40. Plymouth Company holds a 90% interest in Savannah, Inc., which was acquired in a previous year. As of

the end of the current fiscal period, the following information is available:

Plymouth

Savannah

Company

Inc.

Internally generated net income

$80,000

$60,000

Weighted average common shares outstanding

25,000

12,000

Warrants to acquire sub’s common stock:

Held by unaffiliated investors

2,000

Warrants to acquire parent’s common stock:

Held by Savannah

1,000

Held by unaffiliated investors

2,000

Preferred shares 5% convertible, par $100

1,000

Preferred shares 10% nonconvertible, par $2

5,000

Additional information:

·

The warrants to acquire Savannah stock were issued July 1 of the current year. Exercise price is $9; stock price is $12.

·

The warrants to acquire Plymouth stock were issued in a previous fiscal period. Exercise price is $12; stock price is $18.

·

Each share of convertible preferred can be converted into 5 shares of Savannah common stock. Plymouth owns 60% of the convertible

preferred stock.

Required:

Compute consolidated basic and diluted earnings per share for the current year. Ignore any tax effects.

SUBSIDIARY

CONSOLIDATED

inator

inator

Income

$ 60,000

$ 80,000

Weighted Average Shares

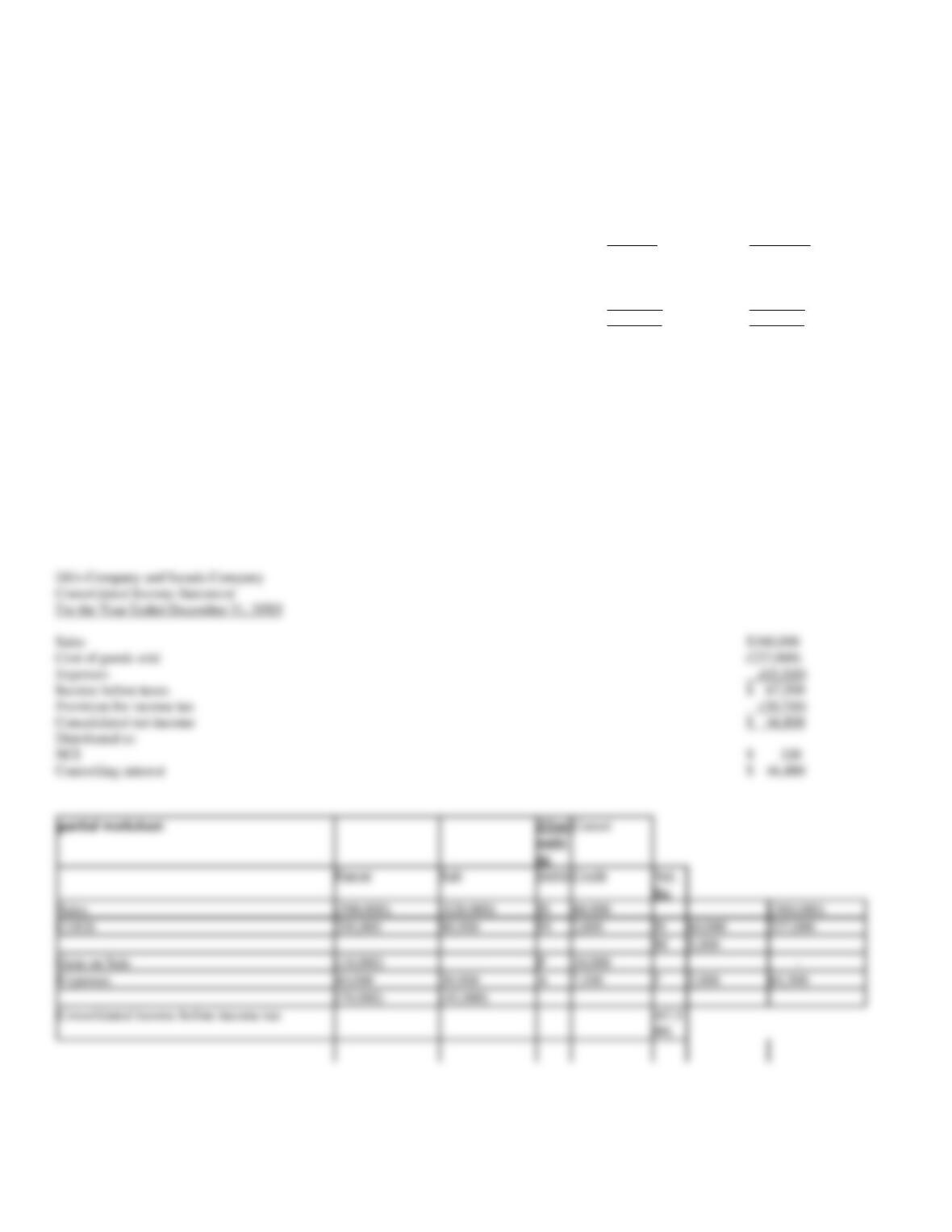

O/S

12,000

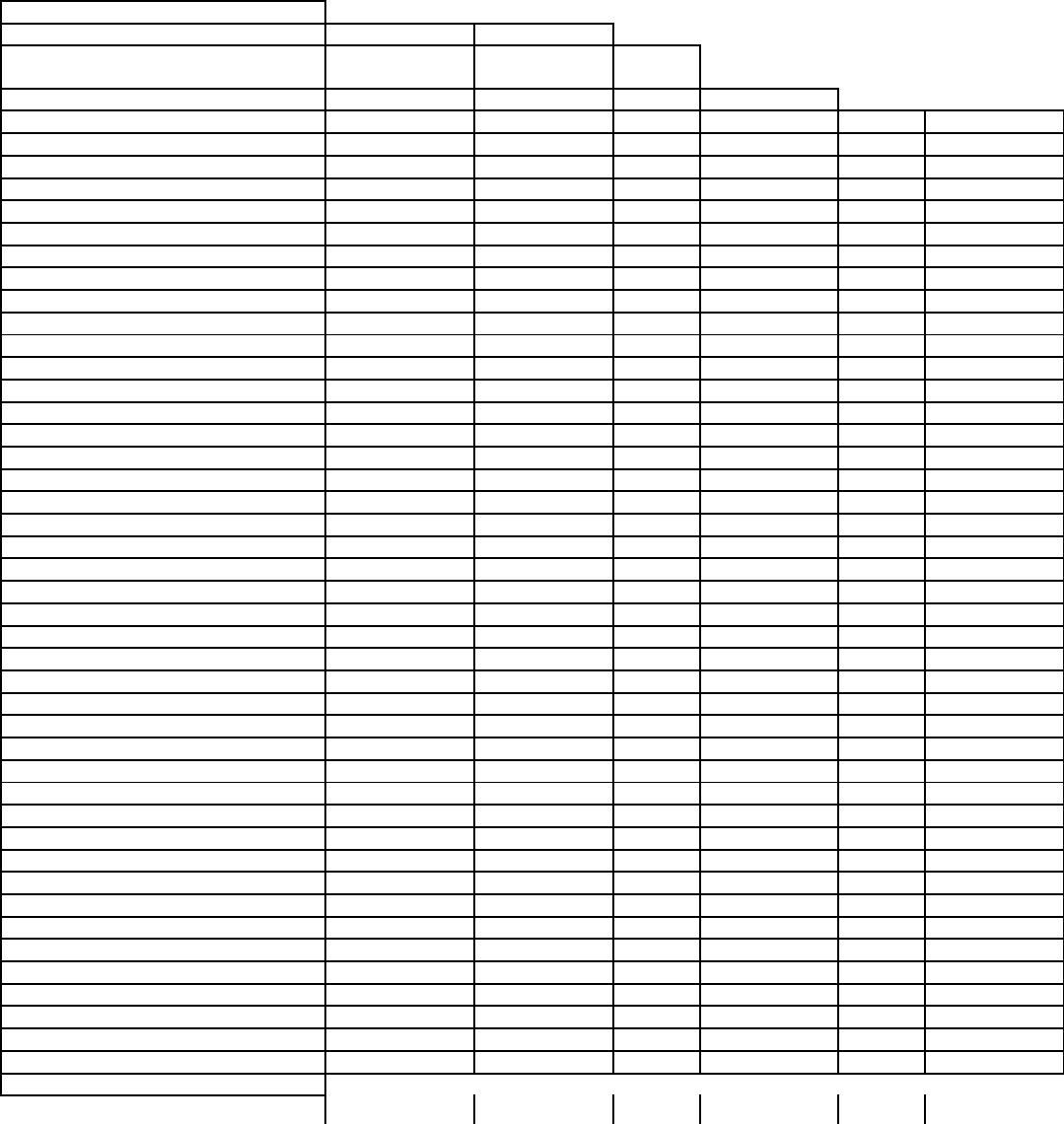

