Archives: Solution Manual

978-0133428704 Chapter 6 Solution Manual Part 3

6-1 1. When the office manager receives calls from potential customers, she is instructed to handle the contracts herself. Recently, however, the number of contracts written up by the office manager has declined. At the same time, one of the […]

978-0133428704 Chapter 6 Solution Manual Part 2

6-1 6-23 (45 min.) Budgeting: service company. Sunshine Window Washers (SWW) provides window-washing services to commercial clients. The company has enjoyed considerable growth in recent years due to a successful marketing campaign and favorable reviews on service-rating Web sites. Sunshine […]

978-0133428704 Chapter 6 Solution Manual Part 1

6-1 CHAPTER 6 MASTER BUDGET AND RESPONSIBILITY ACCOUNTING 6-1 The budgeting cycle includes the following elements: a. Planning the performance of the company as a whole as well as planning the performance of its subunits. Management agrees on what is […]

978-0133428704 Chapter 5 Solution Manual Part 7

5-40 (30 min.) Unused capacity, activity-based costing, activity-based management. Whitewater Adventures manufactures two models of kayaks, Basic and Deluxe, using a combination of machining and hand finishing. Machine setup costs are driven by the number of setups. Indirect manufacturing labor […]

978-0133428704 Chapter 5 Solution Manual Part 6

5-36 (30–40 min.) Activity-based costing, merchandising. Pharmahelp, Inc., a distributor of special pharmaceutical products, operates at capacity and has three main market segments: a. General supermarket chains b. Drugstore chains c. Mom-and-pop single-store pharmacies Rick Flair, the new controller of […]

978-0133428704 Chapter 5 Solution Manual Part 5

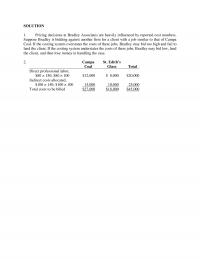

SOLUTION 1. Pricing decisions at Bradley Associates are heavily influenced by reported cost numbers. Suppose Bradley is bidding against another firm for a client with a job similar to that of Campa Coal. If the costing system overstates the costs […]

978-0133428704 Chapter 5 Solution Manual Part 4

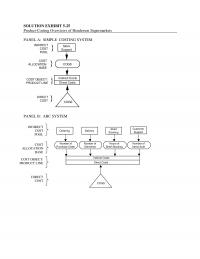

SOLUTION EXHIBIT 5-25 Product-Costing Overviews of Henderson Supermarkets PANEL A: SIMPLE COSTING SYSTEM COST OBJECT: PRODUCT LINE Indirect Costs Direct Costs Store Support COGS COGS INDIRECT COST POOL COST ALLOCATION BASE DIRECT COST PANEL B: ABC […]

978-0133428704 Chapter 5 Solution Manual Part 3

SOLUTION Note: The cost driver for engineering is number of engineering-hours, not number of engineers. This change does not, however, affect the solution itself. 1. Using the simple costing system, total overhead costs are equally allocated to projects. There were […]

978-0133428704 Chapter 5 Solution Manual Part 2

SOLUTION 1. Actual plantwide variable MOH rate based on machine hours, $308,600 4,000 $77.15 per machine hour United Motors Holden Motors Leland Auto Total Variable manufacturing overhead, allocated based on machine hours ($77.15 120; $77.15 2,800; $77.15 […]

978-0133428704 Chapter 5 Solution Manual Part 1

5-1 CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT 5-1 Broad averaging (or “peanut–butter costing”) describes a costing approach that uses broad averages for assigning (or spreading, as in spreading peanut butter) the cost of resources uniformly to cost objects when […]

978-0133428704 Chapter 4 Solution Manual Part 7

4-38 (40−55 min.) Overview of general ledger relationships. Brandon Company uses normal costing in its job-costing system. The company produces custom bikes for toddlers. The beginning balances (December 1) and ending balances (as of December 30) in their inventory accounts […]

978-0133428704 Chapter 4 Solution Manual Part 6

SOLUTION Although not required, the following overview diagram is helpful to understand Kidman’s job– costing system. 1. Professional Partner Labor Professional Associate Labor Budgeted compensation per professional Divided by budgeted hours of billable time per professional Budgeted direct-cost rate $ […]

