Archives: Solution Manual

Accounting Chapter 10 A zero coupon bond simply means that no periodic

Financial Accounting, 10/e 10–37 P10–15. Req. 1 Present value: $800,000 x 0.56743 = $453,944 $64,000* x 3.60478 = 230,706 Issue price = $684,650 *$800,000 x .08 **Using Excel or a financial calculator results in a present value of $684,647 (rounded). […]

Accounting Chapter 10 Relying just on the ratios computed above

Financial Accounting, 10/e 10–21 E10–23. Present value: $1,400,000 x 0.78941 = $1,105,174 $56,000* x 7.01969 = 393,103 Issue price = $1,498,277 ** *$1,400,000 x .08 x 1/2 **Using Excel or a financial calculator results in a present value of $1,498,276 […]

Accounting Chapter 10 The Difference The Result Rounding The Present

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 10 Reporting and Interpreting Bonds ANSWERS TO QUESTIONS 1. A company might choose to issue bonds instead of stock […]

Accounting Chapter 10 Were These Bonds Issued Discount Premium Why

Chapter 10 – Reporting and Interpreting Bond Securities 10–14 2. Several years ago, Amazon issued callable bonds with a face value of $100,000; when the book value was $101,000, Amazon called the bonds at 102% of face value a. Journal […]

Accounting Chapter 10 Refer Students Pause For Payments Are Accounted

Chapter 10 – Reporting and Interpreting Bond Securities 10-1 CHAPTER 10 REPORTING AND INTERPRETING BOND SECURITIES Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects 10-1 Describe the characteristics of bond securities. […]

Accounting Appendix A The fair value method must be used when less

Financial Accounting, 10/e Appendix A-35 APA–3. Req. 1 The fair value method must be used for both securities: (1) For Square common stock, only 6% of the outstanding shares is owned (below the 20% limit), and it is assumed there […]

Accounting Appendix A No entry is required for either security because

Financial Accounting, 10/e Appendix A-21 PA–4. Req. 1 The fair value method must be used for both securities: (1) For D-Light common stock, only 15% of the outstanding shares is owned (below the 20% limit), and it is assumed there […]

Accounting Appendix A A short-term investment is one that meets

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Appendix A Reporting and Interpreting Investments in Other Corporations ANSWERS TO QUESTIONS 1. A short-term investment is one that meets […]

Accounting Appendix A The account is reduced by the proportional amount

Appendix A – Reporting and Interpreting Investments in Other Corporations Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. expense 8. Dividends Declared will receive $20,000 ($0.50 × 40,000 shares) […]

Accounting Appendix A The Trading Securities Portfolio Adjusted Down Fair

Appendix A – Reporting and Interpreting Investments in Other Corporations App A – 1 APPENDIX A REPORTING AND INTERPRETING INVESTMENTS IN OTHER CORPORATIONS Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects […]

Accounting Chapter 9 Accrual-based accounting is more useful

Req. 2 December 31: Interest expense (+E, –SE). …………………………………….. 2,100 Interest payable (+L) …………………………………………… 2,100 ($35,000 x .08 x 9/12 = $2,100). December 31: Deferred rent revenue (-L) ……………………………………… 5,000 Rent revenue (+R, +SE) ……………………………………… 5,000 ($6,000 x 5/6 = […]

Accounting Chapter 9 Companies typically list obligations to pay suppliers

© 2020 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 9 Ensure The Equation Still Balances And Debits

Chapter 09 – Reporting and Interpreting Liabilities 9-13 and i must be restated to be consistent with the length of the interest period 2. If compounding is quarterly: a. The interest period is one quarter of a year (i.e., four […]

Accounting Chapter 9 Updated descriptions of how to calculate present

Chapter 09 – Reporting and Interpreting Liabilities 9-1 CHAPTER 9 REPORTING AND INTERPRETING LIABILITIES Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects 9-1 Define, measure, and report current liabilities. 1 1, […]

Accounting Chapter 8 Net Sales is disclosed on the Income Statement

CP8–2. (dollar amounts in thousands) 1. The company uses the straight-line method of depreciation. This is disclosed in Note 2 Summary of Significant Accounting Policies under the heading Property and Equipment, Net. 2. Accumulated depreciation was $642,434. This is disclosed […]

Accounting Chapter 8 ending inventory is to be reported at the lower of cost

Financial Accounting, 10/e 8-61 COMP8-1. (continued) Case D (continued) c. Weighted average Cost of ending inventory: Cost of goods available for sale $17,800 ($1,600 beg. + $16,200 purch.) ÷ Number of goods available ÷ 900 units Cost per unit $19.78 […]

