Archives

Appendix N 1 Per The Fas b All But The Following

A. the investee’s net income. B. any intercompany profits in inventory. C. the investee company’s dividends. D. the amortization of the excesses of the price over the book value of the investment. A. $363,000 B. $360,000 C. $355,500 D. $349,500 […]

Chapter 1 Critical Characteristic Derivative That The Instrument Derives

Module—Derivatives and Related Accounting Issues Key 1. Which of the following statements is true? 2. A critical characteristic of a derivative is that the instrument A. derives its value from a related asset or liability. B. derives its value from […]

Chapter 1 Economic Advantage Business Combination Includes Utilizing

Chapter 1—Business Combinations: New Rules for a Long– Standing Business Practice Key 1. An economic advantage of a business combination includes 2. One large Midwestern bank’s acquisition of another midwestern bank would be an example of a: A. market extension […]

Chapter 1 the fair values of pink coral’s net assets were as follows

38. On January 1, 20X1, Honey Bee Corporation purchased the net assets of Green Hornet Company for $1,500,000. On this date, a condensed balance sheet for Green Hornet showed: Book Fair Value Value Current Assets $ 500,000 $800,000 Long-Term Investments […]

Chapter 10 For Hedge Exposed Position Describe The

64. Rex Corporation, a U.S. firm with a calendar accounting year, agreed to buy a specially made truck from a Japanese firm for delivery on February 28, 20X2 with payment due on that date. On the same date the agreement […]

Chapter 10 June Reduce Exchange Risks Lion Purchased Contract

57. Lion Corporation, a U.S. firm, entered into several foreign currency transactions during the year. Determine the effect of each transaction on net income for that current accounting year only. Lion has a June 30 year end. Required: a. On […]

Chapter 10 When Economic Transaction Denominated Currency Other Than

Chapter 10—Foreign Currency Transactions Key 1. When an economic transaction is denominated in a currency other than the entity’s domestic currency, the entity must establish a 2. The best definition for direct quotes would be “direct quotes measure A. how […]

Chapter 11 foreign firms operating in highly inflationary economies received

58. Green Corporation, a wholly owned British subsidiary of a U.S. firm began the year with 1,300,000 British pounds in net assets. The subsidiary incurred a 65,000 British pound net loss for 20X1. The subsidiary issued common stock for 100,000 […]

Chapter 11 The Functional Currency Approach Adopted Fa sb Requires

Chapter 11—Translation of Foreign Financial Statements Key 1. The functional currency approach adopted by FASB 52 requires: 2. Exchange rates will not usually directly affect the cash flows of the parent entity in which of the following cases? A. The […]

Chapter 12 Consider The Following Case Income Loss

46. Millstone Company’s first-quarter 20X3, pretax income is $25,000. The company anticipates an annual tax credit of $5,500. Millstone is projecting income for the remaining three quarters of $95,000. For the second quarter of 20X4, Millstone reports $55,000 of pretax […]

Chapter 12 The Primary Emphasis Interim Reporting On Interim

Chapter 12—Interim Reporting and Disclosures about Segments of an Enterprise Key 1. The primary emphasis of interim reporting is on: 2. Which of the following best describes the proper accounting for interim financial reports? A. The interim period is viewed […]

Chapter 13 The Characteristic Partnership Where Specific Assets Contributed

A. a fiduciary relationship B. tenancy in partnership C. mutual agency D. the proprietary theory A. Partnership entities provide for taxes at the same rates used by corporations. B. In theory, partnerships are more able to attract capital. C. Like […]

Chapter 14 Changes Partnership Ownership Are Presumed Arms Length

Chapter 14—Partnerships: Ownership Changes and Liquidations Key 1. Changes in partnership ownership are presumed to be arm’s length transactions that may require which of the following actions? 2. The bonus method A. is conservative. B. follows a book-value approach. C. […]

Chapter 14 Richardson And George Have Been Partners

Book value of previous partnership 150,000 Patton’s contribution 50,000 Book value of new partnership 200,000 Patton’s share 30 % 60,000 Patton’s contribution 50,000 Bonus to Patton 10,000 Cash 30,000 Machinery 20,000 Capital, Lee (10,000 x 30%) 3,000 Capital, Alverez (10,000 […]

Chapter 15 following is a list of selected transactions for the city of

a. Estimated Revenues 450,000 Appropriations 392,000 Budgetary Fund Balance – Unassigned 58,000 To record budget. b. Encumbrances 15,000 Fund Balance – Assigned 15,000 To reinstate encumbrance. Expenditures 15,400 Vouchers Payable 15,400 To record voucher. Fund Balance – Assigned 15,000 Encumbrances […]

Chapter 15 Primary Distinction Between The Flow Resources Through

Chapter 15—Governmental Accounting: The General Fund and the Account Groups Key 1. A primary distinction between the flow of resources through a business enterprise and through a governmental entity is that operations in a governmental entity consume resources and assets […]

