Chapter 26 – Mergers and Acquisitions

CHAPTER 26

MERGERS AND ACQUISITIONS

CHAPTER WEB SITES

Section Web Address

26.1 www.marketwatch.com

www.firstlist.com

www.mergernetwork.com

26.4 www.thedeal.com

CHAPTER ORGANIZATION

26.1 The Legal Forms of Acquisitions

Merger or Consolidation

Acquisition of Stock

Acquisition of Assets

Acquisition Classifications

A Note about Takeovers

Alternatives to Merger

26.2 Taxes and Acquisitions

Determinants of Tax Status

Taxable versus Tax-Free Acquisitions

26.3 Accounting for Acquisitions

The Purchase Method

More about Goodwill

26.4 Gains from Acquisition

Synergy

Revenue Enhancement

Cost Reductions

Lower Taxes

Reductions in Capital Needs

Avoiding Mistakes

A Note about Inefficient Management

26.5 Some Financial Side Effects of Acquisitions

EPS Growth

Diversification

26.6 The Cost of an Acquisition

Case I: Cash Acquisition

26-1

Chapter 26 – Mergers and Acquisitions

Case II: Stock Acquisition

Cash versus Common Stock

26.7 Defensive Tactics

The Corporate Charter

Repurchase and Standstill Agreements

Poison Pills and Share Rights Plans

Going Private and Leveraged Buyouts

Other Devices and Jargon of Corporate Takeovers

26.8 Some Evidence on Acquisitions: Do M&A Pay?

26.9 Divestitures and Restructurings

26.10 Summary and Conclusions

ANNOTATED CHAPTER OUTLINE

Video Note: See “Mergers and Acquisition”

26.1 The Legal Forms of Acquisitions

Bidder firm – the company making an offer to buy the stock or assets of another

firm

Target firm – the firm that is being sought

Consideration – cash or securities offered in an acquisition or merger

Lecture Tip: Overall, the massive wave of mergers and restructurings of the

1980s resulted in increased competitiveness, lower costs, and greater efficiency. A

not-uncommon downside to the picture, however, is the job loss and dislocation

associated with the redeployment of corporate assets. Unfortunately, popular

press writers rarely grasp the true causes of such events. One person who does is

Peter Lynch, the successful former manager of the Fidelity Magellan fund.

Consider some of his statements.

“It’s amazing that the basic cause of downsizing is so rarely

acknowledged: these companies have more workers than they

really need – or can afford to pay.

CEOs aren’t callous Scrooges shouting ‘Bah, humbug!’ as they

shove people out the door; they are responding to a competitive

situation that demands that they become more productive.

26-2

Chapter 26 – Mergers and Acquisitions

If we must blame somebody for the layoffs, it ought to be you and

me. All of us are looking for the best deals in clothing, computers

and telephone service – and rewarding the high-quality, low-cost

providers with our business. I haven’t met one person who would

agree to pay AT&T twice the going rate for phone service if AT&T

would promise to stop laying people off. These companies are

responding to the constant pressure from consumers and

shareholders.”

A. Merger or Consolidation

Merger – the complete absorption of one company by another

(assets and liabilities). The bidder remains and the target ceases to

exist.

Advantage – legally simple and relatively cheap

Disadvantage – must be approved by a majority vote of the

shareholders of both firms, usually requiring the cooperation of

both managements

Consolidation – a new firm is created. Joined firms cease their

previous existence.

Lecture Tip: Appearing relatively infrequently in previous

decades, the use of the hostile takeover bid to acquire control of a

target firm exploded in the 1980s. The term “corporate raider”

(used previously to describe someone who attempted to acquire

board seats via a proxy contest) entered the mainstream and the

stereotypical raider was cemented in the public consciousness in

the guise of the Gordon Gekko character from the movie “Wall

Street.”

Hostile takeover bids are often made via tender offer to current

shareholders, which obviates the need to obtain approval from the

target firm board. The rapid growth of hostile takeovers resulted in

the creation of an array of defensive mechanisms with which to

fight them off.

26-3

Chapter 26 – Mergers and Acquisitions

Often, but not always, hostile bids are launched against firms that

have been performing poorly; the combination of a depressed

share price and dissatisfaction with management increases the

bidder’s chance of success. Of course, bids occur for other

reasons; the series of attempts by Kirk Kerkorian against Chrysler

came following tremendous firm growth. Kerkorian, however,

wanted management to release some of the $7 billion in cash

reserves the firm had built up.

