CHAPTER 10

MAKING CAPITAL INVESTMENT

DECISIONS

Answers to Concepts Review and Critical Thinking Questions

1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a

2. For tax purposes, a firm would choose MACRS because it provides for larger depreciation

3. It’s probably only a mild oversimplification. Current liabilities will all be paid, presumably. The cash

portion of current assets will be retrieved. Some receivables won’t be collected, and some inventory

4. Management’s discretion to set the firm’s capital structure is applicable at the firm level. Since any

5. The EAC approach is appropriate when comparing mutually exclusive projects with different lives

that will be replaced when they wear out. This type of analysis is necessary so that the projects have

6. Depreciation is a noncash expense, but it is tax-deductible on the income statement. Thus

depreciation causes taxes paid, an actual cash outflow, to be reduced by an amount equal to the

7. There are two particularly important considerations. The first is erosion. Will the essentialized book

simply displace copies of the existing book that would have otherwise been sold? This is of special

CHAPTER 27 – 2

8. Definitely. The damage to Porsche’s reputation is definitely a factor the company needed to consider.

9. One company may be able to produce at lower incremental cost or market better. Also, of course,

10. Porsche would recognize that the outsized profits would dwindle as more product comes to market

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. The $3.5 million acquisition cost of the land six years ago is a sunk cost. The $3.9 million current

aftertax value of the land is an opportunity cost if the land is used rather than sold off. The $16.7

2. Sales due solely to the new product line are:

Increased sales of the motor home line occur because of the new product line introduction; thus:

in new sales is relevant. Erosion of luxury motor coach sales is also due to the new campers; thus:

is relevant. The net sales figure to use in evaluating the new line is thus:

CHAPTER 27 – 3

3. We need to construct a basic income statement. The income statement is:

Sales $ 635,000

Variable costs 279,400

4. To find the OCF, we need to complete the income statement as follows:

Sales $ 713,500

Costs 497,300

The OCF for the company is:

OCF = EBIT + Depreciation – Taxes

The depreciation tax shield is the depreciation times the tax rate, so:

Depreciation tax shield = TC(Depreciation)

The depreciation tax shield shows us the increase in OCF by being able to expense depreciation.

5. To calculate the OCF, we first need to calculate net income. The income statement is:

Sales $ 164,000

Variable costs 87,000

Using the most common financial calculation for OCF, we get:

OCF = EBIT + Depreciation – Taxes

CHAPTER 27 – 4

The top-down approach to calculating OCF yields:

OCF = Sales – Costs – Taxes

The tax-shield approach is:

OCF = (Sales – Costs)(1 – TC) + TC(Depreciation)

And the bottom-up approach is:

OCF = Net income + Depreciation

All four methods of calculating OCF should always give the same answer.

