Archives: Solution Manual

978-0132664257 Chapter 4 Solution Manual

Chapter 4 Choosing Elements to Build Brand Equity Chapter Objectives 1. Identify the dierent types of brand elements. 2. List the general criteria for choosing brand elements. 3. Describe key tactics in choosing dierent brand elements. 4. Explain the rationale […]

978-0132664257 Chapter 3 Solution Manual

Chapter 3 Brand Resonance and the Brand Value Chain Chapter Objectives 1. Dene brand resonance. 2. Describe the steps in building brand resonance. 3. Dene the brand value chain. 4. Identify the stages in the brand value chain. 5. Contrast […]

978-0132664257 Chapter 2 Solution Manual

Chapter 2 Customer-Based Brand Equity and Brand Positioning Learning Objectives 1. Dene customer-based brand equity. 2. Outline the sources and outcomes of customer-based brand equity. 3. Identify the four components of brand positioning. 4. Describe the guidelines in developing a […]

978-0132664257 Chapter 1 Solution Manual

Chapter 1 Brands & Brand Management Chapter Objectives 1. Dene “brand,” state how brand diers from a product, and explain what brand equity is. 2. Summarize why brands are important. 3. Explain how branding applies to virtually everything. 4. Describe […]

978-1133939283 Chapter 16 Solution Manual Part 7

had problems but did not go bankrupt. Both companies have shown improved results of Thus, liquidity measures such as cash flow yield and cash flows to sales and assets, as their operations since 2009. Standard & Poor’s (S&P) judges the […]

978-1133939283 Chapter 16 Solution Manual Part 6

*Rounded days times $293,600 25.6 2.5 times Ranbaxy 1.2 $3,941,600 $293,600 $338,400 + $338,400 $456,000$5,013,600 = $1,600,000 $3,941,600 14.3 $1,600,000 a. 1. Quick ratio* d. Operating asset management analysis b. Current ratio* $10,519,200 $4,184,000 $4,184,000 $1,376,000 22.7 $2,211,200 $1,376,000 $320,000 […]

978-1133939283 Chapter 16 Solution Manual Part 5

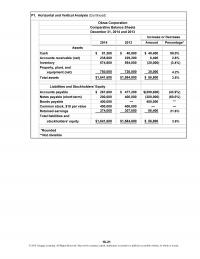

1. 2014 2013 Amount Percentage* Alternate Problems P7. Horizontal and Vertical Analysis Comparative Income Statements For the Years Ended December 31, 2014 and 2013 Increase or Decrease Rylander Corporation *Rounded 16-41 © 2014 Cengage Learning. All Rights Reserved. May not […]

978-1133939283 Chapter 16 Solution Manual Part 4

Quick ratio* Operating asset management analysis b. d. c. Design a. *Rounded $552,800 2.8 days16.1= times times Days’ sales uncollected* Receivables turnover* = times Design Single $1,253,400 $400,000 $73,400 $985,400$84,600 $400,000 times= $1,262,400 = $1,046,000 1.2 25.6 14.3= days times […]

978-1133939283 Chapter 16 Solution Manual Part 3

2014 2013 Amount Percentage* Property, plant, and equipment (net) 750,000 720,000 30,000 4.2% Total assets $1,641,600 $1,584,800 $ 56,800 3.6% Accounts payable $ 267,600 $ 477,200 $(209,600) (43.9%) Notes payable (short-term) 200,000 400,000 (200,000) (50.0%) Bonds payable 400,000 — 400,000 […]

978-1133939283 Chapter 16 Solution Manual Part 2

1. c 6. 2. e 7. 3. c 8. 4. b 9. 5. a 10. 2014 2013 2012 2011 2010 *Rounded Exercises: Set A Although sales increased over the five-year period, operating income decreased because cost of goods sold increased […]

978-1133939283 Chapter 16 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ9. DQ10. are full values similar to those at year end. Thus, any ratios that use data from the income statement or statement of cash flows as their basis will be less than they increase in […]

978-1133939283 Chapter 16 Lecture Note

Chapter 16 Financial Statement Analysis Learning Objectives 1. Describe the concepts, standards of comparison, and sources of information used in measuring nancial performance. 2. Apply horizontal analysis, vertical analysis, and ratio analysis to nancial statements. 3. Apply nancial ratio analysis […]

