Chapter 1—Business Combinations: New Rules for a Long–

Standing Business Practice Key

1. An economic advantage of a business combination includes

2. One large Midwestern bank’s acquisition of another midwestern bank would be an example of a:

3. A large nation-wide bank’s acquisition of a major investment advisory firm would be an example of a:

4. A building materials company’s acquisition of a television station would be an example of a:

5. A tax advantage of business combination can occur when the existing owner of a company sells out and

receives:

6. A controlling interest in a company implies that the parent company

7. Some advantages of obtaining control by acquiring a controlling interest in stock include all but:

8. A(n) ________________ occurs when the management of the target company purchases a controlling interest

in that company and the company incurs a significant amount of debt as a result.

9. Acquisition costs such as the fees of accountants and lawyers that were necessary to negotiate and

consummate the purchase are

10. Which of the following costs of a business combination can be deducted from the value assigned to paid-in

capital in excess of par?

11. When determining the fair values of assets acquired in an acquisition, the highest level of measurement per

GAAP is

12. Company B acquired the net assets of Company S in exchange for cash. The acquisition price exceeds the

fair value of the net assets acquired. How should Company B determine the amounts to be reported for the plant

and equipment, and for long-term debt of the acquired Company S?

Plant and Equipment Long-Term Debt

13. Crystal Co. purchased all of the common stock of Sill Corp. on January 1 of the current year. Five years

prior to the acquisition, Sill Corp. had issued 30-year bonds bearing an interest rate of 8%. At the time of the

acquisition, the prevailing interest rate for similar bonds was 5%. These bonds should be included in the

consolidated balance sheet at

14. ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following

information was available related to Comb’s balance sheet:

Book Value

Fair Value

Current Assets

$50,000

$ 50,000

Building

80,000

100,000

Equipment

40,000

50,000

Liabilities

30,000

30,000

What is the amount recorded by ACME for the Building?

15. ABC Co. is acquiring XYZ Inc. XYZ has the following intangible assets:

Patent on a product that is deemed to have no useful life $10,000.

Customer list with an observable fair value of $50,000.

A 5-year operating lease with favorable terms having a discounted present value of $8,000.

Identifiable research and development costs of $100,000.

ABC will record how much for acquired Intangible Assets from the purchase of XYZ Inc?

16. Which of the following would not be considered an identifiable intangible asset?

17. A contingent liability of an acquiree

18. Goodwill results when:

19. Cozzi Company is being purchased and has the following balance sheet as of the purchase date:

Current assets

$200,000

Liabilities

$ 90,000

Fixed assets

180,000

Equity

290,000

Total

$380,000

Total

$380,000

The price paid for Cozzi’s net assets is $500,000. The fixed assets have a fair value of $220,000, and the liabilities have a fair value of $110,000. The

amount of goodwill to be recorded in the purchase is:

20. Publics Company acquired the net assets of Citizen Company during 20X5. The purchase price was

$800,000. On the date of the transaction, Citizen had no long-term investments in marketable equity securities

and $400,000 in liabilities, of which the fair value approximated book value. The fair value of Citizen assets on

the acquisition date was as follows:

Current assets

$ 800,000

Noncurrent assets

600,000

$1,400,000

How should Publics account for the difference between the fair value of the net assets acquired and the acquisition price of $800,000?

21. ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following

information was available related to Comb’s balance sheet:

Book Value

Fair Value

Current Assets

$50,000

$ 50,000

Building

80,000

100,000

Equipment

40,000

50,000

Liabilities

30,000

30,000

What is the amount of goodwill or gain related to the acquisition?

22. Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded

assets and liabilities was $1,500,000 and $250,000, respectively. Jackson also had unrecorded copyrights valued

at $150,000 and its direct costs related to the acquisition were $50,000. What was the amount of the goodwill

related to the acquisition?

23. Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded

assets and liabilities was $1,500,000 and $250,000, respectively. Jackson also had in-process research and

development projects valued at $150,000 and its pension plan’s projected benefit obligation exceeded the plan

assets by $50,000. What was the amount of the goodwill related to the acquisition?

