Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

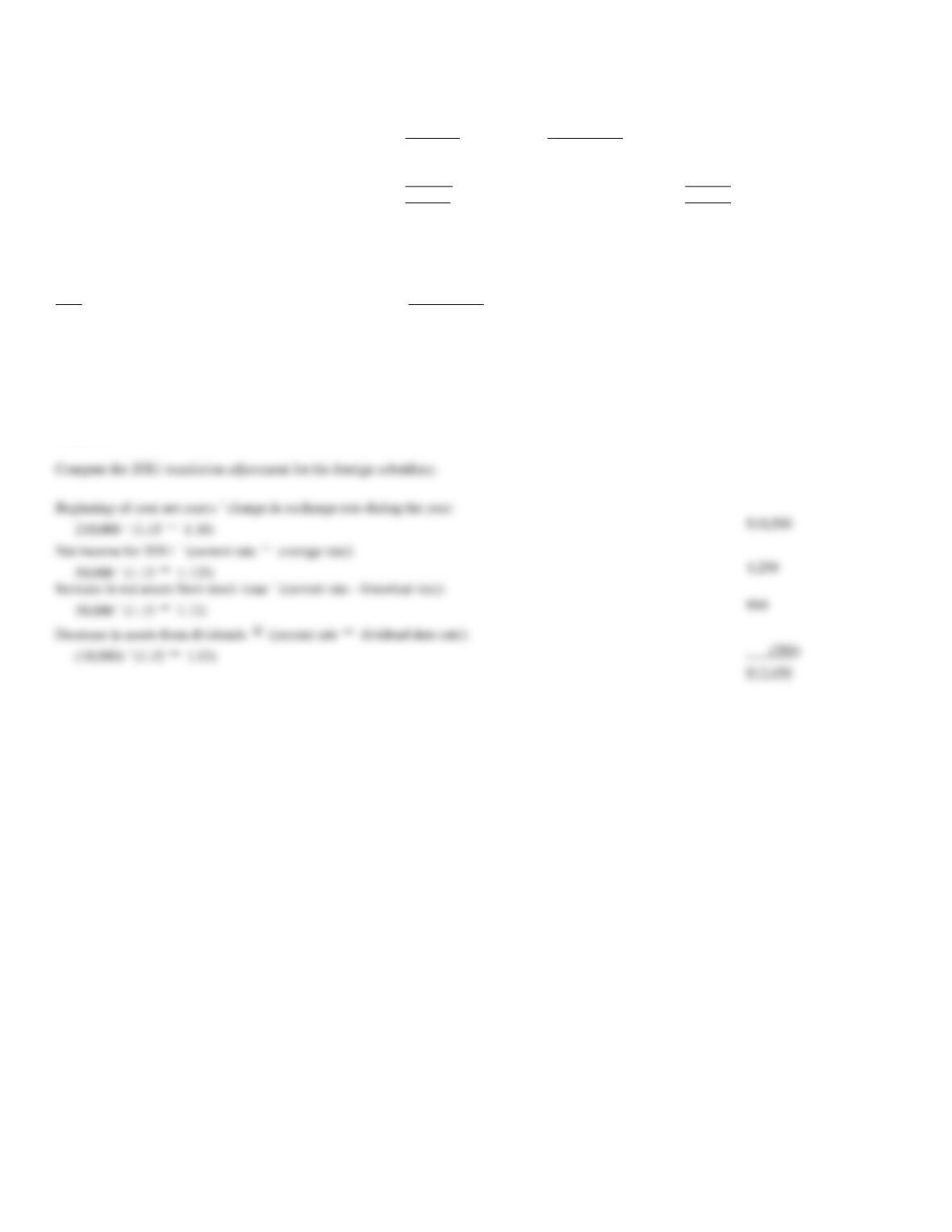

58. Green Corporation, a wholly owned British subsidiary of a U.S. firm began the year with 1,300,000 British

pounds in net assets. The subsidiary incurred a 65,000 British pound net loss for 20X1. The subsidiary issued

common stock for 100,000 British pounds on November 15, 20X1. Assume the following exchange rates for

20X1:

Date

1 British pound equal to

January 1, 20X1

$1.10

November 15, 20X1

$1.15

December 31, 20X1

$1.13

20X1 average

$1.14

Required:

Compute the translation adjustment for 20X1 using the direct method.

