28. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000,

$120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as

follows:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

20,000

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used,

was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of

8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 20X1 and December 31, 20X2 assuming that Parent

records its investment in Subsidiary using

a. the cost method

b. the simple equity method

If date alignment entries are not required, give rationale.

Investment in Subsidiary

n/a

(1) 32,000

R/E-Parent

n/a

32,000

Dividend Income

(2) 8,000

(3) 16,000

Dividends Declared-Sub

8,000

16,000

12/31/X1

12/31/X2

Subsidiary Income

(4) 40,000

(5) 72,000

Investment in Subsidiary

40,000

72,000

Investment in Subsidiary

(2) 8,000

(3) 16,000

Dividends Declared-Sub

8,000

16,000

29. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000,

$120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as

follows:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

20,000

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used,

was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of

8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X1. Assume Parent uses the simple equity method of

accounting for its investment in Subsidiary.

CY1

Subsidiary Income ($50,000 x 80%)

40,000

Investment in Subsidiary

40,000

CY2

Investment in Subsidiary ($10,000 x 80%)

8,000

Dividends Declared-Subsidiary

8,000

Common stock-Sub ($40,000 x 80%)

32,000

Paid in capital in excess of par-Sub ($120,000 x 80%)

96,000

Retained earnings-Sub ($190,000 x 80%)

152,000

Investment in Subsidiary

280,000

D

Cost of Goods Sold

5,000

Building

15,000

Goodwill

25,000

Investment in Subsidiary ($45,000 x 80%)

36,000

Retained earnings-Sub (NCI) ($45,000 x 20%)

9,000

A

Depreciation expense ($15,000 / 8 years)

1,875

Accumulated depreciation-building

1,875

30. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000,

$120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as

follows:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

20,000

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used,

was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of

8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Prepare all necessary elimination entries for the consolidating worksheet of December 31, 20X2. Assume Parent uses the simple equity method of

accounting for its investment in Subsidiary.

CY1

Subsidiary Income ($90,000 x 80%)

72,000

Investment in Subsidiary

72,000

CY2

Investment in Subsidiary ($20,000 x 80%)

16,000

Dividends Declared-Sub

16,000

Common stock-Sub ($40,000 x 80%)

32,000

Paid in capital in excess of par-Sub ($120,000 x 80%)

96,000

Investment in Subsidiary

312,000

D

Retained earnings-Sub (20% inventory)

1,000

Retained earnings-Parent (80% inventory)

4,000

Building

15,000

Goodwill

25,000

Investment in Subsidiary

36,000

Retained earnings-Sub (NCI)

9,000

A

Depreciation Exp ($15,000 / 8 years)

1,875

Retained earnings-Sub

375

Retained earnings-Parent

1,500

Accumulated depreciation-building (2 yrs)