B. Acquisition of Stock

Taking control by buying the voting stock of another firm with

cash, securities, or both.

Tender offer – offer by one firm or individual to buy shares in

another firm from any shareholder. Such deals are often contingent

on the bidder obtaining a minimum percentage of the shares;

otherwise no go.

Some factors involved in choosing between a tender offer and a

merger:

1. No shareholder vote is required for a tender offer. Shareholders

choose to sell or not.

2. The tender offer bypasses the board and management of the

target firm.

3. In unfriendly bids, a tender offer may be a way around unwilling

managers.

4. In a tender offer, if the bidder ends up with less than 80% of the

target firm’s stock, it must pay taxes on any dividends paid by the

target.

5. Complete absorption requires a merger. A tender offer is often

the first step toward a formal merger.

C. Acquisition of Assets

In an acquisition of assets, one firm buys most or all of another’s

assets, but liabilities are not involved as with a merger.

Transferring titles can make the process costly. The selling firm

may remain in business.

D. Acquisition Classifications

1. Horizontal acquisition – firms in the same industry

26-4

Chapter 26 – Mergers and Acquisitions

2. Vertical acquisition – firms at different steps of in the production

process

3. Conglomerate acquisition – firms in unrelated industries

Real-World Tip: It is useful to give names to the various types of

mergers. For example, McDonnell-Douglas/Boeing,

Conoco/Phillips, and SBC/AT&T are all examples of horizontal

mergers. An example of a vertical merger would be Texaco (excess

refining capacity) and Getty Oil (significant oil reserves). U.S.

Steel’s acquisition of Marathon Oil would be a conglomerate

acquisition.

E. A Note about Takeovers

Lecture Tip: The popularity of proxy contests as a means of

gaining control has waxed and waned over the last several

decades. In the 1950s, this approach was a relatively popular

means of removing target firm management; as noted previously,

those who initiated proxy contests were even referred to in the

popular press as “corporate raiders!” Empirical evidence

suggests, however, that proxy contests are time-consuming,

expensive for the dissident shareholder, and unlikely to result in

complete victory.

Tender offers came to the fore in the 1960s and 1970s. Some

believe that the use of the proxy battle waned because of its

relatively high cost and low probability of success. However, the

ubiquity of takeover defenses and regulatory constraints has

contributed to the return of the importance of the proxy battle as a

means of gaining control.

Real-World Tip: An interesting example of a long, drawn-out

proxy battle appeared in The Wall Street Journal on October 8,

1996. Physician Steven Scott founded Coastal Physicians Group,

Inc., but was subsequently ousted by its board of directors. Dr.

Scott then filed suit and launched a proxy fight. In return, the

firm’s management counter-sued and blamed him for the firm’s

poor performance. Following several months of wrangling, two

candidates backed by Dr. Scott won board seats. The struggle for

control of Coastal is not unlike many proxy fights, in that they are

often associated with claims and counter-claims, lawsuits, and a

great deal of acrimony and expense.

26-5

Chapter 26 – Mergers and Acquisitions

Four means to gain control of a firm:

1. Acquisitions – merger or consolidation, tender offer, acquisition

of assets

2. Proxy contests – gain control by electing directors using proxies

3. Going private – all shares bought by a small group of investors

4. Leveraged buyouts (LBOs) – going private with borrowed

money

F. Alternatives to Merger

Firms could simply agree to work together via a joint venture or

strategic alliance.

26.2 Taxes and Acquisitions

A. Determinants of Tax Status

Tax-free – acquisitions must be for a business purpose, and there

must be a continuity of equity interest

Taxable – if cash or a security other than stock is used, the

acquisition is taxable

B. Taxable versus Tax-Free Acquisition

Capital gains effect – if taxable, the target’s shareholders may end

up paying capital gains taxes, driving up the cost of the acquisition

Write-up effect – if taxable, the target’s assets may be revalued,

i.e., written up and depreciation increased. However, the Tax

Reform Act of 1986 made the write up a taxable gain, making the

process less attractive.

26.3 Accounting for Acquisitions

In 2001, FASB eliminated the pooling of interest option.

There are no cash flow consequences stemming from the

accounting method used.

A. The Purchase Method

The target firm’s assets are reported at fair market value on the

bidder’s books. The difference between the assets’ market value

and the acquisition price is goodwill.

26-6

Chapter 26 – Mergers and Acquisitions

Below is an additional example depicting the balance sheet effects

of the purchase method.