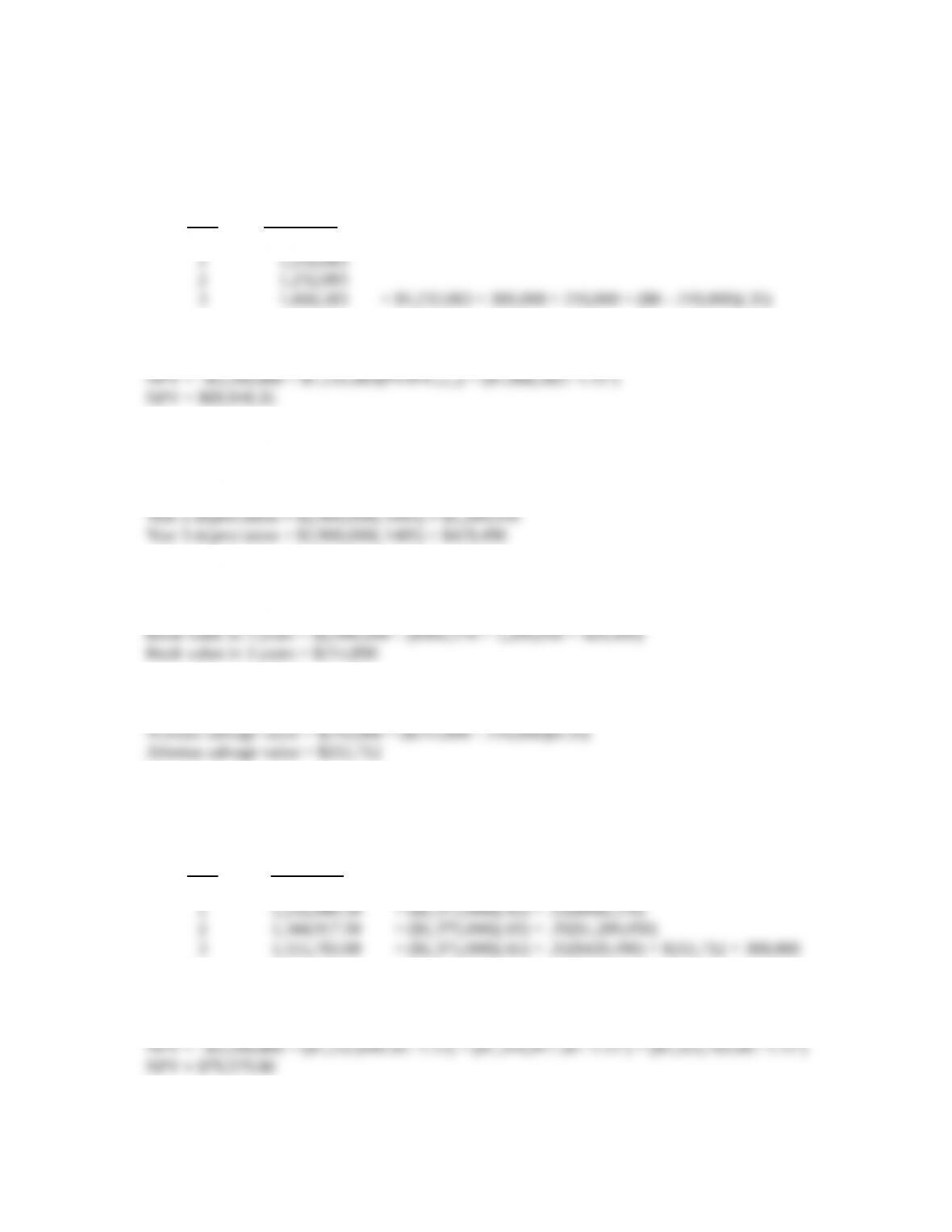

6. The MACRS depreciation schedule is shown in Table 10.7. The ending book value for any year is

the beginning book value minus the depreciation for the year. Remember, to find the amount of

depreciation for any year, you multiply the purchase price of the asset times the MACRS percentage

for the year. The depreciation schedule for this asset is:

Year

Beginning

Book Value MACRS Depreciation

Ending

Book value

1 $1,240,000.00 .1429 $177,196.00 $1,062,804.00

2 1,062,804.00 .2449 303,676.00 759,128.00

7. The asset has an eight-year useful life and we want to find the BV of the asset after five years. With

straight-line depreciation, the depreciation each year will be:

So, after five years, the accumulated depreciation will be:

CHAPTER 27 – 5

The book value at the end of Year 5 is thus:

The asset is sold at a loss to book value, so the depreciation tax shield of the loss is recaptured.

To find the taxes on salvage value, remember to use the equation:

8. To find the BV at the end of four years, we need to find the accumulated depreciation for the first

four years. We could calculate a table as in Problem 6, but an easier way is to add the MACRS

depreciation amounts for each of the first four years and multiply this percentage times the cost of

the asset. We can then subtract this from the asset cost. Doing so, we get:

The asset is sold at a gain to book value, so this gain is taxable.

9. Using the tax shield approach to calculating OCF (Remember the approach is irrelevant; the final

answer will be the same no matter which of the four methods you use.), we get:

OCF = (Sales – Costs)(1 – TC) + TC(Depreciation)

10. Since we have the OCF, we can find the NPV as the initial cash outlay plus the PV of the OCFs,

which are an annuity, so the NPV is:

CHAPTER 27 – 6

11. The cash outflow at the beginning of the project will increase because of the spending on NWC. At

the end of the project, the company will recover the NWC, so it will be a cash inflow. The sale of the

equipment will result in a cash inflow, but we also must account for the taxes that will be paid on this

sale. So, the cash flows for each year of the project will be:

Year Cash Flow

0 –$3,200,000 = –$2,900,000 – 300,000

And the NPV of the project is:

12. First we will calculate the annual depreciation for the equipment necessary for the project. The

depreciation amount each year will be:

Year 1 depreciation = $2,900,000(.3333) = $966,570

So, the book value of the equipment at the end of three years, which will be the initial investment

minus the accumulated depreciation, is:

The asset is sold at a gain to book value, so this gain is taxable.

To calculate the OCF, we will use the tax shield approach, so the cash flow each year is:

OCF = (Sales – Costs)(1 – TC) + TC(Depreciation)

Year Cash Flow

0 –$3,200,000 = –$2,900,000 – 300,000

Remember to include the NWC cost in Year 0, and the recovery of the NWC at the end of the

project. The NPV of the project with these assumptions is:

CHAPTER 27 – 7

13. First we will calculate the annual depreciation of the new equipment. It will be:

Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus

(or plus) the taxes on the sale of the equipment, so:

Very often the book value of the equipment is zero as it is in this case. If the book value is zero, the

equation for the aftertax salvage value becomes:

We will use this equation to find the aftertax salvage value since we know the book value is zero. So,

the aftertax salvage value is:

Using the tax shield approach, we find the OCF for the project is:

Now we can find the project NPV. Notice we include the NWC in the initial cash outlay. The

recovery of the NWC occurs in Year 5, along with the aftertax salvage value.

14. First we will calculate the annual depreciation of the new equipment. It will be:

The aftertax salvage value of the equipment is:

Using the tax shield approach, the OCF is:

CHAPTER 27 – 8

Now we can find the project IRR. There is an unusual feature that is a part of this project. Accepting