67.

Gotham City

General Fund Trial Balance

June 30, 20X9

Debit

Credit

Cash

230,000

Taxes Receivable—Current

150,000

Allowances for Uncollectible Current Taxes

10,000

Taxes Receivable—Delinquent

25,000

Allowances for Uncollectible Delinquent Taxes

20,000

Inventory of Supplies

55,000

Vouchers Payable

110,500

Tax Anticipation Notes Payable

100,000

Fund Balance—Nonspendable

55,000

Fund Balance—Unassigned

50,000

Revenues

2,455,000

Expenditures

2,255,000

Other Financing Sources

110,000

Other Financing Uses

95,500

Encumbrances

125,000

Fund Balance—Assigned

125,000

Estimated Revenues

2,450,000

Appropriations

2,300,000

Estimated Other Financing Sources

110,000

Estimated Other Financing Uses

96,000

Budgetary Fund Balance—Unassigned

164,000

5,545,500

5,545,500

The Inventory of Supplies and Fund Balance—Nonspendable have been adjusted to reflect ending inventory. The beginning inventory balance was

$0. Fund Balance—Unassigned was $5,000 before the adjustment.

Using the information above, prepare the closing entries for the General Fund of Gotham City on June 30, 20X9.

Appropriations

2,300,000

Estimated Other Financing Uses

96,000

Budgetary Fund Balance—Unassigned

164,000

Estimated Revenue

2,450,000

Estimated Other Financing Sources

110,000

Revenues

2,455,000

Other Financing Sources

110,000

Expenditures

2,255,000

Other Financing Uses

95,500

Encumbrances

125,000

Fund Balance—Unassigned

89,500

68. The pre-closing trial balance of the General Fund of Volter Village at the end of its fiscal year, June 30,

20X1, is as follows:

Cash

19,800

Tax Receivable—Delinquent

40,000

Allowance for Uncollectible Delinquent Taxes

8,400

Vouchers Payable

19,000

Fund Balance—Assigned

22,000

Fund Balance—Unassigned

46,000

Revenues

201,600

Expenditures

215,200

Encumbrances

22,000

Estimated Revenues

200,000

Appropriations

196,000

Budgetary Fund Balance—Unassigned

4,000

497,000

497,000

Required:

a.

Prepare closing entries.

b.

Prepare a statement of revenues, expenditures, and changes in fund balances for the General Fund for the year ended June 30, 20X1.

c.

Prepare the General Fund balance sheet as of June 30, 20X1.

