48. The following events are for the Public Health Agency, a voluntary health and welfare organization that

conducts two programs: public health research and public health education:

a.

The agency received a donation of capital stock with a market value of $200,000, with the stipulation that the income and principal may be

used only for additions to plant.

b.

An adjoining building and land were purchased at a cost of $600,000. A 10% cash down payment was made. A mortgage note for the

remainder was signed.

c.

Unused sterilizers with a cost of $15,000 and a book value of $5,000 were sold for $3,000 cash.

d.

New sterilizers costing $28,000 were purchased.

e.

A payment of $90,000 was made to cover semiannual mortgage interest of $20,000 and reduction of principal of $70,000.

f.

Annual depreciation of $180,000 was recorded.

g.

The directors approved the following percentages for allocating all expenses (but not losses):

Public health research program

30%

Public health education program

40%

Management and general services

10%

Fund-raising services

20%

Total

100%

Required:

Prepare the journal entries for the events.

49. The following events are for the Public Health Agency, a voluntary health and welfare organization that

conducts two programs: public health research and public health education:

a.

The agency received its first contribution, consisting of 1,000 shares of Parker House common stock valued at $60,000. The

stock was donated by Ron Wolf, a local financier, who specified that earnings from the permanent endowment would not be

subject to any restrictions.

b.

Dianne Stein, a widow who was a volunteer for the Public Health Agency, died. Her will established a cash endowment of

$200,000 and stipulated that gains on the sale of any investments purchased with these funds should increase the permanent

endowment. However, earnings should be used for the purchase of equipment. The cash was accepted under the terms in the

will.

c.

Investments were made from the Stein endowment fund. Utility bonds with a face value of $100,000 and a contract rate of

12% were purchased at par, plus $2,000 of accrued interest for 2 months on May 1, 20X7. The bonds mature in 40 months.

On the same date, $90,000 was invested in money market certificates yielding 7%.

d.

The following revenue was received on September 1, 20X7:

Dividends on the Parker House common stock

$3,000

Semiannual interest on the utility bonds

$6,000

e.

The Parker House common stock is sold at a net price of $67 per share on October 1, 20X7.

f.

The $67,000 proceeds from the sale of Parker House common stock were invested in 10% industrial bonds with a face

value of $70,000 and a market value of $67,000 on an interest payment date. The bonds mature in 60 months. This

transaction had the approval of Wolf, who recommended that only the cash flow be available for operations. The board

agreed that this was preferable.

g.

At year end, accrued interest for four months on the utility bonds was $4,000; accrued interest for three months on the

industrial bonds was $1,750 and amortization of the discount was $150. The interest on money market certificates was

accrued.

Required:

Prepare journal entries for the year ended December 31, 20X7:

50. The Elder Citizens Agency is a voluntary health and welfare organization. The following events occur:

a.

This year’s fund drive resulted in unrestricted pledges totaling $130,000. Pledges of $25,000 were received for a special hot meal program.

b.

Cash collected from pledges: unrestricted, $100,000; restricted, $18,000.

c.

A philanthropist, who is an attorney, contributed a painting valued at $4,000, which is to be auctioned off at a Thanksgiving supper

organized to raise funds for a legal assistance program for the elderly. The event was an unexpected success. The painting was sold for

$7,800. Additional gross cash revenues were $4,900. Direct costs paid were $1,700.

d.

The agency received $11,000 from the local division of United Way for general support.

e.

Salaries amounted to $70,000, payroll taxes were $6,000, and other employee benefits amounted to $10,000. Of these items, $5,000 is

unpaid.

f.

Arrangements have been made to have a local catering firm bring in a hot lunch. Senior citizens are charged $0.75 per meal. To date,

payments to the catering service are $2,300. Cash collections from the meal program service totaled $900.

g.

It is estimated that 10% of the remaining unrestricted pledges and 5% of the remaining restricted pledges will prove uncollectible.

h.

