33. Selected information from the separate and consolidated balance sheets and income statements of Palo Alto,

Inc. and its subsidiary, Stanford Co., as of December 31, 20X1, and for the year then ended is as follows:

Palo Alto

Stanford

Consolidated

Balance sheet accounts:

Accounts receivable

$ 26,000

$ 19,000

$ 42,000

Inventory

30,000

25,000

50,000

Investment in Stanford

67,000

—

—

Stockholders’ equity

154,000

50,000

154,000

Income statement accounts:

Revenues

$200,000

$140,000

$300,000

Cost of goods sold

150,000

110,000

225,000

Gross profit

50,000

30,000

75,000

Equity in earnings of Stanford

$ 9,000

—

—

Net income

$ 36,000

$ 20,000

$ 36,000

Additional information:

During 20X1, Palo Alto sold goods to Stanford at the same markup on cost that Palo Alto uses for all sales. At December 31, 20X1, Stanford had not

paid for all of these goods and still held 50% of them in inventory.

Palo Alto acquired its interest in Stanford five years earlier (as of December 31, 20X1).

Required:

For each of the following items, calculate the required amount.

a.

The amount of intercompany sales from Palo Alto to Stanford during 20X1.

b.

The amount of Stanford’s payable to Palo Alto for intercompany sales as of December 31, 20X1.

c.

In Palo Alto’s December 31, 20X1, consolidated balance sheet, the carrying amount of the inventory that Stanford purchased from Palo

Alto.

