Financial Accounting, 10/e 7-41

P7–7.

(dollars in thousands)

Req. 1

Projected

change

No change from

beginning of year

Req. 2

Projected decrease in inventory = $582,500– $384,610= $197,890

Req. 3

An increase in the inventory turnover ratio indicates an increase in the number of times

average inventory was produced and sold during the period. A higher ratio indicates that

P7–8.

(dollars in millions)

Req. 1

A change that increases beginning inventory will decrease net income while a change

that increases ending inventory will increase net income.

Impact on International Paper’s Net

Income (in millions)

Change in ending inventory $293

Use of FIFO would result in an increase of $2.1 million in International Paper’s reported

net income. The change would result in an increase in income taxes because the LIFO

Req. 2

If FIFO had been used, the ending inventory would have been $293 million higher.

Instead LIFO was used and the $293 million was allocated to cost of goods sold in earlier

Req. 3

The reduction in taxes (compared to FIFO) was $0.9 million (calculated in Req. 1).

P7–9.

Req. 1

2016 2017 2018 2019

Sales revenue $2,025,000 $2,450,000 $2,700,000 $2,975,000

Cost of goods sold 1,505,000 1,645,000* 1,764,000* 2,113,000

Req. 2

2016 2017 2018 2019

Gross profit ratio (gross profit ÷ sales):

(a) Before correction:

$520,000 ÷ $2,025,000 = 0.26

Req. 3

The effect of the error on income tax expense was:

2017 2018

Income tax expense reported $93,000 $114,000

P7–10. (Supplement A)

(dollars in millions)

Req. 1 Pretax operating profit (loss) for the current year had FIFO accounting been

employed instead of LIFO.

Req. 2 Since prices are rising, LIFO liquidations increase net income before taxes. The

change in pretax operating profit during the current year is given in the footnote

ALTERNATE PROBLEMS

AP7−1.

a) Goods available for sale for all methods:

Unit Total

Units Cost Cost

b) and c)

1. Average cost:

2. First-in, first-out:

Ending inventory (460 units x $37) +

(270 units x $34.25) $26,267.50

3. Last-in, first-out:

Ending inventory (390 units x $32) +

(340 units x $34.25) $24,125

AP7−1. (continued)

4. Specific identification:

Ending inventory (658 units x $34.25) +

(72 units x $37) $25,200.50

Financial Accounting, 10/e 7-47

AP7–2.

Req. 1

NEWRIDGE COMPANY

Partial Income Statement

For the Month Ended January 31, current year

(a) (b) (c) (d)

Average Specific

Cost FIFO LIFO Identification

Computations:

*Sales revenue = 240 units @ $16 = $3,840.

**Cost of Goods Sold Amounts:

a)

Average Cost

Number of Units

x

Unit Cost

=

Total

Cost

120

x

$8

=

$ 960

380

x

=

200

x

=

700

for Sale

$6,580

700 units

Cost of Goods Sold

=

$9.40 x 240 units

=

$2,256

Cost of Goods Sold

Units

Unit

Cost

Total

Cost

b)

FIFO

First Units in (Beginning Inventory)

120

$8

$ 960

Next Units in (January 12)

120

9

1,080

Total Cost of Goods Sold (FIFO)

240

$2,040

c)

LIFO

Last Units in (January 26)

$2,200

Next Units in (January 12)

AP7–2. (continued)

Cost of Goods Sold

Units

Unit

Cost

Total Cost

d)

Specific

First sale

100

$ 8

$ 800

Identification

Second sale

Total Cost of Goods Sold

$2,060

Cost of Ending Inventory Amounts:

a)

Average Cost

Ending Inventory

=

$9.40 x 460 units

=

$4,324

Ending Inventory

Units

Unit

Cost

Total Cost

b)

FIFO

Last Units in (January 26)

200

$11

$2,200

Next Units in (January 12)

260

Total Ending Inventory FIFO

460

c)

LIFO

First Units in (Beginning Inventory)

120

Next Units in (January 12)

340

Total Ending Inventory LIFO

460

Req. 2

FIFO reports a higher pretax income than LIFO because (1) prices are rising and (2) FIFO

allocates the older (lower) unit costs to cost of goods sold. For the same reason, FIFO

will report a higher EPS because it produces a higher pretax income than LIFO.

Ending Inventory

Units

Unit

Cost

Total Cost

d)

Specific

Beginning

20

$ 8

$ 160

Identification

January 12

240

January 26

200

Total Ending Inventory (Spec.)

