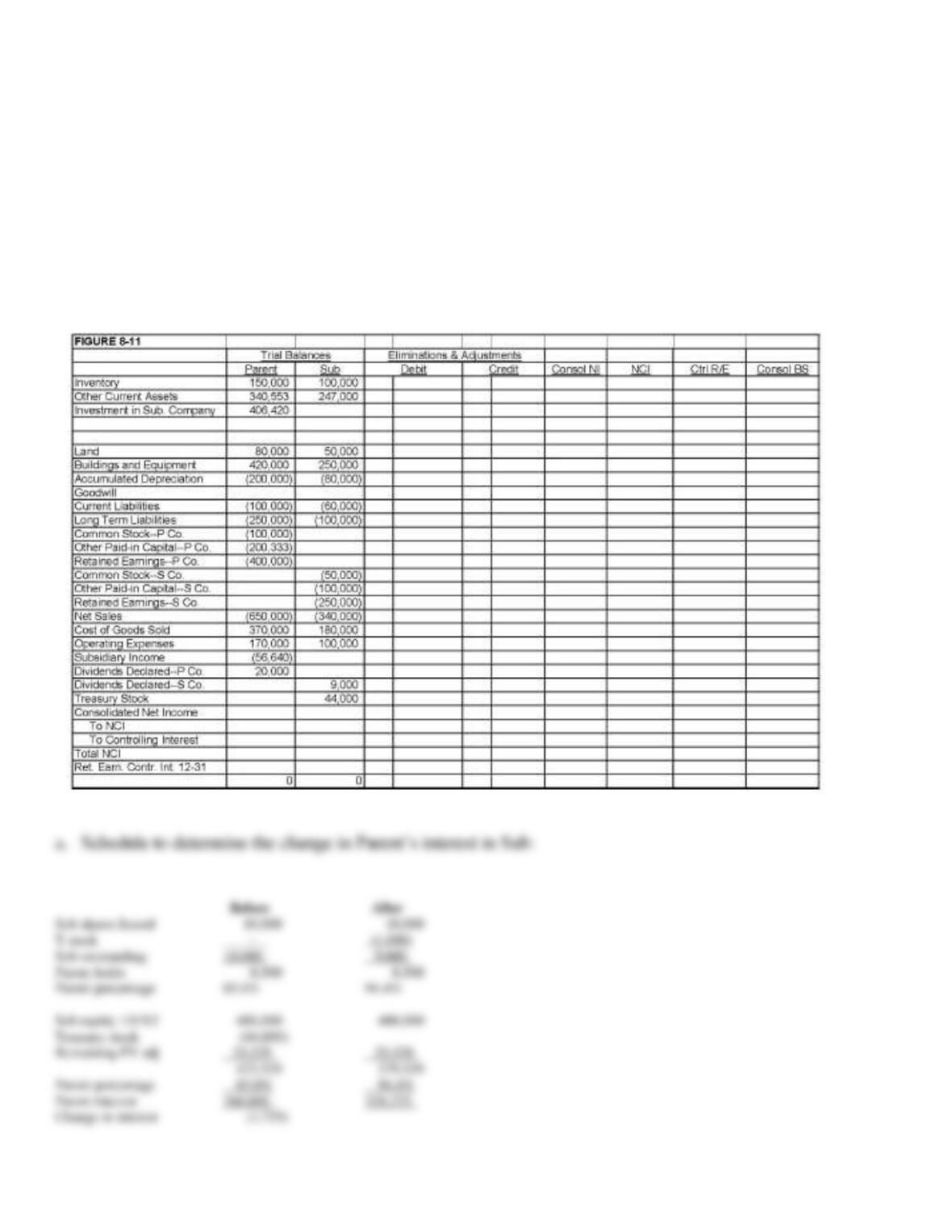

35. On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary

Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings

of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common

stock, 10% of the stock outstanding on that date. The price paid was $44,000. The trial balances of Parent and

Sub as of 12/31/X2 are given below:

Trial Balances

12/31/X2

Parent

Sub

Inventory

$ 150,000

$ 100,000

Other Current Assets

340,553

247,000

Investment in Sub. Company

406,420

Land

80,000

50,000

Buildings and Equipment

420,000

250,000

Accumulated Depreciation

(200,000)

(80,000)

Current Liabilities

(100,000)

(60,000)

Long Term Liabilities

(250,000)

(100,000)

Common Stock – P Co.

(100,000)

Other Paid-in Capital – P Co.

(200,333)

Retained Earnings – P Co.

(400,000)

Common Stock – S Co.

(50,000)

Other Paid-in Capital – S Co.

(100,000)

Retained Earnings – S Co.

(250,000)

Net Sales

(650,000)

(340,000)

Cost of Goods Sold

370,000

180,000

Operating Expenses

170,000

100,000

Subsidiary Income

(56,640)

Dividends Declared – P Co.