24. Orbit Inc. purchased Planet Co. on January 1, 20X3. At that time an existing patent having a 5-year life was

not recorded as a separately identified intangible asset. At the end of fiscal year 20X4, it is determined the

patent is valued at $20,000, and goodwill has a book value of $100,000. How should intangible assets be

reported at the beginning of fiscal year 20X5?

25. Orbit Inc. purchased Planet Co. on January 1, 20X3. At that time an existing patent having a 5-year

estimated life was assigned a provisional value of $10,000 and goodwill was assigned a value of $100,000. By

the end of fiscal year 20X3, better information was available that indicated the fair value of the patent was

$20,000. How should intangible assets be reported at the beginning of fiscal year 20X4?

26. Balter Inc. acquired Jersey Company on January 1, 20X5. When the purchase occurred Jersey Company had

the following information related to fixed assets:

Land

$ 80,000

Building

200,000

Accumulated Depreciation

(100,000)

Equipment

100,000

Accumulated Depreciation

(50,000)

The building has a 10-year remaining useful life and the equipment has a 5-year remaining useful life. The fair value of the assets on that date were:

Land

$100,000

Building

130,000

Equipment

75,000

What is the 20X5 depreciation expense Balter will record related to purchasing Jersey Company?

27. Polk issues common stock to acquire all the assets of the Sam Company on January 1, 20X5. There is a

contingent share agreement, which states that if the income of the Sam Division exceeds a certain level during

20X5 and 20X6, additional shares will be issued on January 1, 20X7. The impact of issuing the additional

shares is to

28. Jones company acquired Jackson Company for $2,000,000 cash. At that time, the fair value of recorded

assets and liabilities was $1,500,000 and $250,000, respectively. If Jackson meets specified sales targets, Jones

is required to pay an additional $200,000 in cash per the acquisition agreement. Jones estimates the probability

of this to be 50%. The direct costs related to the acquisition were $50,000. What was the amount of the

goodwill related to the acquisition?

29. ACME Co. paid $110,000 for the net assets of Comb Corp. At the time of the acquisition the following

information was available related to Comb’s balance sheet:

Book Value

Fair Value

Current Assets

$50,000

$ 50,000

Building

80,000

100,000

Equipment

40,000

50,000

Liabilities

30,000

30,000

What is the amount of gain or loss on disposal of business should Comb Corp. recognize?

30. Vibe Company purchased the net assets of Atlantic Company in a business combination accounted for as a

purchase. As a result, goodwill was recorded. For tax purposes, this combination was considered to be a tax-free

merger. Included in the assets is a building with an appraised value of $210,000 on the date of the business

combination. This asset had a net book value of $70,000. The building had an adjusted tax basis to Atlantic (and

to Vibe as a result of the merger) of $120,000. Assuming a 40% income tax rate, at what amount should Vibe

record this building on its books after the purchase?

Deferred Tax

Building Liability

31. When an acquisition of another company occurs, FASB requires disclosing all of the following except:

32. While performing a goodwill impairment test, the company had the following information:

Estimated implied fair value of reporting unit

$420,000

Fair value of net assets on date of measurement (without goodwill)

$400,000

Existing net book value of reporting unit (without goodwill)

$380,000

Book value of goodwill

$ 60,000

Based upon this information the proper conclusion is:

33. In performing the impairment test for goodwill, the company had the following 20X6 and 20X7 information

available.

20X6

20X7

Fair value of the reporting unit

$350,000

$400,000

Net book value (including $50,000 goodwill)

$360,000

$380,000

Assume that the carrying value of the identifiable assets are a reasonable approximation of their fair values. Based upon this information what are the

20X6 and 20X7 adjustment to goodwill, if any?

20X6 20X7

34. Which of the following income factors should not be considered in expected future income when estimating

the value of goodwill?