Chapter 16 The Following Are Selected Activities For

48. The following are selected activities for the Monterey City Natural Gas Company, a governmental entity: a. Billing for the year: To outside customers $400,000 To other Monterey City funds 70,000 b. Service provided to outside customers but not billed […]

Chapter 16 Which The Following Activities Would Not Accounted

Chapter 16—Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds Key 1. Which of the following activities would not be accounted for in a Special Revenue Fund? 2. In a Special Revenue fund: A. projects are permitted to expand […]

Chapter 17 The Gasb Statement No Reporting Model Includes

A. A budgetary comparison statement or schedule B. Management discussion and analysis C. pension related information D. information about the condition of infrastructure assets A. water utility enterprise B. chamber of commerce C. pension plan D. affiliated booster club A. […]

Chapter 18 Currently Which The Following Has Jurisdiction Over

Chapter 18—Accounting for Private Not-for-Profit Organizations Key 1. Which of the following is not a required characteristic of a private not-for-profit organization per the definition given by the AICPA? 2. Currently, which of the following has jurisdiction over accounting and […]

Chapter 18 the following events are for the public health agency

b. Cash 17,000 Special Events Support—Unrestricted 17,000 To record proceeds from rummage sales. Cost of Special Events 4,000 Cash 4,000 To record payment of direct costs. c. Cash 50,000 Legacies and Bequests—Unrestricted 50,000 To record legacy from Terry Well. d. […]

Chapter 19 elder care services reconciliation of excess of revenues over

a. Accounts Receivable 300,000 Patient Service Revenue 300,000 To record billings. Provision for Bad Debts 15,000 Contractual Adjustments 45,000 Allowance for Uncollectible Receivables and Third Party Contractual Adjustments 60,000 To record 5% allowance. b. Cash 62,000 Allowance for Uncollectible Receivables […]

Chapter 19 The Following Events Occurred Part Operations

66. The following events occurred as part of operations in Hard Knocks (private) University: a. To construct a new computer center, the University floated at par a $10,000,000 10% serial bond issued on January 1, paying interest December 31 and […]

Chapter 19 What The Basis Accounting Used Accounting For

Chapter 19—Accounting for Not-for-Profit Colleges and Universities and Health Care Organizations Key 1. With the adoption of GASB statement #35 in 1999, public colleges and universities are required to report their activities in a manner more like a(n): 2. What […]

Chapter 2 Investor Receives Dividends From Its Investee And

Chapter 2—Consolidated Statements: Date of Acquisition Key 1. An investor receives dividends from its investee and records those dividends as dividend income because: 2. An investor prepares a single set of financial statements which encompasses the financial results for both […]

Chapter 2 North Shore Railroad Operates Between Chicago

42. North Shore Railroad operates between Chicago and upper Michigan and Wisconsin. Dallas Ingold, purchasing manager of North Shore Railroad, anticipates the price of diesel fuel will increase over the next few months. On September 4th, Ingold purchased an out-of-the-money […]

Chapter 2 parent company purchased 80% of the common stock

35. On December 31, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $280,000. On this date, Subsidiary had total owners’ equity of $250,000 (common stock $20,000; other paid-in capital, $80,000; and retained earnings, $150,000). Any […]

Chapter 20 died and left the following stocks to his two sons

Estate of Trent Tyler Charge and Discharge Statement For the Period January 15 through January 31, 20X9 As to Principal I charge myself with: Assets per original inventory $485,400 Assets subsequently discovered 450 Gain of disposal of mortgage 6,000 Total […]

Chapter 20 Intestate Distribution Personal Property Distributed Under The

Chapter 20—Estates and Trusts: Their Nature and the Accountant’s Role Key 1. In an intestate distribution, personal property is distributed 2. An administrator of an estate differs from an executor of a will in that an administrator A. has fiduciary […]

Chapter 21 Fresh start Accounting Must Adopted Certain Debtors

36. Rockee Corporation, a bio-tech firm, has found itself in financial difficulty and may file for bankruptcy. Rockee’s Statement of Affairs reflects the following summary information: Book value of assets $700,000 Net realizable value of assets 370,000 Total liabilities 400,000 […]

Chapter 21 what is the amount of the gain on restructuring

Chapter 21—Debt Restructuring, Corporate Reorganizations, and Liquidations Key 1. Which of the following is an illustration of an action that can be taken to help a troubled firm without using the court system? 2. Land and buildings having a book […]

Chapter 3 The Method Accounting For Subsidiaries That Better

Chapter 3—Consolidated Statements: Subsequent to Acquisition Key 1. The method of accounting for subsidiaries that better reflects the investment account on parent-only financial statements is the 2. The method of accounting for subsidiaries that is required for influential investments is […]