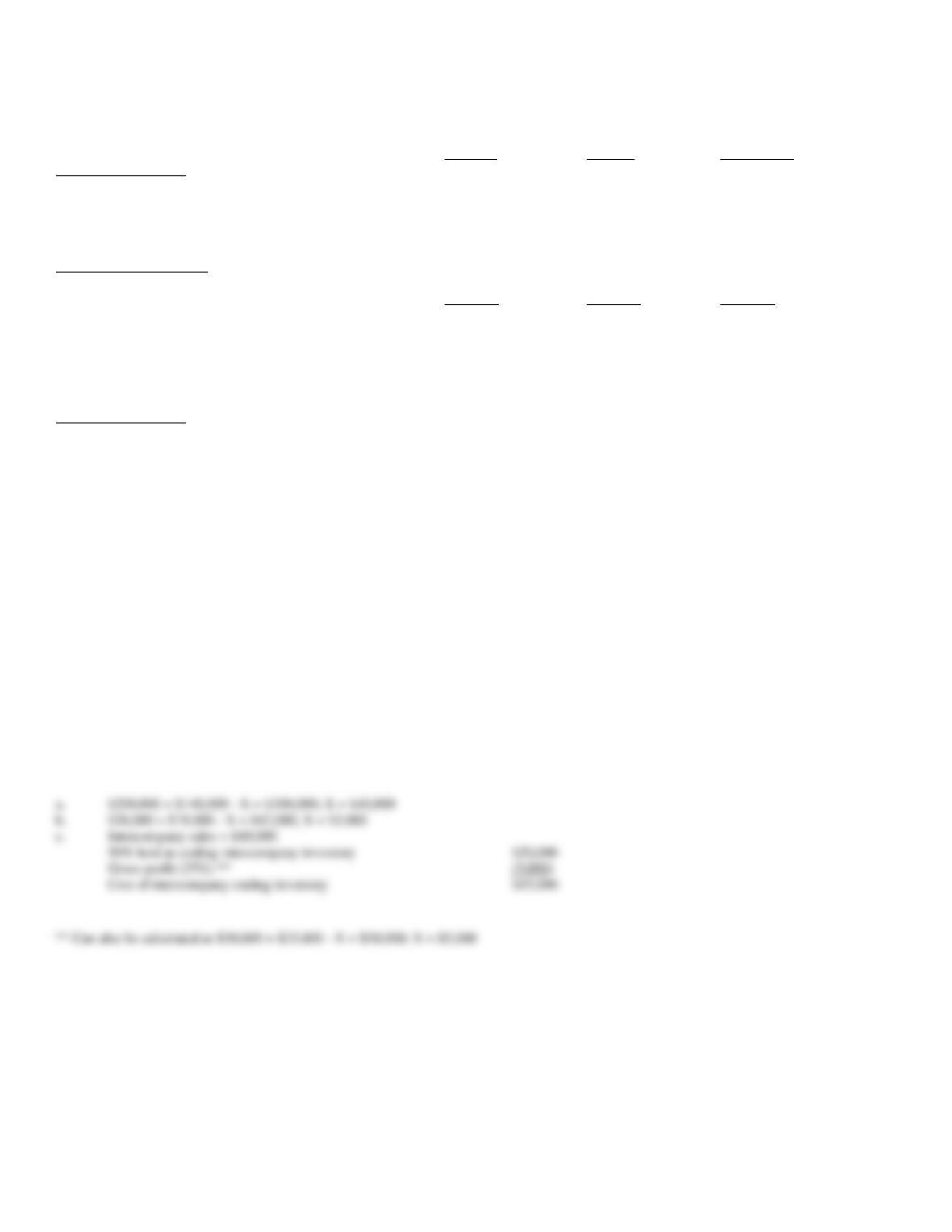

$200,000 + $140,000 – X = $300,000; X = $40,000

b.

$26,000 + $19,000 – X = $42,000; X = $3,000

Intercompany sales = $40,000

50% held as ending intercompany inventory

$20,000

Gross profit (25%) **

(5,000)

Cost of intercompany ending inventory

$15,000

34. On January 1, 20X1, Pinto Company purchased an 80% interest in Sands Inc. for $1,000,000. The equity

balances of Sands at the time of the purchase were as follows:

Common stock ($10 par)

$100,000

Paid-in capital in excess of par

400,000

Retained earnings

500,000

Any excess of cost over book value is attributable to goodwill.

No dividends were paid by either firm during 20X6. The following trial balances were prepared for Pinto Company and its subsidiary, Sands Inc., on

December 31, 20X6:

Pinto

Sands

Cash

120,000

70,000

Accounts receivable

240,000

197,000

Inventory

200,000

176,000

Land

600,000

180,000

Buildings and equipment

1,100,000

800,000

Accumulated depreciation

(180,000)

(120,000)

Investment in Sands

1,000,000

Accounts payable

(110,000)

(50,000)

Common stock, $10 par

(800,000)

(100,000)

Paid-in capital in excess of par

(660,000)

(400,000)

Retained earnings

(1,340,000)

(650,000)

Sales

(600,000)

(300,000)

Other income

(40,000)

(15,000)

Cost of goods sold

320,000

180,000

Other expenses

150,000

32,000

Total

–

–

Sands sold a machine to Pinto Company for $40,000 on January 1, 20X6. The machine cost Sands $50,000, and $25,000 of accumulated depreciation

had been recorded as of the sale date. The machine had a 5-year remaining life and no salvage value. Pinto Company is using straight-line

depreciation.

Since the purchase date, Pinto has sold merchandise for resale to Sands, Inc. at a mark-up on cost of 25%. Sales during 20X6 were $150,000. The

inventory of these goods held by Sands was $15,000 on January 1, 20X6, and $18,000 on December 31, 20X6.

Required:

Prepare a consolidated income statement for 20X6, including income distribution schedules to support your distribution of income to the

noncontrolling and controlling interest interests.

