Archives: Solution Manual

978-0133428704 Chapter 19 Solution Manual Part 4

SOLUTION EXHIBIT 19-28A Quality improvement, Pareto diagram, cause-and-effect diagram 2. Prevention activities that could reduce failures in Pauli’s Pizza deliveries could include the following: a. Better staff training b. Improved technology for order processing c. Additional time for delivery personnel […]

978-0133428704 Chapter 19 Solution Manual Part 3

19-24 (25 min.) Waiting time, cost considerations, and customer satisfaction (continued from 19-23). Refer to the information presented in Exercise 19-23. The head of the registration advisors at SMU has decided that the advisors must finish their advising in 2 […]

978-0133428704 Chapter 19 Solution Manual Part 2

SOLUTION 1. Cell Design’s managers plan to increase spending on CAD design improvement improving machine calibrations to achieve product specifications. These are prevention activities. Cell Design’s managers plan to increase prevention costs to improve quality. This is consistent with much […]

978-0133428704 Chapter 19 Solution Manual Part 1

19- 1 CHAPTER 19 BALANCED SCORECARD: QUALITY, TIME, AND THE THEORY OF CONSTRAINTS 19-1 Quality costs (including the opportunity cost of lost sales because of poor quality) can be as much as 10% to 20% of sales revenues of many […]

978-0133428704 Chapter 18 Solution Manual Part 4

SOLUTION 1. Inspection Inspection Inspection at 30% at 60% at 100% Work in process, beginning (40%)* Started during November To account for 2,400 12,000 14,400 2,400 12,000 14,400 2,400 12,000 14,400 Good units completed and transferred out Normal spoilage 9,000a […]

978-0133428704 Chapter 18 Solution Manual Part 3

18-30 (25 min.) Scrap, job costing. The Russell Company has an extensive job-costing facility that uses a variety of metals. Consider each requirement independently. Required: 1. Job 372 uses a particular metal alloy that is not used for any other […]

978-0133428704 Chapter 18 Solution Manual Part 2

SOLUTION Spoilage represents the amount of resources that go into the process but do not result in finished product. A simple way to account for spoilage in process costing is to calculate the amount of direct material that was spoiled. […]

978-0133428704 Chapter 18 Solution Manual Part 1

18- 1 CHAPTER 18 SPOILAGE, REWORK, AND SCRAP 18-1 Managers have found that improved quality and intolerance for high spoilage have lowered overall costs and increased sales. 18-2 Spoilage—units of production that do not meet the standards required by customers […]

978-0133428704 Chapter 17 Solution Manual Part 8

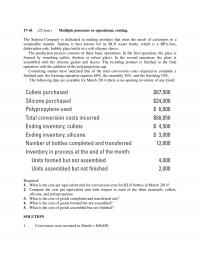

17-41 (25 min.) Multiple processes or operations, costing. The Sedona Company is dedicated to making products that meet the needs of customers in a sustainable manner. Sedona is best known for its KLN water bottle, which is a BPA-free, dishwasher-safe, […]

978-0133428704 Chapter 17 Solution Manual Part 7

SOLUTION EXHIBIT 17-39A Summarize the Flow of Physical Units and Compute Output in Equivalent Units; FIFO Method of Process Costing, Binding Department of Publishers, Inc., for April 2014. (Step 1) (Step 2) Equivalent Units Flow of Production Physical Units Transferred-in […]

978-0133428704 Chapter 17 Solution Manual Part 6

SOLUTION 1. & 2. The equivalent units of work done in April 2014 in the Assembly Department for direct materials and conversion costs are shown in Solution Exhibit 17-37A. Solution Exhibit 17-37B summarizes the total Assembly Department costs for April […]

978-0133428704 Chapter 17 Solution Manual Part 5

17-35 (30 min.) Transferred-in costs, FIFO method (continuation of 17-34). Refer to the information in Problem 17-34. Suppose that Larsen Company uses the FIFO method instead of the weighted-average method in all of its departments. The only changes to Problem […]

978-0133428704 Chapter 17 Solution Manual Part 4

SOLUTION 1. Because direct materials are added at the beginning of the assembly process, the units in this department must be 100% complete with respect to direct materials. Solution Exhibit 17-31A shows equivalent units of work done to date: Direct […]

