Archives

978-0077861704 Chapter 1 Case Solutions

Case Solutions Fundamentals of Corporate Finance Ross, Westerfield, and Jordan 11th edition Updated: 01/17/2015 Prepared by Brad Jordan University of Kentucky Joe Smolira Belmont University CHAPTER 1 THE McGEE CAKE COMPANY 1. The advantages to an LLC are: (a) Reduction […]

978-0077861704 Chapter 1 Lecture Note Part 1

Chapter 1 INTRODUCTION TO CORPORATE FINANCE CHAPTER WEB SITES Section Web Address 1.1 www.mhhe.com/rwj www.cfo.com 1.2 http://www.incorporate.com www.llc.com 1.3 www.soxlaw.com 1.4 www.business-ethics.com finance.yahoo.com 1.5 www.sec.gov www.nyse.com www.nasdaq.com SUGGESTED VIDEOS The Role of the Chief Financial Officer Financial Markets CHAPTER ORGANIZATION […]

978-0077861704 Chapter 1 Lecture Note Part 2

Chapter 01 – Introduction to Corporate Finance 1.1. The Agency Problem and Control of the Corporation A. Agency Relationships – The relationship between stockholders and management is called the agency relationship. This occurs when one party (principal) hires another (agent) […]

978-0077861704 Chapter 1 Solutions Manual

Solutions Manual Fundamentals of Corporate Finance 11th edition Ross, Westerfield, and Jordan 01-17-2015 Prepared by Brad Jordan University of Kentucky Joe SmoliraBelmont University CHAPTER 1 INTRODUCTION TO CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. Capital budgeting […]

978-0077861704 Chapter 10 Case Solutions

CHAPTER 10 CONCH REPUBLIC ELECTRONICS, PART 1 This is an in-depth capital budgeting problem. The initial cash outlay at Time 0 is the cost of the new equipment, $40,500,000. The sales each year are a combination of the sales of […]

978-0077861704 Chapter 10 Solutions Manual Part 1

CHAPTER 10 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a 2. For tax […]

978-0077861704 Chapter 10 Solutions Manual Part 2

15. To evaluate the project with a $150,000 cost savings, we need the OCF to compute the NPV. Using the tax shield approach, the OCF is: The NPV with a $100,000 cost savings is: OCF = $100,000(1 – .35) + […]

978-0077861704 Chapter 10 Solutions Manual Part 3

31. We will begin by calculating the aftertax salvage value of the equipment at the end of the project’s life. The aftertax salvage value is the market value of the equipment minus any taxes paid (or refunded), so the aftertax […]

978-0077861704 Chapter 11 Case Solutions

CHAPTER 11 CONCH REPUBLIC ELECTRONICS, PART 2 1. Here we want to examine the sensitivity of NPV to changes in the price of the new smart phone. The calculations for sensitivity to changes in price are similar to the original […]

978-0077861704 Chapter 11 Lecture Note

Chapter 11 – Project Analysis and Evaluation Chapter 11 PROJECT ANALYSIS AND EVALUATION CHAPTER ORGANIZATION 11.1 Evaluating NPV Estimates The Basic Problem Projected versus Actual Cash Flows Forecasting Risk Sources of Value 11.2 Scenario and Other What-If Analyses Getting Started […]

978-0077861704 Chapter 11 Solutions Manual Part 2

14. We can use the equation for DOL to calculate fixed costs. The fixed costs must be: DOL = 3.42 = 1 + FC / OCF If the output rises to 18,500 units, the percentage change in quantity sold is: […]

978-0077861704 Chapter 11 Solutions Manual Part 3

22. To calculate the sensitivity of the NPV to changes in the price of the new club, we simply need to We will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and […]

978-0077861704 Chapter 12 Case Solutions

CHAPTER 12 A JOB AT S&S AIR 1. The biggest advantage the mutual funds have is instant diversification. The mutual funds have a 2. Both the APR and EAR are infinite. The match is instantaneous, so the number of periods […]

978-0077861704 Chapter 12 Lecture Note

Chapter 12 – Some Lessons from Capital Market History Chapter 12 SOME LESSONS FROM CAPITAL MARKET HISTORY CHAPTER WEB SITES Section Web Address Introduction www.mhhe.com/rwj 12.1 finance.yahoo.com www.marketwatch.com 12.2 www.globalfinancialdata.com bigcharts.marketwatch.com 12.4 www.robertniles.com www.morningstar.com 12.6 www.investorhome.com CHAPTER ORGANIZATION 12.1 Returns […]

978-0077861704 Chapter 12 Solutions Manual Part 1

CHAPTER 12 SOME LESSONS FROM CAPITAL MARKET HISTORY Answers to Concepts Review and Critical Thinking Questions 1. They all wish they had! Since they didn’t, it must have been the case that the stellar performance was 2. As in the […]

978-0077861704 Chapter 13 Case Solutions

CHAPTER 13 THE BETA FOR COLGATE-PALMOLIVE NOTE: The example below shows the results from late 2013. The actual answer to the case will change based on current market conditions 1. The information used for the analysis is presented below. Note […]

978-0077861704 Chapter 13 Lecture Note Part 1

Chapter 13 – Return, Risk, and the Security Market Line Chapter 13 RETURN, RISK, AND THE SECURITY MARKET LINE CHAPTER WEB SITES Section Web Address 13.2 www.thestreet.com 13.5 www.investopedia.com/university 13.6 www.investools.com moneycentral.msn.com finance.yahoo.com money.cnn.com CHAPTER ORGANIZATION 13.1 Expected Returns and […]