$4,520

Financial Accounting, 10/e 7-49

AP7–2. (continued)

Req. 3

Because LIFO reports a lower pretax income than FIFO for the reasons given in

Req. 4

LIFO will provide a more favorable cash flow of $156 compared to FIFO because less

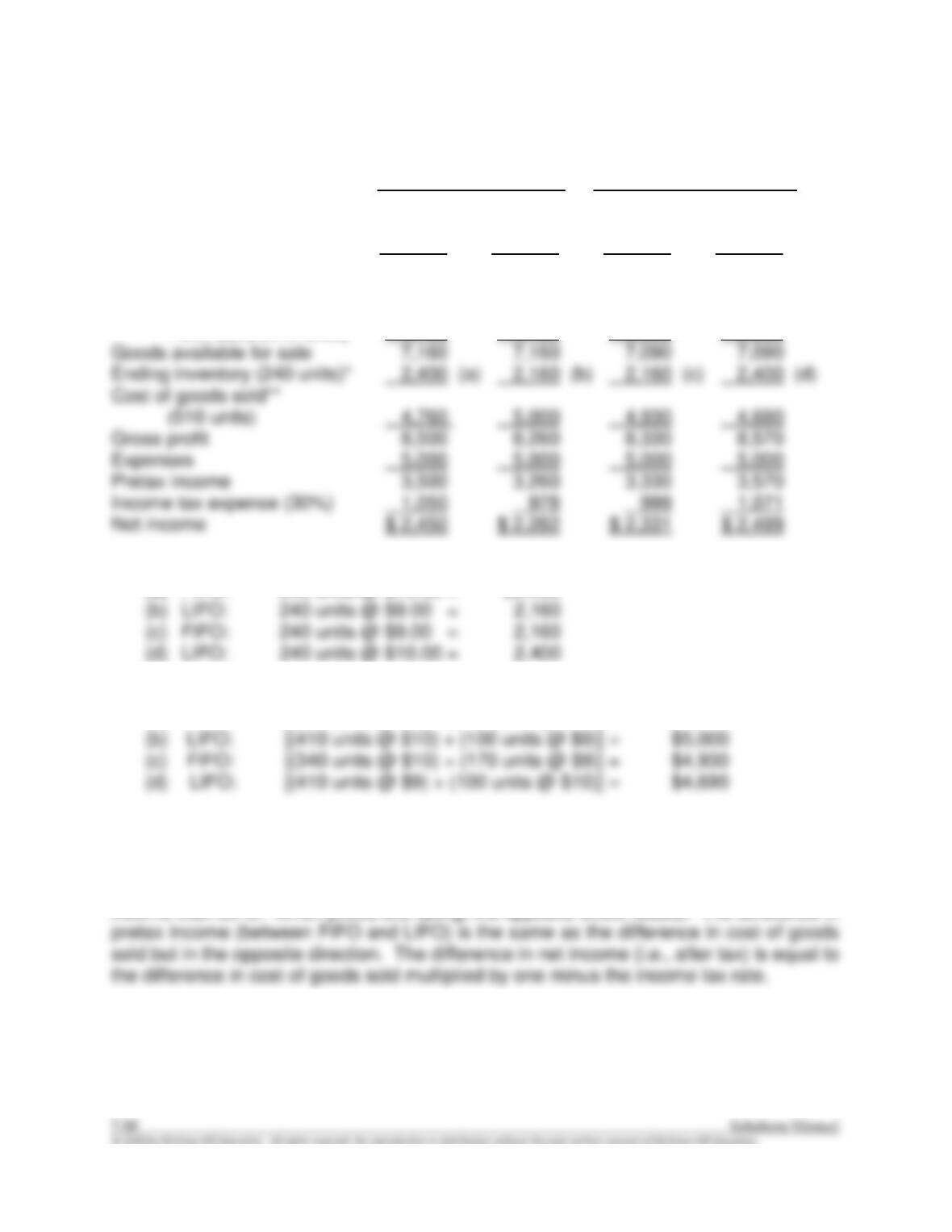

AP7–3.

Req. 1

Prices Rising Prices Falling

A B C D

FIFO LIFO FIFO LIFO

Sales revenue (510 units) $13,260 $13,260 $13,260 $13,260

Cost of goods sold:

Beginning inventory

(340 units) 3,060 3,060 3,400 3,400

Purchases (410 units) 4,100 4,100 3,690 3,690

*Ending inventory computations:

(a) FIFO: 240 units @ $10.00 = $2,400

** Cost of goods sold (direct computations):

(a) FIFO: [(340 units @ $9) + (170 units @ $10)] = $4,760

Req. 2

The above tabulation demonstrates that when prices are rising, FIFO gives a higher net

income than LIFO. When prices are falling, the opposite effect results. The difference in

Financial Accounting, 10/e 7-51

AP7–3. (continued)

Req. 3

When prices are rising, LIFO derives a more favorable cash position (than FIFO) equal

Req. 4

Either method can be defended reasonably. If one focuses on current income and EPS,

FIFO derives a more favorable result (higher than LIFO) when prices are rising.

AP7–4.

Req. 1

COLCA COMPANY

Income Statements Corrected

2016 2017 2018 2019

Sales revenue $60,000 $63,000 $65,000 $68,000