Example: Firm X borrows $10 million to acquire Firm Y, creating

Firm XY.

Balance Sheets (in millions) prior to the acquisition:

Firm X Firm Y

Working Capital $ 2 Debt $ 0 Working Capital $

1

Debt $ 0

Fixed Assets 18 Equity 20 Fixed Assets 5 Equity 6

Total Assets $20 Total L&E $20 Total Assets $6 Total L&E $6

Firm Y’s fixed assets have a market value of $8 million, making

total assets worth $9 million.

Balance Sheet after the acquisition

Firm XY

Working Capital $ 3 Debt $10

Fixed Assets 26 Equity 20

Goodwill 1

Total Assets $30 Total L & E $30

B. More about Goodwill

Because of the requirement that all mergers be accounted for using

the purchase method, the FASB changed the rules on Goodwill.

Companies are no longer required to amortize goodwill. However,

it must be reduced in the case where the value has decreased.

26.4 Gains from Acquisition

A. Synergy

The difference between the value of the combined firms and the

sum of the individual firms is the incremental gain, V = VAB –

(VA + VB).

Synergy – the value of the whole exceeds the sum of the parts (V

> 0)

26-7

Chapter 26 – Mergers and Acquisitions

The value of Firm B to Firm A = VB* = V + VB. VB* will be

greater than VB if the acquisition produces positive incremental

cash flows, CF.

CF = EBIT + Depreciation – Taxes – Capital Requirements

CF = Revenue – Costs – Taxes – Capital Requirements

B. Revenue Enhancement

1. Marketing gains – changes in advertising efforts, changes in the

distribution network, changes in the product mix

2. Strategic benefits (beachheads) – acquisitions that allow a firm

to enter a new industry that may become a platform for further

expansion

3. Market power – reduction in competition or increase in market

share

Lecture Tip: The text notes several reasons for M&A activity. The

following was sent via email to members of a mergers and

acquisitions listserv.

“Do you know a business experiencing a decline in

sales, loss of direction, no longer competitive,

ineffective management, … Or a business that’s being

neglected by its corporate parent … Or a [sic] owner

looking to retire that built a once successful business

now needing reinventing … or a company that needs

strong marketing, finance, and manufacturing

disciplines … If you know such a business … it will be

worth your while to reply.”

C. Cost Reductions

1. Economies of scale – per unit costs decline with increasing

output

2. Economies of vertical integration – coordinating closely related

activities or technology transfers

3. Complementary resources (economies of scope) – example:

banks that allow insurance or stock brokerage services to be sold

on premises

D. Lower Taxes

1. Net operating losses (NOL) – a firm with losses and not paying

taxes may be attractive to a firm with significant tax liabilities

26-8

Chapter 26 – Mergers and Acquisitions

-Carry-back and carry-forward provisions reduce incentive to

merge

-IRS may disallow or restrict the use of NOL

2. Unused debt capacity – adding debt can provide important tax

savings

3. Surplus funds – firms with significant free cash flow can:

-Pay dividends

-Repurchase shares

-Acquire shares or assets of another firm

Lecture Tip: The IRS requires that the merger must have

justifiable business purposes for the NOL carry-over to be

allowed. And, if the acquisition involves a cash payment to the

target firm’s shareholders, the acquisition is considered a taxable

reorganization that results in a loss of NOLs. NOL carry-overs are

allowed in a tax-free reorganization that involves an exchange of

the acquiring firm’s common stock for the acquired firm’s common

stock. Additionally, if the target firm operates as a separate

subsidiary within the acquiring firm’s organization, the IRS will

allow the carry-over to shelter the subsidiary’s future earnings, but

not the acquiring firm’s future earnings.

E. Reductions in Capital Needs

1. A firm needing capacity acquires a firm with excess capacity

rather than building new facilities

2. Possible advantages to raising capital given economies of scale

in issuing securities

3. May reduce the investment in working capital

F. Avoiding Mistakes

1. Do not ignore market values. Use the current market value as a

starting point and ask “What will change if the merger or

acquisition takes place?”

2. Estimate only incremental cash flows. These are the basis of

synergy

3. Use the correct discount rate. Make sure to use a rate appropriate

to the risk of the cash flows

4. Be aware of transaction costs. These can be substantial and

should include fees paid to investment bankers and lawyers, as

well as disclosure costs

G. A Note about Inefficient Management

26-9

Chapter 26 – Mergers and Acquisitions

If management isn’t doing its job well, or others may be able to do

the job better, acquisitions are one way to replace management.

