Chapter 20—Estates and Trusts: Their Nature and the Accountant’s

Role Key

1. In an intestate distribution, personal property is distributed

2. An administrator of an estate differs from an executor of a will in that an administrator

3. Which of the following would not be included in the corpus or principal of an estate?

4. Which of the following items is not included in the estate principal subsequent to the date of death?

5. In the initial journal entry recording the inventory of the estate, liabilities incurred by the decedent are

6. Property that is titled as “joint tenants” allows for:

7. When assets are discovered after the initial accounting for estate principal, the fiduciary will credit:

8. The party ultimately receiving the principal of an estate may be referred to as the

9. The primary purpose of accounting for estates is to facilitate reporting to the court during the fiduciary’s term.

Therefore, which of the following concepts is least important?

10. Which of the following is not an example of income in an estate?

11. Which of the following items is not charged against the income of an estate?

12. Which of the following items are chargeable against the income of an estate?

13. Which of the following statements is true concerning the handling of discounts and premiums for bonds that

are part of an estate at the time of death?

14. Which of the following best describes the accounting for discounts and premiums for bonds purchased by a

fiduciary for an estate?

15. Which of the following statements concerning accounting for depreciation and depletion in an estate is not

true?

16. All of the following would be charged to principal in an estate except:

17. Which of the following is not a legacy?

18. A gift from a specific source, with the will stipulating that if the amount cannot be satisfied from that

source, it should be satisfied from the general estate is a __________ legacy.

19. In a testate distribution, a gift of property left after all other legacies have been assigned is referred to as a

20. If after paying debts and expenses, the estate principal is not adequate to satisfy the various legacies, the

legacies are satisfied to whatever extent possible through the:

21. The primary purpose of an estate’s charge and discharge statement is to detail

22. The Charge and Discharge Statement accounting indicates the need to segregate

23. Planning for estate taxes should address:

24. Which of the following statements is true concerning the maximum gift that can be given within a year

without incurring any gift tax or using any of the unified credit?

25. Which of the following statements is not true?

26. Which of the following is not true about the unified credit that accompanies the unified transfer tax?

27. The unified tax base used to compute federal estate tax is calculated as follows:

28. When determining a decedent’s gross estate for federal tax purposes, which of the following items would not

be included?

29. The gross estate of a decedent:

30. The starting point for the computation of federal estate tax is the gross estate. Which of the following

statements is not true regarding the computation of the gross estate?

31. The effect of the marital deduction is:

32. The alternate valuation date is how many months after the decedent’s death?

33. Which of the following statements is true concerning the election of the alternate valuation date?

34. Jane Ramos owned stock with a cost of $200,000. The stock has a market value on Jane’s date of death of

$375,000. The stock was willed to Jane’s niece Jenny. Which of the following is true?

35. Which of the following statements is true concerning federal income tax laws and estates?

36. A charitable remainder trust

37. A trust created through a will is called a(n)

38. The party to which legal title and management responsibilities are initially given in a trust agreement is

referred to as the

39. Complete the following statements by filling in the blanks:

a.

Real property disposed of under a valid will is called a(n) __________.

b.

A person who dies without a valid will is said to die __________.

c.

The personal representative of the decedent under a valid will is called the __________.

d.

For an unmarried person, the amount of property exempted from the federal estate tax is referred to as the __________.

e.

Since estate rates increase as the tax base increases, the rates are said to be __________.

f.

With spousal consent, nontaxable gifts per individual per year amount to __________.

g.

Under appropriate conditions, the fiduciary of an estate may value assets at a date six months after death. The date is called the

__________.

h.

A valid will says, “My nephew shall receive the gold Canadian maple leaf coins in my Greenwood Trust safety deposit box.” This is an

example of a(n) __________ legacy.

i.

Income from an asset may be assigned to one party called the __________. After a stipulated period of time, the asset itself may be

distributed to another party called the __________.

devise

b.

intestate

executor or executrix

d.

unified credit

progressive

f.