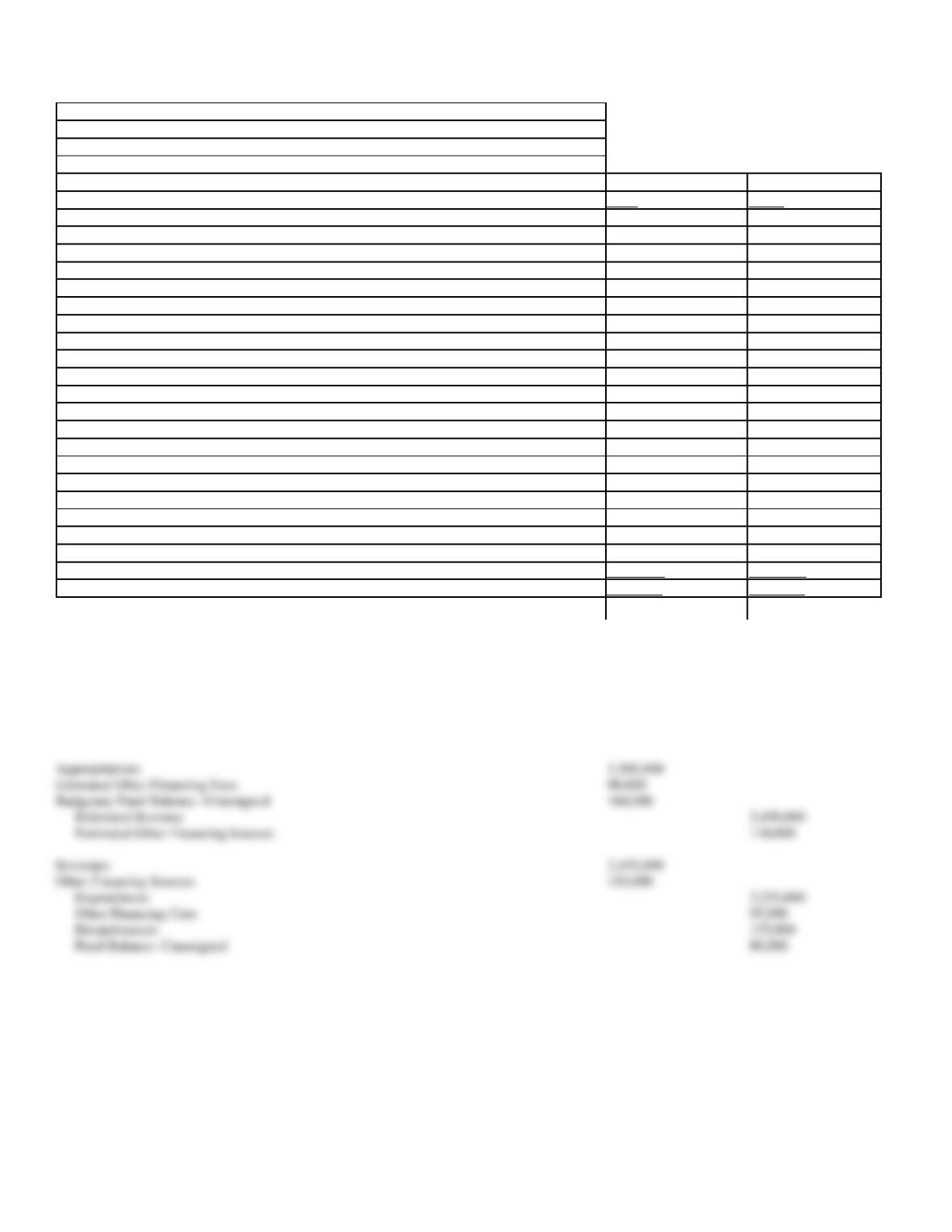

69.

Gotham City

General Fund Trial Balance

June 30, 20X9

Debit

Credit

Cash

230,000

Taxes Receivable—Current

150,000

Allowances for Uncollectible Current Taxes

10,000

Taxes Receivable—Delinquent

25,000

Allowances for Uncollectible Delinquent Taxes

20,000

Inventory of Supplies

55,000

Vouchers Payable

110,500

Tax Anticipation Notes Payable

100,000

Fund Balance—Nonspendable

55,000

Fund Balance—Unassigned

50,000

Revenues

2,455,000

Expenditures

2,255,000

Other Financing Sources

110,000

Other Financing Uses

95,500

Encumbrances

125,000

Fund Balance—Assigned

125,000

Estimated Revenues

2,450,000

Appropriations

2,300,000

Estimated Other Financing Sources

110,000

Estimated Other Financing Uses

96,000

Budgetary Fund Balance—Unassigned

164,000

5,545,500

5,545,500

The Inventory of Supplies and Fund Balance—Nonspendable have been adjusted to reflect ending inventory. The beginning inventory balance was

$0. Fund Balance—Unassigned was $5,000 before the adjustment.

Using the information above, prepare a Statement of Revenues, Expenditures, and Change in Fund Balance—Budget and Actual for the General Fund

for Gotham City for the year end June 30, 20X9.

