Chapter 8—Subsidiary Equity Transactions, Indirect Subsidiary

Ownership, and Subsidiary Ownership of Parent Shares Key

1. A parent company owns a 100% interest in a subsidiary. Recently, the subsidiary paid a 10% stock dividend.

The dividend should be recorded on the books of the parent

2. Company P purchased a 80% interest in the Company S on January 1, 20X1, for $600,000. Any excess of

cost is attributed to the Company’s building with a 20-year life. The equity balances of Company S are as

follows:

January 1, 20X1

December 31, 20X4

Common stock, $10 par

$100,000

$140,000

Other paid-in capital

200,000

280,000

Retained earnings

250,000

450,000

The only change in paid-in capital is a result of a 40% stock dividend paid in 20X3. The cost to simple equity conversion to bring the investment

account to its December 31, 20X4, balance is ____.

3. When the parent purchases some newly issued shares of a subsidiary, any adjustments resulting from the

subsidiary stock sales should be made

4. On January 1, 20X1, Paris Ltd. paid $600,000 for its 75% interest in the Scott Company when Scott had total

equity of $550,000. Any excess of cost over book value was attributed to equipment with a 10-year life. On

January 1, 20X3, Scott Company had the following stockholders’ equity:

Common stock, $10 par

$100,000

Other paid-in capital

200,000

Retained earnings

350,000

On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $90 each in a private offering to noncontrolling shareholders. As a

result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

5. On January 1, 20X1, Paris Ltd. paid $600,000 for its 75% interest in the Scott Company when Scott had total

equity of $550,000. Any excess of cost over book value was attributed to equipment with a 10-year life. On

January 1, 20X3, Scott Company had the following stockholders’ equity:

Common stock, $10 par

$100,000

Other paid-in capital

200,000

Retained earnings

350,000

On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $60 each in a private offering to noncontrolling shareholders. As a

result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

6. When a parent purchases a portion of the newly issued stock of its subsidiary and the parent’s percentage of

ownership interest remains the same,

7. Company P owns 80% of the 10,000 outstanding common stock of Company S. If Company S issues 2,500

added shares of common stock, and Company P purchases some of the newly issued shares, which of the

following statements is true?

8. When a parent purchases a portion of the newly issued stock of its subsidiary and the ownership interest

increases,

9. On January 1, 20X1, Paul, Inc. acquired a 90% interest in Stephan Company. The $45,000 excess of purchase

price (parent’s share only) was attributable to goodwill. On January 1, 20X3, Stephan Company had the

following stockholders’ equity:

Common stock, $10 par

$100,000

Other paid-in capital

200,000

Retained earnings

300,000

On January 2, 20X3, Stephan sold 2,000 additional shares in a private offering. Stephan issued the new shares for $80 per share; Paul, Inc. purchased

all the shares. What is the journal entry that Paul will prepare to record this investment?

10. When a parent purchases a portion of the newly issued stock of its subsidiary in a private offering and the

ownership interest decreases,

11. On January 1, 20X1, Paul, Inc. acquired a 90% interest in Stephan Company. The $45,000 excess of

purchase price (parent’s share only) was attributable to goodwill. On January 1, 20X3, Stephan Company had

the following stockholders’ equity:

Common stock, $10 par

$100,000

Other paid-in capital

200,000

Retained earnings

300,000

On January 2, 20X3, Stephan sold 2,000 additional shares in a private offering. Stephan issued the new shares for $70 per share; Paul, Inc.

purchased 600 of the shares. As a result of this sale, there is a(n)

12. Pepper Company owns 60,000 of Salt Company’s 100,000 outstanding shares. This year, Salt purchased

20,000 of its outstanding shares from the NCI for $70,000. Pepper’s interest after the treasury stock purchase

is:

13. Pepper Company owned 60,000 of Salt Company’s 100,000 outstanding shares. On January 2, 20X3, Salt

purchased 20,000 of its outstanding shares from the NCI for $70,000. Pepper purchased its shares on January