978-0077861704 Chapter 13 Lecture Note Part 2

Chapter 13 – Return, Risk, and the Security Market Line 1. Systematic Risk and Beta A. The Systematic Risk Principle The principle – The reward for bearing risk depends only on the systematic risk of the investment. The implication – […]

978-0077861704 Chapter 13 Solutions Manual Part 2

24. We know the total portfolio value and the investment of two stocks in the portfolio, so we can find the weight of these two stocks. The weights of Stock A and Stock B are: Since the portfolio is as […]

978-0077861704 Chapter 14 Case Solutions

CHAPTER 14 COST OF CAPITAL FOR SWAN MOTORS NOTE: The example below shows the results during April 2014. The actual answer to the case will change based on current market conditions. 1. The book value of the company’s liabilities and […]

978-0077861704 Chapter 14 Lecture Note Part 1

Chapter 14 – Cost of Capital Chapter 14 COST OF CAPITAL CHAPTER WEB SITES Section Web Address 14.2 www.zacks.com www.bloomberg.com 14.4 www.ibbotson.com www.valuepro.net www.sternstewart.com CHAPTER ORGANIZATION 14.1 The Cost of Capital: Some Preliminaries Required Return versus Cost of Capital Financial […]

978-0077861704 Chapter 14 Lecture Note Part 2

Chapter 14 – Cost of Capital Video Note: “Economic Value Added (EVA)” can be used to reinforce the concepts. 1. Divisional and Project Costs of Capital A. The SML and the WACC The WACC is the appropriate discount rate only […]

978-0077861704 Chapter 14 Solutions Manual Part 1

CHAPTER 14 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this, value is created. 5. […]

978-0077861704 Chapter 14 Solutions Manual Part 2

22. To find the aftertax cost of debt for the company, we need to find the weighted average of the four debt issues. We will begin by calculating the market value of each debt issue, which is: So, the total […]

978-0077861704 Chapter 15 Case Solutions

CHAPTER 15 S&S AIR GOES PUBLIC 1. The main difference in the costs is the reduced possibility of underpricing in a Dutch auction. As to which is better, we don’t actually know. In theory, the Dutch auction should be better […]

978-0077861704 Chapter 15 Lecture Note Part 2

Chapter 15 – Raising Capital 1. IPOs and Underpricing A. Underpricing: The 1999 – 2000 Experience The number of IPOs and the average return on IPOs during 1999 and 2000 was enormous compared to past periods. 1999 set a record […]

978-0077861704 Chapter 15 Solutions Manual Part 1

CHAPTER 15 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company’s internally generated cash flow provides a source of equity financing. For a profitable company, outside equity may never be needed. Debt issues are larger because […]

978-0077861704 Chapter 16 Case Solutions

CHAPTER 16 STEPHENSON REAL ESTATE RECAPITALIZATION 1. If Stephenson wishes to maximize the overall value of the firm, it should use debt to finance the $95 2. Since Stephenson is an all-equity firm with 9 million shares of common stock […]

978-0077861704 Chapter 16 Solutions Manual Part 1

CHAPTER 16 FINANCIAL LEVERAGE AND CAPITAL STRUCTURE POLICY Answers to Concepts Review and Critical Thinking Questions 1. Business risk is the equity risk arising from the nature of the firm’s operating activity and is directly related to the systematic risk […]

978-0077861704 Chapter 16 Solutions Manual Part 2

10. With no taxes, the value of an unlevered firm is the EBIT divided by the unlevered cost of equity, so: V = EBIT / WACC 11. If there are corporate taxes, the value of an unlevered firm is: VU […]

978-0077861704 Chapter 17 Case Solutions

CHAPTER 17 ELECTRONIC TIMING, INC. 1. The value of the company will decline by the amount of the dividend. Ignoring taxes, shareholders 2. The value of the company could increase or decrease. If the company is over-levered, paying off debt […]

978-0077861704 Chapter 17 Lecture Note Part 1

Chapter 17 – Dividends and Dividend Policy Chapter 17 DIVIDENDS AND DIVIDEND POLICY CHAPTER WEB SITES Section Web Address 17.1 www.reuters.com/finance/EarningsUS 17.2 www.fool.com 17.8 www.stocksplits.net CHAPTER ORGANIZATION 17.1 Cash Dividends and Dividend Payment Cash Dividends Standard Method of Cash Dividend […]

978-0077861704 Chapter 17 Lecture Note Part 2

Chapter 17 – Dividends and Dividend Policy 1. Stock Repurchase: An Alternative to Cash Dividends A. Cash Dividends versus Repurchase A firm may choose to buy back outstanding shares instead of paying a cash dividend (or instead of increasing a […]

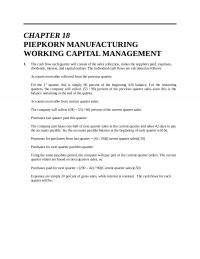

978-0077861704 Chapter 18 Case Solutions

CHAPTER 18 PIEPKORN MANUFACTURING WORKING CAPITAL MANAGEMENT 1. The cash flow each quarter will consist of the sales collection, minus the suppliers paid, expenses, For the 1st quarter, this is simply 80 percent of the beginning A/R balance. For the […]

