30. On 1/1/X1 Poncho acquired an 80% interest in Stroller for $560,000 when Stroller’s equity consisted of

$530,000 paid-in capital and $100,000 Retained Earnings. Any excess of purchase price over was attributed to

goodwill.

On January 1, 20X6, Stroller had the following stockholders’ equity:

Common stock ($20 par)

$180,000

Paid-in capital in excess of par

350,000

Retained earnings

220,000

Total stockholders’ equity

$750,000

On January 2, 20X6, Company S sold 1,000 additional shares to noncontrolling shareholders in a public offering for $50 per share. Stroller’s net

income for 20X6 was 80,000. Poncho uses the simple equity method to record its investment in Stroller.

Required:

a.

Prepare Poncho’s journal entry to adjust its Investment in Stroller account on January 2, 20X6. Assume that Poncho has $500,000

additional paid-in capital.

b.

Determine the carrying value of Poncho’s Investment in Stroller account on December 31, 20X6.

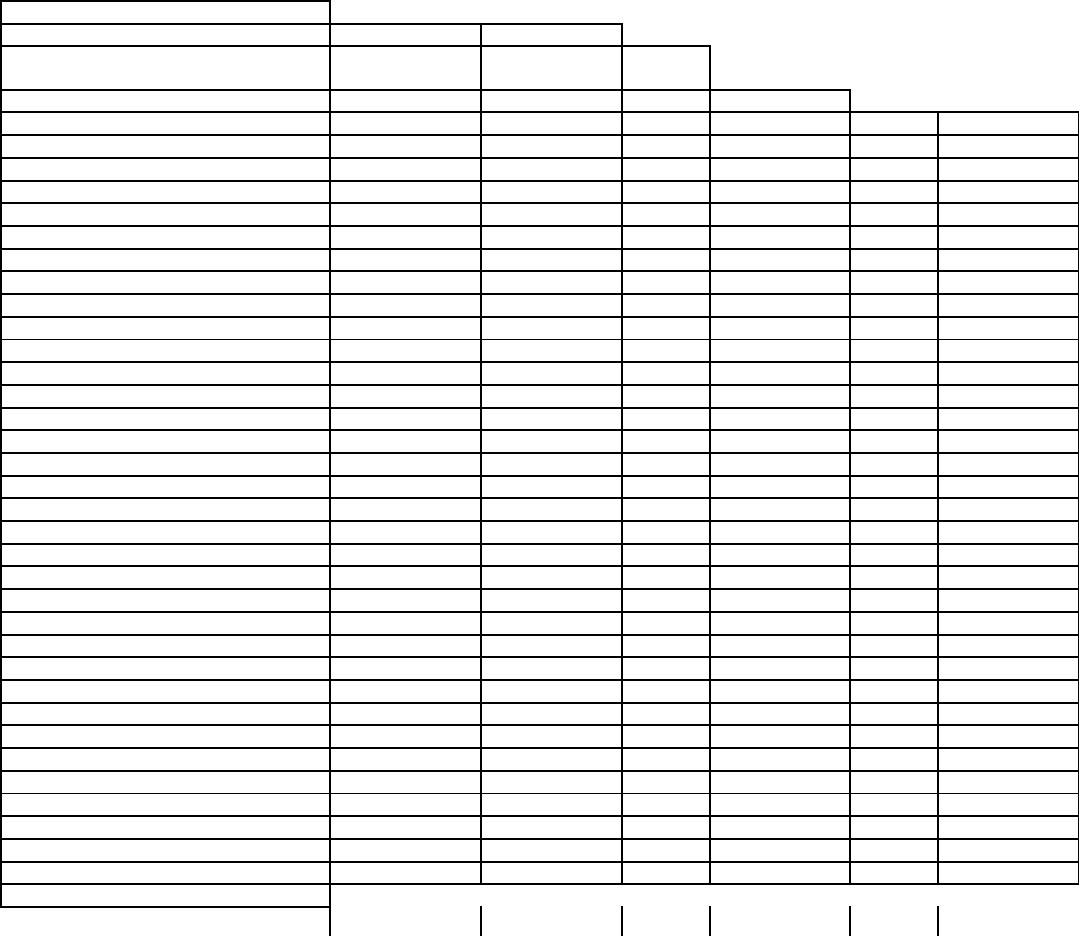

80%

20%

Entity

Parent

NCI

Entity FV

$700,000

$560,000

$140,000

Book value:

Common Stock

180,000

Paid-in Cap in Excess of Par

350,000

RE 1/1/X1

100,000

Book value:

630,000

504,000

126,000

Excess

70,000

56,000

14,000

Goodwill

70,000

Sub equity 1/1/X1

$630,000

Unamortized excess

70,000

Increase in RE (now $220,000)

120,000

Equity adjusted for fair value

$820,000

Sub equity prior to new issue

$820,000

$656,000

Issue 1,000 shares @ $50

50,000

Sub equity after new issue

$870,000

$626,400

Decrease in investment

$ 29,600

Paid-in Capital in Excess of Par

29,600

Investment in Stroller

29,600

*Sub’s outstanding shares before new issue

9,000

(180,000 / 20)

Sub issued

1,000

Sub outstanding after new issue

10,000

Parent holds 7,200 shares from its original investment

31. On January 1, 20X1, Parent Company purchased 9,000 shares of the common stock of Subsidiary Company

for $405,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares

issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively.

On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 10 years.

Subsidiary’s net income and dividends for two years were:

20X1

20X2

Net income

$50,000

$80,000

Dividends

10,000

20,000

On January 1, 20X2, Subsidiary Company sold an additional 2,000 shares of common stock for $50 per share. Parent purchased 1,200 shares of the

new issue, and noncontrolling shareholders purchased the other 800.

For both 20X1 and 20X2, Parent Company has applied the simple equity method.

Required:

a.

Prepare a schedule that measures Parent’s change in interest ownership effective with Sub’s issuance of the 2,000 shares and Parent’s

acquisition of 1,200 of those shares.

b.

Prepare Parent’s journal entry to record its purchase of the 1,200 shares on 1/1/X2

c.

Prepare a schedule showing the 12/31/X2 balance of Parent’s Investment in Sub account

Sub share issued

10,000

10,000

New issue

–

2,000

Sub outstanding

10,000

12,000

Parent holds

9,000

10,200

Parent percentage

90.0%

85.0%

Sub equity 1/1/X2

440,000

440,000

New equity

100,000

Remaining FV adj

45,000

45,000

485,000

585,000

Parent percentage

90.0%

85.0%

Parent interest

436,500

497,250

Change in interest

60,750

Price paid

(60,000)

Increase(decrease) in parent’s equity

Investment in Subsidiary

60,750

Paid-in Capital in Excess of Par-Parent

750

Cash

60,000

32. On January 1, 20X1, Parent Company purchased 8,000 shares of the common stock of Subsidiary Company

for $350,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares

issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively.

On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years. Parent

Company uses the simple equity method to account for its investment in Sub.

Subsidiary’s net income and dividends for two years were:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

30,000

On January 1, 20X2, Subsidiary Company sold an additional 2,500 shares of common stock to noncontrolling shareholders for $50 per share.

In the last quarter of 20X2, Subsidiary Company sold goods to Parent Company for $40,000. Subsidiary’s usual gross profit on intercompany sales is

40%. On December 31, $7,500 of these goods are still in Parent’s ending inventory.

Required: Prepare the following items

a.

Determination and distribution schedule effective 1/1/X1

b.

Parent’s journal entry to record change in ownership interest due to Sub’s issuance of additional shares on 1/1/X2. Support with

schedule of Parent’s ownership interest before and after the 1/1/X2 issuance.

c.