59. A U.S.-owned foreign subsidiary has the following beginning and ending stockholders' equity for 20X1:

January 1

December 31

Common stock

120,000

FC

140,000

FC

Paid-in capital in excess of par

30,000

40,000

Retained earnings

60,000

100,000

210,000

FC

280,000

FC

The change in common stock resulted from a sale of stock to the parent firm on May 15. The change in retained earnings resulted from a July 1

dividend of 10,000 FC and net income for 20X1. Various exchange rates were as follows:

Date

1 FC equal to

January 1, 20X1

$1.10

May 15, 20X1

$1.12

July 1, 20X1

$1.13

December 31, 20X1

$1.15

20X1 average

$1.125

Required:

60. A U.S. firm purchased 100% of a foreign firm on January 1, 20X1, when the foreign firm had the following

equity accounts:

Common stock

150,000

FC

Paid-in excess of par value

50,000

FC

Retained earnings

200,000

FC

400,000

FC

The U.S. firm paid 420,000 FCs for the foreign firm. The payment in excess of book value is traceable to undervalued land owned by the foreign

firm. The foreign firm had a net income of 25,000 FCs during 20X1. Assume that the following exchange rates are relevant:

Date

1 FC equal to

January 1, 20X1

$2.00

December 31, 20X1

$1.80

20X1 average

$1.95

Required:

Prepare all the journal entries to record and update the investment account of the U.S. firm and the necessary eliminating and adjusting entries for the

20X1 consolidated statement. Assume that the U.S. firm used the simple equity method.

61. On January 1, 20X1, Rapid Corporation purchased 25% of a foreign firm when its stockholders' equity

section totaled 240,000 FCs. Rapid Corporation paid 75,000 FCs, with the excess over book value being

attributed to equipment with a 5-year useful life. The foreign firm reported net income of 80,000 FCs for 20X1.

Relevant exchange rates were as follows:

Date

1 FC equal to

January 1, 20X1

$0.30

December 31, 20X1

$0.35

Average 20X1

$0.33

Required:

Prepare the journal entries necessary to record the events concerning Rapid's investment in the foreign firm.

62. On January 1, 20X2, U.S.A. Inc. created an Algerian subsidiary, Niko, Inc. The books are kept in Algerian

dinars, but the functional currency is the U.S. dollar. Dividends are paid on December 31, and income is earned

evenly throughout the year. The earnings and dividends of Niko in dinars are as follows:

Net Income

Dividends

20X2

100,000

50,000

20X3

200,000

80,000

20X4

325,000

105,000

Exchange rates are given below.

Yearly Average

Dec. 31 Spot

20X2

.0175

.0185

20X3

.0188

.022

20X4

.019

.025

Required:

Calculate the balance in retained earnings for Niko in dollars as of December 31, 20X4.

63. Renta USA, Inc. formed a foreign subsidiary on January 1, 20X3; the subsidiary issued 15,000 of its no-par

10FC stock to Renta. The subsidiary's books are kept in their functional currency. Income earned in 20X3 and

20X4 totaled 100,000 FC and 120,000 FC, respectively. Dividends of 40,000 FC have been paid on December

31 of each year. In addition, 1,000 shares of common stock (no par) were issued on July 1, 20X4 for 20 FC

each.

Exchange rates relating this foreign currency to U.S. dollars are as follows:

January 1, 20X3

1.00

December 31, 20X3

1.04

Average 20X3

1.02

July 1, 20X4

1.05

December 31, 20X4

1.10

Average 20X4

1.08

Required:

Calculate the owners' equity of the subsidiary on December 31, 20X4.

64. On January 1, 20X8, Cayane Inc. purchased 90% of an German firm, Brosch Manufacturing when Brosch's

equity consisted of the following:

Common stock

500,000

euros

Paid-in capital in excess of par

100,000

Retained earnings

150,000

750,000

euros

Cayane paid 810,000 euros for its 90% interest in Brosch. The excess over book value was attributed to a building with a 20-year useful life. Brosch

reported net income for 20X8 of 150,000 euros. The year-end cumulative translation adjustment is $10,000 credit. Relevant exchange rates are as

follows:

January 1, 20X8

1 euro = $.65

December 31, 20X8

1 euro = .68

20X8 average

1 euro = .66

Required:

Prepare all the journal entries related to Cayane's investment in Brosch and all the necessary eliminating and adjusting entries for consolidation of

Brosch, assuming the use of the simple equity method.