978-0133428704 Chapter 4 Solution Manual Part 5

SOLUTION overhead rate 1. Budgeted manufacturing = Budgeted manufacturing overhead cost Budgeted direct manufacturing labor cost $125,000 50% of direct manufacturing labor cost $250,000 == 2. Overhead allocated = 50% Actual direct manufacturing labor cost = 50% $228,000 […]

978-0133428704 Chapter 4 Solution Manual Part 4

SOLUTION Some instructors may wish to assign Problem 4-25. It demonstrates the relationships of journal entries, general ledger, subsidiary ledgers, and source documents. 1. An overview of the product-costing system is 2. Amounts in millions. (1) Materials Control Accounts Payable […]

978-0133428704 Chapter 4 Solution Manual Part 3

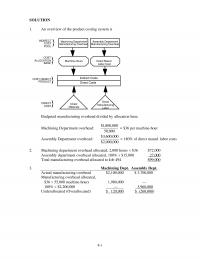

SOLUTION Some instructors may also want to assign Exercise 4-25. It demonstrates the relationships of the general ledger to the underlying subsidiary ledgers and source documents. 1. An overview of the product costing system is: 2. & 3. This answer […]

978-0133428704 Chapter 4 Solution Manual Part 2

4-1 SOLUTION 1. An overview of the product costing system is COST OBJECT: PRODUCT COST ALLOCATION BASE DIRECT COST Machining Department Manufacturing Overhead Machine-Hours Direct Materials INDIRECT COST POOL Direct Manufacturing Labor Indirect Costs Direct Costs […]

978-0133428704 Chapter 4 Solution Manual Part 1

CHAPTER 4 JOB COSTING 4-1 Cost pool––a grouping of individual indirect cost items. Cost tracing––the assigning of direct costs to the chosen cost object. Cost allocation––the assigning of indirect costs to the chosen cost object. Cost-allocation base––a factor that links […]

978-0133428704 Chapter 3 Solution Manual Part 7

SOLUTION 1. Sales of standard and deluxe carriers are in the ratio of 187,500 : 62,500. So for every 1 unit of deluxe, 3 (187,500 ÷ 62,500) units of standard are sold. Contribution margin of the bundle = 3 […]

978-0133428704 Chapter 3 Solution Manual Part 6

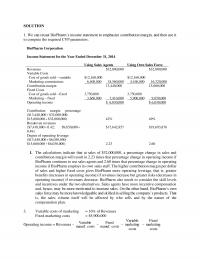

SOLUTION 1. We can recast BioPharm’s income statement to emphasize contribution margin, and then use it to compute the required CVP parameters. BioPharm Corporation Income Statement for the Year Ended December 31, 2014 Using Sales Agents Using Own Sales Force […]

978-0133428704 Chapter 3 Solution Manual Part 5

SOLUTION 1. CMU (SP – VCU = $60 – $40) $ 20.00 a. Breakeven units (FC CMU = $180,000 $20 per unit) 9,000 b. Breakeven revenues (Breakeven units SP = 9,000 units $60 per unit) $540,000 […]

978-0133428704 Chapter 3 Solution Manual Part 4

SOLUTION 1. Monthly Number of Orders Cost of Current System 300,000 $1,000,000 + $45(300,000) = $14,500,000 400,000 $1,000,000 + $45(400,000) = $19,000,000 500,000 $1,000,000 + $45(500,000) = $23,500,000 600,000 $1,000,000 + $45(600,000) = $28,000,000 700,000 $1,000,000 + $45(700,000) = $32,500,000 […]

978-0133428704 Chapter 3 Solution Manual Part 3

SOLUTION 1. Sales of A, B, and C are in ratio 24,000 : 96,000 : 48,000. So for every 1 unit of A, 4 (96,000 ÷ 24,000) units of B are sold, and 2 (48,000 ÷ 24,000) units of C […]

978-0133428704 Chapter 3 Solution Manual Part 2

3- 1 SOLUTION 1. Variable cost percentage is $3.80 $9.50 = 40% Let R = Revenues needed to obtain target net income R – 0.40R – $456,000 = $159,600 1 0.30− 0.60R = $456,000 + $228,000 R = $684,000 […]

978-0133428704 Chapter 3 Solution Manual Part 1

3- 1 CHAPTER 3 COST–VOLUME–PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Cost-volume-profit (CVP) analysis examines the behavior of […]

