Archives: Solution Manual

978-1133939283 Chapter 9 Solution Manual Part 4

● Cases amount of uncollectible accounts that will arise from these credit sales and record it as C1. Conceptual Understanding: Role of Credit Sales Mitsubishi established the generous credit terms of 14 months without interest and pay- ments because management […]

978-1133939283 Chapter 9 Solution Manual Part 3

×11 /×/= 2. 3 ×12/×/= May $2,288.22 $120,000 365 58 100 16 × 13 / × / = May 100 $64,000 365 45 1,025.75 31 × 11 / × / = 542.47 100 30 $60,000 365 May 3. 0 90 […]

978-1133939283 Chapter 9 Solution Manual Part 2

Before Write-off After Write-off Write-off 2,400 Bal. 800 3,200Bal. Accounts Receivable Bal. 32,500 32,500 3,600 Write-off 2,400 Bal. Sale Bal. 34,900 Collection 1,200 Allowance for Uncollectible Accounts E7A. Write-off of Accounts Receivable *Rounded 9-10 © 2014 Cengage Learning. All Rights […]

978-1133939283 Chapter 9 Solution Manual Part 1

DQ1. period to period, especially in the absence of changes in credit policies or economic cial flexibility (cash flows). RECEIVABLES Discussion Questions CHAPTER 9―Solutions Accrual accounting and valuation are violated by the direct charge-off method be- 9-1 © 2014 Cengage […]

978-1133939283 Chapter 9 Lecture Note

Chapter 9 Receivables Learning Objectives 1. Dene receivables, and explain the allowance method for valuation of receivables as an application of accrual accounting. 2. Apply the allowance method of accounting for uncollectible accounts. 3. Make common calculations for notes receivable. […]

978-1133939283 Chapter 8 Solution Manual Part 3

1. (the receiving clerk) are separated from recordkeeping (the accounting with the existing assets at reasonable intervals. The comparison of the cash regis- compared with the invoices before payment is authorized. In addition, prior to pay- ment, the invoice should […]

978-1133939283 Chapter 8 Solution Manual Part 2

1. 2. Periodic independent verification The accountant compares the inventory transfer transfer sheets, all of which are prenumbered and accounted for. onstrate knowledge of control procedures. Physical controls The warehouse is secured and access is limited to authorized Sound personnel […]

978-1133939283 Chapter 8 Solution Manual Part 1

DQ1. independently. greater risk of human error in recording the large number of transactions involved and because there is a greater risk of theft. CHAPTER 8—Solutions with GAAP and that the company’s assets are protected. A system of internal control […]

978-1133939283 Chapter 8 Lecture Note

Chapter 8 Cash and Internal Control Learning Objectives 1. Describe the components of internal control, control activities, and limitations on internal control. 2. Apply internal control activities to common merchandising transactions. 3. Dene cash equivalents, and explain methods of controlling […]

978-1133939283 Chapter 7 Solution Manual Part 5

Units Cost Amount 10 60 49 100 52 $ 8,140 19 (60) 49 (30) 52 (4,500) 31 70 52 $ 3,640 4120 53 6,360 Ending inventory Purchase Apr. 47052 120 53 $ 10,000 15 50 54 2,700 Purchase 15 70 […]

978-1133939283 Chapter 7 Solution Manual Part 4

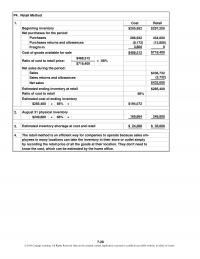

1. Cost Retail 2. $249,800 × 68% = 169,864 249,800 3. $ 24,208 $ 35,600 Estimated inventory shortage at cost and retail 4. The retail method is an efficient way for companies to operate because sales em- ployees in many […]

978-1133939283 Chapter 7 Solution Manual Part 3

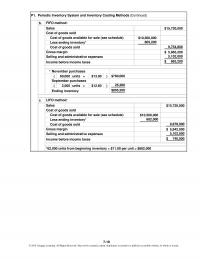

b. * ( 60,000 units × $13.00 ) ( 2,000 units × $12.60 ) September purchases $780,000 25,200 c. $15,720,000 $10,560,000 682,000 9,878,000 $ 5,842,000 5,102,000 $ 740,000 Cost of goods available for sale (see schedule) Less ending inventory* Cost […]