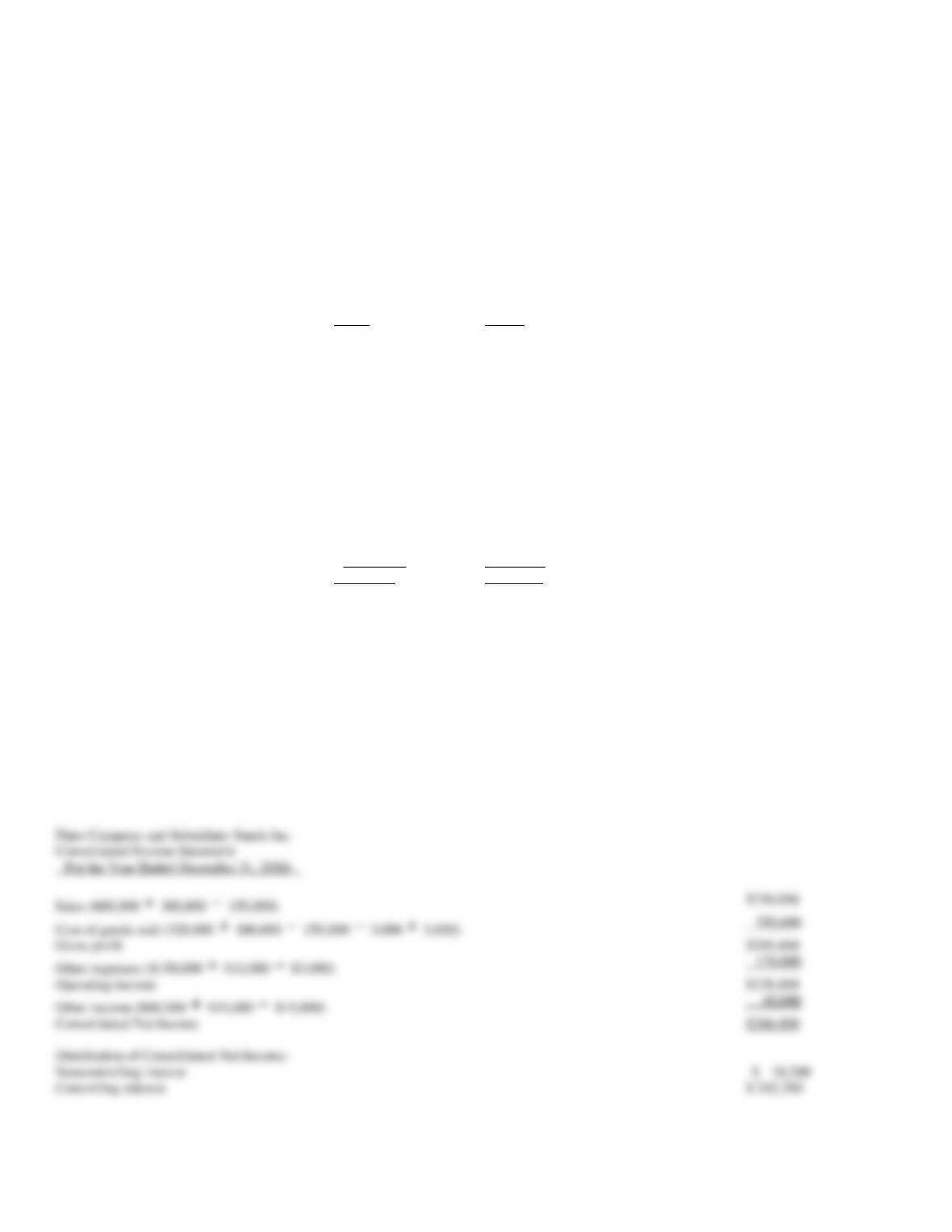

Pinto Company and Subsidiary Sands Inc.

Consolidated Income Statement

For the Year Ended December 31, 20X6

Sales (600,000 300,000 150,000)

Cost of goods sold (320,000 180,000 150,000 3,000 3,600)

Gross profit

$399,400

Other expenses ($150,000 $32,000 $3,000)

Operating income

$220,400

Other income ($40,000 $15,000 $15,000)

Consolidated Net Income

$260,400

Distribution of Consolidated Net Income:

35. On January 1, 20X1, Parent Company acquired 100% of the common stock of Subsidiary Company for

$750,000. On this date Subsidiary had total owners’ equity of $540,000.

Any excess of cost over book value is attributable to land, undervalued $10,000, and to goodwill.

During 20X1 and 20X2, Parent has appropriately accounted for its investment in Subsidiary using the simple

equity method.

On January 1, 20X2, Parent held merchandise acquired from Subsidiary for $10,000. During 20X2, Subsidiary

sold merchandise to Parent for $100,000, of which $20,000 is held by Parent on December 31, 20X2.

Subsidiary’s usual gross profit on affiliated sales is 40%.

On December 31, 20X2, Parent still owes Subsidiary $20,000 for merchandise acquired in December.

On January 1, 20X2, Parent sold to Subsidiary some equipment with a cost of $50,000 and a book value of

$20,000. The sales price was $40,000. Subsidiary is depreciating the equipment over a five-year life, assuming

no salvage value and using the straight-line method.