The threat of takeover may be enough to make managers act in the

best interest of shareholders.

Lecture Tip: One of the fathers of modern takeover theory is

Henry Manne, who published “Mergers and the Market for

Corporate Control” in 1965. In this seminal work, Manne

proposes the (now commonly accepted) notion that poorly run

firms are natural takeover targets because their market values will

be depressed, permitting acquirers to earn larger returns by

running the firms successfully. This proposition has been verified

empirically in dozens of academic studies over the last four

decades.

26.5 Some Financial Side Effects of Acquisitions

A. EPS Growth

An acquisition may give the appearance of growth in EPS without

actually changing cash flows. This happens when the bidder’s

stock price is higher than the target’s, so that fewer shares are

outstanding after the acquisition than before.

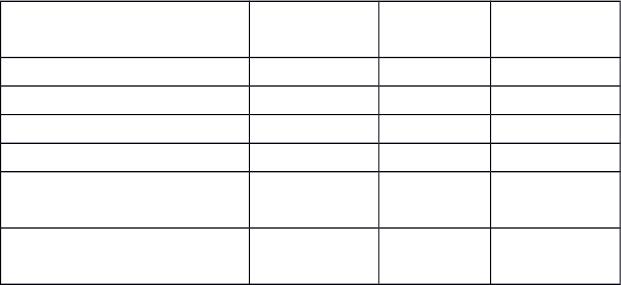

Example: Pizza Shack wants to merge with Checkers Pizza. The

merger won’t create any additional value, so, assuming the market

isn’t fooled, the new firm, Stop ‘n Go Pizza, will be valued at the

sum of the separate market values of the firms.

Stop ‘n Go is valued at $1,875,000 and has 125,000 shares

outstanding with a price of $15 per share. Pizza Shack

stockholders receive 100,000 shares, and Checkers Pizza

stockholders receive 25,000 shares.

Before and after merger financial positions

Pizza

Shack

Checkers

Pizza

Stop ‘n Go

Pizza

Total Earnings $150,000 $75,000 $225,000

Number of Shares 100,000 50,000 125,000

Earnings per Share $1.50 $1.50 $1.80

Price per Share $15.00 $7.50 $15.00

Price-to-Earnings

Ratio

10 5 8.33

Total Value $1,500,00

0

$375,00

0

$1,875,00

0

26-10

Chapter 26 – Mergers and Acquisitions

Lecture Tip: Who have been some of the top dealmakers? The

February 2007 edition of Mergers and Acquisitions Journal

indicates that six firms advised in 200 or more transactions during

2006. The number of deals and the dollar volume involved was as

follows:

2006

Leaders

(200+

Deals)

Company No. of M&A

Deals

$ Volume of M&A

Deals (millions)

1 Goldman Sachs 269 $735.4

2 JP Morgan 252 $554.5

3 Morgan Stanley 230 $616.4

4 Credit Suisse 226 $435.3

5 UBS 221 $375.6

6 Citigroup 217 $568.4

B. Diversification

A firm’s attempt at diversification does not create value because

stockholders could buy the stock of both firms, probably more

cheaply. Firms cannot reduce their systematic risk by merging.

Lecture Tip: In earlier chapters, we pointed out that conflicts of

interest may exist between stockholders and managers in publicly

traded firms. As noted above, diversification-based mergers don’t

create value for shareholders (this was illustrated using option

pricing theory in an earlier chapter); however, these mergers may

increase sales and reduce the total variability of firm cash flows. If

managerial compensation and/or prestige is related to firm size, or

if less variable cash flows reduce the likelihood of managerial

replacement, then some mergers may be initiated for the wrong

reasons – they may be in the best interest of managers but not

stockholders.

26.6 The Cost of an Acquisition

The NPV of a merger = VB* – Cost to Firm A of the acquisition

Merger premium – amount paid above the stand-alone value

26–11

Chapter 26 – Mergers and Acquisitions

Reconsider Pizza Shack’s merger with Checkers Pizza. Suppose

Pizza Shack acquires Checkers in a buyout. Pizza Shack has

estimated the incremental value of the acquisition, V, to be

$75,000. The value of Checkers to Pizza Shack is VC* = V + VC =

$75,000 + $375,000 = $450,000. Checkers shareholders are willing

to sell for $400,000. Thus, the merger premium is $25,000.