20,000

Dividends Declared – S Co.

9,000

Treasury Stock

44,000

-0-

-0-

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.

Prepare the D&D schedule for the 1/1/X1 acquisition.

b.

Prepare a schedule to determine the change in Parent’s interest in Sub.

c.

Prepare the journal entry the parent needed to adjust its interest in Sub. (Note that it has already been included in the parent’s trial

balance.)

d.

Prepare, in journal form, all elimination entries necessary for the 12/31/X2 consolidation worksheet.

85%

15%

Entity

Parent

NCI

Entity FV

373,529

317,500

56,029

Book value:

Common Stock

50,000

Paid-in Capital in Excess of Par

100,000

RE 1/1/X1

200,000

Book value:

350,000

297,500

52,500

Excess (Goodwill)

23,529

20,000

3,529

36. On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary

Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings

of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common

stock, 10% of the stock outstanding on that date. The price paid was $44,000.

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.

Prepare an analysis to determine Parent’s revised ownership interest following Sub’s treasury stock transaction.

b.

Complete the Figure 8-11 worksheet for consolidated financial statements for 20X2

Sub shares Issued

10,000

10,000

Sub outstanding

10,000

9,000

Parent percentage

85.0%

94.4%

Sub equity 1/1/X2

400,000

400,000

Remaining FV adj

23,529

23,529

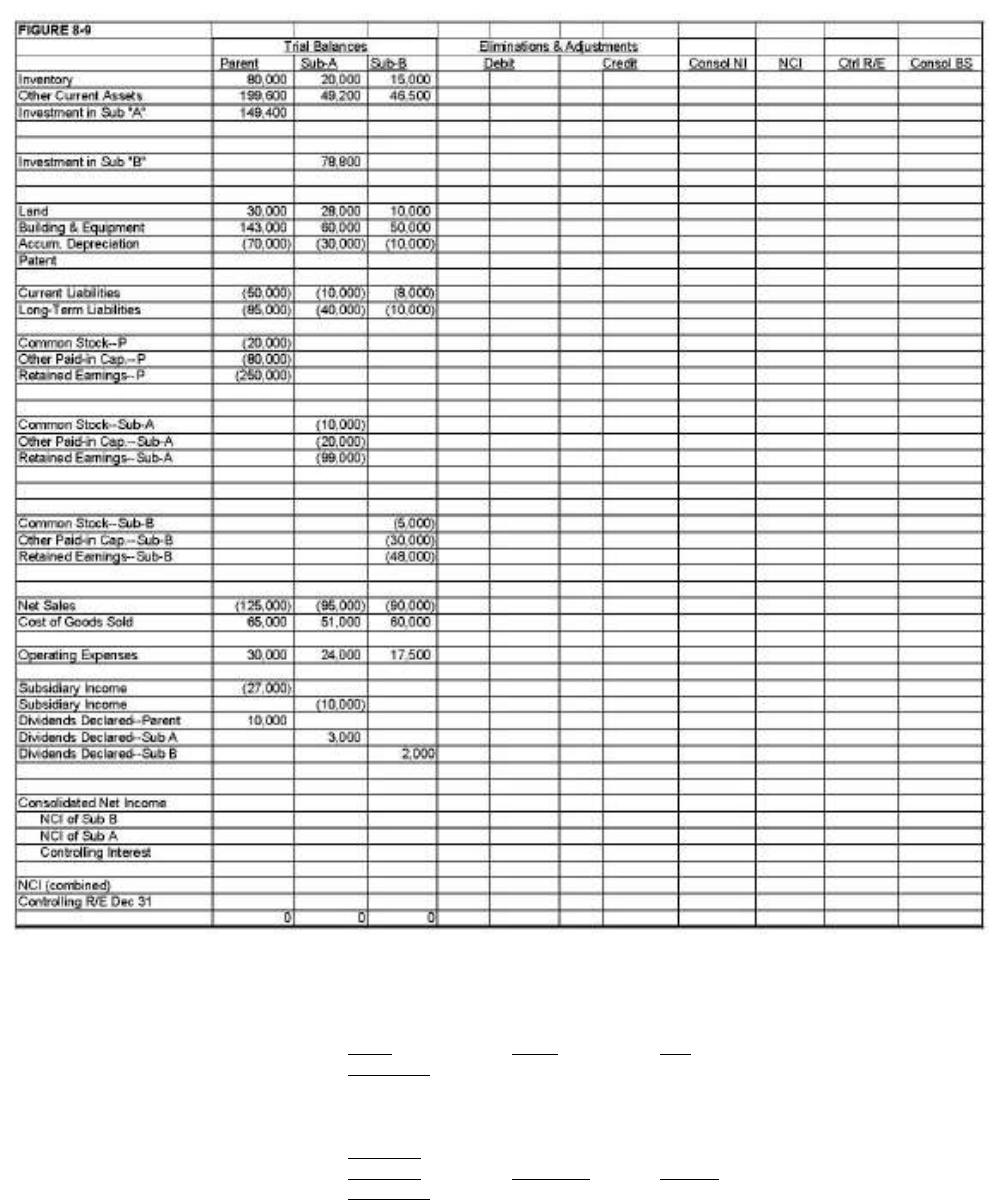

37. On January 1, 20X1, Parent Company purchased 90% of the common stock of Sub-A Company for

$90,000. On this date, Sub-A had common stock, other paid-in capital, and retained earnings of $10,000,