978-0077861704 Chapter 18 Lecture Note Part 1

Chapter 18 – Short-Term Finance and Planning Chapter 18 SHORT-TERM FINANCE AND PLANNING CHAPTER WEB SITES Section Web Address 18.1 www.treasury-management.com 18.4 www.toolkit.com 18.5 www.receivablesxchange.com CHAPTER ORGANIZATION 18.1 Tracing Cash and Net Working Capital 18.2 The Operating Cycle and the […]

978-0077861704 Chapter 18 Lecture Note Part 2

Chapter 18 – Short-Term Finance and Planning 18.3 Some Aspects of Short-Term Financial Policy A. The Size of the Firm’s Investment in Current Assets If cash was collected from sales when the bills had to be paid, then cash balances […]

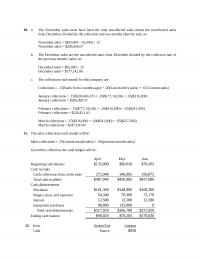

978-0077861704 Chapter 18 Solutions Manual Part 2

10. a. The November sales must have been the total uncollected sales minus the uncollected sales from December, divided by the collection rate two months after the sale, so: b. The December sales are the uncollected sales from December divided […]

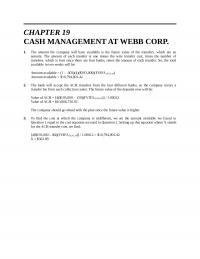

978-0077861704 Chapter 19 Case Solutions

CHAPTER 19 CASH MANAGEMENT AT WEBB CORP. 1. The amount the company will have available is the future value of the transfers, which are an annuity. The amount of each transfer is one minus the wire transfer cost, times the […]

978-0077861704 Chapter 19 Lecture Note Part 1

Chapter 19 – Cash and Liquidity Management Chapter 19 CASH AND LIQUIDITY MANAGEMENT CHAPTER WEB SITES Section Web Address 19.2 www.carreker.fiserv.com 19.3 www.gtnews.com 19.5 www.bloomberg.com CHAPTER ORGANIZATION 19.1 Reasons for Holding Cash The Speculative and Precautionary Motives The Transaction Motive […]

978-0077861704 Chapter 19 Lecture Note Part 2

Chapter 19 – Cash and Liquidity Management 1. Managing Cash Disbursements A. Increasing Disbursement Float Slowing payments by increasing mail delay, processing time, or collection time. May not want to do this from both an ethical standpoint and a valuation […]

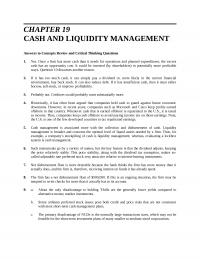

978-0077861704 Chapter 19 Solutions Manual Part 1

CHAPTER 19 CASH AND LIQUIDITY MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. Yes. Once a firm has more cash than it needs for operations and planned expenditures, the excess 2. If it has too much cash, it […]

978-0077861704 Chapter 2 Case Solutions

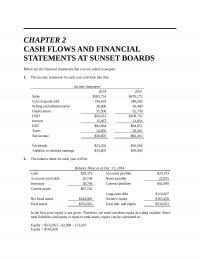

CHAPTER 2 CASH FLOWS AND FINANCIAL STATEMENTS AT SUNSET BOARDS Below are the financial statements that you are asked to prepare. 1. The income statement for each year will look like this: Income Statement 2014 2015 Sales $385,724 $470,172 Cost […]

978-0077861704 Chapter 2 Lecture Note

Chapter 02 – Financial Statements, Taxes, and Cash Flow Chapter 2 FINANCIAL STATEMENTS, TAXES, AND CASH FLOW CHAPTER WEB SITES Section Web Address 2.1 finance.yahoo.com money.cnn.com finance.google.com disney.go.com www.sec.gov www.fasb.org 2.3 www.irs.gov CHAPTER ORGANIZATION 2.1 The Balance Sheet Assets: The […]

978-0077861704 Chapter 20 Case Solutions

CHAPTER 20 CREDIT POLICY AT HOWLETT INDUSTRIES To decide on the optimal credit policy, we need to calculate the NPV of each policy. We will begin with the calculation of the NPV of the current policy. Current Policy First, we […]

978-0077861704 Chapter 20 Lecture Note Part 1

Chapter 20 – Credit and Inventory Management Chapter 20 CREDIT AND INVENTORY MANAGEMENT CHAPTER WEB SITES Section Web Address 20.1 www.treasury.pncbank.com www.treasurystrat.com www.insidearm.com 20.2 www.nacm.org 20.4 www.creditworthy.com 20.5 www.dnb.com 20.7 www.simba.org CHAPTER ORGANIZATION 20.1 Credit and Receivables Components of Credit […]

978-0077861704 Chapter 20 Lecture Note Part 2

Chapter 20 – Credit and Inventory Management 1. Collection Policy A. Monitoring receivables Keeping track of payments to try to spot potential problems (chronic late-payers and possible defaults) to reduce losses. Aging schedule – a break-down of receivables accounts by […]

978-0077861704 Chapter 20 Solutions Manual Part 1

CHAPTER 20 CREDIT AND INVENTORY MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. a. A sight draft is a commercial draft that is payable immediately. b. A time draft is a commercial draft that does not require immediate […]