65. Hylie, a U.S. corporation, owns 100% of Frosan, a French firm. Assume that the dollar is the functional

currency, although the books are kept in euros.

Required:

What currency exchange rate would be used to remeasure Frosan's balance sheet into U.S. dollars? Choose from

current, simple average, weighted average, or historical.

a.

Cash

_____________________

b.

Accounts Receivable

_____________________

c.

Inventory, carried at cost

_____________________

d.

Equipment

_____________________

e.

Accumulated Depreciation

_____________________

f.

Bonds Payable

_____________________

g.

Common Stock

_____________________

h.

Sales

_____________________

66. A Kuwaiti subsidiary of Hiawatha Corp. (a U.S. firm) has certain balance sheet accounts on December 31,

20X4. The functional currency is the U.S. dollar and currency of record is the dinar and the parents books are

kept in U.S. dollars.

Information relating to these account in U.S. dollars is as follows:

Translated at

Current Rate

Historical Rate

Cash

$150,000

$150,000

Accounts Receivable

115,000

110,000

Inventories

285,000

255,000

Prepaid Insurance

12,000

10,000

Land

90,000

180,000

Buildings

500,000

800,000

Required:

From the above information, prepare the asset portion of the subsidiary's trial balance.

67. A French subsidiary of a U.S. firm keeps accounting records in euros. The U.S. dollar is considered the

subsidiary's functional currency. Assume the following exchange rates:

Date

1 euro equal to

January 1, 20X5

$1.05

July 1, 20X5

$1.07

Dec. 31, 20X5

$1.09

Average 20X5

$1.08

January 1, 20X6

$1.09

July 1, 20X6

$1.07

Dec. 31, 20X6

$1.06

Average 20X6

$1.08

Required:

Remeasure the following items from the December 31, 20X6 trial balance of the subsidiary:

a.

Sales made evenly

throughout 20X6 = 100,000

euros

b.

Cost of goods sold = 30,000

euros

5,000 euros purchased July 1, 20X5

25,000 euros purchased July 1, 20X6

c.

Salary expense for 20X6 =

40,000 euros

d.

Land = 1,000,000 euros

200,000 euros purchased January 1, 20X5

800,000 euros purchased July 1, 20X6

68. An American firm owns 100% of a German firm that had the following transactions occur relative to their

equipment account:

January 1, 20X5

Purchased equipment for 50,000 euros

July 1, 20X5

Purchased equipment for 30,000 euros

January 1, 20X6

Purchased equipment for 75,000 euros

July 1, 20X6

Sold equipment purchased on January 1, 20X5 for 48,000 euros

The following exchange rates could be relevant:

Date

euro/$

Date

euro/$

January 1, 20X5

$0.50

January 1, 20X6

$0.53

July 1, 20X5

$0.52

July 1, 20X6

$0.50

December 31, 20X5

$0.53

December 31, 20X6

$0.49

Average 20X5

$0.515

Average 20X6

$0.51

Required:

Assuming that the U.S. dollar is the functional currency and that the German firm uses straight-line depreciation over a 5-year period with a 10%

salvage value, determine the following for remeasurement purposes:

a.

The value of the equipment account on December 31, 20X6.

b.

The value of the depreciation expense for 20X6.

c.

The amount of the gain or loss resulting from the July 1, 20X6, sale.

69. Kerry Manufacturing Company is a German subsidiary of a U.S. company. Kerry records its operations and

prepares financial statements in euros. However, its functional currency is the British pound. Kerry was

organized and acquired by the U.S. company on June 1, 20X4. The cumulative translation adjustment as of

December 31, 20X6, was $79,860. The value of the subsidiary's retained earnings expressed in British pounds

and U.S. dollars as of December 31, 20X7, was 365,000 pounds and $618,000, respectively. On March 1, 20X7,

Kerry declared a dividend of 120,000 euros. The trial balance of Kerry in euros as of December 31, 20X7, is as

follows:

Debit

Credit

Cash

240,000

Accounts Receivable (net)

2,760,000

Inventory (at cost)

3,720,000

Marketable Securities (at cost)