All necessary elimination entries necessary to prepare the consolidating worksheet on 12/31/X2

80%

20%

Entity

Parent

NCI

Entity FV

437,500

350,000

87,500

Book value:

Common Stock

50,000

Paid-in capital in excess of par

150,000

RE 1/1/X1

200,000

Book value:

400,000

320,000

80,000

Excess

37,500

30,000

7,500

Patent

37,500

15 years

2,500 annual

Investment in Sub

4,000

Paid-in Capital in Excess of Par-Parent

4,000

33. On January 1, 20X1, Parent Company purchased 8,000 shares of the common stock of Subsidiary Company

for $350,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares

issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively.

On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years. Parent

Company uses the simple equity method to account for its investment in Sub.

Subsidiary’s net income and dividends for two years were:

20X1

20X2

Net income

$50,000

$90,000

Dividends

10,000

30,000

On January 1, 20X2, Subsidiary Company sold an additional 2,500 shares of common stock to noncontrolling shareholders for $50 per share.

In the last quarter of 20X2, Subsidiary Company sold goods to Parent Company for $40,000. Subsidiary’s usual gross profit on intercompany sales is

40%. On December 31, $7,500 of these goods are still in Parent’s ending inventory.

Required:

Complete the Figure 8-6 worksheet for consolidated financial statements for 20X2.