978-0077861704 Chapter 20 Solutions Manual Part 2

15. The cash flow from the old policy is: And the cash flow from the new policy will be: Cash flow from new policy = ($127 – 98)(1,350) Cash flow from new policy = $39,150 The incremental cash flow, which […]

978-0077861704 Chapter 21 Case Solutions

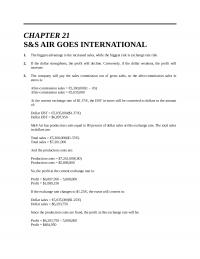

CHAPTER 21 S&S AIR GOES INTERNATIONAL 3. The company will pay the sales commission out of gross sales, so the after-commission sales in euros is: After-commission sales = €5,300,000(1 – .05) After-commission sales = €5,035,000 At the current exchange rate […]

978-0077861704 Chapter 21 Lecture Note

Chapter 21 – International Corporate Finance Chapter 21 INTERNATIONAL CORPORATE FINANCE CHAPTER WEB SITES Section Web Address 21.1 www.adr.com www.bloomberg.com 21.2 www.swift.com www.xe.com www.exchangerate.com www.ft.com 21.4 www.travlang.com/money www.marketwatch.com 21.7 https://www.cia.gov/library/publications/the- world-factbook/index.html CHAPTER ORGANIZATION 21.1 Terminology 21.2 Foreign Exchange Markets and […]

978-0077861704 Chapter 21 Solutions Manual Part 1

CHAPTER 21 INTERNATIONAL CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. a. The dollar is selling at a premium because it is more expensive in the forward market than in b. The franc is expected to depreciate […]

978-0077861704 Chapter 22 Case Solutions

CHAPTER 22 YOUR 401(k) ACCOUNT AT S&S AIR 1. Before the fact, you would expect that mutual funds managers would be able to outperform the market. This is due, in part, to the Darwinian nature of the business. Good performing […]

978-0077861704 Chapter 22 Lecture Note

Chapter 22 – Behavioral Finance: Implications for Financial Management Chapter 22 BEHAVIORAL FINANCE: IMPLICATIONS FOR FINANCIAL MANAGEMENT CHAPTER WEB SITES Section Web Address 22.4 www.behavioralfinance.net 22.5 www.zakon.org/robert/internet/timeline CHAPTER ORGANIZATION 22.1 Introduction to Behavioral Finance 22.2 Biases Overconfidence Overoptimism Confirmation Bias […]

978-0077861704 Chapter 22 Solutions Manual Part 1

CHAPTER 22 BEHAVIORAL FINANCE: IMPLICATIONS FOR FINANCIAL MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. The least likely limit to arbitrage is firm-specific risk. For example, in the 3Com/Palm case, the 2. Overconfidence is the belief that one’s […]

978-0077861704 Chapter 23 Lecture Note

Chapter 23 – Enterprise Risk Management Chapter 23 Enterprise Risk Management CHAPTER WEB SITES Section Web Address Introduction www.numa.com 23.4 www.cbot.com www.cme.com www.theice.com www.biz.uiowa.edu/iem www.cftc.gov 23.5 www.isda.org 23.6 www.cboe.com www.optionseducation.com www.margrabe.com www.treasurers.org CHAPTER ORGANIZATION 23.1 Insurance 23.2 Managing Financial Risk […]

978-0077861704 Chapter 24 Case Solutions

CHAPTER 24 S&S AIR’S CONVERTIBLE BOND 1. We can use the PE ratio to calculate the current stock price. Doing so, we get: PE = Price / EPS This means the conversion premium of the bond is: Conversion premium = […]

978-0077861704 Chapter 24 Lecture Note Part 1

Chapter 24 – Options and Corporate Finance Chapter 24 OPTIONS AND CORPORATE FINANCE CHAPTER WEB SITES Section Web Address 24.1 www.cboe.com www.cmegroup.com www.euronext.com finance.yahoo.com 24.2 www.financial-guide.ch/ica/derivatives 24.4 www.esopassociation.org www.nceo.org CHAPTER ORGANIZATION 24.1 Options: The Basics Puts and Calls Stock Options […]

978-0077861704 Chapter 24 Lecture Note Part 2

Chapter 24 – Options and Corporate Finance 1. Valuing a Call Option A. A Simple Model: Part II The option may, however, finish out-of-the money. So, adjust your second portfolio as follows: instead of loaning the PV(E), loan the PV(lowest […]

978-0077861704 Chapter 24 Solutions Manual Part 1

CHAPTER 24 OPTIONS AND CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put […]

978-0077861704 Chapter 24 Solutions Manual Part 2

17. a. The value of the call is the maximum of the stock price minus the present value of the exercise price, or zero, so: The option isn’t worth anything. b. The stock price is too low for the option […]

978-0077861704 Chapter 25 Case Solutions

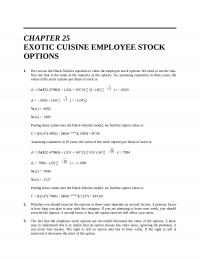

CHAPTER 25 EXOTIC CUISINE EMPLOYEE STOCK OPTIONS 1. We can use the Black-Scholes equation to value the employee stock options. We need to use the risk- free rate that is the same as the maturity as the options. So, assuming […]