Gotham City

General Fund Statement of Revenues, Expenditures, and

Change in Fund Balance – Budget to Actual

For the Fiscal Year Ended June 30, 20X9

Favorable

Budget

Actual

(Unfavorable)

Revenues

$2,450,000

$2,455,000

$ 5,000

Expenditures

2,300,000

2,255,000

45,000

Excess of revenues over expenditures

$ 150,000

$ 200,000

$50,000

Other financing sources (uses)

14,000

14,500

500

Excess of revenues and other sources

over expenditures and other uses

$ 164,000

$ 214,500

$50,500

Fund balance July 1, 20X8

5,000

5,000

0

Fund balance June 30, 20X9

$ 169,000

$ 219,500

$50,500

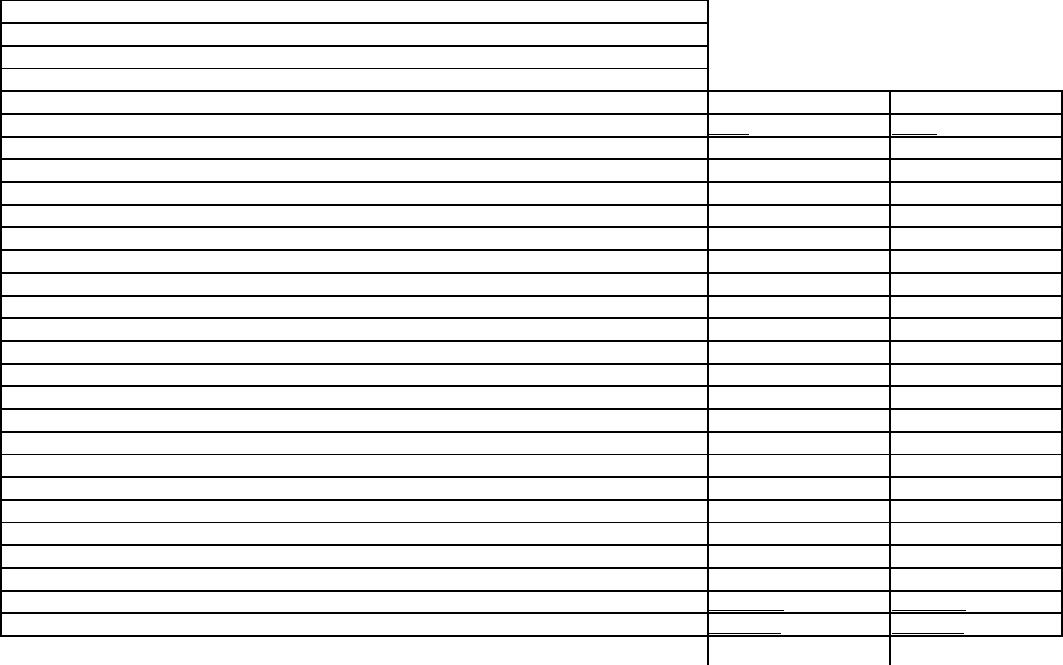

70.

Gotham City

General Fund Trial Balance

June 30, 20X9

Debit

Credit

Cash

230,000

Taxes Receivable—Current

150,000

Allowances for Uncollectible Current Taxes

10,000

Taxes Receivable—Delinquent

25,000

Allowances for Uncollectible Delinquent Taxes

20,000

Inventory of Supplies

55,000

Vouchers Payable

110,500

Tax Anticipation Notes Payable

100,000

Fund Balance—Nonspendable

55,000

Fund Balance—Unassigned

50,000

Revenues

2,455,000

Expenditures

2,255,000

Other Financing Sources

110,000

Other Financing Uses

95,500

Encumbrances

125,000

Fund Balance—Assigned

125,000

Estimated Revenues

2,450,000

Appropriations

2,300,000

Estimated Other Financing Sources

110,000

Estimated Other Financing Uses

96,000

Budgetary Fund Balance—Unassigned

164,000

5,545,500

5,545,500

The Inventory of Supplies and Fund Balance—Nonspendable have been adjusted to reflect ending inventory. The beginning inventory balance was

$0. Fund Balance—Unassigned was $5,000 before the adjustment.

Using the information above, the year-end trial balance for the General Fund of Gotham City, prepare the June 30, 20X9, General Fund balance

sheet for Gotham City.