978-1133939283 Chapter 15 Solution Manual Supplement- Solutions

=+(–) =+ = = +(–)+(–) =+ + = = –(–)+(–)– =– + – = =+ = CHAPTER 15 SUPPLEMENT—Solution s $96,200 THE STATEMENT OF CASH FLOWS $12,500 $600 $79,000 Cost of $294,200 $294,200 $304,800 Expense $58,700 $79,000 $426,500 $457,700 $426,500 […]

978-1133939283 Chapter 15 Solution Manual Part 4

ating activities. The financial press would give a better picture of a company’s cash posi- tion by focusing on cash flows from operating activities and cash flow yield. assets and current liabilities, which can have a significant effect on cash […]

978-1133939283 Chapter 15 Solution Manual Part 3

Operating Investing Financing Noncash Activity Activity Activity Transaction Increase Decrease No Effect dividend. X X issuing stock. XX ment with cash. X X equipment. X X securities (long-term). X X stock. X X 10. Sold a machine at a loss. […]

978-1133939283 Chapter 15 Solution Manual Part 2

Net Cash Flows from Operating Activities Instructor’s Resource CD and website. E9A. Cash-Generating Efficiency Ratios and Free Cash Flow $390,000 =Net Income Cash Flow Yield 15-9 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or […]

978-1133939283 Chapter 15 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. current liabilities, the results could overwhelm the earnings and create negative cash flows from operating activities. statement. cash flows are the details of the changes. For instance, cash flows from oper- ating activities is […]

978-1133939283 Chapter 15 Lecture Note

Chapter 15 The Statement of Cash Flows Learning Objectives 1. Describe the principal purposes and concepts underlying the statement of cash ows, and identify its components and format. 2. Use the indirect method to determine cash ows from operating activities. […]

978-1133939283 Chapter 14 Solution Manual Part 6

Cases C1. Conceptual Understanding: Bond Issue Unsecured notes (or debenture bonds) are bonds issued on the general credit of the or- the original issue price was face value or 100, both the interest expense and the interest payment were 6.125 […]

978-1133939283 Chapter 14 Solution Manual Part 5

4. a. b. c. $10,000,000 Bonds payable (×) (150,000) $ 9,850,000 ( × $ 5,000,000 4,850,000 $ 9,850,000 Total common stock issue amount $20shares $150,000 of the $300,000 discount remains to be amortized. Since the call takes place after 10 […]

978-1133939283 Chapter 14 Solution Manual Part 4

(××6/12)− (××6/12)= −= (××6/12)− (××6/12)= −= Paid semiannual interest and amortized 0.09 the discount on 9%, 20-year bonds 0.10 2015 $9,147,000 $10,000,000 $457,000 $457,350 $450,000 $7,000 $450,000 $7,350 * 31 457,350 7,350 450,000 May Cash Unamortized Bond Discount Bond Interest […]

978-1133939283 Chapter 14 Solution Manual Part 3

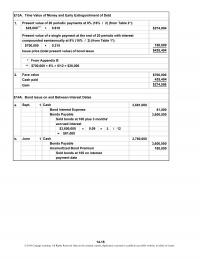

1. * ** 2. $700,000 425,404 $274,596 a. 1 3,681,000 81,000 3,600,000 Face value Cash paid Bond Interest Expense Bonds Payable Sept. Cash Gain E14A. Bond Issue on and Between Interest Dates ××3/ = $81,000 b. 1 3,780,000 3,600,000 180,000 […]

978-1133939283 Chapter 14 Solution Manual Part 2

Present value of 40 periodic payments at 6% (from Table 2*): *From Appendix B E3A. Valuing Bonds Using Present Value Choice A 14-8 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a […]

978-1133939283 Chapter 14 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. amount paid on a lease is tax-deductible and provides greater liquidity. This is debt to equity and interest coverage ratios. The analysis may also include a his- can then judge how well […]

978-1133939283 Chapter 14 Lecture Note Part 2

Summary A bond is a security, usually long-term, that represents money that a corporation or some other entity borrows from the investing public. Bondholders are considered creditors (not owners) of the issuing corporation, who are entitled to periodic interest plus […]