At the end of the previous year, $10,000 of the balance of the Unrestricted Net Assets had been designated for a special program for

handicapped elderly persons. The program was to be conducted during the current year if sufficient support could be generated. The idea

was abandoned this year for lack of interest. The governing board authorizes the reclassification of the amount as undesignated.

i.

The Elder Citizens Agency had budgeted $500 per month to rent space to conduct its general activities. A generous citizen permits the

agency to occupy equivalent space at a nominal fee of $100 per year. The annual fee is paid, and the appropriate expense for the year is

recorded.

Required:

Prepare journal entries to record the events.

51. The Community Drug Clinic is a voluntary health and welfare organization that conducts two programs:

drug abuse research and drug abuse education. An inexperienced accountant recorded the following entries:

a.

Pledges Receivable

200,000

Income

200,000

To record signed pledges received. Of the total,

20% must be used for a special local college

program. It is estimated that 5% of the

unrestricted pledges will prove uncollectible.

b.

Cash

100,000

Income

100,000

Received money from a successful business

person, formerly a drug addict. Amount must

be used to acquire a building for the clinic’s

program

c.

Building, etc

100,000

Cash

100,000

To record down payment on land,

building, and equipment with funds

received in step (b). A mortgage note

was signed for an additional $150,000.

d.

Cash

15,000

Income

15,000

To record amount received for general

operations from the will of the

former mayor, who died.

e.

Cash

120,000

Pledges Write-Off Expense

5,000

Pledges Receivable

125,000

To record collection of all pledges

for special college program (step a)

and partial collection and some

write-offs for remaining pledges.

f.

Equipment

20,000

Cash

20,000

To record purchase of equipment from

unrestricted funds.

g.

Operating Expenses

100,000

Cash

100,000

To record payment of expenses, 80% of

which are related to unrestricted activity

and the remainder to restricted.

h.

Depreciation Expense

4,000

Accumulated Depreciation

4,000

To record annual depreciation provision.

Required:

Omitting explanations, prepare the correct entries, including the entry to assign expenses to programs and services. Assume that the incorrect entries

of the previous accountant are reversed prior to your entries.

52. The Good Health Agency is a voluntary health and welfare organization that conducts two programs: public

health research and public health education. Activities for the year ended December 31, 20X2 were as follows:

a.

Public support for general activities consisted of the following:

Cash

$ 60,000

Gross pledges (20% are for the 20X3 fund drive)

295,000

Estimated uncollectible pledges

15,000

b.

During the year, several rummage sales were held to raise funds for general operations. Gross cash proceeds were

$17,000, with $4,000 of direct costs paid in cash.

c.

Terry Well, a former nurse, died. Her will provided $50,000 to be used as the board of directors saw fit.

d.

Investments in the permanently restricted fund increased in value $22,000. The donor had requested that

unrealized gains and losses remain with the original principal of the gift; however the dividends, which were

$13,000, are to be used for developing materials for educational programs.

e.

Income from certificate of deposits in permanently restricted net assets for the year totaled $11,800. Income is

unrestricted.

f.

A health club was formed by the agency. Its members could use various facilities of the agency. Cash received

from membership dues was $1,700.

g.

The following expenses were vouchered:

Salaries and related expenses

$171,900

Professional fees and expenses

75,600

Administrative expenses

35,000

Rent expense

19,700

Conference and meeting expenses

16,900

Printing and distribution expenses

34,200

Transportation expenses

17,700

Total

$371,000

h.

Len Duke, a member of the Board of Trustees, donated 1,000 shares of Bank Three stock on December 31. He

had purchased the shares for $25 each, but they were trading for $30 on December 31. The gift is permanently

restricted, but the income will be unrestricted.

i.

An analysis of the above expenses was prepared and showed the following allocations:

Programs:

Public health research

$118,300

Public health education *

140,800

Supporting Services:

Management and general

59,500

Fund-raising

52,400

Total

$371,000

* including materials meeting conditions of the endowment gift in d.

j.