$26,000

g.

alternate valuation date

h.

specific

income beneficiary; remainderman

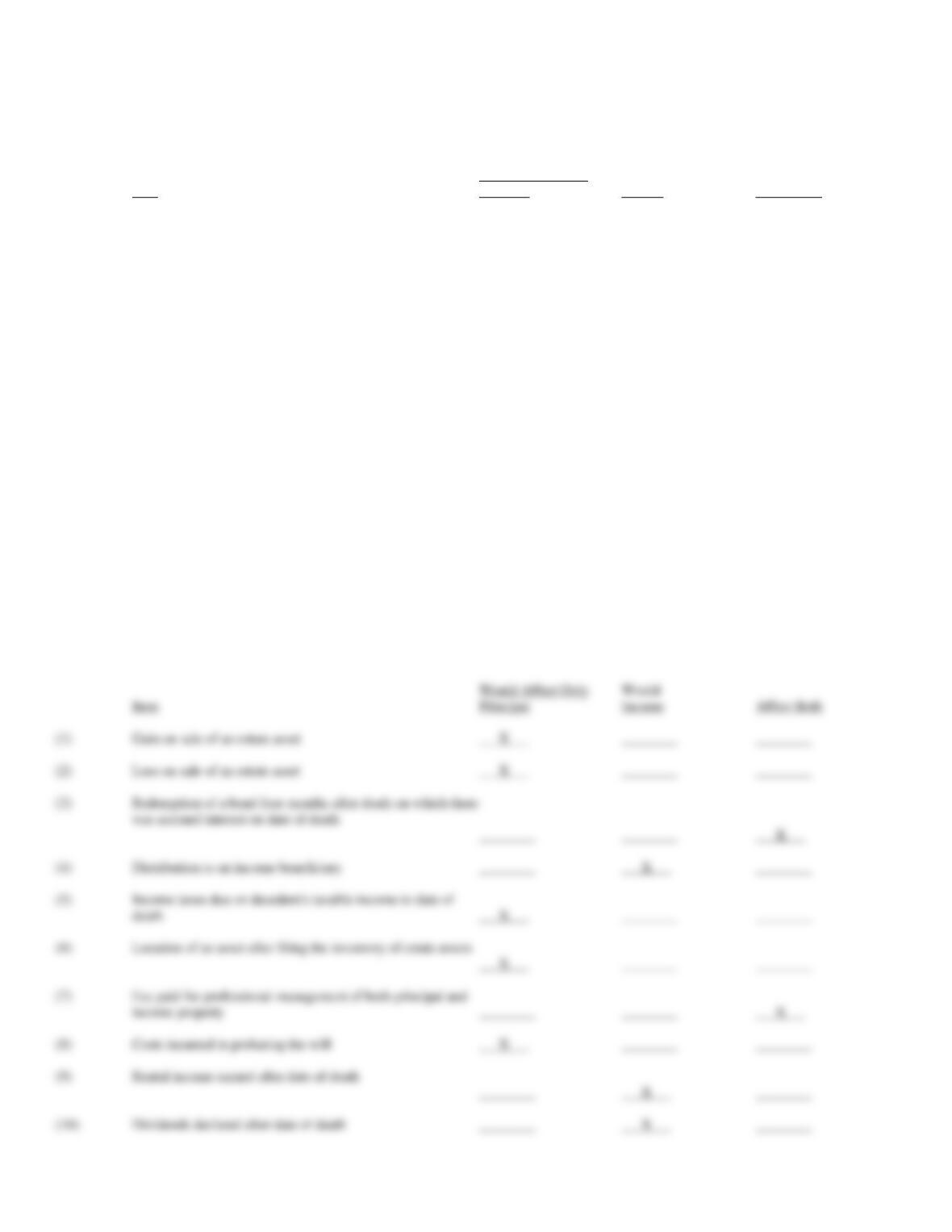

40. Assuming that no stipulation is made in the will, indicate by placing a check mark in the appropriate column

whether the typical accounting treatment of each of the following items would affect principal only, income

only, or both principal and income accounts of an estate.