3,750

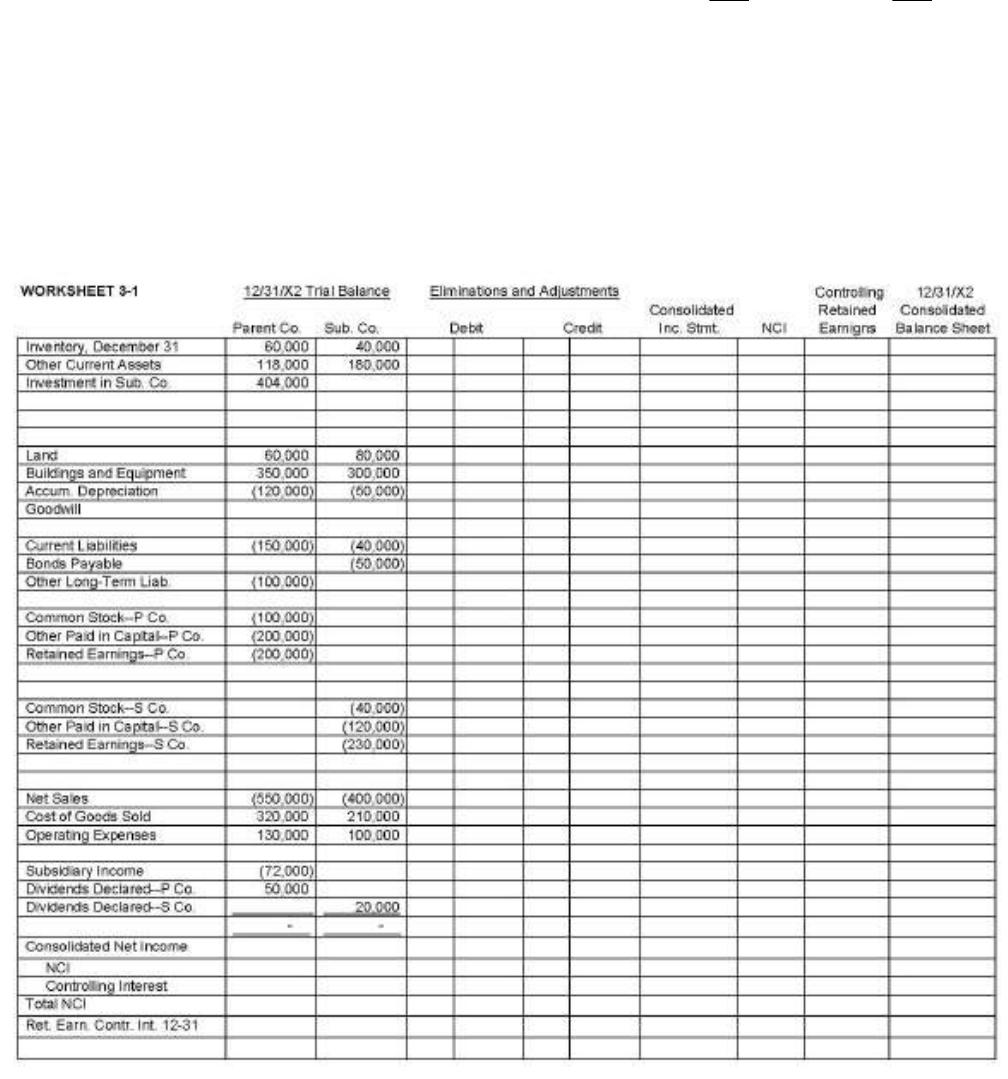

31. Refer to the information below and Worksheet 3-1.

On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$316,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $40,000,

$120,000, and $190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as

follows:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

20,000

On January 1, 20X1, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used,

was worth $5,000 more than cost. The inventory was sold in 20X1. Building, which was worth $15,000 more than book value, has a remaining life of

8 years, and straight-line depreciation is used. Any remaining excess is goodwill.

Required:

a. Complete the consolidating worksheet for December 31, 20X2.

b. Prepare supportive Income Distribution Schedules for Subsidiary and Parent.

32. The Paris Company purchased an 80% interest in Seine, Inc. for $600,000 on July 1, 20X1, when Seine had

the following balance sheet:

Assets

Accounts receivable

$ 50,000

Inventory

120,000

Land

80,000

Building

270,000

Equipment

80,000

Total

$600,000

Liabilities and Equity

Current liabilities

$100,000

Common stock, $5 par

50,000

Paid-in capital in excess of par

150,000

Retained earnings (July 1)

300,000

Total

$600,000

The inventory is understated by $20,000 and is sold in the third quarter of 20X1. The building has a fair value of $320,000 and a 10-year remaining

life. The equipment has a fair value of $120,000 and a remaining life of 5 years. Any remaining excess is attributed to goodwill.

From July 1 through December 31, 20X1, Seine had net income of $100,000 and paid $10,000 in dividends.

Assume that Paris uses the cost method to record its investment in Seine.

Required:

a.

Prepare a determination and distribution of excess schedule as of July 1, 20X1.

b.

Prepare the eliminations and adjustments that would be made on the December 31, 20X1, consolidated worksheet to eliminate the

investment in Seine. Distribute and amortize any excess.