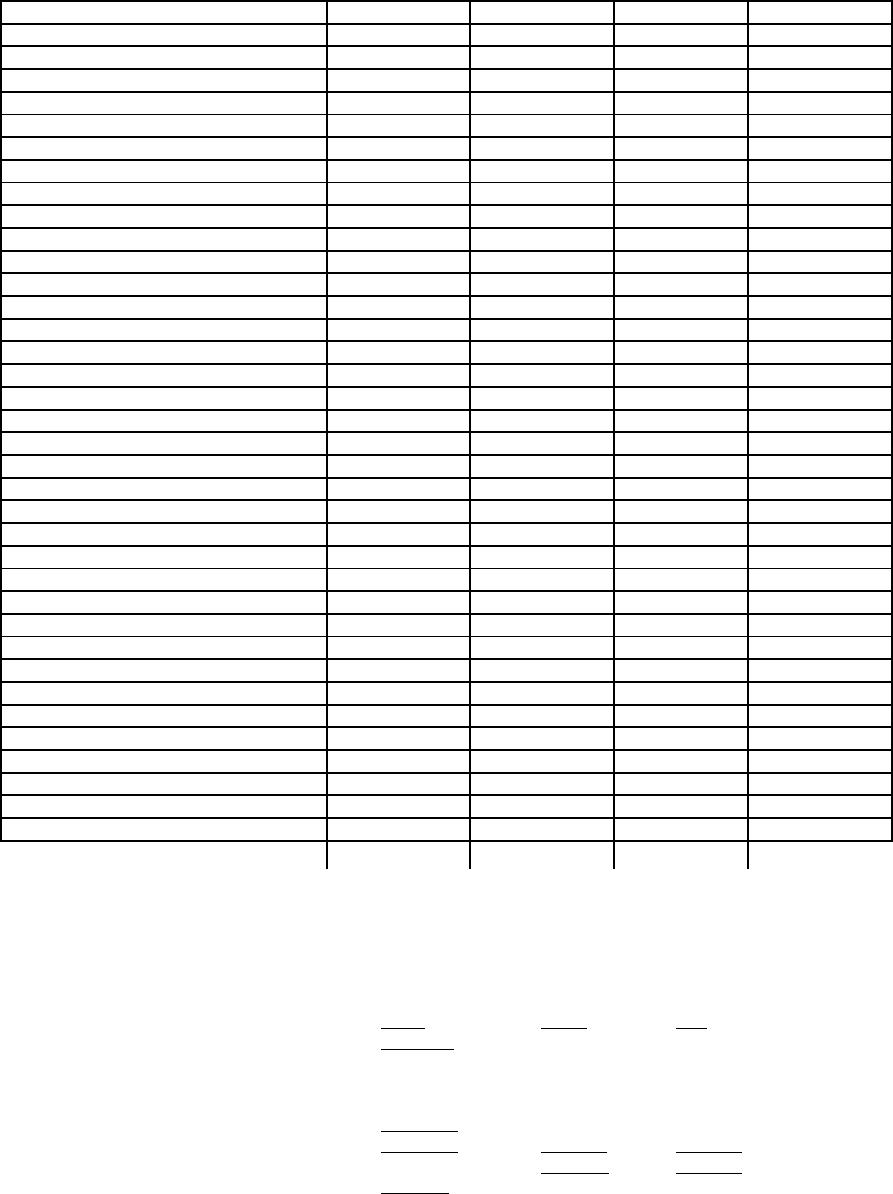

Figure 8-6

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

52,000

Other Current Assets

112,200

373,000

Investment in Sub. Company

424,400

Land

50,000

80,000

Buildings and Equipment

350,000

320,000

Accumulated Depreciation

(100,000)

(60,000)

Patent

Current Liabilities

(120,000)

(40,000)

Long-Term Liabilities

(200,000)

(100,000)

Common Stock – P Co.

(200,000)

Other Paid-in Capital – P Co.

(108,000)

Retained Earnings – P Co.

(201,000)

Common Stock – S Co.

(62,500)

Other Paid-in Capital – S Co.

(262,500)

Retained Earnings – S Co.

(240,000)

Net Sales

(520,000)

(450,000)

Cost of Goods Sold

300,000

260,000

Operating Expenses

120,000

100,000

Subsidiary Income

(57,600)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

30,000

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Land

Buildings and Equipment

Accumulated Depreciation

Patent

Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Subsidiary Income

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

0

0

D&D Schedule

1/1/X1

80%

20%

Entity

Parent

NCI

Entity FV

437,500

350,000

87,500

Book value:

Common Stock

50,000

Paid-in capital in excess of par

150,000

RE 1/1/X1

200,000

Book value:

400,000

320,000

80,000

Excess

37,500

30,000

7,500

Patent

37,500

15 years

2,500 annual

amortization

34. Parrot, Inc. purchased a 60% interest in Swallow Company on January 1, 20X1, for $204,000. Any excess

of cost was attributable to goodwill.

On January 1, 20X4, Swallow purchased 2,400 of its shares held by noncontrolling stockholders for $50 per

share. Swallow equity balances on various dates were as follows:

January 1,

December 31,

January 1,

20X1

20X3

20X5

Capital stock ($10 par)

$120,000

$120,000

$120,000

Paid-in capital in excess of par

60,000

60,000

60,000

Retained earnings

160,000

240,000

340,000

Treasury stock (at cost) *

(120,000)

*(2,400 x $50)

Parrot maintains its investment at cost; Swallow recorded the purchase of its shares as treasury stock at cost.

Required:

Prepare the necessary determination and distribution of excess schedules and all Figure 8-7 worksheet eliminations and adjustments on the following

partial worksheet prepared on December 31, 20X5:

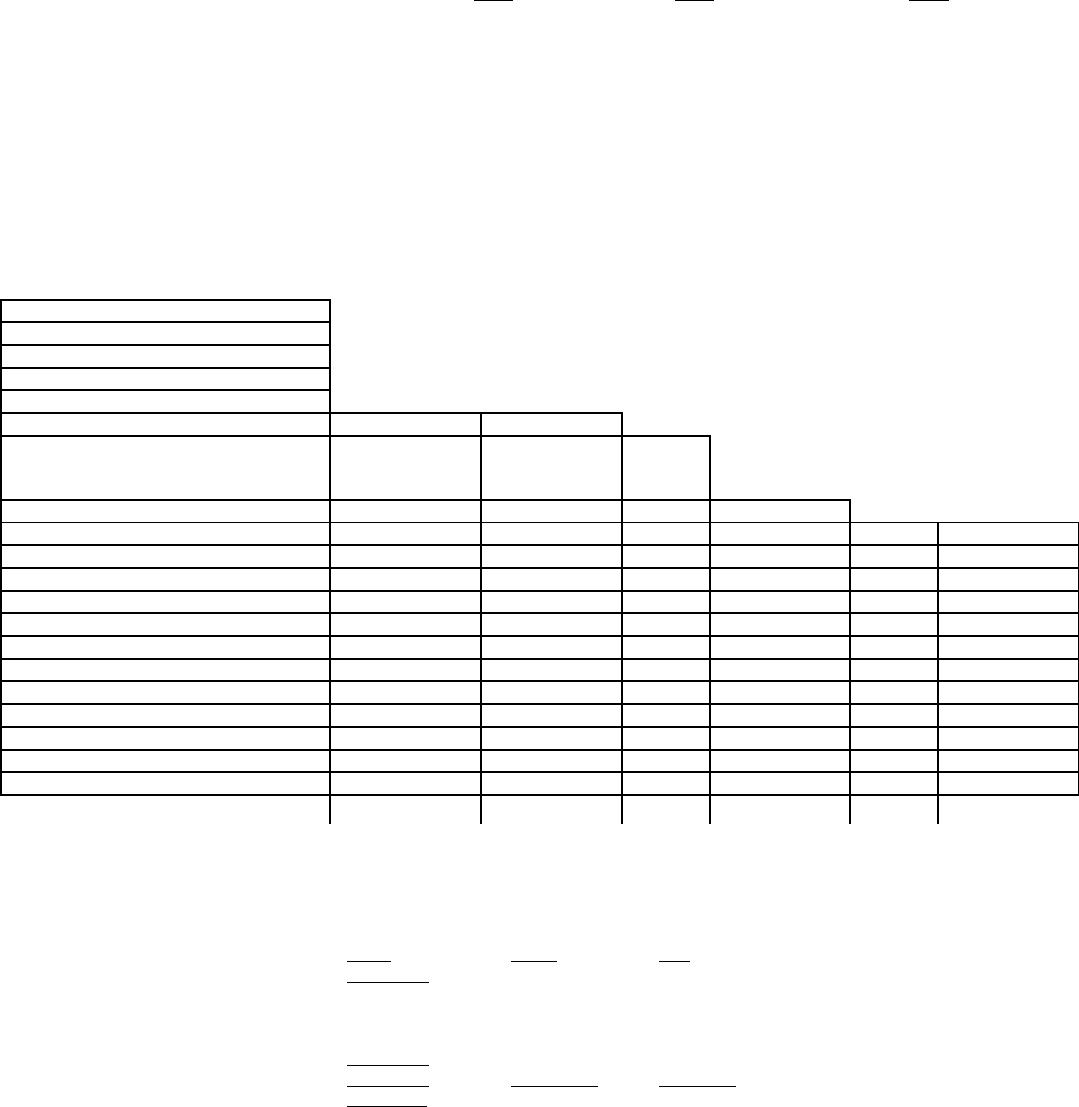

Figure 8-7

Parrot and Swallow

Consolidated Partial Worksheet

For the Year Ended December 31, 20X5

Trial Balance

Eliminations

and

Adjustment

s

Account Titles

Parrot

Swallow

Debit

Credit

Investment in Swallow

204,000

Goodwill

Common Stock – S

(120,000)

Paid-in Cap in Excess of Par – S

(60,000)

Retained Earnings – S

(340,000)

Retained Earnings – P

(300,000)

Treasury Stock (at cost)

120,000

Determination and Distribution of Excess Schedule:

Entity

Parent

NCI

Entity FV

340,000

204,000

136,000

Book value:

Common Stock ($10)

120,000

Paid-in Cap in Excess of Par

60,000

RE 1/1/X1

160,000

Book value:

340,000

204,000

136,000

Excess

-0-