Archives: Solution Manual

Chapter 1 Vast resources would have been wasted as pilots

Principle 7: Resources should be used efficiently to achieve society’s goals. Priceline.com exploited an oppor- tunity to use resources more efficiently. It is inefficient to have empty hotel rooms and airline seats if someone is willing to pay some price […]

Psychology Chapter 7 Homework The Psychodynamic Viewpoint Originally Focused Drive Theory

Psychology Chapter 6 Homework All Therapists Have Legal And Ethical Responsibilities

Psychology Chapter 5 Homework Origins And Growth Family Therapy Learning

Psychology Chapter 4 Homework Change Common Families They Face Life Cycle

Psychology Chapter 3 Homework Culture, gender, and socioeconomic status are key interrelated

Psychology Chapter 2 Homework While The Progression Generally Orderly And Sequenced

Psychology Chapter 1 Homework The Way Functions Establishes Rules Communicates And

Accounting Chapter 24 Strikes are considered general knowledge and therefore

CA 24.3 (Continued) Situation 3 The fact that a company chooses to self-insure the contingency of injury to others caused by its vehicles is not enough of a basis to accrue a loss contingency that has not occurred at the […]

Accounting Chapter 24 The Possible Effect The Market Price The

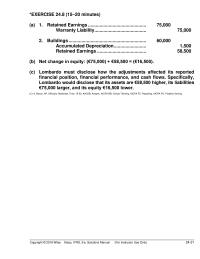

*EXERCISE 24.8 (15–20 minutes) (a) 1. Retained Earnings ……………………………………… 75,000 Warranty Liability …………………………………. 75,000 2. Buildings …………………………………………………… 60,000 Accumulated Depreciation ……………………. 1,500 Retained Earnings ……………………………….. 58,500 (b) Net change in equity: (€75,000) + €58,500 = (€16,500). (c) Lombardo must disclose […]

Accounting Chapter 24 Ratio computations and additional analysis

CHAPTER 24 Presentation and Disclosure in Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis * 1. The disclosure principle; type of disclosure. 2, 3, 22 1, 2, 3 * 2. Role of […]

Accounting Chapter 24 Income Tax Expense Benefit 8 Significant Noncash

Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s Manual 24–13 *51. (L.O. 13) When a company first adopts IFRS, it must present at least one year of comparative information, and its first set of financial […]

Accounting Chapter 24 Accountants and business executives are fully aware

Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s Manual 24-1 CHAPTER 24 Presentation and Disclosure in Financial Reporting LEARNING OBJECTIVES 1. Review the full disclosure principle and describe how it is implemented. 2. Discuss the […]

Accounting Chapter 23 Puma Concerning Trend That Should Monitored Investors

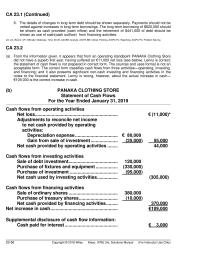

CA 23.1 (Continued) 6. The details of changes in long-term debt should be shown separately. Payments should not be netted against increases in long-term borrowings. The long-term borrowing of $620,000 should be shown as cash provided (cash inflow) and the […]

Accounting Chapter 23 Reduction in long-term notes payable

PROBLEM 23.3 MORTONSON PLC Statement of Cash Flows For the Year Ended December 31, 2019 (£ in thousands) Cash flows from operating activities Cash receipts from customers ……………….. £3,520 (a) Cash payments: Payments for merchandise ………………… £1,270 (b) Salaries and […]

Accounting Chapter 23 Depreciation Expense Gain Sale Investment

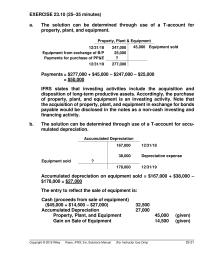

EXERCISE 23.10 (25–35 minutes) a. The solution can be determined through use of a T-account for property, plant, and equipment. Property, Plant & Equipment 12/31/18 247,000 45,000 Equipment sold Equipment from exchange of B/P 25,000 Payments for purchase of PP&E […]

Accounting Chapter 23 Net Cash Provided Financing Activities

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement. 1, 2, 5, 7, 8, 12 1, 2, 5, 6 2. Classifying […]

Accounting Chapter 23 Changes Deferred Income Taxes Affect Net Income

1. Describe the usefulness and format of the statement of cash flows. 3. Contrast the direct and indirect methods of calculating net cash flows from operating activities. Copyright © 2018 John Wiley & Sons, Inc. Kieso Intermediate: IFRS 3e, Instructor’s […]