1, 20X1, at which time the fair value of Salt exceeded its book value by $50,000. This difference was due to

machinery that was undervalued and had a remaining life of 5 years. On December 31, 20X2, Salt Company

had the following stockholders’ equity:

Common stock, $1 par

$100,000

Paid-in capital in excess of par

50,000

Retained earnings

270,000

Assuming Pepper uses the equity method to account for its investment in Salt, the adjustment to the Pepper’s books would include:

14. Pepper Company owned 60,000 of Salt Company’s 100,000 outstanding shares. On January 2, 20X3, Salt

purchased 20,000 of its outstanding shares from the NCI for $70,000. Pepper purchased its shares on January

1, 20X1, at which time the fair value of Salt exceeded its book value by $50,000. This difference was due to

machinery that was undervalued and had a remaining life of 5 years. On December 31, 20X2, Salt Company

had the following stockholders’ equity:

Common stock, $1 par

$100,000

Paid-in capital in excess of par

50,000

Retained earnings

270,000

The amount of the adjustment to Pepper’s equity would be a:

15. Consolidated statements for X, Y, and Z are proper if

16. Apple Inc. owns a 90% interest in Banana Company. Banana Company, in turn, owns a 80% interest in

Carrot Company. During 20X4, Carrot Company sold $50,000 of merchandise to Apple Inc. at a gross profit of

20%. Of this merchandise, $10,000 was still unsold by Apple Inc. at year end. The adjustment to the controlling

interest in consolidated net income for 20X4 is ____.

17. Apple Inc. purchased a 70% interest in the Banana Company for $490,000 on January 1, 20X3, when

Banana Company had the following stockholders’ equity:

Common stock, $10 par

$100,000

Paid-in capital in excess of par

250,000

Retained earnings

150,000

At the time of Apple’s purchase, Banana Company was an 80% owner of the Carrot Company. Also on that date, Carrot Company has a machine that

has a market value in excess of book value of $20,000. There is no difference between book and market value for any Banana Company assets. The

goodwill that would result from this purchase is ____.

18. Able Company owns an 80% interest in Barns Company and a 20% interest in Carns Company. Barns owns

a 40% interest in Carns Company.

19. Able Company owns an 80% interest in Barns Company and a 20% interest in Carns Company. Barns owns

a 40% interest in Carns Company. The reported income of Carns is $20,000 for 20X4. Which of the following

shows how it will be distributed?

Barns Carns

Controlling Non- Non-

Interest Controlling Controlling

20. Which of the following situations is viewed as the parent having treasury stock?

21. When a subsidiary owns shares of the parent, the subsidiary’s investment account

22. When a subsidiary purchases shares of the parent, on a consolidated basis:

23. Plum Inc. acquired 90% of the capital stock of Sterling Co. on 1/1/X1 at a cost of $540,000. On this date

Sterling had equipment (10-year life) carried at $200,000 under market and total equity amounting to $350,000.

On 1/1/X1 Sterling acquired 5% (10,000 shares) of Plum’s outstanding common stock for $3 per share.

Internally generated net income was $50,000 for Plum and $40,000 for Sterling.

Consolidated net income for 20X2 is

24. Plum Inc. acquired 90% of the capital stock of Sterling Co. on 1/1/X1 at a cost of $540,000. On this date

Sterling had equipment (10-year life) carried at $200,000 under market and total equity amounting to $350,000.

On 1/1/X1 Sterling acquired 5% (10,000 shares) of Plum’s outstanding common stock for $3 per share.

Internally generated net income was $50,000 for Plum and $40,000 for Sterling. The noncontrolling interest in

consolidated net income is

25. Company P had 300,000 shares of common stock outstanding. It owned 80% of the outstanding common

stock of S. S owned 20,000 shares of P common stock. In the consolidated balance sheet, Company P’s

outstanding common stock may be shown as

26. A owns 80% of B and 20% of C. B owns 32% of C, and C owns 10% of A. Which interest will be

considered NCI in the consolidated balance sheet?