$20,000, and $60,000 respectively.

On January 1, 20X2, Sub-A Company purchased 80% of the common stock of Sub-B Company for $64,000.

On this date, Sub-B Company had common stock, other paid-in capital, and retained earnings of $5,000,

$30,000, and $40,000 respectively.

Any excess of cost over book value on either purchase is due to a patent, to be amortized over ten years.

Both Parent and Sub-A have accounted for their investments using the simple equity method.

During 20X2, Sub-B sold merchandise to Sub-A for $20,000, of which one-fourth is still held by Sub-B on

December 31, 20X2. Sub-B’s usual gross profit is 40%. During 20X3, Sub-B sold more goods to Sub-A for

$30,000, of which $10,000 is still on hand on December 31, 20X3.

Required:

Complete the Figure 8-9 worksheet for consolidated financial statements for 20X3.

Determination and Distribution of Excess Schedule for Sub-A:

Entity

Parent

NCI

Entity FV

100,000

90,000

10,000

Book value:

Common Stock ($10)

10,000

Paid-in Cap in Excess of Par

20,000

RE 1/1/X1

60,000

Book value:

90,000

81,000

9,000

Excess-attributable to patent

10,000

Determination and Distribution of Excess Schedule for Sub-B:

Eliminate 90% of Sub-A Company equity balances at the beginning of the year against the Parent’s investment account.

Distribute the $10,000 excess of cost over book value to the patent.

Sub B

NCI-B

Sub A

NCI-A

Parent

Amortize B’s patent

(500)

Defer profit in End Inventory

(4,000)

Adjusted income — Sub A

27,000

2,700

24,300

38. Paula Inc. purchased an 80% interest in the Sharon Co. for $480,000 on January 1, 20X1, when Sharon Co.

had the following stockholders’ equity:

Common stock, $10 par

$200,000

Retained earnings

300,000

Total equity

$500,000

Any excess is attributable to goodwill.

On January 1, 20X3, Sharon Co. purchased a 10% interest in the Paula Inc. at a price equal to book value. Both firms maintain investments under the

cost method.

Required:

a.

Complete the Figure 8-11 partial worksheet for December 31, 20X3, assuming the use of the treasury stock method.

b.

Calculate the distribution of income for 20X3, assuming that internally generated net income is $50,000 for Paula and $20,000 for Sharon.

Figure 8-11

Paula Inc. and Sharon Co.

Consolidated Partial Worksheet

For the Year Ended December 31, 20X3

Trial Balance

Eliminations

and

Adjustment

s

Account Titles

Paula Inc.

Sharon Co.

Debit

Credit

Investment in Sharon Co.

480,000

Investment in Paula Inc.

80,000

Goodwill

Common Stock – Sharon Co.

(200,000)

Retained Earnings – Sharon Co.

(400,000)

Common Stock – Paula Inc.

(200,000)

Retained Earnings – Paula Inc.

(600,000)

Treasury Stock

Determination and Distribution of Excess Schedule:

Entity

Parent

NCI

Entity FV

600,000

480,000

120,000

Book value:

Common Stock ($10)

200,000

RE 1/1/X1

300,000

Book value:

500,000

400,000

100,000

Excess-attributable to goodwill

100,000

39. Two types of intercompany stock purchases significantly complicate the consolidation process. The first

occurs when the subsidiary issues added shares of stock in a public issue and the parent buys a portion of the

shares. The second occurs when the subsidiary purchases outstanding shares of the parent company.

Required:

a.

Discuss the current theoretical consolidation procedure for situations in which the parent buys a portion of the newly issued subsidiary

shares that is (1) equal to its existing ownership percentage, (2) greater than its existing ownership percentage, and (3) less than its existing

ownership percentage.

b.

Discuss the most widely supported, current theoretical consolidation procedures used when the subsidiary purchases outstanding common

stock shares of the parent.

and there is no equity adjustment.

and distribution of excess schedule for the added interest. There will be separate

compared to the equity interest after the issuance. If there is an increase, paid-in capital

in excess of par increases. If there is a decrease, paid-in capital in excess of par

decreases.