978-1133939283 Chapter 7 Solution Manual Part 2

2. FIFO LIFO Method Method E5A. Effects of Inventory Costing Methods on Cash Flows (Concluded) The results under the FIFO method are the same with or without the purchase, but Sales cause the ending inventory is below the beginning inventory […]

978-1133939283 Chapter 7 Solution Manual Part 1

DQ1. DQ7. For one thing, the value put on inventory has a direct dollar-for-dollar effect on net tory than a smaller inventory. In addition to storage and insurance costs, there is income. For another, it is relatively easy to falsify […]

978-1133939283 Chapter 7 Lecture Note

Chapter 7 Inventory Learning Objectives 1. Explain the concepts underlying inventory accounting. 2. Calculate inventory cost under the periodic inventory system using various costing methods. 3. Explain the eects of inventory costing methods on income determination and income taxes. 4. […]

978-1133939283 Chapter 6 Solution Manual Supplement- Solutions Part 2

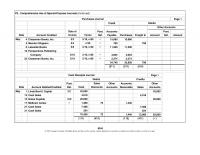

Page 1 Credit Post. Accounts Post. Account Credited Ref. Payable Purchases Freight In Account Ref. Amount 19 Perspectives Publishing Company 4,604 4,604 23 Chassman Books, Inc. 2,374 2,374 34,748 33,958 790 5/19 5/18 5/10, n/60 5/10, n/60 (211) (511) (514) […]

978-1133939283 Chapter 6 Solution Manual Supplement- Solutions Part 1

Page 1 Account Post. Sales Other Accounts Other Debited/Credited Ref. Cash Discounts Accounts Receivable Sales Accounts Nov. 4 J. Walker 980 20 1,000 9 Truck/Fred Kimball, Capital 10,000 14,000 24,000 14 Sales 2,834 2,834 17 P. Sivula 120 120 18 […]

978-1133939283 Chapter 6 Solution Manual Part 4

18 400 18 240 240 Cost of Goods Sold 24 6,400 6,400 Cash 25 3,800 3,800 Accounts Receivable 2. are equivalent. Net sales reflects gross sales adjusted for any sales discounts, sales returns, or allow- ances granted the buyer. When […]

978-1133939283 Chapter 6 Solution Manual Part 3

1. $433,912 $ 81,222 $221,185 30,238 $190,947 10,078 Freight-in Purchases Less purchases returns and allowances Net purchases 201,025 $282,247 76,664 205,583 $217,079 Gross margin Cost of goods sold Cost of goods available for sale Less merchandise inventory, March 31, 2014 […]

978-1133939283 Chapter 6 Solution Manual Part 2

400 g. 5,200 g. 5,200 d. 5,200 Bal. 670 h. 1,800 h. 1,800 Bal.** 12,270 13,000 13,000 d. 5,000 2,800 f. f. c. 5,000 * Bal. — 5,000 e. 1,000 2,800 4,800 12,600 1,000 11,600 c. Bal. d. * ** […]

978-1133939283 Chapter 6 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ4. DQ7. balance if merchandise has been lost or stolen. dise would belong to you when it left the shipper and would be your loss. You would want the terms to be FOB destination because the loss […]

978-1133939283 Chapter 6 Lecture Note Part 2

Teaching Strategy To help students understand the merchandising or manufacturing company’s multistep income statement, you may want to reproduce Exhibit 2 and explain it line by line. Exhibit 1 is helpful in understanding the cost of goods sold computation. Explain […]

978-1133939283 Chapter 6 Lecture Note Part 1

Chapter 6 Accounting for Merchandising Operations Learning Objectives 1. Dene merchandising accounting, and dierentiate perpetual from periodic inventory systems. 2. Describe the features of multistep and single-step classied income statements. 3. Describe the terms of sale related to merchandising transactions. […]

978-1133939283 Chapter 5 Solution Manual Part 4

Cases of net income. The auditors may become concerned if the loss is greater in the future or if management does not take action to try to reduce it. decisions of users of financial statements. The $120,000 inventory loss represents […]

978-1133939283 Chapter 5 Solution Manual Part 3

3. cause it is a good indicator of a company’s ability to pay its bills and to repay outstanding loans. The other measure, the debt to equity ratio, shows the pro- portion of the company financed by creditors in comparison […]

978-1133939283 Chapter 5 Solution Manual Part 2

Current A sset s Current Liabilities Working Ca p ital Current Ratio $ 85,000 $25,000 $60,000 3.40 100,000 45,000 55,000 2.22 $ 5,000 1.18 Net Income Sales Profit Margin Average Total Asset Assets Turnover Return on Assets A verage Owner’s […]