978-0077861704 Chapter 25 Lecture Note

Chapter 25 – Option Valuation CHAPTER 25 OPTION VALUATION CHAPTER WEB SITES Section Web Address 25.1 http://www.optionseducation.org/ 25.2 www.numa.com 25.3 www.ivolatility.com www.margrabe.com/optionpricing.html 25.4 finance.yahoo.com CHAPTER ORGANIZATION 25.1 Put-Call Parity Protective Puts An Alternative Strategy The Result Continuous Compounding: A Refresher […]

978-0077861704 Chapter 25 Solutions Manual Part 2

19. a. The combined value of equity and debt of the two firms is: Equity = $4,222.99 + 6,726.34 b. For the new firm, the combined market value of assets is $47,400, and the combined face value of debt is […]

978-0077861704 Chapter 26 Case Solutions

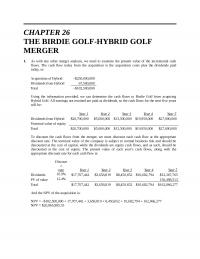

CHAPTER 26 THE BIRDIE GOLF-HYBRID GOLF MERGER 1. As with any other merger analysis, we need to examine the present value of the incremental cash flows. The cash flow today from the acquisition is the acquisition costs plus the dividends […]

978-0077861704 Chapter 26 Lecture Note

Chapter 26 – Mergers and Acquisitions CHAPTER 26 MERGERS AND ACQUISITIONS CHAPTER WEB SITES Section Web Address 26.1 www.marketwatch.com www.firstlist.com www.mergernetwork.com 26.4 www.thedeal.com CHAPTER ORGANIZATION 26.1 The Legal Forms of Acquisitions Merger or Consolidation Acquisition of Stock Acquisition of Assets […]

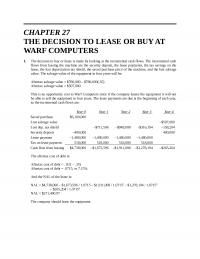

978-0077861704 Chapter 27 Case Solutions

CHAPTER 27 THE DECISION TO LEASE OR BUY AT WARF COMPUTERS 1. The decision to buy or lease is made by looking at the incremental cash flows. The incremental cash Aftertax salvage value = $780,000 – $780,000(.35) Aftertax salvage value […]

978-0077861704 Chapter 27 Lecture Note

Chapter 27 – Leasing CHAPTER 27 LEASING CHAPTER WEB SITES Section Web Address Introduction www.monitordaily.com 27.1 www.bloomberg.com www.keystoneleasing.com 27.5 www.lease-vs-buy.com www.cars.com 27.7 www.ilfc.com CHAPTER ORGANIZATION 27.1 Leases and Lease Types Leasing versus Buying Operating Leases Financial Leases 27.2 Accounting and […]

978-0077861704 Chapter 27 Solutions Manual Part 1

CHAPTER 27 LEASING Answers to Concepts Review and Critical Thinking Questions 1. Some key differences are: (a) Lease payments are fully tax-deductible, but only the interest portion 2. The less profitable one because leasing provides, among other things, a mechanism […]

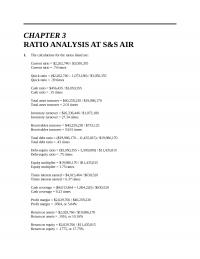

978-0077861704 Chapter 3 Case Solutions

CHAPTER 3 RATIO ANALYSIS AT S&S AIR 1. The calculations for the ratios listed are: Quick ratio = ($2,262,740 – 1,073,180) / $3,050,355 Quick ratio = .39 times Cash ratio = $456,435 / $3,050,355 Cash ratio = .15 times Total […]

978-0077861704 Chapter 3 Lecture Note

Chapter 03 – Working with Financial Statements Chapter 3 WORKING WITH FINANCIAL STATEMENTS CHAPTER WEB SITES Section Web Address 3.1 www.financials.com finance.yahoo.com finance.google.com money.msn.com 3.3 www.reuters.com www.onlinewbc.gov www.chalfin.com 3.5 www.naics.com investing.businessweek.com CHAPTER ORGANIZATION 3.1 Cash Flow and Financial Statements: A […]

978-0077861704 Chapter 3 Solutions Manual Part 2

17. a. Current ratio = Current assets / Current liabilities b. Quick ratio = (Current assets – Inventory) / Current liabilities Quick ratio 2014 = ($90,717 – 51,163) / $62,939 = .63 times Quick ratio 2015 = ($100,617 – 56,295) […]

978-0077861704 Chapter 4 Case Solutions

CHAPTER 4 PLANNING FOR GROWTH AT S&S AIR 1. To calculate the internal growth rate, we first need to find the ROA and the retention ratio, so: ROA = NI / TA b = Addition to RE / NI b […]

978-0077861704 Chapter 4 Lecture Note

Chapter 04 – Long-Term Financial Planning and Growth CHAPTER 4 LONG-TERM FINANCIAL PLANNING AND GROWTH CHAPTER WEB SITES Section Web Address 4.1 www.reuters.com finance.yahoo.com 4.2 www.jaxworks.com www.planware.org CHAPTER ORGANIZATION 4.1 What Is Financial Planning? Growth as a Financial Management Goal […]

978-0077861704 Chapter 4 Solutions Manual Part 2

14. We first must calculate the ROE to calculate the sustainable growth rate. To do this we must realize two other relationships. The total asset turnover is the inverse of the capital intensity ratio, and the equity multiplier is 1 […]