Assets

Tax receivable—delinquent

$ 25,000

Less allowances for uncollectible delinquent taxes

20,000

5,000

Inventory of supplies

55,000

Total Assets

$430,000

Liabilities:

Vouchers payable

$110,500

Tax anticipation notes payable

100,000

Nonspendable

55,000

Unassigned

39,500

Total Fund Balance

219,500

Accounts closed to Fund Balance:

Other Financing Uses

(95,500)

Ending Fund Balance

$219,500

Fund Balance—Nonspendable

55,000

180,000

71. The following activities took place in the city of Littlewood during 20X2. Make the necessary journal

entries to account for these transactions in the General Fund, including the year end closing entries. Littlewood

does not utilize an encumbrance system.

a.

The budget for 20×2 was approved.

Estimated Revenues

$1,300,000

Estimated Other Financing Sources

50,000

Estimated Operating Expenditures

800,000

Estimated Equipment Purchases

100,000

Estimated Other Financing Uses

10,000

b.

The general tax levy for 20X2 was $1,000,000 with a 5% estimate of uncollectible accounts. The remaining

balance from the 2001 fiscal year was $75,000 in Taxes Receivable-Current with and Allowance of $20,000.

c.

Equipment was purchased that was invoiced at $93,500.

d.

Invoices were received for operating expenditures in the amount of $815,000 and vouchered.

e.

Payment was made on items (c) and (d) above.

f.

Collections of $895,000 on current taxes and $5,000 on Delinquent taxes were received. A state grant was

received in the amount of $250,000.

g.

Fines and fees are collected in the amount of $85,000.

h.

The city sold equipment having a basis of $60,000 in the General Fixed Asset Account Group for $50,000.

72. Consider the following events:

a.

The General Fund vouchered the purchase of trucks for $65,000. The purchase had been encumbered earlier in the year at $60,000.

b.

Several years ago, equipment costing $15,000 was acquired with General Fund Revenues. It was sold for $5,000, with proceeds belonging

to the General Fund.

c.

Early in the year, a citizen donated land appraised at $100,000 to the city. She submitted plans for a new library and agreed to cover the

total cost of construction, paying the company directly as work proceeds. At year end, the building was two-thirds finished, with costs to

date of $300,000.

d.

A snow plow was purchased with General Fund cash for $48,000, which represented a cost of $61,000 less trade-in of $13,000 for an old

snow plow originally purchased for $35,000 from Special Revenue Funds. As an emergency purchase, the acquisition of the new snow

plow had not been encumbered.

Required:

Prepare journal entries to record the events using the General Fund and the General Fixed Assets Account Group:

73. Following is a list of selected transactions for the City of Alpena:

a.

The city used general property taxes to purchase a computer for the police department. The cost of the computer was $30,000. It was not

encumbered.

b.

Joseph Green donated land and a building to the city with book values of $25,000 and $150,000, respectively. When the gift was made, the

appraisal values were $35,000 for the land and $135,000 for the building.

c.

The city sold an old police car originally purchased by the General Fund for $10,000. The selling price was $2,500.

Required:

Make the necessary journal entries in the funds and account groups affected.

General Fund

Expenditures

30,000

Vouchers Payable

30,000

GFAAG

Equipment

30,000

Investment in General Fixed

Assets—General Fund Revenues

30,000

b.

GFAAG

Land

35,000

Building

135,000

Investment in General

Fixed Assets—Donations

170,000

General Fund

Cash

2,500

Other Financing

Source—Disposal of Asset

2,500

GFAAG

Investment in General Fixed

Assets—General Fund Revenues

10,000

Equipment

10,000

74. The following transactions occurred in the City of Maineville during 20X1:

a.

General obligation term bonds with a face value of $2,500,000 were sold for $2,550,000. The proceeds from the bond issue were to be

used to construct a new library and were received by the Capital Projects Fund.

b.

$200,000 was transferred from the General Fund to the Debt Service Fund to begin saving for the retirement of the bonds in transaction a.

at maturity.

c.

$150,000 was transferred from the General Fund to the Debt Service Fund to retire a portion of a serial bond due in 20X1.

d.

A police car was purchased for $18,000 and the trade-in of an old police car originally purchased for $15,000 from the General Fund. The

new vehicle had a list price and fair market value of $21,500.

e.

The serial bonds funded in transaction c. were retired on their maturity date.

f.

By year end, $450,000 of the work had been completed on the new library.