978-0133428704 Chapter 17 Solution Manual Part 3

17-27 (35–40 min.) Transferred-in costs, FIFO method. Refer to the information in Exercise 17-26. Suppose that Trendy uses the FIFO method instead of the weighted-average method in all of its departments. The only changes to Exercise 17-26 under the FIFO […]

978-0133428704 Chapter 17 Solution Manual Part 2

17- 1 17-23 (20-25 min.) Operation costing. Whole Goodness Bakery needs to determine the cost of two work orders for the month of June. Work order 215 is for 2,400 packages of dinner rolls, and work order 216 is for […]

978-0133428704 Chapter 17 Solution Manual Part 1

17- 1 CHAPTER 17 PROCESS COSTING 17-1 Industries using process costing in their manufacturing areas include chemical processing, oil refining, pharmaceuticals, plastics, brick and tile manufacturing, semiconductor chips, beverages, and breakfast cereals. 17-2 Process costing systems separate costs into cost […]

978-0133428704 Chapter 16 Solution Manual Part 6

SOLUTION 1. Byproduct—production method journal entries i) At time of production: Work-in–process Inventory 600,000 Accounts Payable, etc. 600,000 For Byproduct: Finished Goods Inv – Shreds 35,000 Work-in-process Inventory 35,000 For Joint Products Finished Goods Inv – Floor 226,000 Finished Goods […]

978-0133428704 Chapter 16 Solution Manual Part 5

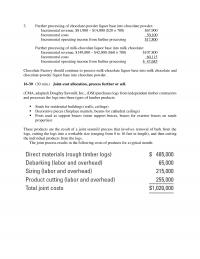

3. Further processing of chocolate-powder liquor base into chocolate powder: Incremental revenue, $81,900 – $14,000 ($20 × 700) $67,900 Incremental costs 50,100 Incremental operating income from further processing $17,800 Further processing of milk-chocolate liquor base into milk chocolate: Incremental revenue, […]

978-0133428704 Chapter 16 Solution Manual Part 4

SOLUTION 1. Net realizable value of human product: (2,000 gallons × $585) – $120,000 = $1,050,000 Net realizable value of veterinarian product: 500 gallons × ($410 – $10) = $200,000 Joint costs: $60,000 + $90,000 = $150,000 Joint costs charged […]

978-0133428704 Chapter 16 Solution Manual Part 3

SOLUTION 1a. PANEL A: Allocation of Joint Costs using Sales Value at Splitoff Method Special B/ Beef Ramen Special S/ Shrimp Ramen Total Sales value of total production at splitoff point (20,000 tons $5 per ton; 28,000 $20 […]

978-0133428704 Chapter 16 Solution Manual Part 2

16-1 SOLUTION EXHIBIT 16-19 Joint Costs Separable Costs Processing $120000 for 10000 gallons Processing $2 per gallon Processing $3 per gallon 7500 gallons 2500 gallons Methanol: 2500 gallons at $21 per gallon Turpentine: 7500 gallons at $14 per gallon Splitoff […]

978-0133428704 Chapter 16 Solution Manual Part 1

16-1 CHAPTER 16 COST ALLOCATION: JOINT PRODUCTS AND BYPRODUCTS 16-1 Exhibit 16-1 presents many examples of joint products from four different general industries. These include: Industry Separable Products at the Splitoff Point Food Processing: • Lamb • Lamb cuts, tripe, […]

978-0133428704 Chapter 15 Solution Manual Part 8

Collaborative Learning Problem 15-35 (20–25 min.) Revenue allocation, bundled products. Premier Resorts (PR) operates a five-star hotel with a championship golf course. PR has a decentralized management structure, with three divisions: ▪ Lodging (rooms, conference facilities) ▪ Food (restaurants and […]

978-0133428704 Chapter 15 Solution Manual Part 7

SOLUTION 1. Stand-alone cost-allocation method. Taylor Inc. = (600 $60) (1,000 $54) (600 $60) (400 $60) + = $36,000 $54,000 ($36,000 $24,000) + = $32,400 Victor Inc. = (400 $60) (1,000 $54) (600 $60) (400 $60) […]