Trish Dyer, CPA, performed the agency’s audit on a pro bono basis. The value of the audit was estimated to be $4,000, and was accrued

after the end of the year.

k.

The net assets at December 31, 20X1 were:

Unrestricted

$320,000

Temporarily restricted

104,000

Permanently restricted

575,000

Required:

Prepare a statement of activities for Good Health Agency for the year ended December 31, 20X2.

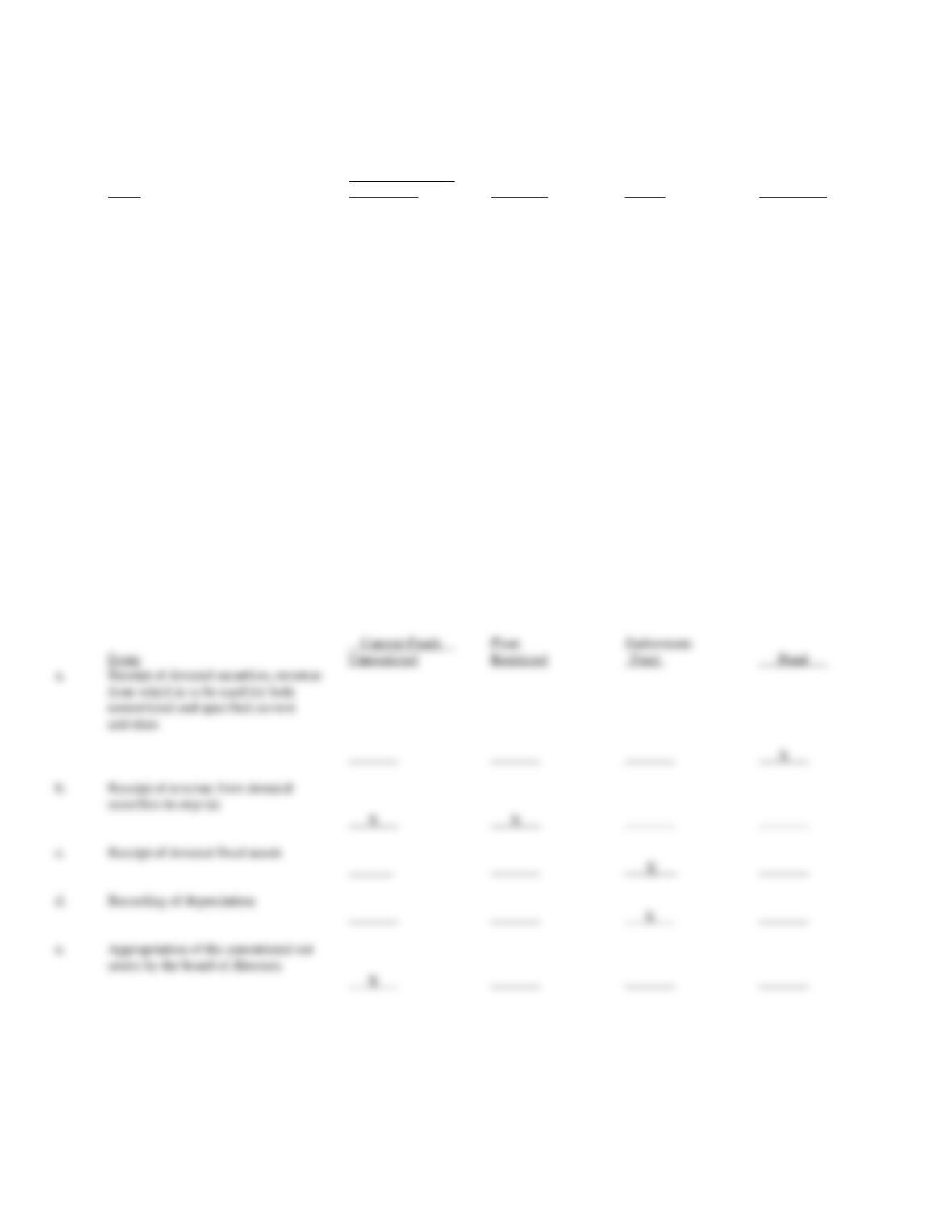

53. By placing a check mark in the appropriate column, indicate in which fund of a voluntary health and welfare

organization the following events normally would be recorded. (Note: An event may require entries in more

than one fund.)