Required:

Prepare the necessary journal entries to record the transactions in the General Fixed Asset Account Group (GFAAG) and the General Long-term

Debt Account Group (GLTDAG), and identify in which it should be recorded.

Fund or

Entry

DEBIT

CREDIT

Group

a.

Amount to Be Provided for Payment

of Term Bonds

2,500,000

GLTDAG

Term Bonds Payable

2,500,000

b.

Amount Available in Debt Service

Funds-Term Bonds

200,000

GLTDAG

Amount to Be Provided for

Payment of Term Bonds

200,000

c.

Amount Available in Debt Service

Funds—Serial Bond

150,000

GLTDAG

Amount to be Provided for

Payment of Serial Bonds

150,000

d.

Equipment

21,500

GFAAG

Investment in General Fixed

Assets—General Fund

21,500

Investment in General Fixed

Assets—General Fund

15,000

GFAAG

Equipment

15,000

e.

Serial Bonds Payable

150,000

GLTDAG

Amount Available in Debt Service

Funds—Serial Bonds

150,000

Construction in Progress

450,000

GFAAG

Investment in General Fixed Assets

—Capital Projects Fund

450,000

75. The following transactions were made by Cape City:

August 1, 20X9

A wealthy business person donates a downtown office building to Cape City. Its fair market value is

$2,500,000. The city intends to sell the building.

August 15, 20X9

The city purchases a warehouse to be used for storage and pays $1,500,000 from the General Fund.

September 1, 20X9

The donated office building is sold for $2,600,000.

Required:

Make the journal entries necessary to record the transactions in the General Fund and in the General Fixed Assets Account Group (GFAAG).

August 1, 20X9

General Fund

No entry required

GFAAG

Office Building

2,500,000

Investment in General Fixed

Assets—Donations

2,500,000

August 15, 20X9

General Fund

Expenditures

1,500,000

Cash

1,500,000

GFAAG

Warehouse

1,500,000

Investment in General Fixed

Assets—General Fund Revenues

1,500,000

September 1, 20X9

General Fund

Cash

2,600,000

Other Financing Source—

Disposal of Asset

2,600,000

GFAAG

Investment in General Fixed

Assets—Donations

2,500,000

Office Building

2,500,000

76. Following is a list of selected transactions for the City of Andrew:

a.

The city issued $750,000 in term bonds. The bonds sold at 102.

b.

After the payment of interest, the city transferred $100,000 from the General Fund to retire serial bonds.

c.

The bonds in b are retired.

Required:

Make the necessary journal entries in the funds and account groups affected except the Debt Service Fund.

77. What is the concept of interperiod equity?

General Fund

Cash (750,000 x 1.02)

765,000

Other Financing

Source—Bond Proceeds

765,000

General

Amount to Be Provided

Long-term Debt

for Payment of Term

Account Group

Bonds

750,000

Term Bonds

750,000

b.

General Fund

Other Financing Use

100,000

Cash

100,000

GLTDAG

Amount Available in Debt

Service Fund—Serial

Bonds

100,000

Amount to Be Provided

for Payment of

Serial Bonds

100,000

c.

GLTDAG *

Serial Bonds Payable

100,000

Amount Available in

Debt Service Funds—

Serial Bonds

100,000

78. Describe the three basic fund types and account groups and explain what changes, if any, the adoption of

GASB standard #34 has made on these classifications?

The three basic funds are:

79. 1) Discuss how revenue is recognized under the modified accrual method.

2) Discuss how this impacts each of the revenues listed below:

a) Imposed taxes such as property taxes

b) Grants from governmental units

c) Donations

d) Service charges such as trash removal fees

e) Investment revenue

f) Fees from licenses and permits

g) Derived taxes such as sales taxes

80. Explain why governmental funds use budgetary accounts.

time period in which they may be used, Deferred Revenue is credited.

group.

e) Investment revenue should be recognized when earned. Gains and losses should be recognized when an investment is sold.

soon enough thereafter to finance expenditures for the period.

81. Define an encumbrance and explain why a state or local government would use encumbrances.

82. What is infrastructure and where would it be accounted for?