Accounting Chapter 8 Failing Record Depreciation Expense Ratio Computation Earnings

Financial Accounting, 10/e 8-41 P8–6. Req. 1 a. Machine A – Sold on January 1 of the current year: (1) Depreciation expense for the current year – none recorded because disposal date was January 1. (2) To record disposal: Cash […]

Accounting Chapter 8 If the machine is used evenly throughout its

Financial Accounting, 10/e 8-21 E8–10. (continued) Req. 2 If the machine is used evenly throughout its life and its efficiency (economic value in use) is expected to decline steadily each period over its life, then straight-line depreciation would be preferable. […]

Accounting Chapter 8 Machinery Original Cost Accumulated Depreciation End

Chapter 8 Reporting and Interpreting Property, Plant, and Equipment; Intangibles; and Natural Resources ANSWERS TO QUESTIONS 1. Long-lived assets are noncurrent assets, which a business retains beyond one year, not for sale, but for use in the course of normal […]

Accounting Chapter 8 Misinterpretation Eliminate Its Effect Any Gain Or

Chapter 08 – Reporting and Interpreting Property, Plant, and Equipment; Intangibles; and Natural Resources 8-13 intangible assets for possible impairment 3. Two steps are necessary: estimated future cash flows, then asset is impaired b. Step 2: Compute Impairment Loss – […]

Accounting Chapter 8 Focus and contrast company data updated

Chapter 08 – Reporting and Interpreting Property, Plant, and Equipment; Intangibles; and Natural Resources 8-1 CHAPTER 8 REPORTING AND INTERPRETING PROPERTY, PLANT, AND EQUIPMENT; INTANGIBLES; AND NATURAL RESOURCES Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems […]

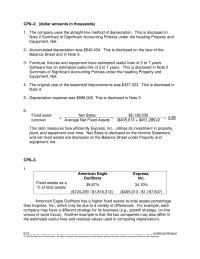

Accounting Chapter 7 American Eagle Outfitters Was More Successful Than

AP7–4. (continued) Req. 2 2016 2017 2018 2019 Gross profit ratio (gross profit ÷ sales): Before correction: $21,000 ÷ $60,000 = 0.35 $20,000 ÷ $63,000 = 0.32 $21,000 ÷ $65,000 = 0 .32 $22,000 ÷ $68,000 = 0.32 After correction: […]

Accounting Chapter 7 Income Statement For The Month Ended January

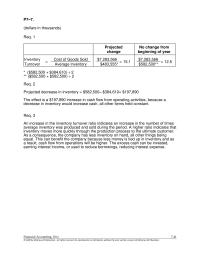

Financial Accounting, 10/e 7-41 P7–7. (dollars in thousands) Req. 1 Projected change No change from beginning of year Inventory = Cost of Goods Sold $7,283,566 = 15.1 $7,283,566 = 12.5 Turnover Average Inventory $483,555* $582,500** * ($582,500 + $384,610) ÷ […]

Accounting Chapter 7 Goods Held Consignment Are Owned The Consignor

Financial Accounting, 10/e 7-21 E7–11. (continued) Req. 3 When prices are falling, the opposite effect occurs–LIFO produces higher net income and less favorable cash flow than does FIFO. Thus LIFO is preferable in terms of net income, and FIFO is […]

Accounting Chapter 7 Beginning Inventory Purchases Goods Available

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 7 Reporting and Interpreting Cost of Goods Sold and Inventory ANSWERS TO QUESTIONS 1. Inventory often is one of […]

Accounting Chapter 7 Calculations of FIFO cost of goods sold will always

Chapter 07 – Reporting and Interpreting Cost of Goods Sold and Inventory 7-13 VI. Chapter Supplement A: LIFO Liquidations A. LIFO Liquidations inventory become part of cost of goods sold 2. LIFO liquidation – a sale of a lower-cost inventory […]

Accounting Chapter 7 The Inventory Record Gives The Amount Both

Chapter 07 – Reporting and Interpreting Cost of Goods Sold and Inventory 7-1 CHAPTER 7 REPORTING AND INTERPRETING COST OF GOODS SOLD AND INVENTORY Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Compre- hensive […]

Accounting Chapter 6 Net Sales Its Computation Gross Profit The

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AP6–2. (Amounts in thousands) Req. 1. Bad debt expense (+E, –SE) …………………………………………….. 6,014 Allowance for doubtful accounts (+XA, –A) ………………… […]