978-0077861704 Chapter 4 Solutions Manual Part 3

27. The pro forma income statements for all three growth rates will be: FLEURY INC. Pro Forma Income Statement 15 % Sales Growth 20% Sales Growth 25% Sales Growth Sales $1,025,340 $1,069,920 $1,114,500 Costs 797,640 832,320 867,000 Dividends $41,468 $43,396 […]

978-0077861704 Chapter 5 Lecture Note

Chapter 05 – Introduction to Valuation: The Time Value of Money Chapter 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY CHAPTER WEB SITES Section Web Address 5.1 www.financeprofessor.com www.teachmefinance.com 5.3 www.calculator.org www.moneychimp.com www.about.com/ www.studyfinance.com www.investopedia.com CHAPTER ORGANIZATION 5.1 Future […]

978-0077861704 Chapter 5 Solutions Manual Part 2

16. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 […]

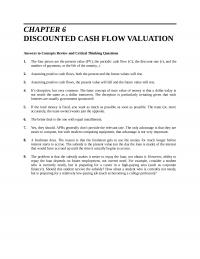

978-0077861704 Chapter 6 Case Solutions

CHAPTER 6 THE MBA DECISION 1. Age is obviously an important factor. The younger an individual is, the more time there is for the 2. Perhaps the most important nonquantifiable factors would be whether or not he is married and […]

978-0077861704 Chapter 6 Lecture Note

Chapter 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY CHAPTER WEB SITES Section Web Address 5.1 www.financeprofessor.com www.teachmefinance.com 5.3 www.calculator.org www.moneychimp.com www.about.com/ www.studyfinance.com www.investopedia.com CHAPTER ORGANIZATION 5.1 Future Value and Compounding Investing for a Single Period Investing for More […]

978-0077861704 Chapter 6 Solutions Manual Part 1

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and the 4. It’s deceptive, but very common. […]

978-0077861704 Chapter 6 Solutions Manual Part 2

23. The time line is: 0 1 ∞ $215,00 0 0 0 0 0 0 0 0 0 Here we need to find the interest rate that equates the perpetuity cash flows with the PV of the cash flows. Using […]

978-0077861704 Chapter 6 Solutions Manual Part 3

47. The time line is: 0 123456 …20 PV $3,50 0 $3,50 0 $3,50 0 $3,50 0 We want to find the value of the cash flows today, so we will find the PV of the annuity, and then bring […]

978-0077861704 Chapter 6 Solutions Manual Part 4

63. This is the same question as before, with different values. So: The time line is: 0 1 –$9,700 $11,20 0 $11,200 = $9,700(1 + r) r = ($11,200 / $9,700) – 1 = .1546, or 15.46% The effective rate […]

978-0077861704 Chapter 6 Solutions Manual Part 5

77. a. The APR is the interest rate per week times 52 weeks in a year, so: b. In a discount loan, the amount you receive is lowered by the discount, and you repay the full principal. With a discount […]

978-0077861704 Chapter 6 Solutions Manual Part 6

44. CFo$1,000,000 C01 $1,450,000 F01 1 C02 $1,900,000 F02 1 I = 7% NPV CPT $23,656,191.50 45. Enter 360 .80($2,700,000) $13,400 N I/Y PV PMT FV Solve for .527% APR = .527% 12 = 6.32% Enter 6.32% 12 NOM […]

978-0077861704 Chapter 7 Lecture Note Part 1

Chapter 07 – Interest Rates and Bond Valuation Chapter 7 INTEREST RATES AND BOND VALUATION CHAPTER WEB SITES Section Web Address 7.1 bonds.yahoo.com personal.fidelity.com money.cnn.com/markets/bondcenter www.bankrate.com investorguide.com 7.2 www.investinginbonds.com www.finra.org/marketdata www.sifma.org www.sec.gov 7.3 www.standardandpoors.com www.moodys.com www.fitchinv.com www.publicdebt.treas.gov www.brillig.com/debt_clock www.ny.frb.org 7.4 […]

978-0077861704 Chapter 7 Lecture Note Part 2

Chapter 07 – Interest Rates and Bond Valuation 1. Bond Ratings Lecture Tip: The question sometimes arises as to why a potential issuer would be willing to pay rating agencies tens of thousands of dollars in order to receive a […]

978-0077861704 Chapter 7 Solutions Manual Part 1

CHAPTER 7 INTEREST RATES AND BOND VALUATION Answers to Concepts Review and Critical Thinking Questions 3. No. If the bid price were higher than the ask price, the implication would be that a dealer was willing to sell a bond […]

978-0077861704 Chapter 7 Solutions Manual Part 2

21. The current yield is: Current yield = Annual coupon payment / Price The bond price equation for this bond is: P0 = $1,068 = $32(PVIFAR%,36) + $1,000(PVIFR%,36) Using a spreadsheet, financial calculator, or trial and error we find: R […]

978-0077861704 Chapter 7 Solutions Manual Part 3

38. To answer this question, we need to find the monthly interest rate, which is the APR divided by 12. We also must be careful to use the real interest rate. The Fisher equation uses the effective annual rate, so, […]

978-0077861704 Chapter 8 Case Solutions

CHAPTER 8 STOCK VALUATION AT RAGAN, INC. 1. The total dividends paid by the company were $90,000. Since there are 100,000 shares outstanding, the total earnings for the company were: This means the payout ratio was: Payout ratio = $90,000 […]