27. Manke Company owns a 90% interest in Neske Company. Neske, in turn, owns a 10% interest in Manke.

Neske has 10,000 common stock shares outstanding, and Manke has 20,000 common stock shares outstanding.

How many shares would each firm show as outstanding in the consolidated balance sheet, under the treasury

stock method?

28. On January 1, 20X1, Prism Company purchased 7,500 shares of the common stock of Sight Company for

$495,000. On this date, Sight had 20,000 shares of $10 par common stock authorized, 10,000 shares issued and

outstanding. Other paid-in capital and retained earnings were $200,000 and $300,000 respectively. On January

1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years.

Sight’s net income and dividends for two years were:

20X1

20X2

Net income

$50,000

$80,000

Dividends

10,000

20,000

In November 20X1, Sight Company declared a 10% stock dividend at a time when the market price of its common stock was $50 per share. The

stock dividend was distributed on December 31, 20X1.

For both 20X1 and 20X2, Prism Company has accounted for its investment in Sight Company using the simple equity method.

During 20X1, Sight Company sold goods to Prism Company for $40,000, of which $10,000 was on hand on December 31, 20X1. During 20X2,

Sight sold goods to Prism for $60,000 of which $15,000 was on hand on December 31, 20X2. Sight’s gross profit on intercompany sales is 40%.

Required:

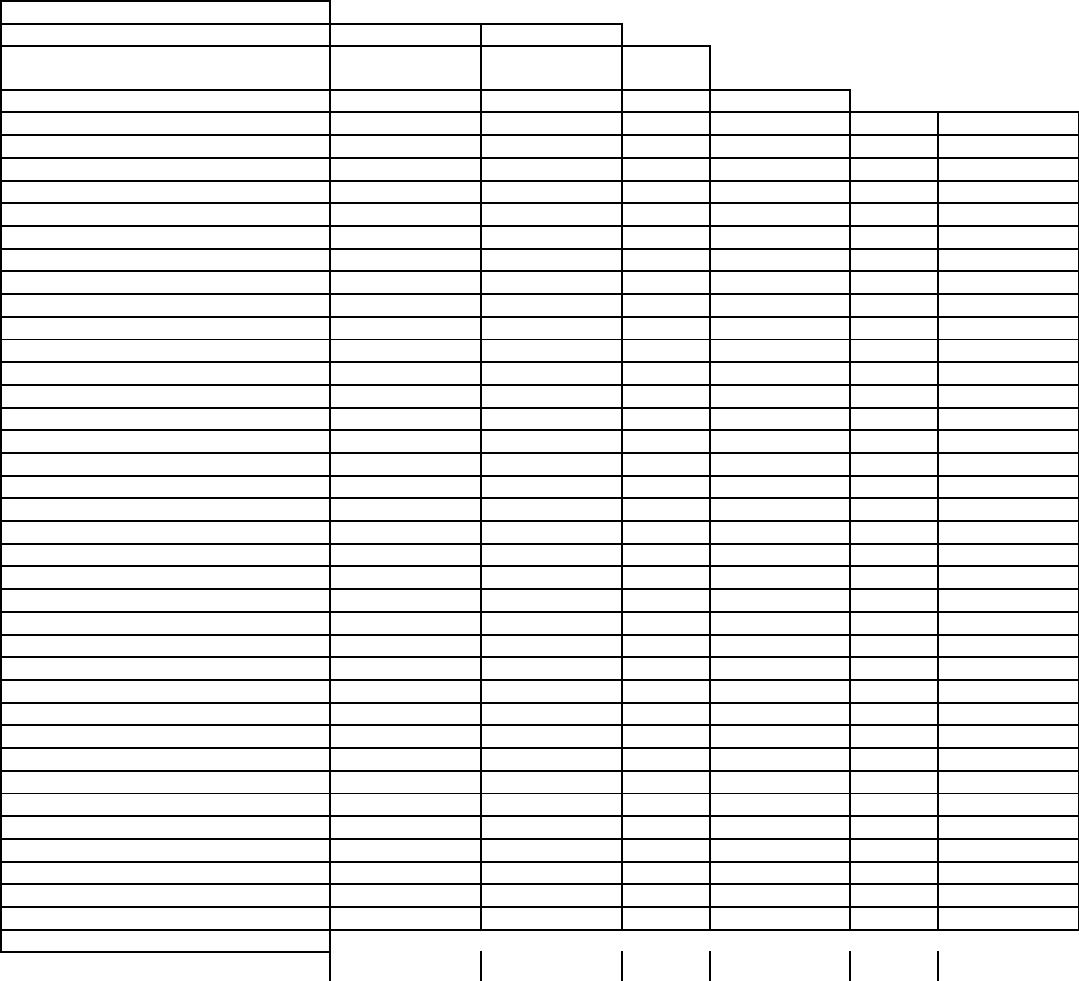

Complete the Figure 8-1 worksheet for consolidated financial statements for 20X2.