A. Case I: Cash Acquisition

Suppose Pizza Shack pays Checkers’ stockholders $400,000 in

cash. Then, NPV = $450,000 – $400,000 = $50,000.

The value of the combined firm = $1,500,000 + $50,000 =

$1,550,000

With 100,000 shares outstanding, the price per share becomes

$15.50

B. Case II: Stock Acquisition

Suppose, instead of cash, Pizza Shack gives Checkers stockholders

Pizza Shack stock valued at $15 per share. Checkers stockholders

will get 400,000 / 15 = 26,667 shares (rounded). The new firm will

have 126,667 shares outstanding and a value of $1,500,000 +

$375,000 + $75,000 = $1,950,000 for a per share price of $15.39.

The total consideration is 26,667(15.39) = $410,405.13. The extra

$10,405.13 comes from allowing Checkers stockholders

proportional participation in the $50,000 NPV.

C. Cash versus Common Stock

1. Sharing gains – When cash is used, the target’s stockholders

can’t gain beyond the purchase price. Of course, they can’t fall

below either.

2. Taxes – Cash transactions are generally taxable; exchanging

stock is generally tax-free.

3. Control – Using stock may have implications for control of the

merged firm.

26-12

Chapter 26 – Mergers and Acquisitions

Lecture Tip: Emphasize that the logic used in determining the

NPV of an acquisition is the same as that used to find the NPV of

any other project. The acquisition is desirable if the present value

of the incremental cash flows exceeds the cost of acquiring them.

However, some financial theorists argue that many acquisitions

contain a “winner’s curse.” The argument is that the winner of an

acquisition contest is the firm that most overestimates the true

value of the target. As such, this bid is most likely to be excessive.

For a more detailed discussion of the “winner’s curse,” see Nik

Varaiya and Kenneth Ferris, “Overpaying in Corporate

Takeovers: The Winner’s Curse,” Financial Analysts Journal,

1987, vol. 43. no. 3. Richard Roll, in “The Hubris Hypothesis of

Corporate Takeovers,” Journal of Business, 1986, vol. 59, no. 2,

attributed the rationale for this behavior to hubris, i.e., the

excessive arrogance or greed of management.

26.7 Defensive Tactics

A. The Corporate Charter

-Usually, 67% of stockholders must approve a merger. A

supermajority amendment requires 80% or more to approve a

merger.

-Staggered terms for board members

B. Repurchase and Standstill Agreements

A standstill agreement involves getting the bidder to agree to back

off, usually by buying the bidder’s stock back at a substantial

premium (targeted repurchase); also called greenmail.

Example: Ashland Oil bought off the Belzbergs of Canada in a

targeted repurchase. Ashland also had an established employee

stock ownership with 27% of outstanding shares owned by

employees and had earlier adopted a supermajority provision.

C. Poison Pills and Share Rights Plans

In a share rights plan, the firm distributes rights to purchase stock

at a fixed price to existing shareholders. These can’t be detached or

exercised until “triggered,” but they can be bought back by the

firm. They are usually triggered when a tender offer is made.

26-13

Chapter 26 – Mergers and Acquisitions

Flip-over provision – the “poison” in the pill. Effectively, the target

firm’s shareholders get to buy stock in the target firm at half price.

D. Going Private and Leveraged Buyouts

Can prevent takeovers from management’s point of view.

E. Other Devices and Jargon of Corporate Takeovers

1. Golden parachutes – compensation to top management in the

event of a takeover

2. Poison puts – forces the firm to buy stock back at a set price

3. Crown jewels – a “scorched earth” strategy of threatening to sell

major assets

4. White knights – target of hostile bid hopes to find a friendly firm

(white knight) to buy a large block of stock (often on favorable

terms) to halt takeover

5. Lockups – option granted to friendly firm giving it the right to

buy stock or major assets at a fixed price in the event of a hostile

takeover

6. Shark repellent – any tactic designed to discourage unwanted

takeovers

7. Bear hug – “an offer you can’t refuse”

8. Fair price provision – all selling shareholders must receive the

same price from the bidder – eliminates the ability to make a two-

tier offer to encourage shareholders to tender early

9. Dual class capitalization – more than one class of common stock

with most of the voting power privately held

10. Countertender offer – “Pac-man” defense – target offers to buy

the bidder

Ethics Note, page 834: In The Law and Finance of Corporate

Insider Trading: Theory and Evidence (Kluwer Publishing, 1993)

Arshadi and Eyssell argue that an active market for corporate

control will be characterized by increases in the nature and

complexity of defensive tactics and by an increasing volume of pre-

announcement insider trading. In the case of the former, managers

facing an environment that is (from their perspective) increasingly

hostile and will seek to defend themselves and their positions.