Accounting Chapter 22 Under This Approach The Cumulative Effect The

PROBLEM 22.7 (Continued) (9) Insurance Expense ($12,000 ÷ 3) ………………………………… 4,000 Prepaid Insurance …………………………………………………….. 6,000 Retained Earnings ……………………………………………… 10,000 (10) Amortization Expense ($50,000 ÷ 10) ………………………….. 5,000 Retained Earnings …………………………………………………….. 5,000 Trademarks ……………………………………………………….. 10,000 LO: 3,4, Bloom: AP, Difficulty: Moderate, […]

Accounting Chapter 22 Purpose—to develop an understanding of the correcting

EXERCISE 22.15 (Continued) 4. Amortization Expense—Copyright …………………… 2,500(c) Retained Earnings ………………………………………….. 5,000(d) Copyright ($2,500 + $5,000) ………………………. 7,500 ($50,000 ÷ 20 = $2,500(c); ($2,500 X 2 = $5,000(d)) 5. Loss on Write-down of Inventories (or Cost of Goods Sold) ……………………………….. […]

Accounting Chapter 22 Requirement by International Accounting Standards

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 22-1 CHAPTER 22 Accounting for Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Differences between change […]

Accounting Chapter 22 The Books Have Been Closed The Error

2. Describe the accounting and reporting for changes in estimates. 3. Describe the accounting for correction of errors. 4. Analyze the effect of errors. CHAPTER 22 Accounting Changes and Error Analysis LEARNING OBJECTIVES 1. Discuss the types of accounting changes […]

Accounting Chapter 21 the appropriate accounting treatment which should

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS CA 21.1 (Time 15–25 minutes) Purpose—to provide the student with an understanding of the theoretical reasons for requiring leases to be capitalized by the lessee and how a lease is recorded at its […]

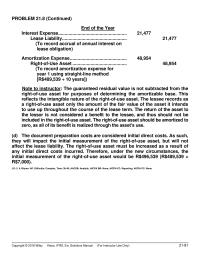

Accounting Chapter 21 The guaranteed residual value is not subtracted from

PROBLEM 21.8 (Continued) End of the Year Interest Expense …………………………………………….. 21,477 Lease Liability ………………………………………….. 21,477 (To record accrual of annual interest on lease obligation) Amortization Expense …………………………………….. 48,954 Right-of–Use Asset …………………………………… 48,954 (To record amortization expense for year 1 using […]

Accounting Chapter 21 August Because The Agreement Began That Date

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 21–61 Problem 21.9 (Time 30–40 minutes) Purpose—to develop an understanding of the accounting treatment accorded a sales-type lease involving an unguaranteed residual value. The student is required […]

Accounting Chapter 21 The Initial Measurement The Right of use Asset Will

EXERCISE 21.11 (20–30 minutes) (a) The lease agreement has a bargain-purchase option. The collectibility of the lease payments by Mooney is probable. The lease, therefore, qualifies as a sales- type lease from the viewpoint of the lessor. The lease payments […]

Accounting Chapter 21 Employee salaries are specifically excluded as initial

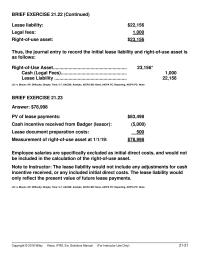

BRIEF EXERCISE 21.22 (Continued) Lease liability: $22,156 Legal fees: 1,000 Right-of–use asset: $23,156 Thus, the journal entry to record the initial lease liability and right–of-use asset is as follows: Right-of–Use Asset ………………………………………………… 23,156* Cash (Legal Fees) …………………………………………… 1,000 Lease Liability […]

Accounting Chapter 21 Lessee Entries with Bargain-Purchase Option

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Rationale for leasing. 1, 2, 3 2. Concepts, and measurement of leases by lessees. 4, 5, 6, 7, 8, 9, […]

Accounting Chapter 21 From The Perspective The Lessee There Unguaranteed

3. Explain the accountinf for leases by lessors. 4. Discuss the accounting and reporting for special features of lease arrangements. *5. Describe the lessee’s accounting for sale-leaseback transactions. *6. Apply lessee and lessor accounting to finance and operating leases. *This […]

Banking Chapter 25 When weights inversely proportional to bid-ask

Accounting Chapter 20 While Selma May Correct Assuming That

CA 20.6 While Selma may be correct in assuming that the termination of non-vested employees would decrease its pension-related liabilities and associated expenses, she is callous to suggest that firing employees is a reasonable approach to correcting the underfunding of […]