Company Implied Fair Value

Parent Price

NCI Value

Fair value of subsidiary

$750,000

$600,000

$150,000

Less book value:

Common stock

50,000

Paid in capital in excess of par

150,000

Retained earnings

300,000

Total equity

500,000

500,000

500,000

Interest Acquired

80%

20%

Book value

400,000

100,000

Excess of fair over book

$250,000

$200,000

$ 50,000

Adjust identifiable accounts:

Life

Amort/Year

Inventory

$ 20,000

[sold in third quarter]

Building

50,000

10

5,000

Equipment

40,000

5

8,000

Goodwill

140,000

Total

$250,000

33. The determination and distribution schedule for the consolidation of Petoskey (80% interest) and Sable

reads in part:

Adjust identifiable accounts:

Life

Amort/Year

Inventory

$ 20,000

[sold in third quarter]

Building

50,000

10

5,000

Equipment

40,000

5

8,000

Goodwill

140,000

Total

$250,000

Prepare the elimination entries to distribute and amortize the excess purchase cost on

a. 1/1/X1, the date of acquisition

b. 12/31/X1, the end of the first year following the acquisition

c. 12/31/X3, the end of the third year following the acquisition.

D

Inventory

20,000

Building

50,000

Equipment

40,000

Goodwill

140,000

Investment in Subsidiary (80%)

200,000

Retained earnings-Sub (NCI) (20%)

50,000

D

Cost of Goods Sold

20,000

Building

50,000

Equipment

40,000

Goodwill

140,000

Investment in Subsidiary (80%)

200,000

Retained earnings-Sub (NCI) (20%)

50,000

A

Depreciation expense

5,000

Accumulated depreciation-Building

5,000

Depreciation expense

8,000

Accumulated depreciation-Equipment

8,000

D

Retained earnings-Parent (80% inventory)

16,000

Retained earnings-Sub (20% inventory)

4,000

Building

50,000

Equipment

40,000

Goodwill

140,000

Investment in Subsidiary (80%)

200,000

Retained earnings-Sub (NCI) (20%)

50,000

A

Depreciation expense

5,000

Depreciation expense

8,000

Retained earnings-Parent

20,800

Retained earnings-Sub (NCI)

5,200

Accumulated depreciation-Building (3 years)

15,000

Accumulated depreciation-Equipment (3 years)

24,000

34. Dickinson Corporation is considering the acquisition of Williston Company through the acquisition of

Williston’s common stock. Dickinson Corporation will issue 15,000 shares of its $5 par common stock, with a

fair value of $30 per share, in exchange for all 10,000 outstanding shares of Williston Company’s voting

common stock. The acquisition meets the criteria for a tax-free exchange as to the seller. Because of this,

Dickinson Corporation will be limited for future tax returns to the book value of the depreciable assets.

Dickinson Corporation falls into the 30% tax bracket. The appraisal of the assets of Williston Company shows

that the inventory has a fair value of $120,000, and the depreciable fixed assets have a fair value of $250,000

and a 10-year life. Any remaining excess is attributed to goodwill. Williston Company has the following

balance sheet just before the acquisition:

Williston Company

Balance Sheet

December 31, 20X1

Assets

Liabilities & Equities

Cash

$ 40,000

Current Liabilities

$ 50,000

Accounts Receivable

150,000

Bonds Payable

100,000

Inventory

100,000

Common Stock ($10 par)

100,000

Depreciable Assets

210,000

Retained Earnings

250,000

$500,000

$500,000

Required:

a.

Prepare a value analysis and a determination and distribution of excess schedule.

b.

Prepare the elimination entries that would be made on the consolidated worksheet on the date of acquisition.

Company Implied Fair Value

Parent Price

Implied entity fair value

$450,000

$450,000

Fair value of entity net identifiable assets [1]

392,000

392,000

Goodwill

$ 58,000

$ 58,000

[1] $350,000 + [($20,000 + $40,000) ´ (1 – 30%)]

Company Implied Fair Value

Parent Price

Fair value of subsidiary

$450,000

$450,000

Less book value:

Common Stock

100,000

Paid in capital in excess of par

–

Retained earnings

250,000

Total equity

350,000

350,000

Interest Acquired

100%

Book value

350,000

Excess of fair over book

$100,000

$100,000

Adjust identifiable accounts:

Life

Annual Amort

Inventory

$ 20,000

1

Deferred tax liability (20,000 x 30%)

(6,000)

1

Depreciable assets

40,000

10

4,000

Deferred tax liability (40,000 x 30%)

(12,000)

10

(1,200)

Goodwill

58,000

Total

$100,000

35. Discuss the merits of accounting for subsidiaries using the:

1) Simple equity method

2) Sophisticated equity method

3) Cost method.