Accounting Chapter 6 Declining sales revenue leads to lower accounts

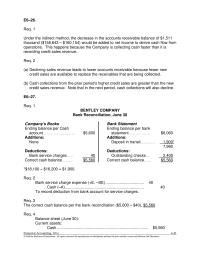

Financial Accounting, 10/e 6-21 E6–26. Req. 1 Under the indirect method, the decrease in the accounts receivable balance of $1,511 thousand ($158,643 – $160,154) would be added to net income to derive cash flow from operations. This happens because the […]

Accounting Chapter 6 A sales discount is a discount given to customers

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 6 Reporting and Interpreting Sales Revenue, Receivables, and Cash ANSWERS TO QUESTIONS 1. The difference between sales revenue and […]

Accounting Chapter 6 The Companys Allowance For Doubtful Accounts Has

Chapter 06 – Reporting and Interpreting Sales Revenue, Receivables, and Cash 6-19 HANDOUT 6 – 1, CONTINUED (4) After many collection attempts, on June 15, Year 2, the company determined that it would not collect $10,000 in accounts receivables from […]

Accounting Chapter 6 The Amounts Bad Debt Expense And Accounts

Chapter 06 – Reporting and Interpreting Sales Revenue, Receivables, and Cash 6-1 CHAPTER 6 REPORTING AND INTERPRETING SALES REVENUE, RECEIVABLES, AND CASH Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects and […]

Accounting Chapter 5 The Balance Sheet lists Property and equipment

CONTINUING PROBLEMS CON5-1. a. Retained earnings (−SE) …………………………………………….. 10,000 Cash (−A) ……………………………………………………………… 10,000 b. Cash (+A) …………………………………………………………………. 2,000 Deferred revenue (+L) …………………………………………….. 2,000 c. Rent expense (+E, −SE) …………………………………………….. 500 Cash (−A) ……………………………………………………………… 500 d. Equipment (+A) …………………………………………………………. 14,000 Note […]

Accounting Chapter 5 It measures the ability to sell goods for

Financial Accounting, 10/e 5-21 P5–3. Req. 1 EXQUISITE JEWELERS Balance Sheet December 31, Current Year Assets Current Assets Cash ………………………………………………………………… $ 58,000 Accounts receivable ……………………………………………. 71,000 Prepaid insurance ………………………………………………. 1,500 Merchandise inventory ………………………………………… 154,000 Total current assets …………………………………….. $284,500 Investment […]

Accounting Chapter 5 Written Public News Announcement That Normally Distributed

Chapter 5 Communicating and Interpreting Accounting Information ANSWERS TO QUESTIONS 1. The primary responsibility for the accuracy of the financial records and conformance with Generally Accepted Accounting Principles (GAAP) in the financial statements rests with management, normally the CEO and […]

Accounting Chapter 5 Accounting Information Handout Classifying Accounts Financial

Chapter 05 – Communicating and Interpreting Accounting Information 5-12 noncash items = cash provided by operating activities G. Notes to Financial Statements 1. Users require additional details to facilitate their analysis a. Accounting rules applied in the company’s statements b. […]

Accounting Chapter 5 Independent Verification Reduces The Risk That The

Chapter 05 – Communicating and Interpreting Accounting Information 5-1 CHAPTER 5 COMMUNICATING AND INTERPRETING ACCOUNTING INFORMATION Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Cases and Projects process (regulators, managers, directors, auditors, information intermediaries, […]

Accounting Chapter 4 This transaction will affect Carey’s financial

CP4–5. (continued) Req. 3 Closing Entry on December 31 of the Current Year: Service revenue (from the adjusted trial balance) (−R) ……… 224,000 Retained earnings (+SE) …………………………………….. 40,480 Expenses (from the adjusted trial balance) (−E) ……… 183,520 Req. 4 Pretax […]

Accounting Chapter 4 Interest Expense The Cost Borrowing Funds For

Financial Accounting, 10/e 4-61 COMP4-2. (continued) Req. 2 a. Cash (+A) …………………………………………………. 20,000 Notes payable (+L) ……………………………. 20,000 b. Equipment (+A) …………………………………………. 18,000 Cash (−A) ………………………………………… 18,000 c. Cash (+A) …………………………………………………. 5,000 Common stock (+SE) ………………………… 1,000 Additional paid-in capital […]