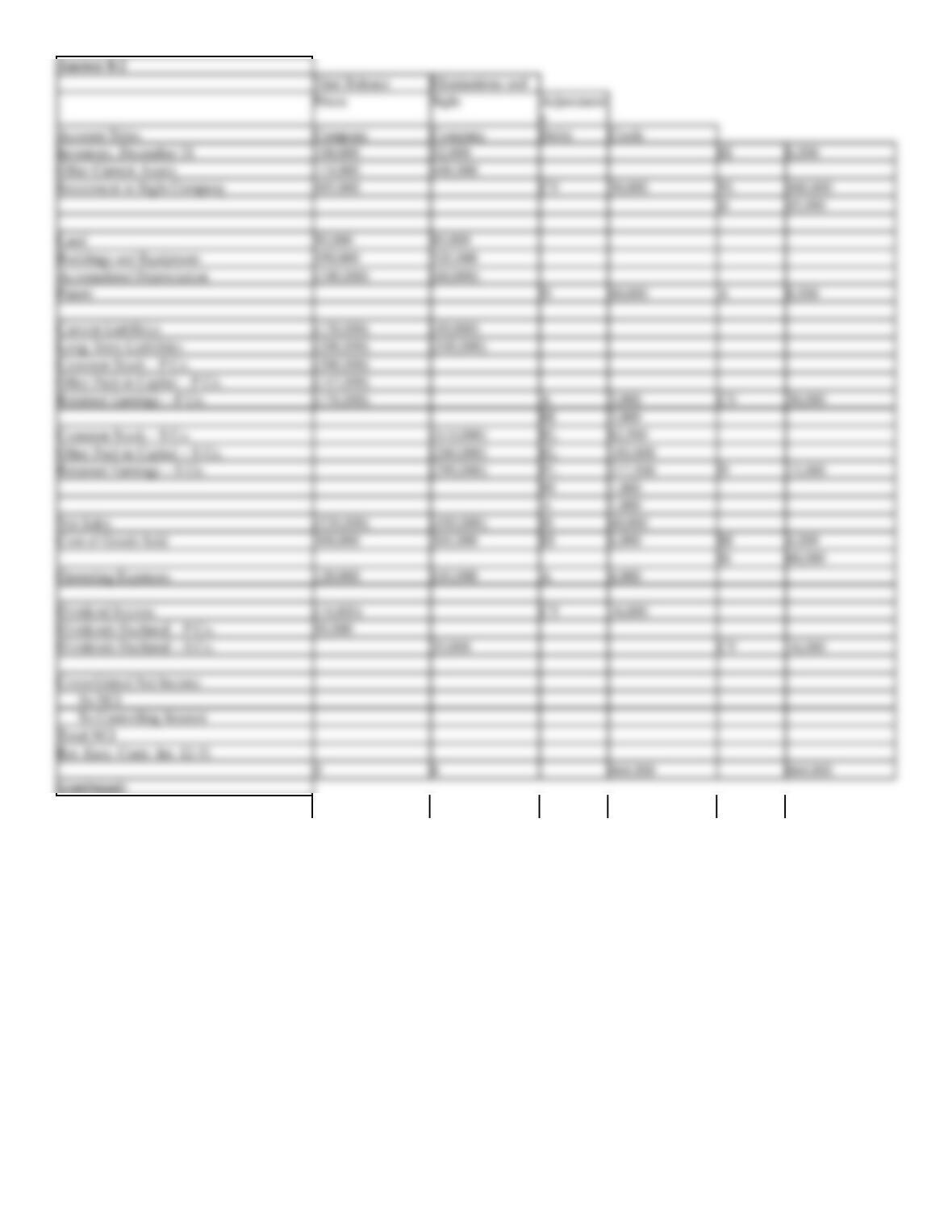

Figure 8-1

Trial Balance

Eliminations and

Prism

Sight

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

52,000

Other Current Assets

167,000

448,000

Investment in Sight Company

570,000

Land

50,000

80,000

Buildings and Equipment

350,000

320,000

Accumulated Depreciation

(100,000)

(60,000)

Patent

Current Liabilities

(120,000)

(40,000)

Long-Term Liabilities

(200,000)

(100,000)

Common Stock – P Co.

(300,000)

Other Paid-in Capital – P Co.

(142,000)

Retained Earnings – P Co.

(265,000)

Common Stock – S Co.

(110,000)

Other Paid-in Capital – S Co.

(240,000)

Retained Earnings – S Co.

(290,000)

Net Sales

(520,000)

(450,000)