978-0133428704 Chapter 15 Solution Manual Part 6

3. Comparison of Methods: Step-down method: Job 88: Machining 17 × $7.686 $130.66 Assembly 7 × $3.584 25.09 $155.75 Job 89: Machining 9 × $7.686 $ 69.17 Assembly 20 × $3.584 71.68 $140.85 Direct method: Job 88: Machining 17 × […]

978-0133428704 Chapter 15 Solution Manual Part 5

15-1 15-28 (20 min.) Revenue allocation Yang Inc. produces and sells DVDs to business people and students who are planning extended stays in China. It has been very successful with two DVDs: Beginning Mandarin and Conversational Mandarin. It is introducing […]

978-0133428704 Chapter 15 Solution Manual Part 4

978-0133428704 Chapter 15 Solution Manual Part 3

15-1 SOLUTION In some print editions of the book, requirement 1 states the airfare to be $1,600. The airfare in requirement 1 should be $1,200 instead of $1,600. 1. Alternative approaches for the allocation of the $1,200 airfare include the […]

978-0133428704 Chapter 15 Solution Manual Part 2

SOLUTION 1a. 15-1 Support Departments Operating Departments AS I S Govt. Corp. Costs $600,000 $2,400,000 Alloc. of AS costs (0.25, 0.40, 0.35) (861,538) 215,385 $ 344,615 $ 301,538 Alloc. of IS costs (0.10, 0.30, 0.60) 261,538 (2,615,385) 784,616 1,569,231 $ […]

978-0133428704 Chapter 15 Solution Manual Part 1

15-1 CHAPTER 15 ALLOCATION OF SUPPORT-DEPARTMENT COSTS, COMMON COSTS, AND REVENUES 15-1 The single-rate (cost-allocation) method makes no distinction between fixed costs and variable costs in the cost pool. It allocates costs in each cost pool to cost objects using […]

978-0133428704 Chapter 14 Solution Manual Part 7

SOLUTION EXHIBIT 14-37 Market-Share and Market-Size Variance Analysis of Houston Infonautics for the Third Quarter 2014. Static Budget: Actual Market Size Actual Market Size Budgeted Market Size Actual Market Share Budgeted Market Share Budgeted Market Share […]

978-0133428704 Chapter 14 Solution Manual Part 6

SOLUTION 1. Customer A Customer B Customer C Others Division Revenue $1,054,826 $1,544,680 $2,210,162 $480,33 2 $5,290,000 Customer-level costs 675,378 951,669 1,517,895 266,058 3,411,000 Customer-level operating income 379,448 593,011 692,267 214,274 1,879,000 Wholesale channel costs1 149,437 233,543 272,633 84,387 740,000 […]

978-0133428704 Chapter 14 Solution Manual Part 5

14-31 (30 min.) Customer-cost hierarchy, customer profitability. Denise Nelson operates Interiors by Denise, an interior design consulting and window treatment fabrication business. Her business is made up of two different distribution channels, a consulting business in which Denise serves two […]

978-0133428704 Chapter 14 Solution Manual Part 4

SOLUTION Actual Budgeted Western region 12.3 million 10 million Soda King 1.23 million 1.25 million Market share 10% 12.5% Average budgeted contribution margin per unit = $3.90 ($4,875,000 ÷ 1,250,000). Solution Exhibit 14-26 presents the sales-quantity variance, market-size variance, and […]

978-0133428704 Chapter 14 Solution Manual Part 3

SOLUTION Note: In some editions of the book, the revenues for the Pulp division has a zero missing at the end. It is shown as $9,800,00 instead of $9,800,000. Percentages for various allocation bases (old and new): Pulp Paper Fibers […]

978-0133428704 Chapter 14 Solution Manual Part 2

14-19 (20−25 min.) Customer profitability, distribution. Best Drugs is a distributor of pharmaceutical products. Its ABC system has five activities: Rick Flair, the controller of Best Drugs, wants to use this ABC system to examine individual customer profitability within each […]

978-0133428704 Chapter 14 Solution Manual Part 1

14-1 N CHAPTER 14 COST ALLOCATION, CUSTOMER-PROFITABILITY ANALYSIS, AND SALES-VARIANCE ANALYSIS 14-1 Disagree. Cost accounting data plays a key role in many management planning and control decisions. The division president will be able to make better operating and strategy decisions […]