978-0133428704 Chapter 23 Solution Manual Part 5

23-34 (30 min.) Financial and nonfinancial performance measures, goal congruence. (CMA, adapted) Precision Equipment specializes in the manufacture of medical equipment, a field that has become increasingly competitive. Approximately 2 years ago, Pedro Mendez, president of Precision, decided to revise […]

978-0133428704 Chapter 23 Solution Manual Part 4

SOLUTION 1. ROI = Operating income ÷ Net book value of total assets St. Louis ROI = $1,446,000 ÷ ($9,000,000 – $6,600,000 + 1,999,600) = $1,446,000 ÷ $4,399,600 = 32.87% Memphis ROI = $1,008,000 ÷ ($7,500,000 – $3,500,000 + 1,536,400) […]

978-0133428704 Chapter 23 Solution Manual Part 3

SOLUTION 1. ROI and residual income: Clothing Cosmetics Operating income after tax $ 800,000 $ 1,800,000 Net assets $3,200,000 $7,500,000 ROI ($800,000 ÷ $3,200,000; $1,800,000 ÷ $7,500,000) 25.00% 24.00% RI ($800,000 − 11% × 3,200,000; $1,800,000 − 11% × $7,500,000) […]

978-0133428704 Chapter 23 Solution Manual Part 2

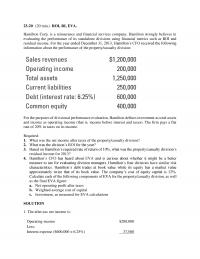

23-20 (20 min.) ROI, RI, EVA. Hamilton Corp. is a reinsurance and financial services company. Hamilton strongly believes in evaluating the performance of its standalone divisions using financial metrics such as ROI and residual income. For the year ended December […]

978-0133428704 Chapter 23 Solution Manual Part 1

23- 1 CHAPTER 23 PERFORMANCE MEASUREMENT, COMPENSATION, AND MULTINATIONAL CONSIDERATIONS 23-1 Examples of financial and nonfinancial measures of performance are Financial: ROI, residual income, economic value added, and return on sales Nonfinancial: Customer perspective: Market share, customer satisfaction Internal-business-processes perspective: […]

978-0133428704 Chapter 22 Solution Manual Part 6

22-35 (25 min.) Transfer pricing, goal congruence. The Croydon Division of CC Industries supplies the Hauser Division with 100,000 units per month of an infrared LED that Hauser uses in a remote control device it sells. The transfer price of […]

978-0133428704 Chapter 22 Solution Manual Part 5

22–33 (30–40 min.) International transfer pricing, taxes, goal congruence. Castor, a division of Gemini Corporation, is located in the United States. Its effective income tax rate is 30%. Another division of Gemini, Pollux, is located in Canada, where the income […]

978-0133428704 Chapter 22 Solution Manual Part 4

22-30 (25 min.) Goal congruence problems with cost-plus transfer-pricing methods, dual pricing system (continuation of 22-29). Assume that Pat Borges, CEO of Cranergy, had mandated a transfer price equal to 150% of full cost. Now he decides to decentralize some […]

978-0133428704 Chapter 22 Solution Manual Part 3

SOLUTION 1. The minimum transfer price that the SD would demand from the AD is the net price it could obtain from selling its screens on the outside market: $100 minus $8 marketing and distribution cost per screen, or $92 […]

978-0133428704 Chapter 22 Solution Manual Part 2

22-21 (30 min.) Effect of alternative transfer-pricing methods on division operating income. (CMA, adapted) Ajax Corporation has two divisions. The mining division makes toldine, which is then transferred to the metals division. The toldine is further processed by the metals […]

978-0133428704 Chapter 22 Solution Manual Part 1

22- CHAPTER 22 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, AND MULTINATIONAL CONSIDERATIONS 22-1 A management control system is a means of gathering and using information to aid and coordinate the planning and control decisions throughout an organization and to guide the […]

978-0133428704 Chapter 21 Solution Manual Part 5

21-1 Difference in after-tax cash flow from terminal disposal of machines: $23,020 – $14,720 = $8,300 (in favor of new machine) 2. The Frooty Company should retain the old equipment because the net present value of the incremental cash flows […]

978-0133428704 Chapter 21 Solution Manual Part 4

21-1 1. Modernizing alternative: Present Value Discount Factors Net Cash Present Year At 10% Flow Value Jan. 1, 2015 1.000 $(36,800000) $(36,800,000) Dec. 31, 2015 0.909 10,432,500 9,483,143 Dec. 31, 2016 0.826 11,700000 9,664,200 Dec. 31, 2017 0.751 12,967,500 9,738,593 […]