Defensive tactics will be implemented, tested by takeover bids and

in the courts, and modified.

26-14

Chapter 26 – Mergers and Acquisitions

Trading on nonpublic information has been shown in numerous

academic studies to be extremely profitable (albeit illegal); thus

the conclusion that financial markets are not strong-form efficient.

In the case of takeover bids, insider trading is argued to be

particularly endemic because of the large potential profits

involved and because of the relatively large number of people “in

on the secret.” Managers, employees, investment bankers,

attorneys, and financial printers have all been accused in various

takeover–related insider trading cases.

Lecture Tip: Less common, but not rare, are “reverse mergers,” in

which a firm goes public by merging with a public (often shell)

company. Ted Turner gained control of Rice Broadcasting (WJRJ-

TV) in 1970 by doing a reverse merger. Rice Broadcasting was

“virtually insolvent,” but by merging into a public company,

Turner was obtaining financing for subsequent growth.

26.8 Some Evidence on Acquisitions: Do M&A Pay?

Available evidence suggests that target stockholders make

significant gains – more in tender offers than in mergers. On the

other hand, bidder stockholders earn comparatively little, breaking

even on mergers and making a few percent on tender offers.

Lecture Tip: It is probably not overstating the matter to say that

the accepted wisdom in modern finance is that, in the aggregate,

more merger and acquisition activity is preferred to less. Dozens of

event studies report that, on average, the wealth of target firm

stockholders is greatly enhanced, while the wealth of acquiring

firm stockholders is unaffected, or at worst, slightly diminished.

For many, the notion that an active market for corporate control is

a good thing has become so ingrained that we are somewhat

surprised when others don’t view things the same way. However, in

an interesting essay in the August 1998 issue of Harpers magazine,

Lewis H. Lapham likens the sequential announcements of

seemingly ever-larger corporate combinations to the elephant act

at the circus:

26-15

Chapter 26 – Mergers and Acquisitions

“The corporate ringmasters left out the part with the

trapeze artists and the clowns. Instead of a band they

brought accountants, introducing Jumbo or Babar to

the cameras in the hotel ballroom with a blare of press

releases – how much cash for what class of stock, the

sum of the combined assets and the disposition of the

principal executives, the fate of 12,000 superfluous

workers, the newly merged colossus proclaimed the

wonder of the age. The attending media never failed to

greet the number with a roar of superlatives (the

biggest this, the richest that), and over a period of eight

weeks so many elephants plodded in and out of the

headlines that I began to wonder how the company

mahouts would manage to fit them all under the same

tent or onto the same golf course. I didn’t take a

complete set of notes, but even a brief list of some of

the more memorable exits and entrances attests to the

great and golden truth that size matters, that big is

beautiful and biggest best of all.”

In at least one sense, Lapham is correct. The 1998 merger pace

was torrid. In the first five months of the year, $630 billion worth

of mergers and acquisitions were announced. Compare that to

1996, a record year for M&A during which activity totaled $658.8

billion for the entire year. Then, take a look at 2000 when volume

was 1.78 trillion, with annual volume exceeding $1trillion in 1998-

2001, and during 2006. When you discuss mergers and the market

for corporate control in your Corporate Finance courses, you may

wish to hunt up Mr. Lapham’s essay to use as a starting point for

class discussion. While you may not agree with the points he

makes, it is extremely well-written and makes a compelling case

for what business strategists have advocated for many years –

getting back to the firm’s “core business” and doing it well.

26.9 Divestitures and Restructurings

Divestiture – a firm sells assets, operations, divisions, or segments

Reasons for a divestiture

1. Requirement after an acquisition for antitrust purposes

2. Unit may be unprofitable

3. Company may need the cash

4. Company may want to focus on core competency

26-16

Chapter 26 – Mergers and Acquisitions

Equity carve-out – parent company creates a separate company of

the division in question and then arranges an IPO where a small

fraction of the company is sold to the public. The parent company

retains enough shares to maintain control.

Spin-off – parent company distributes shares of the subsidiary to

existing stockholders in the same proportion as their ownership in

the parent company.

Split-up – company breaks into two or more companies, and

shareholders receive shares in all of the new companies.

26.10 Summary and Conclusions

26-17