35. Internet Corporation is considering the acquisition of Homepage Corporation and has obtained the following

audited condensed balance sheet:

Homepage Corporation

Balance Sheet

December 31, 20X5

Assets

Liabilities and

Equity

Current assets

$ 40,000

Current Liabilities

$ 60,000

Land

20,000

Capital Stock (50,000

Buildings (net)

80,000

shares, $1 par value)

50,000

Equipment (net)

60,000

Other Paid-in Capital

20,000

Retained Earnings

70,000

$200,000

$200,000

Internet also acquired the following fair values for Homepage’s assets and liabilities:

Current assets

$ 55,000

Land

60,000

Buildings (net)

90,000

Equipment (net)

75,000

Current Liabilities

(60,000)

$220,000

Internet and Homepage agree on a price of $280,000 for Homepage’s net assets. Prepare the necessary journal entry to record the purchase given the

following scenarios:

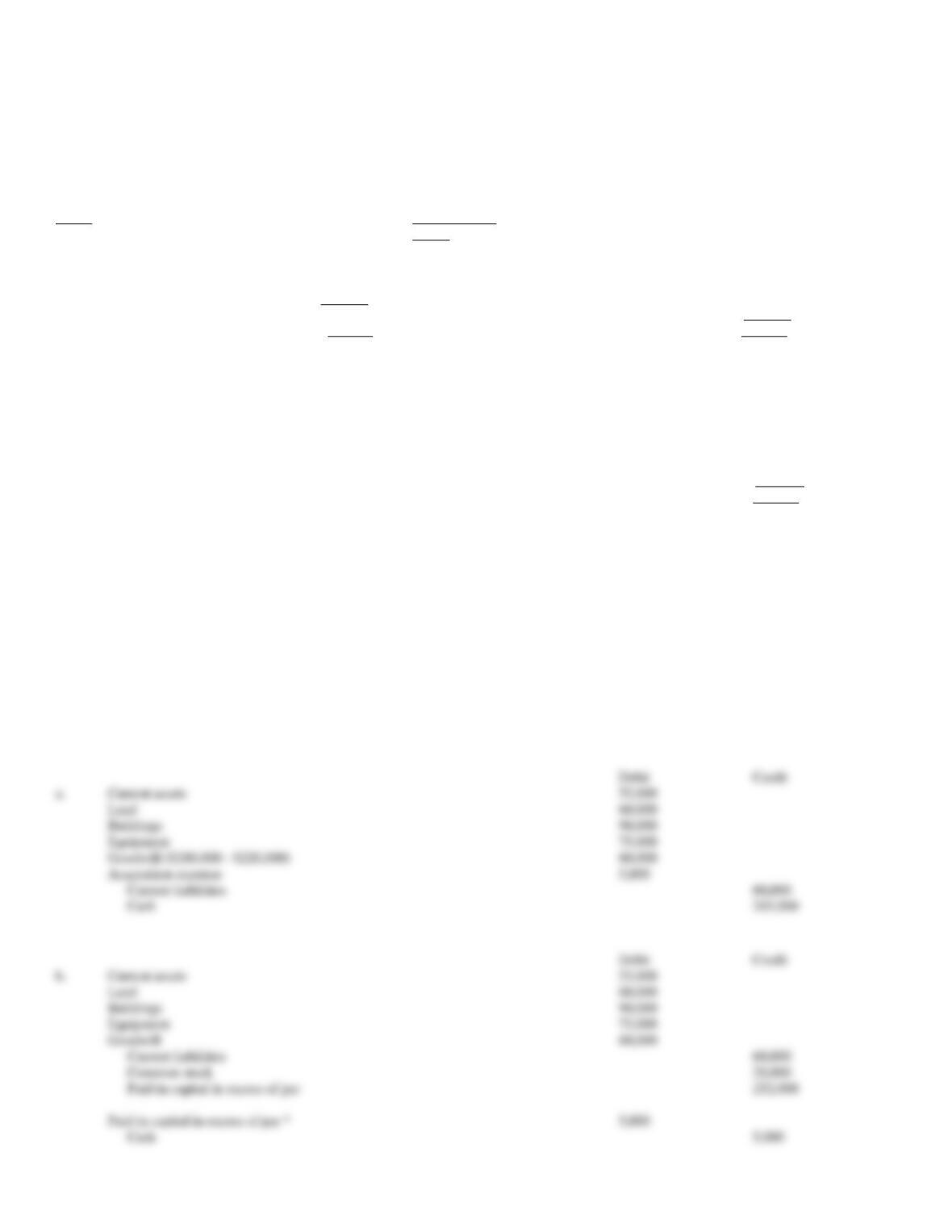

a.