978-0133428704 Chapter 21 Solution Manual Part 3

21-1 SOLUTION 1. The after-tax cash inflow per year is $24,400 ($19,600 + $4,800), as shown below: Annual cash flow from operations ($43,000 – $15,000) $28,000 Deduct income tax payments (0.30 $28,000) 8,400 Annual after-tax cash flow from operations […]

978-0133428704 Chapter 21 Solution Manual Part 2

SOLUTION 1. Present value of annuity of savings in cash operating costs ($31,250 per year for 8 years at 14%): $31,250 4.639 $144,969 Present value of $37,500 terminal disposal price of machine at end of year 8: $37,500 […]

978-0133428704 Chapter 21 Solution Manual Part 1

21-1 CHAPTER 21 CAPITAL BUDGETING AND COST ANALYSIS 21-1 No. Capital budgeting focuses on an individual investment project throughout its life, recognizing the time value of money. The life of a project is often longer than a year. Accrual accounting […]

978-0133428704 Chapter 20 Solution Manual Part 4

SOLUTION 1. (a) Record purchases of direct materials Materials and In-Process Inventory Control Accounts Payable Control 550,000 550,000 (b) Record conversion costs incurred Conversion Costs Control Various Accounts (such as 440,000 Wages Payable Control) 440,000 (c) Record cost of good […]

978-0133428704 Chapter 20 Solution Manual Part 3

SOLUTION 1. 2 DP 2 10,400 $100 EOQ C $13 == EOQ = 400 steering wheels 2. Average weekly demand = 10,400 ÷ 52 weeks = 200 steering wheels per week Purchasing lead time = 1.5 weeks Reorder point […]

978-0133428704 Chapter 20 Solution Manual Part 2

20-1 SOLUTION EXHIBIT 20-21 Annual Relevant Costs of Current Production System and JIT Production System for Colonial Hardware Company Relevant Items Relevant Costs under Current Production System Relevant Costs under JIT Production System Annual tooling costs – $200,000 Required return […]

978-0133428704 Chapter 20 Solution Manual Part 1

20-1 CHAPTER 20 INVENTORY MANAGEMENT, JUST-IN-TIME, AND SIMPLIFIED COSTING METHODS 20-1 Cost of goods sold (in retail organizations) or direct materials costs (in organizations with a manufacturing function) as a percentage of sales frequently exceeds net income as a percentage […]

978-0133428704 Chapter 2 Solution Manual Part 5

SOLUTION 1.(a) Total cost of hours worked at regular rates 48 hours × $20 per hour $ 960 44 hours × $20 per hour 880 43 hours × $20 per hour 860 46 hours × $20 per hour 920 3,620 […]

978-0133428704 Chapter 2 Solution Manual Part 4

SOLUTION Shaler Corporation Schedule of Cost of Goods Manufactured Year Ended December 31, 2014 (in thousands) Direct materials costs Beginning inventory, January 1, 2014 $130,000 Purchases of direct materials 256,000 Cost of direct materials available for use 386,000 Ending inventory, […]

978-0133428704 Chapter 2 Solution Manual Part 3

2-28 (20–30 min.) Inventoriable costs versus period costs. Each of the following cost items pertains to one of these companies: Star Market (a merchandising– sector company), Maytag (a manufacturing-sector company), and Yahoo! (a service-sector company): a. Cost of lettuce and […]

978-0133428704 Chapter 2 Solution Manual Part 2

SOLUTION 1. Variable manufacturing cost per vehicle Steel $1,500 per Surfer Tires 625 per Surfer Direct manufacturing labor 700 per Surfer Total $2,825 per Surfer Fixed manufacturing costs per month Plant management costs ($1,200,000 ÷ 12) $ 100,000 Cost of […]

978-0133428704 Chapter 2 Solution Manual Part 1

2-1 CHAPTER 2 AN INTRODUCTION TO COST TERMS AND PURPOSES 2-1 A cost object is anything for which a separate measurement of costs is desired. Examples include a product, a service, a project, a customer, a brand category, an activity, […]

978-0133428704 Chapter 19 Solution Manual Part 5

3. Delays occur in the processing of B7 and A3 because of (a) uncertainty about how many orders Brandt will actually receive (Brandt expects to receive 125 orders of B7 and 10 orders of A3), and (b) uncertainty about the […]