978-1133939283 Chapter 14 Lecture Note Part 1

Chapter 14 Long-Term Liabilities Learning Objectives 1. Explain the concepts underlying long-term liabilities, and identify the types of long-term liabilities. 2. Describe the features of a bond issue and the major characteristics of bonds. 3. Record bonds issued at face […]

978-1133939283 Chapter 13 Solution Manual Part 6

2015 Jan. 4 Mar. 8 Apr. 20 144,000 144,000 May 4 64,000 48,000 16,000 July 15 412,800 412,800 Dividends Payable share Dividends Treasury Stock, Common Paid-in Capital, Treasury Stock Sold 4,000 shares of treasury stock for $16 per share; originally […]

978-1133939283 Chapter 13 Solution Manual Part 5

4. P9. Preferred and Common Stock Dividends and Dividend Yield (Concluded) have to be made up. The difference is that with noncumulative preferred stock, if Both cumulative and noncumulative preferred stock have a fixed level of dividends and are thus […]

978-1133939283 Chapter 13 Solution Manual Part 4

2. * $11,500 – $980 = $10,520 3. (+ )/2 Preferred stock, $100 par value, 9%, 5,000 shares $11,500 times Average Stockholders’ Equity $236,520 $245,500 $11,500 Net Income = $0.02 $20.00 = 0.1% = = Dividend Yield Dividends per Share […]

978-1133939283 Chapter 13 Solution Manual Part 3

8,000,000 $12,800,000 16,000,000 $28,800,000 $ 4,800,000 Common stock, $4 par value, 1,600,000 shares authorized, 1,200,000 shares issued and outstanding 8,000,000 $12,800,000 16,000,000 $28,800,000 Common stock, $12 par value, 1,600,000 shares authorized, Additional paid-in capital Total contributed capital Total stockholders’ equity […]

978-1133939283 Chapter 13 Solution Manual Part 2

1. 4. 2. 5. 3. 1. 4. 7. 2. 5. 8. Preferred stock, $100 par value, 9% cumulative, 10,000 shares authorized, P CPP E3A. Characteristics of Common and Preferred Stock PC Total stockholders’ equity 3. 6. 9. PCP Contributed capital: […]

978-1133939283 Chapter 13 Solution Manual Part 1

DQ1. DQ5. DQ6. record, the seller will not receive the dividend because the date of record is the own stock, the company is in effect reducing its stockholders’ equity. date at which ownership of the stock of a company and […]

978-1133939283 Chapter 13 Lecture Note Part 2

Summary A corporation’s balance sheet contains assets, liabilities, and a stockholders’ equity section. Stockholders’ equity is made up of contributed capital (the stockholders’ investments) and retained earnings (earnings that have remained in the business), and sometimes treasury stock. A corporation […]

978-1133939283 Chapter 13 Lecture Note Part 1

Chapter 13 Accounting for Corporations Learning Objectives 1. Dene the corporate form of business and its characteristics. 2. Identify the components of stockholders’ equity and their characteristics. 3. Account for the issuance of stock for cash and other assets. 4. […]

978-1133939283 Chapter 12 Solution Manual Part 4

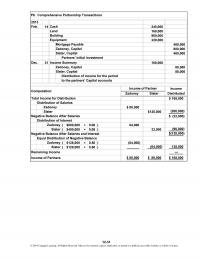

Income of Partner Zadoney Slater Distributed $ 168,000 $ 80,000 $120,000 (200,000) $ (32,000) ( $800,000 × 0.08 ) 64,000 ( $400,000 × 0.08 ) 32,000 (96,000) $(128,000) ( $128,000 × 0.50 ) (64,000) ( $128,000 × 0.50 ) (64,000) […]

978-1133939283 Chapter 12 Solution Manual Part 3

×= 0.20 $90,000 $18,000 b. 31 40,000 40,000 c. 31 60,000 48,000 6,000 2,000 4,000 $180,000 60,000 $240,000 $ 60,000 ×48,000 $ 12,000 Frank, Capital Frank, Capital Computation: Sale of a 20 percent interest in the James, Capital Capital of […]

