36. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$300,000. Any excess of cost over book value on this date is attributed to a patent, to be amortized over 10

years.

On this date, Subsidiary had total shareholders’ equity as follows:

8% Preferred Stock, $100 par

$100,000

Common Stock, $10 par

50,000

Other Paid-in Capital

120,000

Retained Earnings

180,000

Total

$450,000

The 8% preferred stock is cumulative, non-participating, and has a liquidating value of par plus dividends in arrears. There were no preferred

dividends in arrears on January 1, 20X1.

During 20X1, Subsidiary had a net loss of $10,000 and paid no dividends. In 20X2, Subsidiary had net income of $20,000, but paid no dividends. In

20X3, Subsidiary had net income of $100,000 and paid dividends, on preferred and common, totaling $50,000.

On January 1, 20X2, Parent purchased $50,000 par value of Subsidiary’s preferred stock for $52,000. At year end, the preferred is still held as an

investment.

Required:

a.) Prepare Parent’s journal entries for its investment in the subsidiary’s preferred stock for 20X2 and 20X3.

b.) Calculate the increase in equity resulting from the retirement of preferred stock.

c.) Prepare the entries needed to eliminate the parent’s investment in the subsidiary’s preferred stock for the 20X3 consolidated worksheet.

Investment in Subsidiary Preferred Stock

52,000

Cash

Investment in Subsidiary Preferred Stock

4,000

Subsidiary Income

Investment in Subsidiary Preferred Stock

4,000

Subsidiary Income

Price paid

$52,000

Preferred stock at par

$100,000

108,000

x 50%

54,000

Increase in equity

$ 2,000

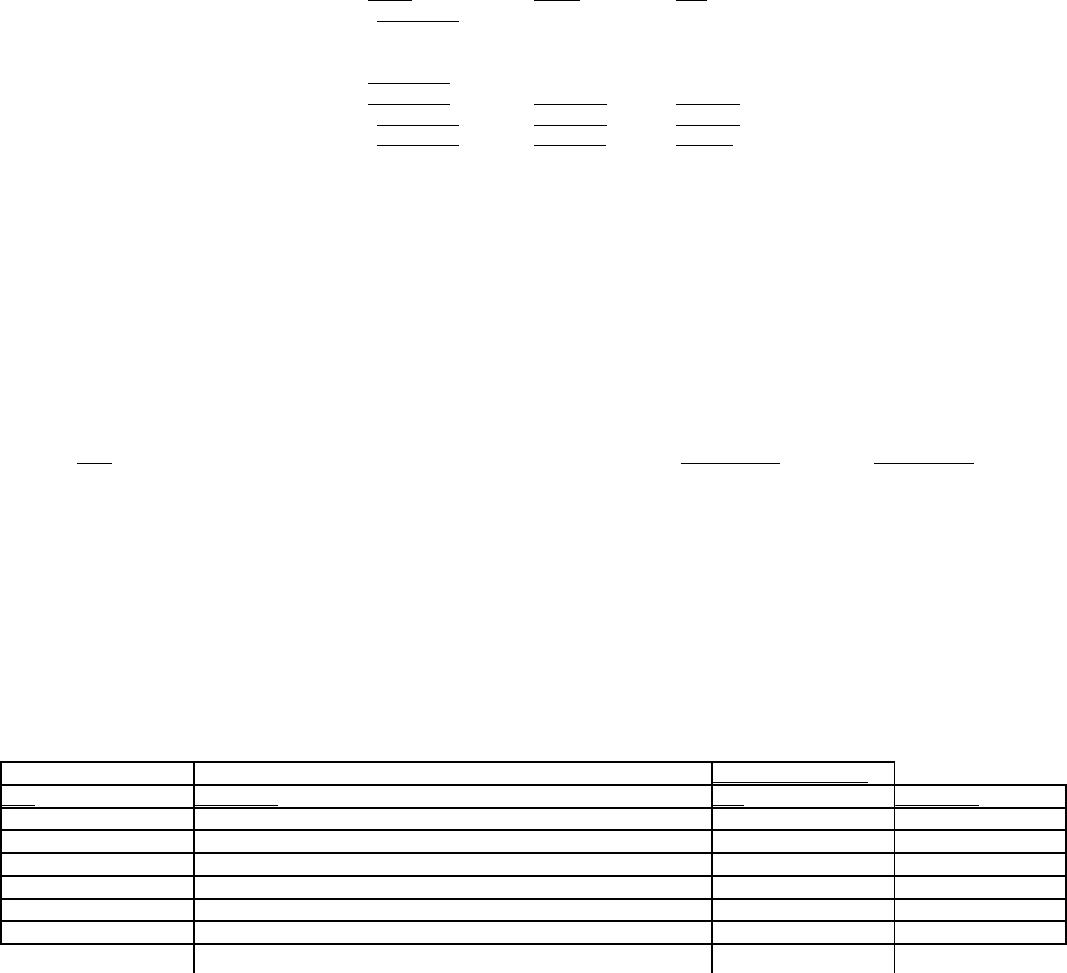

37. Company P Industries purchased a 70% interest in Company S on January 1, 20X1, and prepared the

following determination and distribution of excess schedule:

D&D Schedule

Entity

Parent

NCI

Entity Fair Value

$ 300,000

210,000

90,000

Book value:

Paid-In Capital – Common

200,000

Retained Earnings

80,000

Book value:

280,000

196,000

84,000

Excess

$ 20,000

14,000

6,000

Patent

$ 20,000

20 years

1,000

Since the purchase, there have been the following intercompany transactions:

(1)

On January 1, 20X2, Company P sold a piece of equipment with a net book value

of $40,000 to Company S for $50,000. The equipment had a five-year remaining

life.

(2)

Each year, starting in 20X3, Company S has sold merchandise for resale to

Company P at a gross profit of 20%. A summary of transactions shows the

following:

Ending

Dollar Sales

Inventory

Year

with Mark-up

with Mark-up

20X3

$110,000

$30,000

20X4

$120,000

$40,000

20X5

$140,000

$60,000

(3)

On January 1, 20X5, Company P purchased Company S’s 8%, $100,000 face value

bonds for $98,000, which were issued at par value. The bonds have five years to

maturity.

Required:

Complete the following schedule to adjust the retained earnings of the noncontrolling and controlling interest on the December 31, 20X5, worksheet

for a consolidated balance sheet only. Company P uses the simple equity method to account for its investment.

Adjustment to RE of:

Item

Calculation

NCI

Controlling

Patent

Patent

Equipment

Merchandise

Bonds

Total

38. On January 1, 20X1, Parent Company acquired 90% of the common stock of Subsidiary Company for

$360,000. On this date, Subsidiary had total owners’ equity of $270,000, including retained earnings of

$100,000.

On January 1, 20X1, any excess of cost over book value is attributable to the undervaluation of land, building,

and goodwill. Land is worth $20,000 more than cost. Building is worth $60,000 more than book value. It has a

remaining useful life of 6 years and is depreciated using the straight-line method.

During 20X1, Parent has accounted for its investment in Subsidiary using the cost method.

During 20X1, Subsidiary sold merchandise to Parent for $70,000, of which $20,000 is held by Parent on

December 31, 20X1. Subsidiary’s usual gross profit on affiliated sales is 50%.

On December 31, 20X1, Parent still owes Subsidiary $5,000 for merchandise acquired in December.

On July 1, 20X1, Parent sold to Subsidiary some equipment with a cost of $40,000 and a book value of

$18,000. The sales price was $30,000. Subsidiary is depreciating the equipment over a 4-year life, assuming no

salvage value and using the straight-line method.

Required:

Prepare a determination and distribution of excess schedule. Next, complete the Figure 7-11 worksheet for a

consolidated balance sheet as of December 31, 20X1.