Required:

Prepare the worksheet eliminations that would be made on the 20X2 consolidated worksheet as a result of:

1) the intercompany sale of inventory

2) the intercompany sale of equipment

36. Power Company owns an 70% controlling interest in the Shelton Company. Shelton regularly sells

merchandise to Power, which then sells to outside parties. The gross profit on these sales is the same as sales to

outside parties. On January 1, 20X4, Power sold land and a building to Shelton. Twenty percent of the price

of the real estate was allocated to land and the remaining amount to structures. Additional information for the

companies for 20X4 is summarized as follows:

Power

Shelton

Sales

$2,250,000

$1,500,000

Cost of goods sold

1,850,000

1,050,000

Operating expenses

320,000

240,000

Internally generated net income

$860,000

$435,000

Intercompany merchandise sales

200,000

Intercompany inventory, end of year

50,000

Intercompany inventory, beginning of year

40,000

Book value of real estate sold

150,000

Sales price for real estate

220,000

Depreciable life of building

14 years

Prepare income distribution schedules for 20X4 for Power and Shelton as they would be prepared to distribute income to the noncontrolling and

controlling interests in support of consolidated worksheets.

Calculation of internally generated net income:

Power

Shelton

Sales

$2,250,000

$1,500,000

Cost of goods sold

1,850,000

1,050,000

Gross profit

400,000

450,000

Operating expenses

320,000

240,000

Gain on sale of assets ($220,000 – $150,000)

(70,000)

–

Net income

$ 150,000

$ 210,000

$450,000 / $1,500,000 = 30%

Beginning of year

End of year

Inventory on hand

40,000

50,000

Gross profit @ 30%

12,000

15,000

Gain on real estate

70,000

Portion attributable to buildings

80%

Portion of deferred gain to adjust depreciation

56,000

37. On January 1, 20X1, Parent Company acquired 100% of the common stock of Subsidiary Company for

$750,000. On this date Subsidiary had total owners’ equity of $540,000.

Any excess of cost over book value is attributable to land, undervalued $10,000, and to goodwill.

During 20X1 and 20X2, Parent has appropriately accounted for its investment in Subsidiary using the simple

equity method.

On January 1, 20X2, Parent held merchandise acquired from Subsidiary for $10,000. During 20X2, Subsidiary

sold merchandise to Parent for $100,000, of which $20,000 is held by Parent on December 31, 20X2.

Subsidiary’s usual gross profit on affiliated sales is 40%.

On December 31, 20X2, Parent still owes Subsidiary $20,000 for merchandise acquired in December.

On January 1, 20X2, Parent sold to Subsidiary some equipment with a cost of $50,000 and a book value of

$20,000. The sales price was $40,000. Subsidiary is depreciating the equipment over a five-year life, assuming

no salvage value and using the straight-line method.

Required:

Complete the Figure 4-3 worksheet for consolidated financial statements for the year ended December 31,

20X2.