978-1133939283 Chapter 5 Solution Manual Part 1

DQ1. DQ2. DQ3. DQ7. tions or the economy may make financial information incomparable from year to The statement is false because neither measure is better than the other. However, presenting the financial information. It does not apply to the conditions […]

978-1133939283 Chapter 5 Lecture Note

Chapter 5 Foundations of Financial Reporting and the Classied Balance Sheet Learning Objectives 1. Describe the objective of nancial reporting, and identify the conceptual framework underlying accounting information. 2. Identify and dene the basic components of nancial reporting, and prepare […]

978-1133939283 Chapter 4 Solution Manual Part 8

Ref. Debit Credit Debit Credit 30 J3 5,500 5,500 30 J3 3,576 1,924 Ref. Debit Credit Debit Credit 15 J1 1,600 1,600 30 J2 3,900 5,500 30 J3 5,500 — 15 J4 3,656 3,656 31 J4 3,268 6,924 31 J5 […]

978-1133939283 Chapter 4 Solution Manual Part 7

Page 3 Post. Ref. Debit Credit 2014 30 411 5,500 30 314 3,576 511 1,700 512 240 513 160 514 1,196 515 280 30 314 1,924 311 1,924 Depreciation Expense—Repair Equipment B. Lutz, Capital Income Summary To close the expense […]

978-1133939283 Chapter 4 Solution Manual Part 6

31 29,240 31 23,900 11,360 2,700 1,160 760 5,840 640 1,440 Supplies Expense Insurance Expense Rent Expense Wages Expense Gas, Oil, and Other Truck Expenses Depreciation Expense—Painting Equipment Depreciation Expense—Truck 31 5,340 5,340 G. Ranke, Capital 31 4,000 4,000 G. […]

978-1133939283 Chapter 4 Solution Manual Part 5

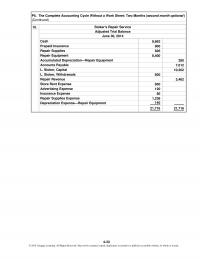

10. 8,662 800 P5. The Complete Accounting Cycle Without a Work Sheet: Two Months (second month optional) (Continued) Cash Prepaid Insurance Stoker’s Repair Service Adjusted Trial Balance June 30, 2014 4-33 © 2014 Cengage Learning. All Rights Reserved. May not […]

978-1133939283 Chapter 4 Solution Manual Part 4

4. 8,570 5. $2,750 $850 120 80 598 140 1,788 $ 962 Net income Repair supplies expense Depreciation expense—repair equipment Total expenses Insurance expense Store rent expense Advertising expense $0 10,000 962 $10,962 600 $10,362 Net income Subtotal Less withdrawals […]

978-1133939283 Chapter 4 Solution Manual Part 3

Debit Credit Debit Credit Debit Credit Debit Credit ( h ) 816 30,130 30,130 ( ) ( ) 13,270 1,430 1,430 ( ) 53,400 ( ) 14,400 67,800 67,800 30,900 ( ) 15,450 46,350 46,350 10,800 ( ) 9,396 9,396 […]

978-1133939283 Chapter 4 Solution Manual Part 2

2014 Dec. 31 12,810 31 7,915 4,055 600 2,130 458 672 Insurance Expense Wages Expense Rent Expense Supplies Expense Depreciation Expense—Repair Equipment 31 4,895 4,895 A. Winter, Capital 31 2,500 2,500 A. Winter, Withdrawals To close the expense accounts Income […]

978-1133939283 Chapter 4 Solution Manual Part 1

DQ1. DQ2. CHAPTER 4—Solutions COMPLETING THE ACCOUNTING CYCLE crual types of adjustments. When the accrual is resolved in the next accounting period through receipt or payment of cash, it is not necessary to know the amount accrued at the end […]

978-1133939283 Chapter 4 Lecture Note

Chapter 4 Completing the Accounting Cycle Learning Objectives 1. Describe the role of closing entries in the preparation of nancial statements. 2. Prepare closing entries. 3. Prepare reversing entries 4. Prepare a work sheet. 5. Explain the importance of the […]