Current Funds

Plant

Endowment

Event

Unrestricted

Restricted

Fund

Fund

a.

Receipt of donated securities, revenue

from which is to be used for both

unrestricted and specified current

activities

_______

_______

_______

_______

b.

Receipt of revenue from donated

securities in step (a)

_______

_______

_______

_______

c.

Receipt of donated fixed assets

_______

_______

_______

_______

d.

Recording of depreciation

_______

_______

_______

_______

e.

Appropriation of the unrestricted net

assets by the board of directors

_______

_______

_______

_______

Event

Unrestricted

Restricted

Fund

Fund

b.

Receipt of revenue from donated

securities in step (a)

X

X

_______

_______

c.

Receipt of donated fixed assets

_______

___X___

_______

d.

Recording of depreciation

Appropriation of the unrestricted net

assets by the board of directors

X

_______

_______

_______

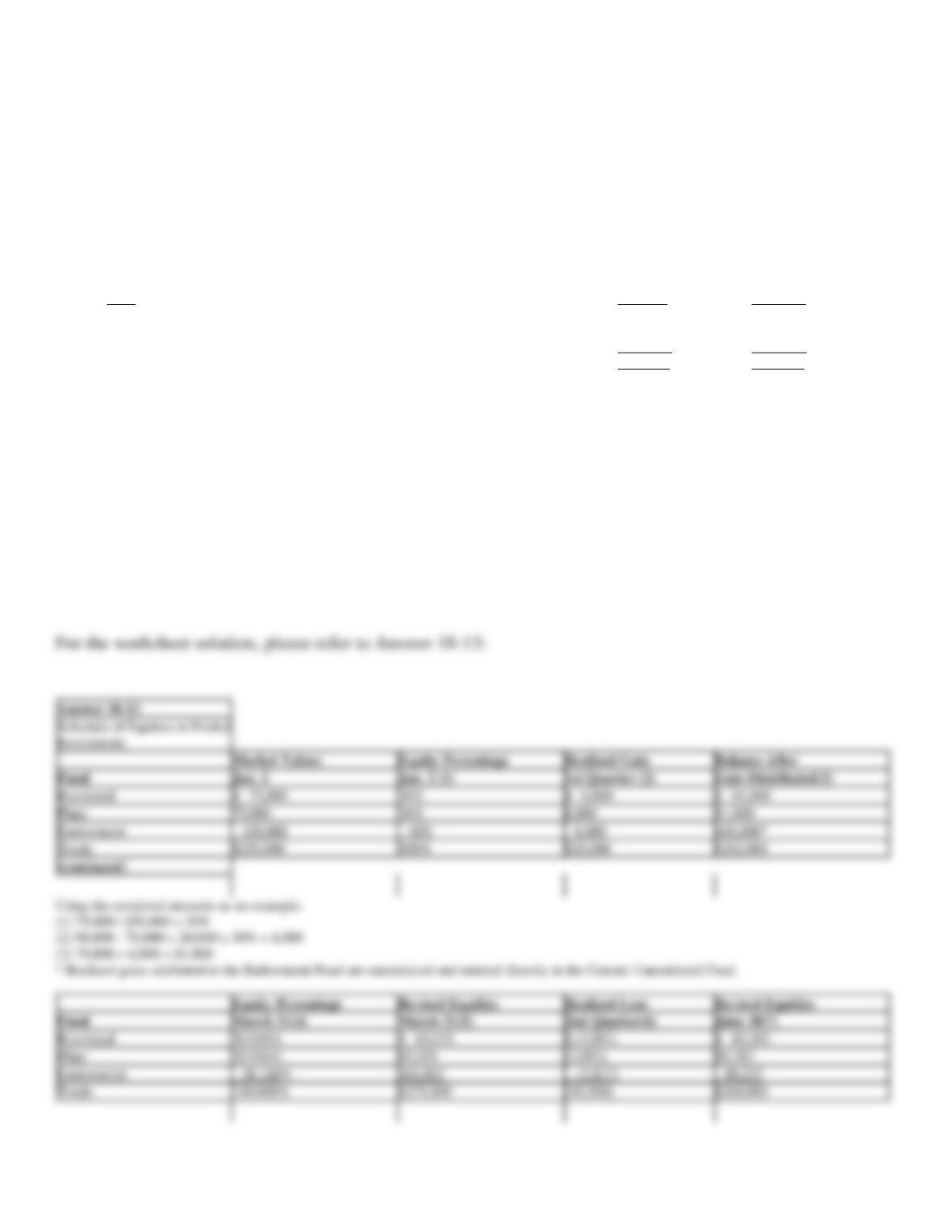

54. Senior Wellness Center is a voluntary health and welfare organization devoted to health education for the

elderly. It has investments in its Restricted Fund, its Plant Fund, and its Endowment Fund. There are no

restrictions on investment income or gains and losses in the endowment fund. On January 2, the organization

decided to pool the investments of the three funds, and thereafter to maintain all investment account balances at

market value.

a.

On January 2, when investments were pooled, the following data applied:

Investments

Market

Original

Values

Fund

Basis

January 2

Restricted

$ 55,000

$ 75,000

Plant

70,000

75,000

Endowment

125,000

100,000

Total

$250,000

$250,000

b.

On March 31, the end of the first quarter, the pool reports sales of investments carried at

$70,000 for $90,000. Realized gains and other realized income are allocated to funds upon

realization. Percentages of equity may be rounded to the nearest tenth of one percent. Total