Internet pays cash for Homepage Corporation and incurs $5,000 of acquisition costs.

b.

Internet issues its $5 par value stock as consideration. The fair value of the stock at the acquisition date is $50 per share. Additionally,

Internet incurs $5,000 of security issuance costs.

Debit

Credit

a.

Current assets

55,000

Land

60,000

Buildings

90,000

Equipment

75,000

Goodwill ($280,000 – $220,000)

60,000

Acquisition expense

5,000

Current liabilities

60,000

Cash

285,000

Debit

Credit

b.

Current assets

55,000

Land

60,000

Buildings

90,000

Equipment

75,000

Goodwill

60,000

Current liabilities

60,000

36. On January 1, 20X5, Brown Inc. acquired Larson Company’s net assets in exchange for Brown’s common

stock with a par value of $100,000 and a fair value of $800,000. Brown also paid $10,000 in direct acquisition

costs and $15,000 in stock issuance costs.

On this date, Larson’s condensed account balances showed the following:

Book Value

Fair Value

Current Assets

$280,000

$370,000

Plant and Equipment

440,000

480,000

Accumulated Depreciation

(100,000)

Intangibles – Patents

80,000

120,000

Current Liabilities

(140,000)

(140,000)

Long-Term Debt

(100,000)

(110,000)

Common Stock

(200,000)

Other Paid-in Capital

(120,000)

Retained Earnings

(140,000)

Required:

Record Brown’s purchase of Larson Company’s net assets.

Acquisition price

$800,000

Fair value of acquired net assets:

Current assets

$370,000

Plant and equipment

480,000

Intangibles – patents

120,000

Current liabilities

(140,000)

Long-term debt

(110,000)

720,000

Goodwill

$ 80,000

Debit

Credit

Current Assets

$370,000

Plant and Equipment

480,000

Intangibles – Patents

120,000

Intangibles – Goodwill

80,000

Current Liabilities

$140,000

Long-term Debt

110,000

Common Stock

100,000

Paid-in Capital in Excess of Par

700,000

Acquisition expenses*

25,000

Cash

25,000

37. On January 1, 20X5, Zebb and Nottle Companies had condensed balance sheets as shown below:

Zebb

Nottle

Company

Company

Current Assets

$1,000,000

$ 600,000

Plant and Equipment

1,500,000

800,000

$2,500,000

$1,400,000

Current Liabilities

$ 200,000

$ 100,000

Long-Term Debt

300,000

300,000

Common Stock, $10 par

1,400,000

400,000

Paid-in Capital in Excess of Par

0

100,000

Retained Earnings

600,000

500,000

$2,500,000

$1,400,000

Required:

Record the acquisition of Nottle’s net assets, the issuance of the stock and/or payment of cash, and payment of the related costs. Assume that Zebb

issued 30,000 shares of new common stock with a fair value of $25 per share and paid $500,000 cash for all of the net assets of Nottle. Acquisition

costs of $50,000 and stock issuance costs of $20,000 were paid in cash. Current assets had a fair value of $650,000, plant and equipment had a fair

value of $900,000, and long-term debt had a fair value of $330,000.

Current Assets

650,000

Plant and Equipment

900,000

Goodwill**

130,000

Acquisition Expenses*

70,000

Current Liabilities

100,000

Long-Term Debt

330,000

Common Stock

300,000

Paid-in Capital in Excess of Par

450,000

Cash ($500,000 + 70,000)

570,000

Acquisition price:

Cash

$ 500,000

Common stock issued (30,000 shares x $25)

750,000

$1,250,000

Fair value of acquired net assets:

Current assets

$650,000

Plant and equipment

900,000

Current liabilities

(100,000)

Long-term debt

(330,000)

1,120,000

Goodwill

$ 130,000