978-1133939283 Chapter 12 Solution Manual Part 2

Amit’s equity ( ×$ 80,000 $120,000 80,000 $ 40,000 ) Bonus to the original partners $400,000 Amit’s investment Less Amit’s equity 0.20 * ×1/5 ×1/5 ×3/5 $ 8,000 24,000 ) ) Ronald ( 8,000 Fenny ( ) $40,000 $40,000 $40,000 […]

978-1133939283 Chapter 12 Solution Manual Part 1

DQ1. to decide how to pay the liabilities, and they will have to settle their capital accounts, just as they would if cash were involved. Discussion Questions Partnerships are indeed separate entities from the partners from an accounting standpoint, CHAPTER […]

978-1133939283 Chapter 12 Lecture Note Part 2

Dissolution of a partnership occurs whenever there is a change in partners. Dissolution can occur upon admission of a new partner, withdrawal of a partner, or death of a partner. For example, when a new partner is admitted to a […]

978-1133939283 Chapter 12 Lecture Note Part 1

Chapter 12 Accounting for Partnerships Learning Objectives 1. Dene the partnership form of business, and identify its principal characteristics. 2. Record partners’ investments of cash and other assets when a partnership is formed. 3. Compute and record the income or […]

978-1133939283 Chapter 11 Solution Manual Part 3

1. (×) (×) (×) 2. the documents are missing. For instance, there may be a bank loan or other loan out- Total current liabilities Federal income tax withholding $14,000 Federal unemployment tax payable 0.008 $36,988.20 952.00 112.00 Current liabilities may […]

978-1133939283 Chapter 11 Solution Manual Part 2

12. 13. 14. 2. Problems P1. Identification of Current Liabilities, Contingencies, and Commitments sheet with a dollar amount and the ones that would involve the most judgment or discretion include the estimated liabilities such as income taxes payable, property taxes […]

978-1133939283 Chapter 11 Solution Manual Part 1

DQ1. DQ6. DQ7. The present value concept allows the decision maker to compare various alterna- Increasing payables turnover is good for the company in the sense that it is able to creasing payables turnover is bad for the company because […]

978-1133939283 Chapter 11 Lecture Note Part 2

Summary Current liabilities consist of denitely determinable liabilities and estimated liabilities. Denitely determinable liabilities are obligations that can be measured exactly. They include accounts payable, bank loans and commercial paper, notes payable, accrued liabilities, dividends payable, sales and excise taxes […]

978-1133939283 Chapter 11 Lecture Note Part 1

Chapter 11 Current Liabilities and Fair Value Accounting Learning Objectives 1. Dene current liabilities, and identify the concepts underlying them. 2. Identify, compute, and record denitely determinable and estimated current liabilities. 3. Distinguish contingent liabilities from commitments. 4. Identify the […]

978-1133939283 Chapter 10 Solution Manual Part 3

1. Carrying Value * † $22,500 – $2,500 = $20,000 100% / 4 = 25%; 25% × 2 = 50% ** *** 2. a. A loss of ( – b. A loss of ( – $12,500 $12,500 $12,000 $12,000 $500 […]

978-1133939283 Chapter 10 Solution Manual Part 2

2015 225 Accumulated Depreciation—Computer ( – ) / 5 $250 years $2,500 ×6/12= $225 2,500 Computer 2,500 Computer 3. 2015 July 1 Accumulated Depreciation—Computer Cash Computer sold for $400; loss recognized Computer sold for $1,100; gain recognized 1,100 1,575 *($2,500 […]

978-1133939283 Chapter 10 Solution Manual Part 1

1. 7. 8. cipates superior earnings and believes it will more than recoup the goodwill it extra funds to invest and expand. The major advantage for a company that has positive free cash flow is that it has purchased. A […]

978-1133939283 Chapter 10 Lecture Note Part 2

Summary The cost of a long-term asset includes the purchase cost, freight charges, insurance while in transit, installation, and other costs involved in the acquisition of the asset. Interest incurred during the construction of a plant asset is included in […]

978-1133939283 Chapter 10 Lecture Note Part 1

Chapter 10 Long-Term Assets Learning Objectives 1. Identify the classications of long-term assets, and describe how they are valued by allocating their cost to the periods that they benet. 2. Account for the acquisition cost of property, plant, and equipment. […]