978-0133428704 Chapter 13 Solution Manual Part 5

13-33 (30 min.) Airline pricing, considerations other than cost in pricing. Northern Airways is about to introduce a daily round-trip flight from New York to Los Angeles and is determining how to price its round- trip tickets. The market research […]

978-0133428704 Chapter 13 Solution Manual Part 4

13-28 (25 min.) Cost-plus, target return on investment pricing. Zoom-o-licious makes candy bars for vending machines and sells them to vendors in cases of 30 bars. Although Zoom-o-licious makes a variety of candy, the cost differences are insignificant, and the […]

978-0133428704 Chapter 13 Solution Manual Part 3

13-24 (25 min.) Considerations other than cost in pricing decisions. Fun Stay Express operates a 100-room hotel near a busy amusement park. During June, a 30-day month, Fun Stay Express experienced a 65% occupancy rate from Monday evening through Thursday […]

978-0133428704 Chapter 13 Solution Manual Part 2

SOLUTION 1. and 2. Manufacturing costs of HJ6 in 2012 and 2013 are as follows: 2012 2013 Per Unit Per Unit Total (2) = Total (4) = (1) (1) ÷ 2,700 (3) (3) ÷ 4,600 Direct materials, $1,400 × 2,700; […]

978-0133428704 Chapter 13 Solution Manual Part 1

13-1 CHAPTER 13 PRICING DECISIONS AND COST MANAGEMENT 13-1 The three major influences on pricing decisions are 1. Customers 2. Competitors 3. Costs 13-2 Not necessarily. For a one-time-only special order, the relevant costs are only those costs that will […]

978-0133428704 Chapter 12 Solution Manual Part 5

Required: 1. Was Cerebral successful in implementing its strategy in 2013? Explain your answer. 2. Would you have included some measure of customer satisfaction in the customer perspective? Are these objectives critical to Cerebral for implementing its strategy? Why or […]

978-0133428704 Chapter 12 Solution Manual Part 4

SOLUTION Effect of the industry-market-size factor on operating income Of the 3,000-unit increase in sales from 8,000 to 11,000 units, 10% or 800 (10% 8,000) units are due to growth in market size, and 2,2000 (3,000 − 800) units […]

978-0133428704 Chapter 12 Solution Manual Part 3

The Productivity Component Cost effect of productivity for variable costs = Actual units of Units of input input used required to to produce produce 2013 2013 output ouput in 2012 − Input price in 2013 […]

978-0133428704 Chapter 12 Solution Manual Part 2

SOLUTION Effect of the industry-market-size factor on operating income Of the 28,000-unit (233,000 – 205,000) increase in sales between 2012 and 2013, 20,500 (10% 205,000) units are due to growth in market size, and 7,500 (28,000 – 20,500) units […]

978-0133428704 Chapter 12 Solution Manual Part 1

12- 1 CHAPTER 12 STRATEGY, BALANCED SCORECARD, AND STRATEGIC PROFITABILITY ANALYSIS 12-1 Strategy specifies how an organization matches its own capabilities with the opportunities in the marketplace to accomplish its objectives. 12-2 The five key forces to consider in industry […]

978-0133428704 Chapter 11 Solution Manual Part 7

SOLUTION 1. Let D represent the batches of Della’s Delight made and sold. Let B represent the batches of Bonny’s Bourbon made and sold. The contribution margin per batch of Della’s Delight is $300. The contribution margin per batch of […]

978-0133428704 Chapter 11 Solution Manual Part 6

SOLUTION 1. and 2. Division A Division B Sales $504,000 $948,000 Variable costs of goods sold ($440,000 0.90; $930,000 0.80) 396,000 744,000 Variable S,G & A ($96,000 0.50; $202,500 0.50) 48,000 101,250 Total variable costs 444,000 […]

978-0133428704 Chapter 11 Solution Manual Part 5

SOLUTION 1. 11-1 A110 B382 C657 Selling price $168 $ 112 $140 Variable costs: Direct materials (DM) 48 30 18 Labor and other costs 56 54 80 Total variable costs 104 84 98 Contribution margin $ 64 $ 28 $ […]