Chapter 3 the only tangible assets of Subsidiary that were undervalued

28. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000, $120,000, and $190,000, respectively. Net income and […]

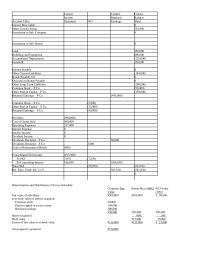

Chapter 4 depreciation is being computed using the straight-line

Consol. Control. Consol. Income Retained Balance Account Titles Statement NCI Earnings Sheet Inventory, December 31 172,000 Other Current Assets 683,000 Investment in Sub. Company 0 Other Long-Term Investments 80,000 Land 220,000 Buildings and Equipment 695,000 Accumulated Depreciation (314,000) Goodwill 150,000 […]

Chapter 4 Selected Information From The Separate And

Answer 4-2 Trial Balance Eliminations and Prange Seaman Adjustment s Account Titles Company Company Debit Debit Credit Inventory, December 31 100,000 105,000 (EI) 8,000 Other Current Assets 285,000 325,000 (IA) 20,000 Investment in Sub. Company 588,000 (CY) 48,000 (EL) 360,000 […]

Chapter 4 Which The Following Should Appear Consolidated Financial

Chapter 4—Intercompany Transactions: Merchandise, Plant Assets, and Notes Key 1. Which of the following should appear in consolidated financial statements? 2. Which of the following intercompany transactions would not require a worksheet elimination in the consolidation process? A. The subsidiary’s […]

Chapter 5 The Bonds Are Still Held December31 20x3on

Consol. Control. Consol. Income Retained Balance Account Titles Statement NCI Earnings Sheet Interest Receivable 0 Other Current Assets 554,900 Investment in Sub. Company 0 Investment in Sub. Bonds 0 Land 150,000 Buildings and Equipment 690,000 Accumulated Depreciation (220,000) Goodwill 150,000 […]

Chapter 5 the planes company owns 100% of the outstanding common

47. On January 1, 20X1 Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively. Any excess […]

Chapter 5 The Usual Impetus For Transactions That Create

Chapter 5—Intercompany Transactions: Bonds and Leases Key 1. The usual impetus for transactions that create a long-term debtor-creditor relationship between members of a consolidated group is due to the: 2. The motivation of a parent company to purchase the outstanding […]

Chapter 6 Plymouth Company holds a 90% interest in Savannah

40. Plymouth Company holds a 90% interest in Savannah, Inc., which was acquired in a previous year. As of the end of the current fiscal period, the following information is available: Plymouth Savannah Company Inc. Internally generated net income $80,000 […]

Chapter 6 The Cash Purchase Controlling Interest Firm Requires

Chapter 6—Cash Flow, EPS, and Taxation Key 1. The cash purchase of a controlling interest in a firm requires disclosure on the consolidated statement of cash flows as a(n) 2. Ponti Company purchased the net assets of the Sorri Company […]

Chapter 7 it is common for a parent firm to record its investment

36. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for $300,000. Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10 years. On […]

Chapter 7 January 20×1 Pepper Company Purchased 90 The

34. On January 1, 20X1, Pepper Company purchased 90% of the common stock of Salt Company for $360,000 when Salt had total shareholders’ equity as follows: 8% Preferred Stock, $100 par $100,000 Common Stock, $10 par 50,000 Other Paid-in Capital […]

Chapter 7 New Subsidiary Being Formed The Parent Company

Chapter 7—Special Issues in Accounting for an Investment in a Subsidiary Key 1. A new subsidiary is being formed. The parent company purchased 70% of the shares for $20 per share. The remaining shares were sold to a variety of […]

Chapter 8 current theoretical consolidation procedures used when

Purchase of treasury shares results in parent having a 75% interest. [12,000 x 60% = 7,200; 7,200 / (12,000 – 2,400) = 75%] For the worksheet solution, please refer to Answer 8-7. Answer 8-7 Parrot and Swallow Consolidated Partial Worksheet […]

Chapter 8 elimination entries for 12/31/x2 consolidation worksheet cy1

30. On 1/1/X1 Poncho acquired an 80% interest in Stroller for $560,000 when Stroller’s equity consisted of $530,000 paid-in capital and $100,000 Retained Earnings. Any excess of purchase price over was attributed to goodwill. On January 1, 20X6, Stroller had […]

Chapter 8 When The Parent Purchases Some Newly Issued

Chapter 8—Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares Key 1. A parent company owns a 100% interest in a subsidiary. Recently, the subsidiary paid a 10% stock dividend. The dividend should be recorded on the […]

Chapter 9 Us Company Purchases Medical Lab Equipment From

A. measurement B. denominated C. purchasing D. selling A. should record the sale for $9,600. B. is exposed to an economic loss on the transaction. C. has an economic gain on the transaction. D. should record the sale for 12,000 […]