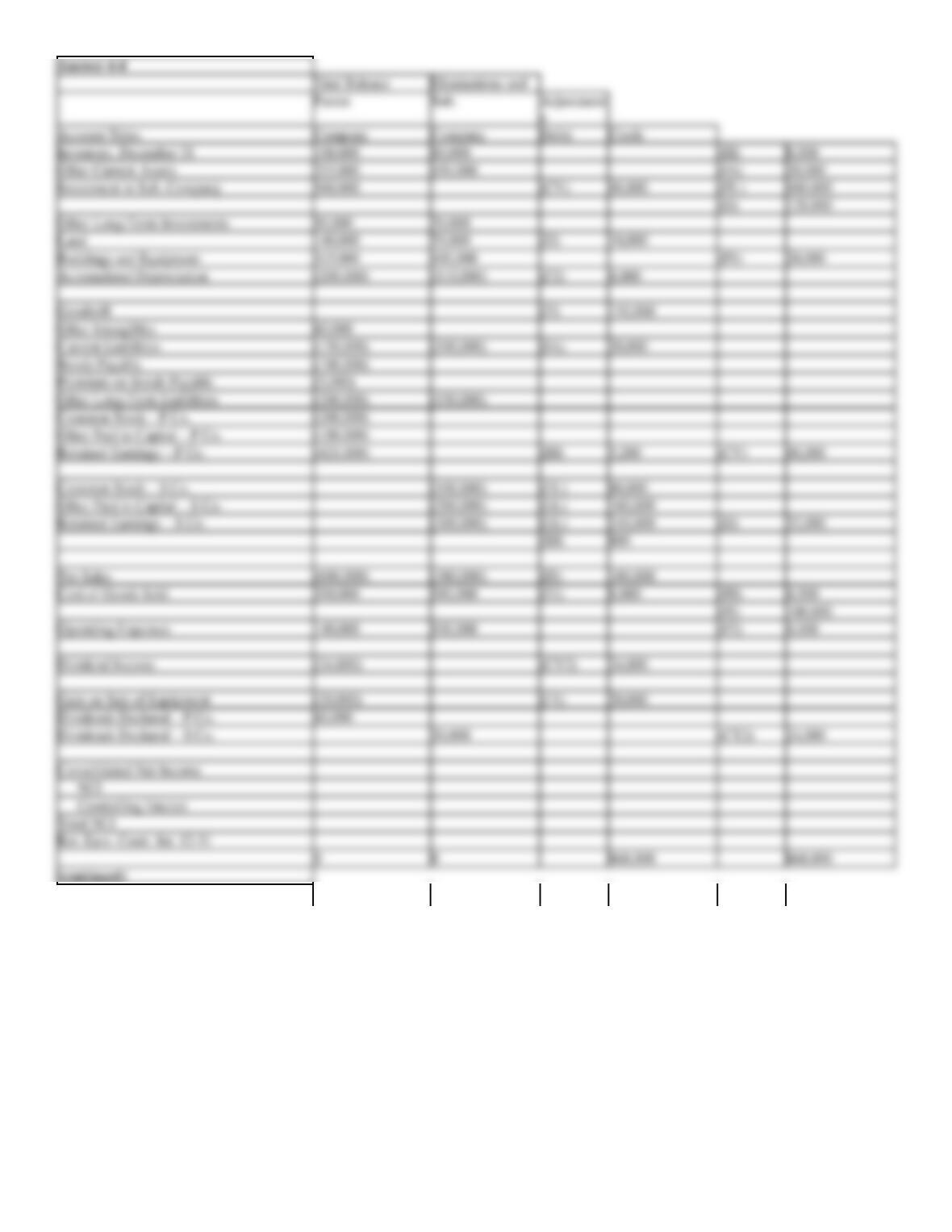

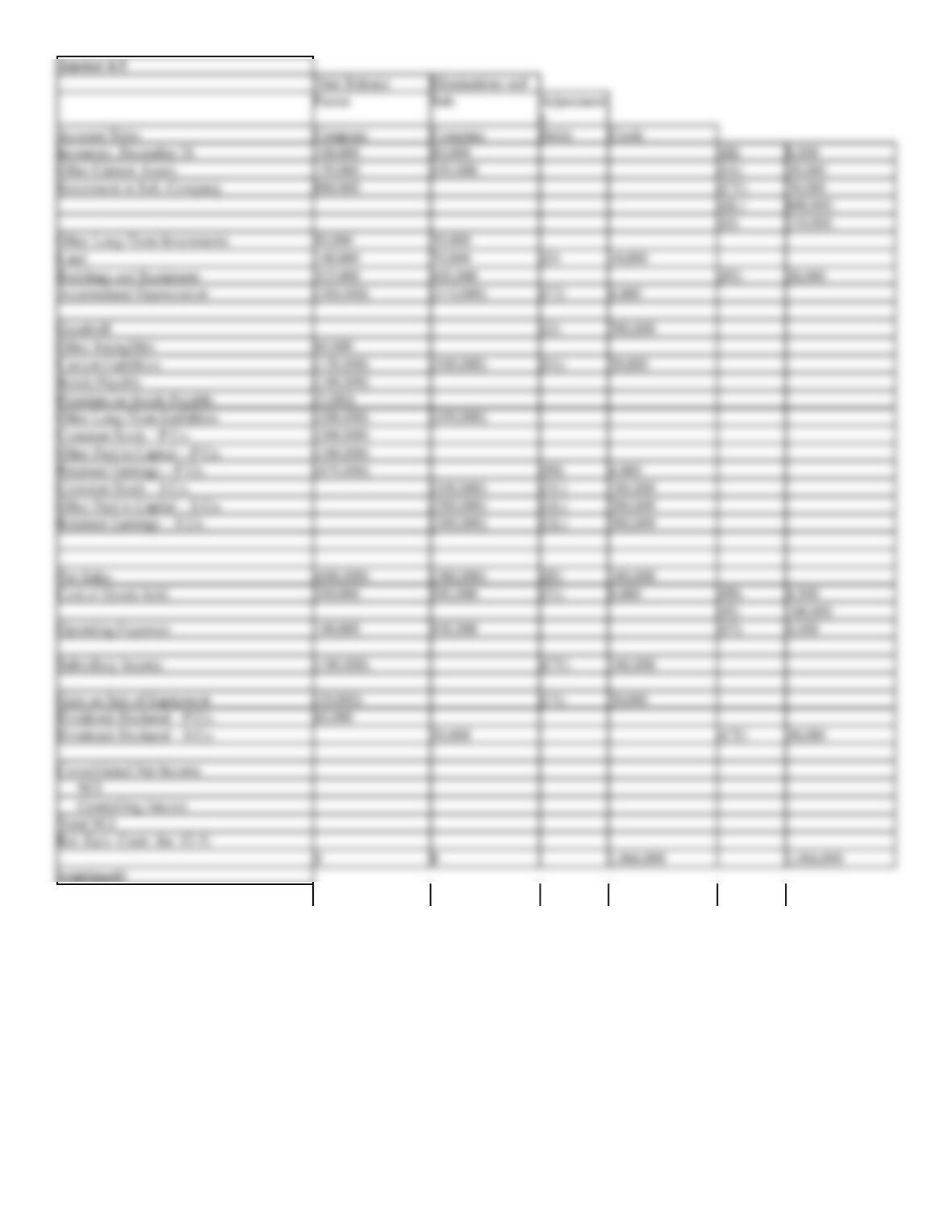

Figure 4-3

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

80,000

Other Current Assets

139,000

450,000

Investment in Sub. Company

880,000

Other Long-Term Investments

50,000

30,000

Land

140,000

70,000

Buildings and Equipment

315,000

400,000

Accumulated Depreciation

(280,000)

(110,000)

Other Intangibles

60,000

Current Liabilities

(150,000)

(100,000)

Bonds Payable

(100,000)

Premium on Bonds Payable

(5,000)

Other Long-Term Liabilities

(200,000)

(150,000)

Common Stock – P Co.

(200,000)

Other Paid in Capital – P Co.

(100,000)

Retained Earnings – P Co.

(479,000)

Common Stock – S Co.

(100,000)

Other Paid in Capital – S Co.

(200,000)

Retained Earnings – S Co.

(300,000)

Net Sales

(600,000)

(380,000)

Cost of Goods Sold

350,000

180,000

Operating Expenses

140,000

100,000

Subsidiary Income

(100,000)

Gain on Sale of Equipment

(20,000)

Dividends Declared – P Co.

60,000

Dividends Declared – S Co.

30,000

Consolidated Net Income

NCI

Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

(continued)

38. On January 1, 20X1, Parent Company acquired 80% of the common stock of Subsidiary Company for

$560,000. On this date Subsidiary had total owners’ equity of $540,000, including retained earnings of

$240,000. During 20X1, Subsidiary had net income of $60,000 and paid no dividends.

Any excess of cost over book value is attributable to land, undervalued $10,000, and to goodwill.

During 20X1 and 20X2, Parent has appropriately accounted for its investment in Subsidiary using the cost

method.

On January 1, 20X2, Parent held merchandise acquired from Subsidiary for $10,000. During 20X2, Subsidiary

sold merchandise to Parent for $100,000, of which $20,000 is held by Parent on December 31, 20X2.

Subsidiary’s usual gross profit on affiliated sales is 40%.

On December 31, 20X2, Parent still owes Subsidiary $20,000 for merchandise acquired in December.

On January 1, 20X2, Parent sold to Subsidiary some equipment with a cost of $50,000 and a book value of

$20,000. The sales price was $40,000. Subsidiary is depreciating the equipment over a five-year life, assuming

no salvage value and using the straight-line method.

Required:

Complete the Figure 4-4 worksheet for consolidated financial statements for the year ended December 31,

20X2.