Cost of Goods Sold

300,000

260,000

Operating Expenses

120,000

110,000

Subsidiary Income

(60,000)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

20,000

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

0

0

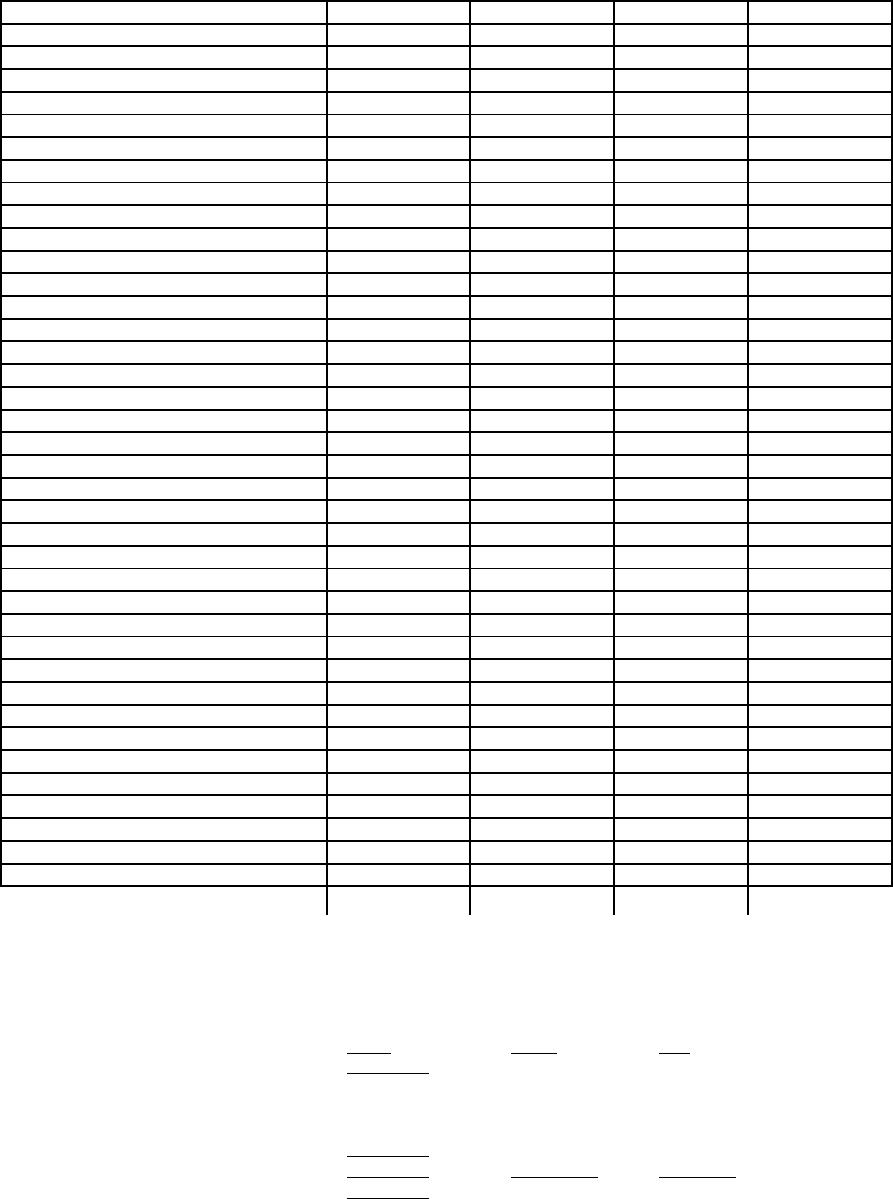

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sight Company

Land

Buildings and Equipment

Accumulated Depreciation

Patent

Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Subsidiary Income

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

Determination and Distribution of Excess Schedule:

Entity

Parent

NCI

Entity FV

660,000

495,000

165,000

Book value:

Common Stock ($10)

100,000

Paid-in Cap in Excess of Par

200,000

RE 1/1/X1

300,000

Book value:

600,000

450,000

150,000

Excess-attributable to patent

60,000

For the worksheet solution, please refer to Answer 8-1.

29. On January 1, 20X1, Prism Company purchased 7,500 shares of the common stock of Sight Company for

$495,000. On this date, Sight had 20,000 shares of $10 par common stock authorized, 10,000 shares issued and

outstanding. Other paid-in capital and retained earnings were $200,000 and $300,000 respectively. On January

1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years.

Sight’s net income and dividends for two years were:

20X1

20X2

Net income

$50,000

$80,000

Dividends

10,000

20,000

In November 20X1, Sight Company declared a 10% stock dividend at a time when the market price of its common stock was $50 per share. The

stock dividend was distributed on December 31, 20X1.

For both 20X1 and 20X2, Prism Company has accounted for its investment in Sight using the cost method.

During 20X1, Sight Company sold goods to Prism Company for $40,000, of which $10,000 was on hand on December 31, 20X1. During 20X2,

Sight sold goods to Prism for $60,000 of which $15,000 was on hand on December 31, 20X2. Sight’s gross profit on intercompany sales is 40%.

Required:

Complete the Figure 8-2 worksheet for consolidated financial statements for 20X2.