978-0077861704 Chapter 8 Lecture Note

Chapter 08 – Stock Valuation Chapter 8 STOCK VALUATION CHAPTER WEB SITES Section Web Address 8.3 www.bloomberg.com www.nyse.com www.nasdaq.com finance.yahoo.com www.otcbb.com www.pinksheets.com CHAPTER ORGANIZATION 8.1 Common Stock Valuation Cash Flows Some Special Cases Components of the Required Return Stock Valuation […]

978-0077861704 Chapter 8 Solutions Manual Part 1

CHAPTER 8 STOCK VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will 2. Investors believe the company will eventually start paying […]

978-0077861704 Chapter 8 Solutions Manual Part 2

24. We can use the two-stage dividend growth model for this problem, which is: P0 = [D0(1 + g1)/(R – g1)]{1 – [(1 + g1)/(1 + R)]t}+ [(1 + g1)/(1 + R)]t[D0(1 + g2)/(R – g2)] 25. We can use […]

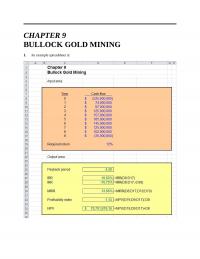

978-0077861704 Chapter 9 Case Solutions

CHAPTER 9 BULLOCK GOLD MINING 1. An example spreadsheet is: Note, there is no Excel function to directly calculate the payback period. We used “If” statements in our spreadsheet. The IF statement we used is: =IF(-D8>(D9+D10+D11+D12+D13+D14),”Greater than 6 years”,IF(- 2. […]

978-0077861704 Chapter 9 Lecture Note

Chapter 09 – Net Present Value and Other Investment Criteria Chapter 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA CHAPTER ORGANIZATION 9.1 Net Present Value The Basic Idea Estimating Net Present Value 9.2 The Payback Rule Defining the Rule Analyzing […]

978-0077861704 Chapter 9 Solutions Manual Part 2

12. a. The IRR is the interest rate that makes the NPV of the project equal to zero. The equation for the IRR of Project A is: Using a spreadsheet, financial calculator, or trial and error to find the root […]

978-0077861704 Chapter 9 Solutions Manual Part 3

Calculator Solutions 7. CFo–$26,000 C01 $11,000 F01 1 8. CFo–$26,000 CFo–$26,000 C01 $11,000 C01 $11,000 F01 1F01 1 C02 $14,000 C02 $14,000 F02 1F02 1 C03 $10,000 C03 $10,000 F03 1F03 1 I = 11% I = 25% NPV CPT […]

FC 13893

What is the amount of the cash flow from investment activity for 2012? A. $18,100 B. $24,800 C. $29,300 D. $32,000 E. $39,400 Answer: Recently, you discovered a putable income bond that is convertible. If you purchase this bond, you […]

FC 17735

Which of the following apply to a partnership that consists solely of general partners? I. double taxation of partnership profits II. limited partnership life III. active involvement in the firm by all the partners IV. unlimited personal liability for all […]

FC 22632

There are two distinct discount rates at which a particular project will have a zero net present value. In this situation, the project is said to: A. have two net present value profiles. B. have operational ambiguity. C. create a […]

FC 29595

Kaylor Equipment Rental paid $75 in dividends and $511 in interest expense. The addition to retained earnings is $418 and net new equity is $500. The tax rate is 35 percent. Sales are $15,900 and depreciation is $680. What are […]

FC 31472

An investment project provides cash flows of $1,190 per year for 10 years. If the initial cost is $8,000, what is the payback period? A. 3.36 years B. 5.28 years C. 6.72 years D. 8.13 years E. never Answer: Which […]

FC 36942

Under credit terms of 1/5, net 15, customers should: A. always pay on the 15th day. B. take the 5 percent discount and pay immediately. C. take the discount and pay on the day following the day of sale. D. […]

FC 48255

You’re trying to determine whether to expand your business by building a new manufacturing plant. The plant has an installation cost of $12 million, which will be depreciated straight-line to zero over its 4-year life. The plant has projected net […]

FC 79078

A trader has just agreed to exchange $2 million U.S. dollars for $1.55 million Euros six months from today. This exchange is an example of a: A. spot trade. B. forward trade. C. currency swap. D. floating swap. E. triangle […]

FC 79650

The Miller-Orr model: A. recommends selling securities in an amount equal to (U* – C) when the cash balance reaches L. B. requires that marketable securities be sold whenever the cash balance falls below the target level. C. bases the […]

FE 33931

Which one of the following names matches the country where the bond is issued? A. Empire: United Kingdom B. Western: United States C. Samurai: China D. Bulldog: France E. Rembrandt: Netherlands Answer: Miller Mfg. is analyzing a proposed project. The […]

FE 57348

The explicit costs, such as legal and administrative expenses, associated with corporate default are classified as _____ costs. A. flotation B. issue C. direct bankruptcy D. indirect bankruptcy E. unlevered Answer: A business firm ceases to exist as a going […]

FE 70950

All else equal, the market value of a stock will tend to decrease by roughly the aftertax value of the dividend on the: A. dividend declaration date. B. ex-dividend date. C. date of record. D. date of payment. E. day […]

FE 97384

Which one of the following is an unintended result of the Sarbanes-Oxley Act? A. more detailed and accurate financial reporting B. increased management awareness of internal controls C. corporations delisting from major exchanges D. increased responsibility for corporate officers E. […]