cash and market value of pooled investments on March 31 is $275,000.

c.

The second-quarter report as of June 30 shows sales of investments for $90,000 which

were carried at $100,000. Total cash and market value of pooled investments on June 30 is

$260,000.

Required:

Prepare a schedule of equities in pooled investments for the three funds at the end of the first two quarters.

Schedule of Equities in Pooled

Restricted

$ 75,000

30%

$ 6,000

$ 81,000

Plant

75,000

30%

6,000

81,000

Endowment

100,000

40%

8,000

100,000*

Totals

$250,000

100%

$20,000

$262,000

Restricted

30.916%

$ 85,019

$ (3,092)

$ 80,382

Plant

30.916%

85,019

(3,092)

80,382

Endowment

38.168%

104,962

(3,817)

99,237

Totals

100.000%

$275,000

(10,000)

$260,000

55.

a.

Describe the basic accounting for private

not-for-profit groups promoted by the

FASB including a brief description of

the three net asset classes.

b.

Indicate in which of the net asset classes

the following transactions belong:

1.

Donor makes a cash gift to not-for profit which must be invested and maintained in perpetuity

2.

Income Earned on donation noted in item #1 is restricted to certain program expenditures

3.

Gains/Losses, both realized and unrealized, on donation noted in item #1. Not stipulated in donor

agreement or by the law

4.

Expenses paid out for programs stipulated in donor agreement relating to donation made in item

#1.

b.

1.

Permanently Restricted

2.

3.

Unrestricted

4.

56. Describe the circumstances that must be true in order for donated, personal services to be recorded as

revenue (contributions) in a not-for-profit organization.

57. How do you differentiate between a voluntary health and welfare organization and another not-for-profit

organization?

58. What are the two major categories of resources obtained by voluntary health and welfare organizations, and

how do they differ?