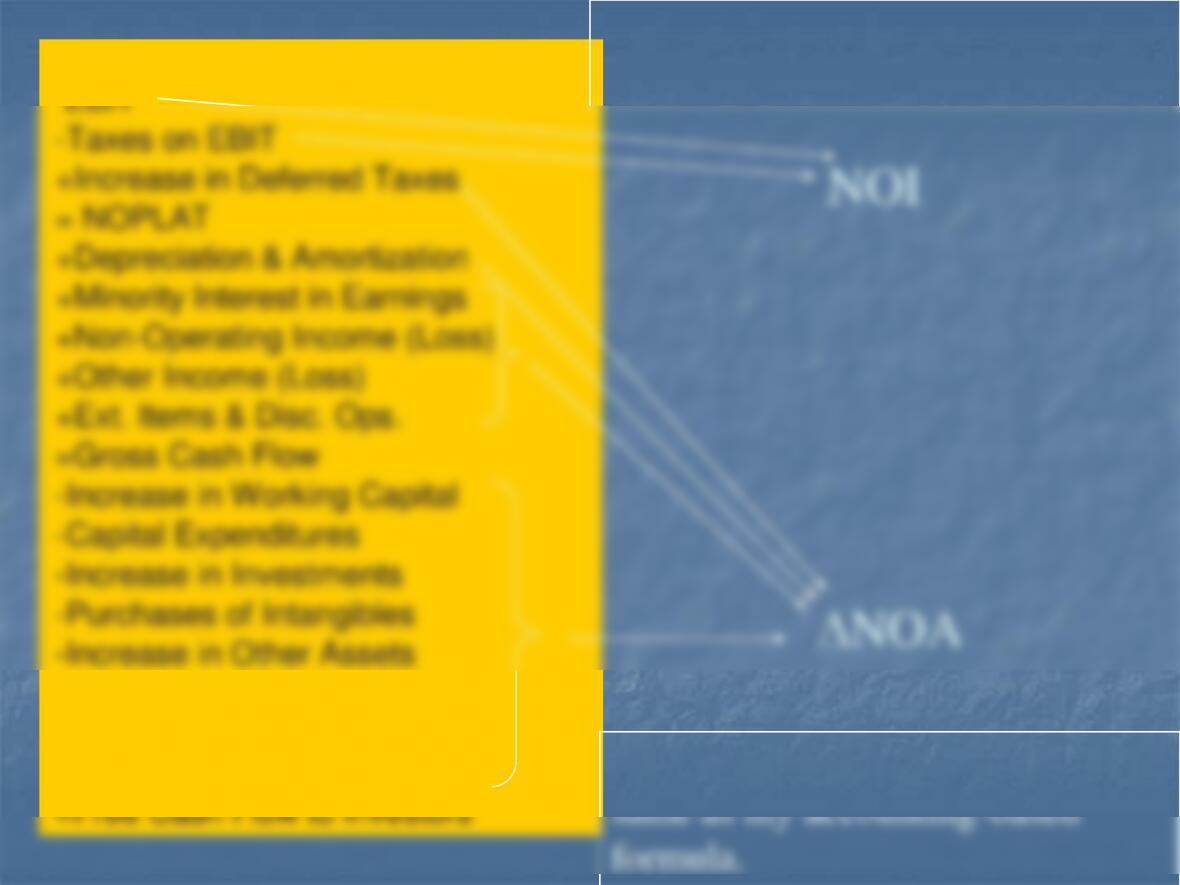

Free Cash Flow Generated (Used):

EBIT

-Taxes on EBIT

+Increase in Other Liabilities

+/-Clean Surplus Plug (Ignore)

The Traditional FCF recipe for the

DCF model is

But it works out to be exactly the