Fin 11039

The Motor Plant wants to raise $21.4 million through a rights offering so it can modernize its facilities. The subscription price for the offering is set at $11 a share. Currently, the company has 2.6 million shares of stock outstanding […]

FIN 18492

Which one of the following is an advantage of the average accounting return method of analysis? A. easy availability of information needed for the computation B. inclusion of time value of money considerations C. the use of a cutoff rate […]

FIN 19345

The Wire House purchases its inventory one quarter prior to the quarter of sale. The purchase price is 55 percent of the sales price. The accounts payable period is 45 days. The accounts payable balance at the beginning of quarter […]

Fin 23108

The common stock of Westover Foods is currently priced at $28.80 a share. One year from now, the stock price is expected to be either $25 or $30 a share. The risk-free rate of return is 4.2 percent. What is […]

Fin 37531

The bid price is: A. an aftertax price. B. the aftertax contribution margin. C. the highest price you should charge if you want the project. D. the only price you can bid if the project is to be profitable. E. […]

FIN 40061

Which of the following are benefits derived from short-term financial planning? I. having advance notice of when your firm will require external financing II. being able to determine the extent of time for which a loan is required III. having […]

Fin 41742

Which one of the following is the electronic system used by the NYSE for directly transmitting orders to specialists? A. OTCDOT B. SuperDOT C. Instinet D. Internet E. Floornet Answer: Which one of the following statements related to corporate dividends […]

Fin 44683

In the spot market, $1 is currently equal to £0.6211. Assume the expected inflation rate in the U.K. is 2.6 percent while it is 4.3 percent in the U.S. What is the expected exchange rate four years from now if […]

FIN 46568

Which one of the following methods determines the amount of the change a proposed project will have on the value of a firm? A. net present value B. discounted payback C. internal rate of return D. profitability index E. payback […]

Fin 48341

What is the operating cash flow for 2011? A. $1,226 B. $1,367 C. $1,644 D. $1,766 E. $1,823 Answer: Which of the following help convince managers to work in the best interest of the stockholders? Assume there are no golden […]

Fin 49997

Which one of the following is a use of cash? A. increase in notes payable B. decrease in inventory C. increase in long-term debt D. decrease in accounts receivables E. decrease in common stock Answer: The internal rate of return […]

FIN 52365

Lucinda owns a convertible bond that matures in six years. The bond has a 9 percent coupon and pays interest annually. The face value of the bond is $1,000 and the conversion price is $22. Similar bonds have a market […]

FIN 55008

The LIBOR is primarily used as the basis for the rate charged on: A. short-term debt in the Lisbon market. B. mortgage loans in the Lisbon market. C. Eurodollar loans in the London market. D. U.S. federal funds. E. interbank […]

Fin 74182

Anytime Ted analyzes a proposed project, he always assigns a much higher probability of success to the project than is warranted by the information he has gathered. Ted suffers from which one of the following? A. frame dependence B. overconfidence […]

Fin 75374

The change in revenue that occurs when one more unit of output is sold is referred to as: A. marginal revenue. B. average revenue. C. total revenue. D. erosion. E. scenario revenue. Answer: The Eliot Co. needs $185,000 a week […]

Fin 76680

In the Black-Scholes model, the symbol “σ” is used to represent the standard deviation of the: A. option premium on a call with a specified exercise price. B. rate of return on the underlying asset. C. volatility of the risk-free […]

FIN 97032

Which one of the following is the primary difference between a swap contract and a forward contract? A. underlying asset B. number of exchanges C. daily marking to the market D. option versus obligation E. time of payment Answer: Real […]

FIN 98786

The last date on which you can purchase shares of stock and still receive the dividend is the date which is _____ business days prior to the date of record. A. 1 B. 2 C. 3 D. 4 E. 5 […]

Finance 20486

Currently, Glasgow Importers sells 280 units a month at a price of $729 a unit. The firm believes it can increase its sales by an additional 40 units if it switches to a net 30 credit policy. The monthly interest […]

Finance 29972

Which of the following statements are true based on the historical record for 1926-2010? I. Risk and potential reward are inversely related. II. Risk-free securities produce a positive real rate of return each year. III. Returns are more predictable over […]

Finance 33974

You just settled an insurance claim. The settlement calls for increasing payments over a 10-year period. The first payment will be paid one year from now in the amount of $10,000. The following payments will increase by 4.5 percent annually. […]

Finance 34409

Steve just computed the present value of a $10,000 bonus he will receive in the future. The interest rate he used in this process is referred to as which one of the following? A. current yield B. effective rate C. […]

Finance 34686

Farmer Mac owns a large orange grove in Florida. The value of his business is directly related to the price of oranges. Which one of the following is a graphical representation of this price-value relationship? A. exchange line B. net […]

Finance 38738

Long-run exposure to exchange rate risk relates to: A. daily variations in exchange rates. B. variances between spot and future rates. C. unexpected changes in relative economic conditions. D. differences between future spot rates and related forward rates. E. accounting […]

Finance 53523

The price-sales ratio is especially useful when analyzing firms that have which one of the following? A. volatile market prices B. negative earnings C. positive PEG ratios D. a negative Tobin’s Q E. increasing sales Answer: Money market securities have […]

Finance 67373

Several rumors concerning Value Rite stock are causing the market price of the stock to be quite volatile. Given this situation, you decide to buy both a one-month European $25 put and a one-month European $25 call on this stock. […]