25,000

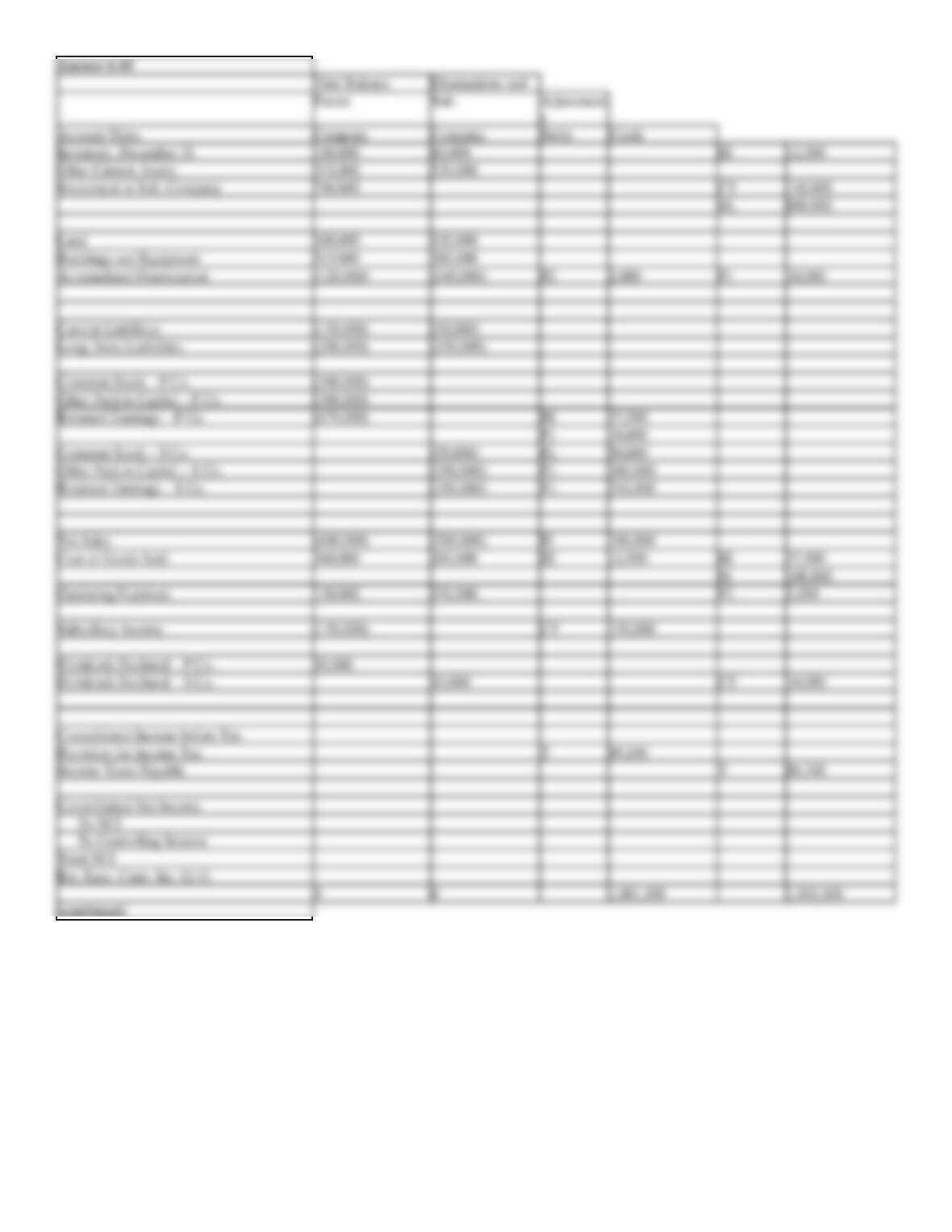

Preferred dividends

(5,000)

(1,000)

$ 55,000

12,000

[a]

49,464

$128,464

25,000

Internal BEPS numerator

$ 55,000

12,000

$ 79,000

25,000

Exercise of Sub Stock

250

Exercise of Par Stock

1,000

Convert preferred to common

5,000

5,000

$ 60,000

17,250

[c]

48,024

26,000

[a]

parent-owned equivalent sub shares ´

Sub BEPS = (12,000 ´ 90%) ´ $4.58

(10,800 + 3,000) ´ $3.48

41. Plymouth Company holds a 90% interest in Savannah, Inc., which was acquired in a previous year. As of

the end of the current fiscal period, the following information is available:

Plymouth

Savannah

Company

Inc.