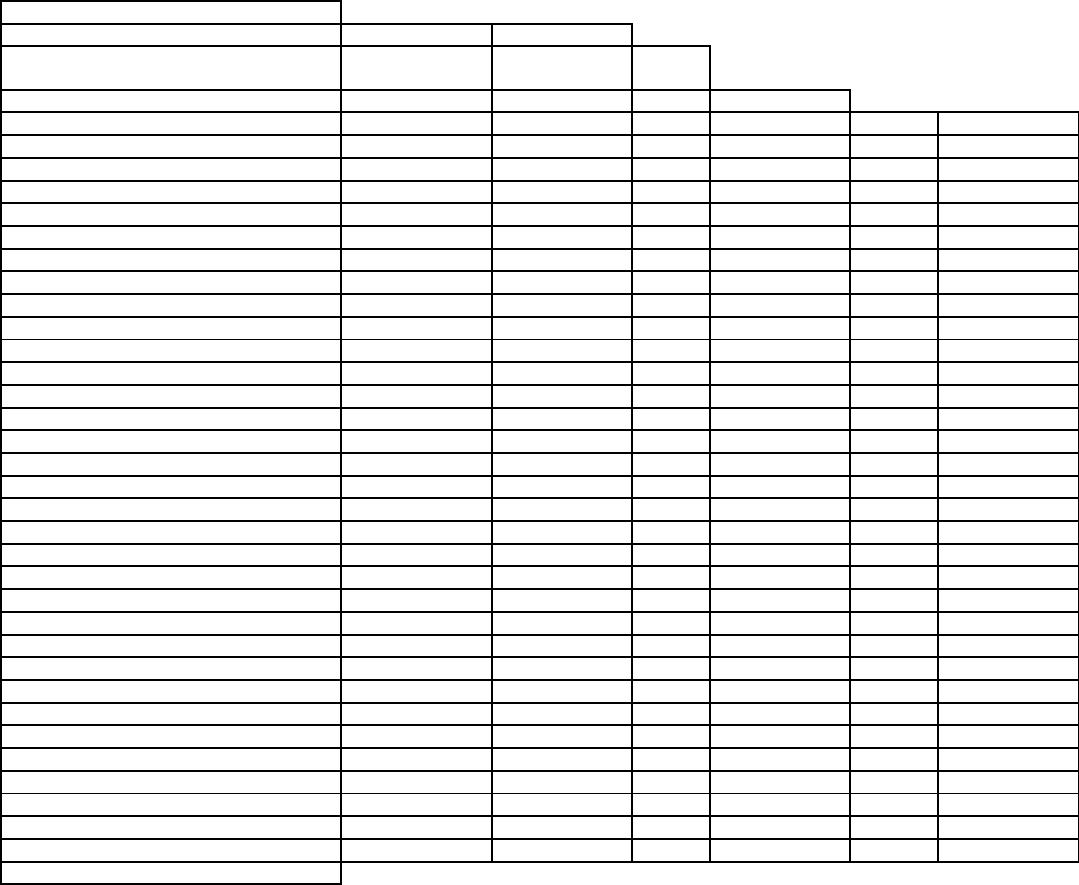

Figure 7-11

Balance Sheet

Eliminations and

Parent

Sub.

Adjustme

nts

Account Titles

Company

Company

Debit

Credit

Assets:

Accounts Receivable

60,000

50,000

Inventory

110,000

90,000

Other Current Assets

87,000

160,000

Invest in Sub. Company

360,000

Land

100,000

30,000

Buildings and Equipment

400,000

280,000

Accumulated Depreciation

(200,000)

(100,000)

Total

917,000

510,000

Liabilities and Equity:

Accounts Payable

91,000

50,000

Other Current Liabilities

86,000

100,000

Long-Term Liabilities

150,000

50,000

Common Stock – P Co.

100,000

Other Pd-In Capt – P Co.

150,000

Retained Earnings – P Co.

340,000

Common Stock – S Co.

50,000

Other Pd-In Capt – S Co.

120,000

Retained Earnings – S Co.

140,000

NCI to Consol Bal Sheet

Total

917,000

510,000

(continued)

Consolidated

Balance Sheet

Account Titles

NCI

Debit

Credit

Assets:

Accounts Receivable

Inventory

Other Current Assets

Invest in Sub. Company

Land

Buildings and Equipment

Accumulated Depreciation

Total

Liabilities and Equity:

Accounts Payable

Other Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Pd-In Capt – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Pd-In Capt – S Co.

Retained Earnings – S Co.

NCI to Consol Bal Sheet

Total

Determination and Distribution of Excess Schedule:

90%

10%

Entity

Parent

NCI

Entity Fair Value

$ 400,000

$ 360,000

$ 40,000

Book value:

170,000

100,000

Book value:

$ 270,000

243,000

27,000

Excess

$ 130,000

$ 117,000

$ 13,000

Adjustments:

Land

$ 20,000

Building

60,000

6 yrs

10,000

Goodwill

50,000

Total

$ 130,000

39. It is common for a parent firm to record its investment in a subsidiary under either the cost or simple equity

method to expedite the elimination process. This does create some complications, however, when all or a

portion of the investment is sold. Assume that in each of the following cases, the parent sells its investment

midway through its fiscal year.

(1)

The parent owned an 80% interest and sold all of its holdings.

(2)

The parent owned an 80% interest and sold a 20% interest to reduce its ownership percentage to 60%.

(3)

The parent owned an 80% interest and sold a 60% interest to reduce its ownership percentage to 20%.

Required:

a.

For each of the above cases, comment on the procedures necessary to record the sale, where the investment is carried under simple equity,

and the impact on consolidated income of the sale.

b.

For each of the above cases, state the added procedures that would be necessary if the investment was recorded under the cost method.

adjust retained earnings for prior years’ amortization, which, in the past, were made on the consolidated worksheet. The gain or loss on

for as it would under the simple equity method.

the simple equity method for both the prior periods and the current partial period.

will be shown in the “other gains and losses” section of the income statement. There will no longer be a consolidation, and the 20%

40. A subsidiary company may have preferred stock as part of its equity structure. Further, suppose that the

preferred stock is cumulative and in arrears on dividends.

Required:

a.

What is the impact of the preferred stock on the excess of cost over book value on the original controlling investment in common stock?

b.

What is the impact of the preferred stock on the annual distribution of income?

c.

What is the theory followed in consolidated reporting when the parent purchases a portion of the subsidiary’s preferred stock?

below book value or as a reduction of previous paid-in from retirement or retained earnings if the price paid exceeds book value.