2,040,000

Prepaid Insurance

210,000

Depreciable Assets

8,730,000

Accumulated Depreciation

1,417,000

Cost of Goods Sold

17,697,000

Selling, General, and

Administrative Expense

4,762,000

Sales Revenue

26,430,000

Investment Income

180,000

Accounts Payable

2,120,000

Unearned Sales Revenue

960,000

Loans and Mortgage Payable

5,872,000

Common Stock

1,500,000

Paid-in Capital in Excess of Par

210,000

Retained Earnings

1,470,000

Total

40,159,000

40,159,000

The marketable securities were acquired on November 1, 20X6, and the prepaid insurance was acquired on December 1, 20X7. The cost of goods

sold and the ending inventory are calculated by the weighted-average method. The underlying costs have been incurred uniformly throughout the

year. On June 1, 20X4, 60% of the depreciable assets existed, and the balance was acquired on March 1, 20X6. The depreciable assets are amortized

over a 10-year period by the straight-line method. Of the total depreciation expense, 80% is traceable to the cost of goods sold and the balance is in

general expenses. On November 1, 20X6, Kerry received a customer prepayment valued at 3,000,000 euros. On February 1, 20X7, 2,040,000 euros

of the prepayment was earned. The balance remains unearned as of December 31, 20X7.

Relevant exchange rates are as follows:

Pounds/Euro

$/Pound

June 1, 20X4

0.310

$1.600

March 1, 20X6

0.300

$1.640

November 1, 20X6

0.305

$1.650

December 31, 20X6

0.310

$1.680

February 1, 20X7

0.302

$1.670

March 1, 20X7

0.300

$1.660

December 1, 20X7

0.290

$1.640

December 31, 20X7

0.288

$1.640

20X7 average

0.297

$1.660

Required:

Prepare a remeasured and translated trial balance of the Kerry Manufacturing Company as of December 31, 20X7. Provide supporting schedules.

For the Trial Balance Translation, please refer to Answer 11-16.

70. A foreign subsidiary operates in a highly inflationary economy. The company's December 31, 20X2, trial

balance includes the following:

Equipment:

Acquired on June 1, 20X1

800,000

FC

Acquired on October 1, 20X2

600,000

FC

Inventory:

Valued at lower cost or market

Market Value

182,000

FC

A cost of 184,000 FC represents 84,000 FC acquired

on December 1, 20X2, and 100,000 FC acquired on

October 1, 20X2.

Gain on sale of land:

This represents a gain from selling land that was

acquired on June 1, 20X1, at a cost of 50,000 FC,

on October 1, 20X2

100,000

FC

Relevant exchange rates are as follows:

Date

Rate

June 1, 20X1

$0.69

July 1, 20X1

$0.68

October 1, 20X2

$0.71

December 1, 20X2

$0.72

December 31, 20X2

$0.74

20X2 average

$0.70

Required:

a.

Discuss the criteria that must be satisfied in order to qualify as a highly inflationary economy.

b.

Discuss how the remeasurement of statements of companies operating in such economies affects net income.

c.

Calculate the dollar value of the trial balance accounts as of December 31, 20X2.