978-1133939283 Chapter 3 Solution Manual Part 6

a. June 30 14,000 b. 30 13,860 13,860 (/5 ×3 = days $13,860 days ) Salaries Payable To record accrued salaries $23,100 c. d. 30 2,837 To record supplies used Supplies Expense No entry 2,837 Supplies +– = $2,846 $2,837 […]

978-1133939283 Chapter 3 Solution Manual Part 5

Ref. Debit Credit Debit Credit Ref. Debit Credit Debit Credit 30 35,000 30 J14 33,750 68,750 Adjustment Ref. Debit Credit Debit Credit 30 78,000 June Balance Ref. Debit Credit Debit Credit 30 42,000 30 J14 21,675 20,325 Adjustment Ref. Debit […]

978-1133939283 Chapter 3 Solution Manual Part 4

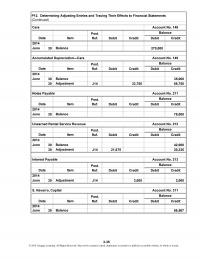

P8. Determining Adjusting Entries and Tracing Their Effects to Financial Statements 1. and 2. Prepaid InsuranceAccounts Receivable Cash 3-26 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly accessible website, in […]

978-1133939283 Chapter 3 Solution Manual Part 3

Ref. Debit Credit Debit Credit Ref. Debit Credit Debit Credit 30 428,498 30 J14 12,185 440,683 Adjustment Ref. Debit Credit Debit Credit 30 89,300 June Balance Ref. Debit Credit Debit Credit 30 206,360 June Balance Ref. Debit Credit Debit Credit […]

978-1133939283 Chapter 3 Solution Manual Part 2

$ 1,200 1,900 $ 1,100 9,750 $10,850 600 $10,250 Potential payments for wages during 2014 Less wages payable at end of 2014 Cash payments for wages during 2014 $ 2,100 4,450 $ 6,550 950 $ 5,600 Cash receipts from fees […]

978-1133939283 Chapter 3 Solution Manual Part 1

DQ1. DQ2. ● Discretionary expenditures can be timed to fall in a desired accounting ● Goods may be delivered or services performed before or after the end of the accrual accounting is to measure net income. Cash accounting is more […]

978-1133939283 Chapter 3 Lecture Note

Chapter 3 Adjusting the Accounts Learning Objectives 1. Dene net income and explain the concepts underlying income measurement. 2. Distinguish cash basis of accounting from accrual accounting, and explain how accrual accounting is accomplished. 3. Identify four situations that require […]

978-1133939283 Chapter 2 Solution Manual Part 5

Ref. Debit Credit Debit Credit 31 1,870 2 J17 270 1,600 Ref. Debit Credit Debit Credit 31 1,700 9 J17 1,200 500 10 J17 700 1,200 22 J18 500 700 Ref. Debit Credit Debit Credit 4 J17 85 85 Feb. […]

978-1133939283 Chapter 2 Solution Manual Part 4

Cash $44,120 = $57,880 + Accounting equation without Cash: 27,500 10,120 13,760 6,500 Equipment Utilities $57,880 $57,880 Accounting equation in balance: Supplies Wages Cash P6. T Accounts, Normal Balance, and the Accounting Equation Assets Cash Accounts Receivable Alternate Problems © […]

978-1133939283 Chapter 2 Solution Manual Part 3

f. 1,740 j. 1,080 e. 330 1,080 c. 190 Bal. 660 4,300 a. 3,600 h. 330 e. 330 480 g. 380 g. 860 4,780 Bal. 3,980 330 1,190 g. Bal. Bal. 860 a. 13,600 m. 300 f. 1,740 440 k. […]

978-1133939283 Chapter 2 Solution Manual Part 2

f. 400 c. 1,000 h. 1,200 1,000 g. 3,720 3,200 e. 900 600 3,800 b. 800 Rent Expense d. Bal. a. a. b. c. d. e. f. Billed customer for services rendered, $2,000. Purchased equipment on account, $2,250. Paid wages […]

978-1133939283 Chapter 2 Solution Manual Part 1

DQ1. DQ6. DQ7. The most common violation of the recognition concept is when a revenue is recog- penses. They appear on opposite sides of the accounting equation. nized before the earnings process is complete. For instance, the recording of an […]

978-1133939283 Chapter 2 Lecture Note Part 2

Teaching Strategy Students will wonder why the rules of debit and credit are as they are. Simply state they are an arbitrary set of rules whose careful interrelationships make them work. In addition, students need to dispel any preconceived notions […]