Internally generated net income

$20,000

$7,000

Weighted average common shares outstanding

10,000

4,000

Subsidiary common stock warrants to

acquire 200 shares parent common stock

200

Dilutive convertible bonds:

Dilutive convertible bonds:

4,000

Parent common stock issued on conversion

2,500

Assume a 50% treasury stock method effect on the stock warrants

Required:

Compute consolidated basic and diluted earnings per share for the current year; ignore income taxes.

inator

inator

Income

$ 7,000

$ 20,000

$ 7,000

4,000

[a]

6,300

10,000

denominator

Conversion of bonds

4,000

2,500

$ 11,000

6,500

6,084

$ 26,084

10,100

42. Dills Company purchased an 80% interest in the common stock of Sarada Company for $140,000 on

January 1, 20X7. On this date the book value of Sarada’s net identifiable assets totaled $100,000. Any excess

was attributed to a patent with a 10-year life.

During 20X9, Dills Company and Sarada Company reported the following internally generated income before

taxes:

Dills Co.

Sarada Co.

Sales

$300,000

$120,000

Cost of goods sold

(200,000)

(90,000)

Gain on machine

10,000

—

Expenses

(40,000)

(20,000)

Income before taxes

$ 70,000

$ 10,000

Sarada Company routinely sells goods to Dills Company. This year those sales amounted to $60,000. Dills Company inventories included

intercompany goods of $30,000 at the beginning of the year and $12,000 at the end of the year. Sarada Company sells goods to Dills Company at a

gross profit of 16.67%.

On January 1, 20X9 Dills Company sold a new machine to Sarada Company, for $40,000. The cost of the machine was $30,000. It has a 5-year life.

The affiliated group files a consolidated tax return and is taxed at 30%.

Required:

Prepare a consolidated income statement for 20X9. Include income distribution for both firms.

Dills Company and Sarada Company

Consolidated Income Statement

For the Year Ended December 31, 20X9

Sales

$360,000

Cost of goods sold

(227,000)

Expenses

(65,500)

Income before taxes

$ 67,500

Provision for income tax

(20,700)

Consolidated net income

$ 46,800

Distributed to:

NCI

$ 320

Controlling interest

$ 46,480

Sales

(300,000)

(120,000)

60,000

(360,000)

COGS

200,000

90,000

2,000

60,000

227,000

5,000

Gain on Sale

(10,000)

F

10,000

–

Expenses

40,000

20,000

A

7,500

F

2,000

65,500

(70,000)

(10,000)

43. Dills Company purchased an 80% interest in the common stock of Sarada Company for $140,000 on

January 1, 20X7. On this date the book value of Sarada’s net identifiable assets totaled $100,000. Any excess

was attributed to a patent with a 10-year life.

During 20X9, Dills Company and Sarada Company reported the following internally generated income before

taxes:

Dills Co.

Sarada Co.

Sales

$300,000

$120,000

Cost of goods sold

(200,000)

(90,000)

Gain on machine

10,000

—

Expenses

(40,000)

(20,000)

Income before taxes

$ 70,000

$ 10,000

Sarada Company routinely sells goods to Dills Company. This year those sales amounted to $60,000. Dills Company inventories included

intercompany goods of $30,000 at the beginning of the year and $12,000 at the end of the year. Sarada Company sells goods to Dills Company at a

gross profit of 16.67%.

On January 1, 20X9 Dills Company sold a new machine to Sarada Company, for $40,000. The cost of the machine was $30,000. It has a 5-year life.

The firms file separate tax returns. Both are subject to a 30% tax rate. Dills Company receives an 80% dividend deduction.

Required:

Prepare a consolidated income statement for 20X9. Include income distribution for both firms.

Dills Company and Sarada Company

Consolidated Income Statement

For the Year Ended December 31, 20X9

Sales

$360,000

Cost of goods sold

(227,000)

Expenses

(65,500)

Income before taxes

$ 67,500

Provision for income tax

(20,885)

Consolidated net income

$ 46,615

Distributed to:

NCI

$ 320

Controlling interest

$ 46,295

Sales

(300,000)

(120,000)

60,000

(360,000)

COGS

200,000

90,000

2,000

60,000

227,000

5,000

Gain on Sale

(10,000)

F

10,000

–

Expenses

40,000

20,000

A

7,500

F

2,000

65,500

(70,000)

(10,000)

44. On January 1, 20X1, Parent Company acquired 100% of the common stock of Subsidiary Company in a

stock exchange. On this date Subsidiary had total owners’ equity of $550,000 and book value approximated fair

value.