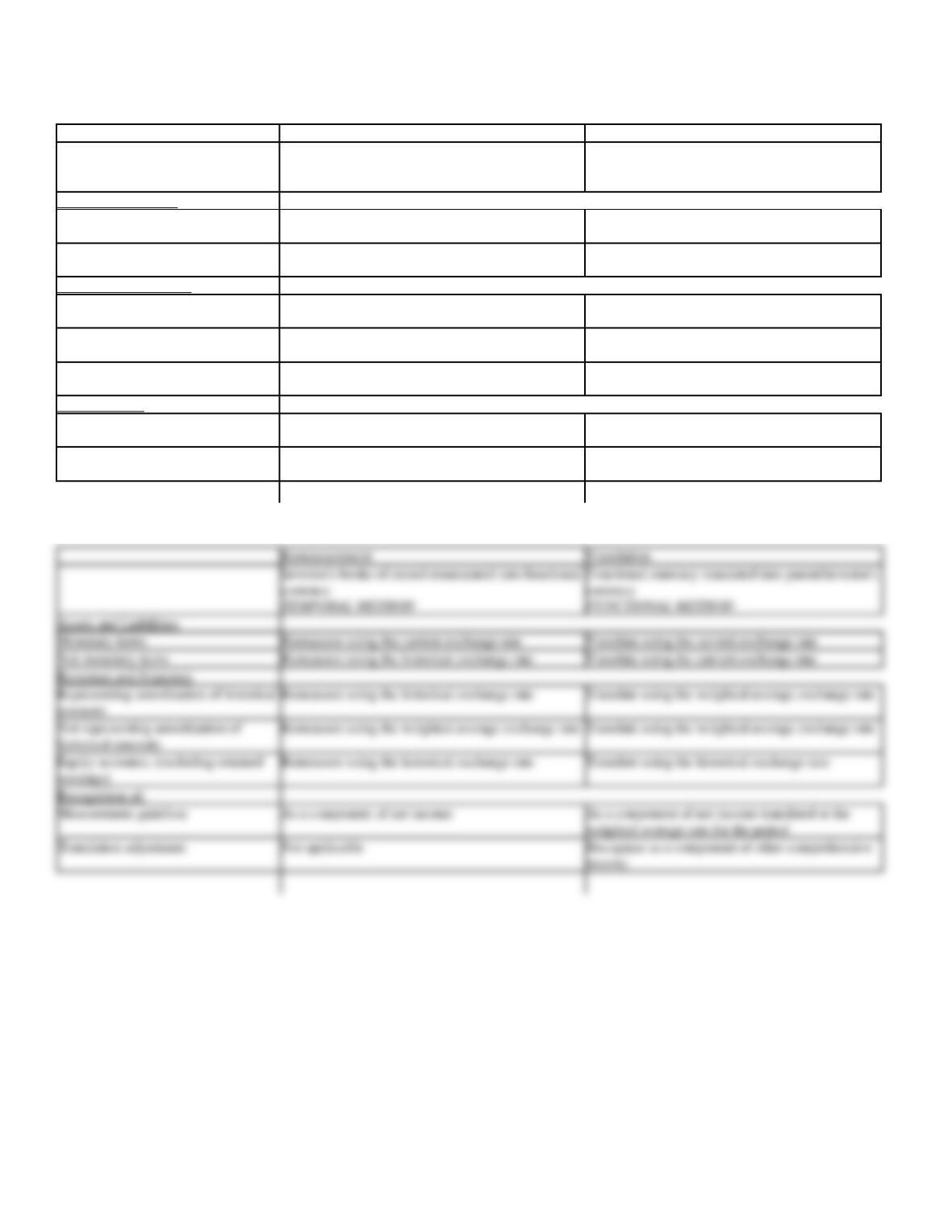

71. For each of the following account balances, identify the exchange rate used to translate or remeasure. The

choices are current exchange rate, historical rate, weighted average, other (specify).

Current Method

Remeasurement Method

Accounts Receivable

Prepaid Assets

Accounts Payable

Common Stock

Land

Goodwill

Sales Revenue

Depreciation Expense

72. Complete the following table:

Remeasurement

Translation

Investee's books of record remeasured into functional

currency

TEMPORAL METHOD

Functional currency translated into parent/investor's

currency

FUNCTIONAL METHOD

Assets and Liabilities

Monetary items

Not monetary items

Revenues and Expenses

Representing amortization of historical

amounts

Not representing amortization of

historical amounts

Equity accounts, (excluding retained

earnings)

Recognition of:

Measurement gain/loss

Translation adjustment

73. Discuss the factors that may be considered in determining if a Mexican subsidiary of a U.S. firm has the

peso or the dollar as its functional currency. The subsidiary only manufactures component parts that are shipped

to the U.S. firm's final production plant in Detroit.

Factors that should be considered include the following:

74. List the two primary objectives of translating foreign financial statements according to the FASB #52,

which emphasizes the concept of the functional currency.

75. Assume Champ Company will be translating the accounts of its foreign subsidiary, Collier, Ltd. for

inclusion in the consolidated financial statements.

1) What are the steps to be taken?

2) Assuming the functional currency is the currency of the country in which Collier is located, what rates should

be used/

3) Where should the adjustment resulting from the translation process be recognized?

76. Company A, an American company, owns Company B, a Canadian subsidiary. Company A borrowed

1,000,000 Canadian dollars as a hedge on its net investment in Company B. For 20X3, Company A recorded an

exchange gain of $40,000 due to exchange rate changes. The 20X3 translation adjustment for Company B was a

debit of $42,000.

Required:

Describe the accounting treatment required for the hedge on Company A's books.

77. Foreign firms operating in highly inflationary economies received special treatment under generally

accepted accounting principles (GAAP) relative to translating their financial statements.

Required:

a.

How does the FASB define a highly inflationary economy?

b.

Why is the method typically used for translating foreign entities not permitted for these firms?

c.

What method is used for remeasuring or translating the statements of these firms?