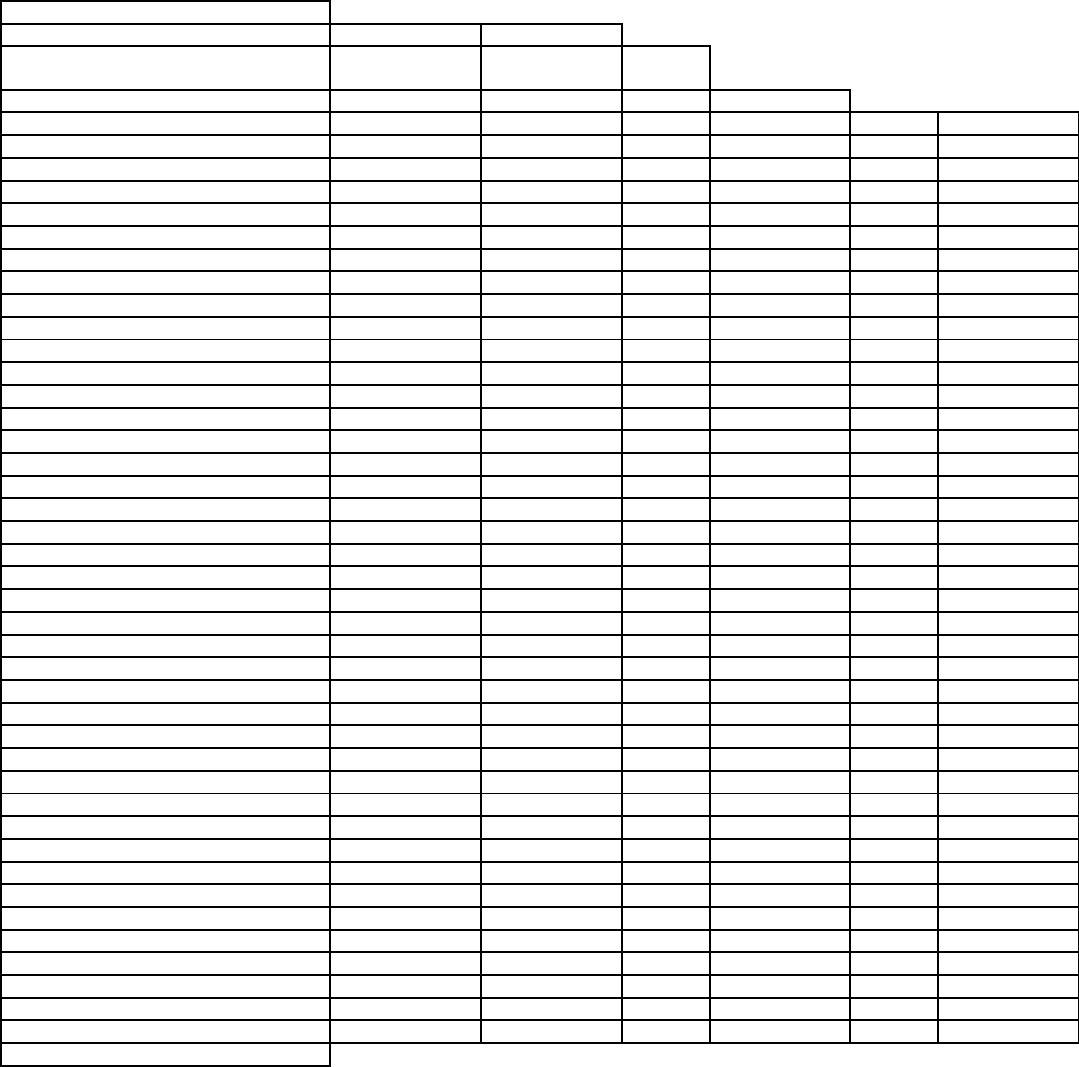

Figure 4-4

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

80,000

Other Current Assets

253,000

450,000

Investment in Sub. Company

560,000

Other Long-Term Investments

50,000

30,000

Land

140,000

70,000

Buildings and Equipment

315,000

400,000

Accumulated Depreciation

(208,000)

(110,000)

Other Intangibles

60,000

Current Liabilities

(150,000)

(100,000)

Bonds Payable

(100,000)

Premium on Bonds Payable

(5,000)

Other Long-Term Liabilities

(200,000)

(150,000)

Common Stock – P Co.

(200,000)

Other Paid in Capital – P Co.

(100,000)

Retained Earnings – P Co.

(421,000)

Common Stock – S Co.

(100,000)

Other Paid in Capital – S Co.

(200,000)

Retained Earnings – S Co.

(300,000)

Net Sales

(600,000)

(380,000)

Cost of Goods Sold

350,000

180,000

Operating Expenses

140,000

100,000

Dividend Income

(24,000)

Gain on Sale of Equipment

(20,000)

Dividends Declared – P Co.

60,000

Dividends Declared – S Co.

30,000

Consolidated Net Income

NCI

Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Other Long-Term Investments

Land

Buildings and Equipment

Accumulated Depreciation

Other Intangibles

Current Liabilities

Bonds Payable

Premium on Bonds Payable

Other Long-Term Liabilities

Common Stock – P Co.

Other Paid in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Dividend Income

Gain on Sale of Equipment

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

NCI

Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

For the worksheet solution, please refer to Answer 4-4.