Would Affect Only

Would

Item

Principal

Income

Affect Both

(1)

Gain on sale of an estate asset

________

________

________

(2)

Loss on sale of an estate asset

________

________

________

(3)

Redemption of a bond four months after death on which there

was accrued interest on date of death

________

________

________

(4)

Distribution to an income beneficiary

________

________

________

(5)

Income taxes due on decedent’s taxable income to date of

death

________

________

________

(6)

Location of an asset after filing the inventory of estate assets

________

________

________

(7)

Fee paid for professional management of both principal and

income property

_________

________

________

(8)

Costs incurred in probating the will

_________

________

________

(9)

Rental income earned after date of death

________

________

________

(10)

Dividends declared after date of death

________

________

________

Would Affect Only

Would

Item

Principal

Income

Affect Both

(1)

Gain on sale of an estate asset

X

________

________

(2)

Loss on sale of an estate asset

X

________

________

________

________

X

(4)

Distribution to an income beneficiary

________

X

________

(5)

Income taxes due on decedent’s taxable income to date of

death

X

________

________

(6)

Location of an asset after filing the inventory of estate assets

X

________

________

(7)

Fee paid for professional management of both principal and

income property

________

________

X

(8)

Costs incurred in probating the will

X

________

________

Dividends declared after date of death

________

X

________

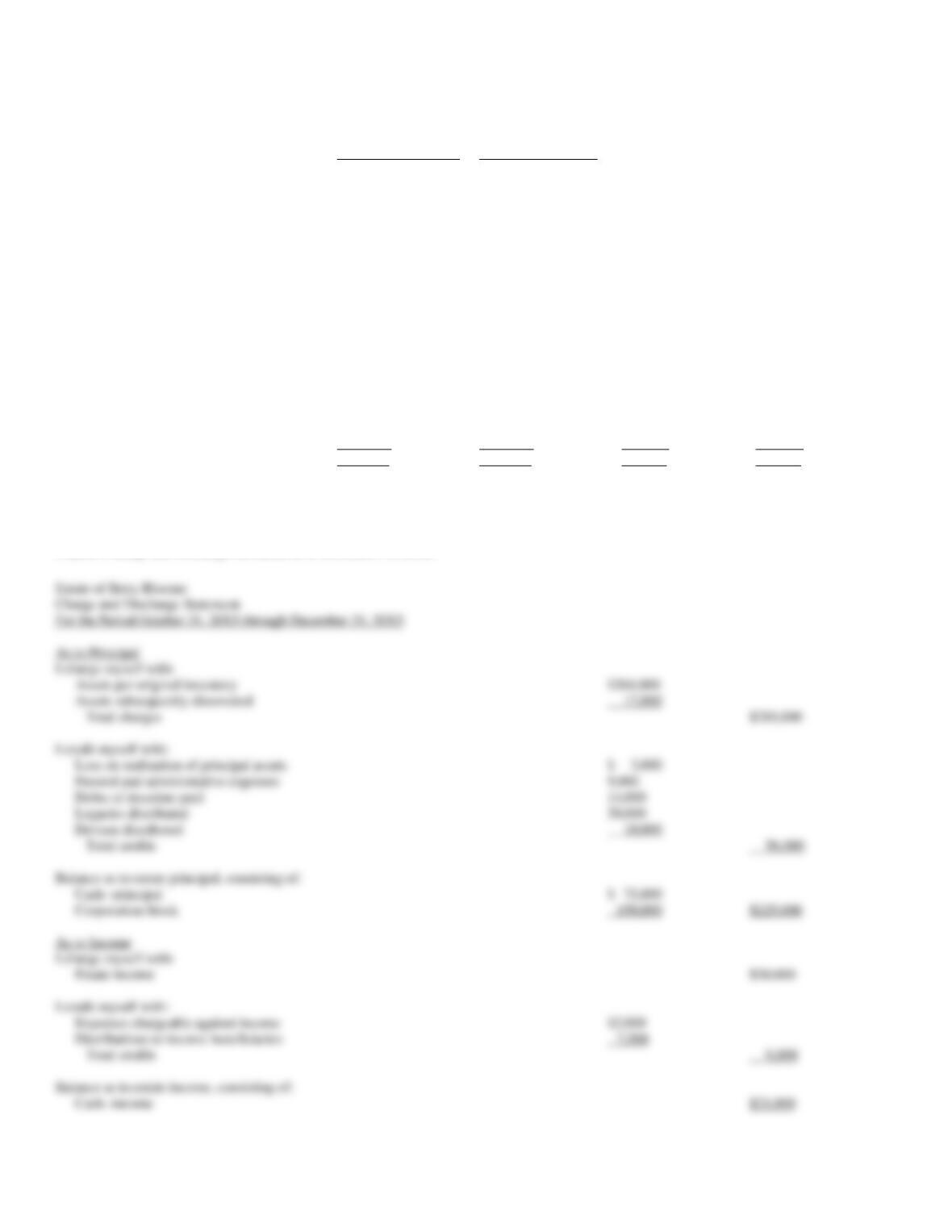

41. Betty Bloome died on February 28, 20X5. The following trial balance was prepared by the executor of

Betty’s estate as of October 31, 20X5:

As to Principal

As to Income

Cash—Principal

$ 75,000

Cash—Income

$21,000

Corporation Stock

150,000

Assets Subsequently

Discovered.

$ 17,000

Loss on Realization of

Principal Assets

3,000

Funeral and Administrative

Expense

9,000

Debts of Decedent Paid

14,000

Legacies Distributed

20,000

Devises Distributed

10,000

Estate Principal

264,000

Expenses Chargeable

Against Income

$ 2,000

Distributions to Income

Beneficiaries

7,000

Estate Income

30,000

$281,000

$281,000

$30,000

$30,000

Required:

Prepare a charge and discharge statement as of December 31, 20X5.

Estate of Betty Bloome

Charge and Discharge Statement

For the Period October 31, 20X5 through December 31, 20X5

As to Principal

I charge myself with:

Assets per original inventory

$264,000

Assets subsequently discovered

17,000

Total charges

$281,000

I credit myself with:

Loss on realization of principal assets

$ 3,000

Funeral and administrative expenses

9,000

Debts of decedent paid

14,000

Legacies distributed

20,000

Devises distributed

10,000

Total credits

56,000

Balance as to estate principal, consisting of:

Cash—principal

$ 75,000

Corporation Stock

150,000

$225,000

I charge myself with:

Estate income

$30,000

I credit myself with:

Expenses chargeable against income

$2,000

Distributions to income beneficiaries

7,000

Total credits

9,000

42. Al Sooner died on January 15, 20X5. Records disclose the following estate:

Cash in the bank

$ 7,500

5% note receivable, including $50 accrued

interest

3,050

Stocks

70,000

Dividends declared on stocks

250

8% mortgage receivable, including $150

accrued interest

30,150

Real estate – apartment house

400,000

Household effects

27,250

Dividends receivable from the Peg Sooner

Trust Fund

250,000

Total inventory of assets

$788,200

Cash receipts:

Jan.

20

Dividends

$ 1,500

25

5% note receivable

3,000

Interest on 5% note receivable

53

Stocks sold, inventoried at $22,500

20,000

8% mortgage sold

33,000

Interest accrued on mortgage

207

28

Sale of assets not inventoried

250

29

Sale of apartment house

395,000

Total cash receipts

$453,010

Cash Disbursements:

Jan.

20

Funeral expenses

$ 2,750

23

Decedent’s debts

8,000

25

Decedent’s bequests

10,000

31

Payment to son, including all estate income

20,000

Total cash disbursements

$40,750

Required:

Prepare journal entries to record the events in his estate for the period January 15 through January 31, 20X5.

To record sale of apartment

43. Trent Tyler died on January 15, 20X9. Records disclose the following estate:

Cash in the bank

$ 15,000

8% note receivable, including $100 accrued interest

8,100

Stocks

80,000

Dividends declared on stocks

600

10% mortgage receivable, including $200 accrued interest

40,200

Real estate – apartment house

220,000

Household effects

21,500

Dividends receivable from Terry Tyler Trust Fund

100,000

Total inventory of assets

$485,400

Cash receipts:

Jan.

20

Dividends

$ 4,500

25

8% note receivable

8,000

Interest on 8% note receivable

120

Stocks sold, inventoried at $62,000

55,000

10% mortgage sold

46,000

Interest accrued on mortgage

300

28

Sale of assets not inventoried

450

29

Sale of apartment house

210,000

Total cash receipts

$324,370

Cash Disbursements:

Jan.

20

Funeral Expenses

$ 6,500

23

Decedent’s debts

5,000

Decedent’s bequests distributed to widow

18,000

31

Payment to son, including all estate income

35,000

Total cash disbursements

$64,500

Required:

Prepare a charge and discharge statement for the period January 15 through January 31, 20X9.