During 20X1 and 20X2, Parent has accounted for its investment in Subsidiary using the simple equity method.

On January 1, 20X2, Parent held merchandise acquired from Subsidiary for $75,000. During 20X2, Subsidiary

sold merchandise to Parent for $100,000, of which $25,000 is held by Parent on December 31, 20X2.

Subsidiary’s usual gross profit on affiliated sales is 50%.

On December 31, 20X1, Parent sold to Subsidiary some equipment with a cost of $75,000 and a book value of

$30,000. The sales price was $40,000. Subsidiary is depreciating the equipment over a 5-year life, assuming no

salvage value and using the straight-line method.

Parent and Subsidiary qualify as an affiliated group for tax purposes and thus will file a consolidated tax return.

Assume a 30% corporate income tax rate.

Required:

Complete the Figure 6-10 worksheet for consolidated financial statements for the year ended December 31,

20X2.

Figure 6-10

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

60,000

Other Current Assets

374,000

520,000

Investment in Sub. Company

740,000

Land

240,000

120,000

Buildings and Equipment

515,000

380,000

Accumulated Depreciation

(120,000)

(140,000)

Current Liabilities

(150,000)

(50,000)

Long-Term Liabilities

(200,000)

(150,000)

Common Stock – P Co.

(300,000)

Other Paid-in Capital – P Co.

(300,000)

Retained Earnings – P Co.

(679,000)

Common Stock – S Co.

(50,000)

Other Paid-in Capital – S Co.

(200,000)

Retained Earnings – S Co.

(350,000)

Net Sales

(600,000)

(500,000)

Cost of Goods Sold

360,000

200,000

Operating Expenses

120,000

150,000

Subsidiary Income

(150,000)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

10,000

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Land

Buildings and Equipment

Accumulated Depreciation

Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Subsidiary Income

Dividends Declared – P Co.

Dividends Declared – S Co.

For the worksheet solution, please refer to Answer 6-10.

45. On January 1, 20X8, Paul Company purchased 80% of the common stock of Smith Company for $300,000.

On this date Smith had total owners’ equity of $350,000. Any excess of cost over book value is attributed to a

patent, to be amortized over 10 years.

During 20X8, Paul has accounted for its investment in Smith using the simple equity method.

During 20X8, Paul sold merchandise to Smith for $50,000, of which $10,000 is held by Smith on December 31,

20X8. Paul’s gross profit on sales is 40%.

During 20X8, Smith sold some land to Paul at a gain of $10,000. Paul still holds the land at year end.

Paul and Smith qualify as an affiliated group for tax purposes and thus will file a consolidated tax return.

Assume a 30% corporate income tax rate.

Required:

Complete the Figure 6-11 worksheet for consolidated financial statements for the year ended December 31,

20X8.

Figure 6-11

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

50,000

Other Current Assets

168,000

250,000

Invest in Smith Company

348,000

Land

240,000

100,000

Buildings and Equipment

300,000

200,000

Accumulated Depreciation

(80,000)

(60,000)

Current Liabilities

(150,000)

(30,000)

Long-Term Liabilities

(200,000)

(100,000)

Common Stock – P Co.

(100,000)

Other Paid-in Capital – P Co.

(180,000)

Retained Earnings – P Co.

(320,000)

Common Stock – S Co.

(100,000)

Other Paid-in Capital – S Co.

(100,000)

Retained Earnings – S Co.

(150,000)

Net Sales

(500,000)

(300,000)

Cost of Goods Sold

300,000

160,000

Operating Expenses

100,000

80,000

Subsidiary Income

(56,000)

Gain on Sale of Land

(10,000)

Dividends Declared – P Co.

30,000

Dividends Declared – S Co.

10,000

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Invest in Smith Company

Land

Buildings and Equipment

Accumulated Depreciation

Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Subsidiary Income

Gain on Sale of Land

Dividends Declared – P Co.

Dividends Declared – S Co.

For the worksheet solution, please refer to Answer 6-11.

46. Discuss how the following items affecting shareholder equity are disclosed in a consolidated statement of

cash flows:

1) The acquisition of controlling interest by issuing shares of stock

2) The purchase of additional subsidiary shares from the noncontrolling interest

3) Subsidiary dividends