Banking Chapter 24 simply subtracts the strike price of 100 from each node of

Accounting Chapter 20 Pension Asset liability The Cumulative Net Pension Expense

20-61 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) CHEN Group. Pension Worksheet—2019 General Journal Entries Memo Record PROBLEM 20.12 Annual Pension Expense Cash OCI— Gain/Loss Pension Asset/Liability Defined Benefit Obligation Plan Assets Balance, Jan. […]

Banking Chapter 23 we conclude that the equity and credit markets

Accounting Chapter 20 Other comprehensive income gain

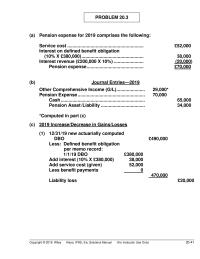

PROBLEM 20.3 (a) Pension expense for 2019 comprises the following: Service cost ………………………………………………….. £52,000 Interest on defined benefit obligation (10% X £380,000) ………………………………………… 38,000 Interest revenue (£200,000 X 10%) ………………….. (20,000) Pension expense …………………………………….. £70,000 (b) Journal Entries—2019 Other Comprehensive […]

Banking Chapter 22 factor ensuring that the process is a martingale

Accounting Chapter 20 A pension worksheet follows to provide supporting

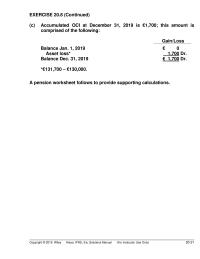

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 20–21 EXERCISE 20.8 (Continued) (c) Accumulated OCI at December 31, 2019 is €1,700; this amount is comprised of the following: Gain/Loss Balance Jan. 1, 2019 € 0 […]

Banking Chapter 22 we begin by looking at the standard formulation a put

Accounting Chapter 20 The Cost The Retroactive Benefits The Increase

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Basic definitions and concepts related to pension plans. 1, 2, 3, 4, 5, 6, 7, 8, 9, […]

Banking Chapter 21 the quadratic variation between the two processes is zero

Banking Chapter 20 This market price of risk is the compensation

Accounting Chapter 20 A pension plan is an arrangement whereby an employer

3. Explain the accounting for past service costs. 4. Explain the accounting for remeasurements. 5. Describe the requirements for reporting pension plans in financial statements. 6. Explain the accounting for other postretirement benefits. CHAPTER 20 Accounting for Pensions and Postretirement […]

Banking Chapter 19 The floating leg of the swap can be seen as a

Accounting Chapter 19 Nol Expected The Year That Future Deductible

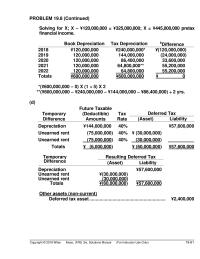

PROBLEM 19.8 (Continued) Solving for X; X – ¥120,000,000 = ¥325,000,000; X = ¥445,000,000 pretax financial income. Book Depreciation Tax Depreciation bDifferenceb 2018 ¥120,000,000 ¥240,000,000* (¥(120,000,000) 2019 120,000,000 144,000,000 (24,000,000) 2020 120,000,000 86,400,000 33,600,000 2021 120,000,000 64,800,000** 55,200,000 2022 120,000,000 […]

Banking Chapter 18 The term represents the long term expected spot rate

Accounting Chapter 19 Permanent Differences Bond Interest Revenue Pollution Fines

Time and Purpose of Problems (Continued) Problem 19.8 (Time 40–50 minutes) Purpose—to test a student’s understanding of the relationships that exist in the subject area of accounting for income taxes. The student is required to compute and classify deferred income […]

Banking Chapter 17 We chose u and d such that the tree is recombining.

Accounting Chapter 19 Originating difference which will result in future

EXERCISE 19.11 (10–15 minutes) Resulting Deferred Tax Temporary Difference (Asset) Liability Depreciation €200,000 Lawsuit obligation €(50,000) Installment sale 300,000 Totals €(50,000) €500,000 Non-current liabilities Deferred tax liability (€500,000 – €50,000) ………………………. €450,000 LO: 1,4, Bloom: AP, Difficulty: Simple, Time: 10-15, […]

Banking Chapter 16 Payoff Diagram for an interest rate swaption

Accounting Chapter 19 The 12000 Deferred Tax Liability Should Classified

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 12 1 1, 2, 4, 12, 18 1, 2, 3, 8 […]