Accounting Chapter 4 Since debits are supposed to equal credits

Financial Accounting, 10/e 4-41 P4–6. (continued) Req. 4 Total asset turnover ratio = Net Sales (or Operating Revenue) Average Total Assets = $66,220 [($110,000 + $136,220)/2] = $66,220 $123,110 = 0.54 (rounded to two decimal places The […]

Accounting Chapter 4 Amount of dividends declared for the period

Financial Accounting, 10/e 4-21 E4–9. Req. 1 a. Accrued revenue b. Deferred expense c. Accrued expense d. Deferred revenue e. Deferred expense f. Deferred expense g. Accrued expense Req. 2 Computations a. Accounts receivable (+A) ………………………….. 3,300 Given Service revenue […]

Accounting Chapter 4 Adjusting entries are made at the end of the accounting

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings ANSWERS TO QUESTIONS 1. Adjusting entries are made at the […]

Accounting Chapter 4 The company borrowed using a note payable from

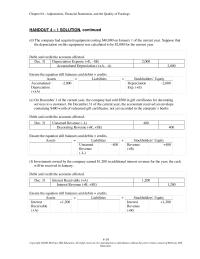

Chapter 04 – Adjustments, Financial Statements, and the Quality of Earnings 4-19 HANDOUT 4 – 1 SOLUTION, continued (d) The company had acquired equipment costing $40,000 on January 1 of the current year. Suppose that the depreciation on this equipment […]

Accounting Chapter 4 New and updated real company information in end

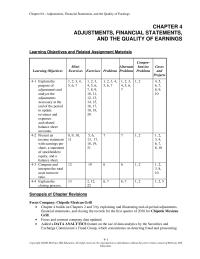

Chapter 04 – Adjustments, Financial Statements, and the Quality of Earnings 4-1 CHAPTER 4 ADJUSTMENTS, FINANCIAL STATEMENTS, AND THE QUALITY OF EARNINGS Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Compre- hensive Problems Cases […]

Accounting Chapter 3 Most retailers settle sales in cash at the register

Financial Accounting, 10/e 3-59 COMP3–1. (continued) Req. 2 Cash Short-Term Investments Accounts Receivable Beg. 0 Beg. 0 Beg. 0 (a) 8,000 2,400 (c) (j) 10,000 (k) 21,000 (b) 20,000 3,040 (d) 10,000 21,000 (k) 21,000 1,000 (f) (o) 25 2,000 […]

Accounting Chapter 3 The net profit margin ratio suggests that the

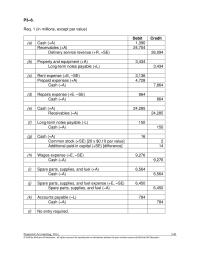

Financial Accounting, 10/e 3-41 P3–6. Req. 1 (in millions, except par value) Debit Credit (a) Cash (+A) 1,390 Receivables (+A) 24,704 Delivery service revenue (+R, +SE) 26,094 (b) Property and equipment (+A) 3,434 Long-term notes payable (+L) 3,434 (c) Rent […]

Accounting Chapter 3 But excludes $910 in salaries incurred by not yet paid

Financial Accounting, 10/e 3-21 E3–11. STACEY’S PIANO REBUILDING COMPANY Income Statement (unadjusted) For the Month Ended January 31 Operating Revenues: Rebuilding fees revenue $ 19,000 Total operating revenues 19,000 Operating Expenses: Wages expense 16,500 Utilities expense 400 Total operating expenses […]

Accounting Chapter 3 Expenses Cost Sales Wages Expense Utilities Expense

© 2020 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 3 Operating Decisions and the Accounting System ANSWERS TO QUESTIONS 1. A typical business operating cycle for a manufacturer […]

Accounting Chapter 3 Ensure the equation still balances and debits

Chapter 03 – Operating Decisions and the Accounting System 3-16 HANDOUT 3 – 1, continued (d) Sell a $1,000 gift certificate. Debit and credit the accounts affected Ensure the equation still balances and debits = credits Assets = Liabilities + […]

Accounting Chapter 3 Revenues Are Recognized When They Are Earned

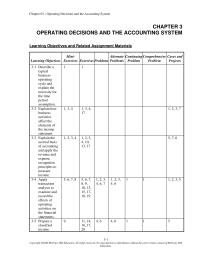

Chapter 03 – Operating Decisions and the Accounting System 3-1 CHAPTER 3 OPERATING DECISIONS AND THE ACCOUNTING SYSTEM Learning Objectives and Related Assignment Materials Learning Objectives Mini- Exercises Exercises Problems Alternate Problems Continuing Problem Comprehensive Problem Cases and Projects operating […]