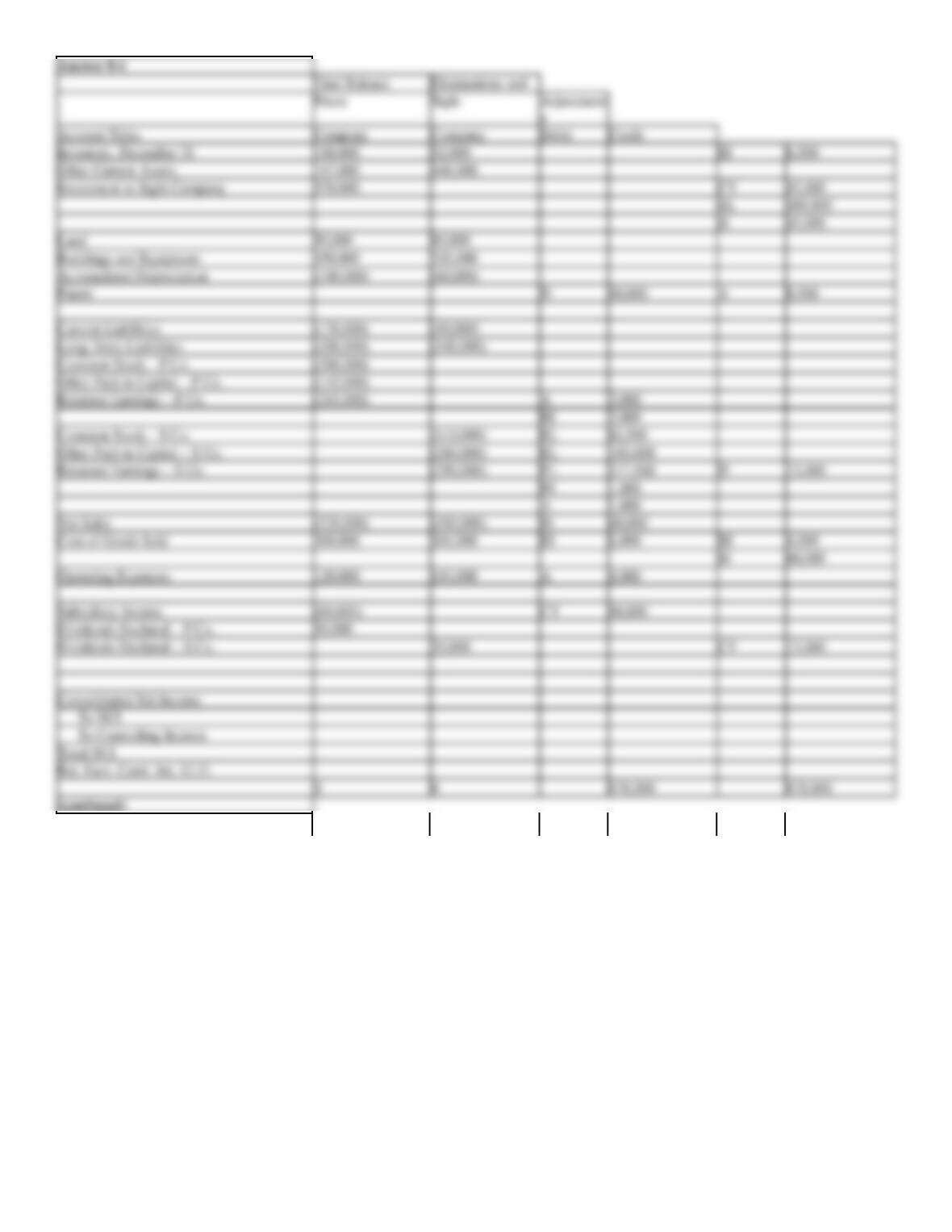

Figure 8-2

Trial Balance

Eliminations and

Prism

Sight

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

100,000

52,000

Other Current Assets

114,000

448,000

Investment in Sight Company

495,000

Land

50,000

80,000

Buildings and Equipment

350,000

320,000

Accumulated Depreciation

(100,000)

(60,000)

Patent

Current Liabilities

(120,000)

(40,000)

Long-Term Liabilities

(200,000)

(100,000)

Common Stock – P Co.

(300,000)

Other Paid-in Capital – P Co.

(147,000)

Retained Earnings – P Co.

(176,000)

Common Stock – S Co.

(110,000)

Other Paid-in Capital – S Co.

(240,000)

Retained Earnings – S Co.

(290,000)

Net Sales

(520,000)

(450,000)

Cost of Goods Sold

300,000

260,000

Operating Expenses

120,000

110,000

Dividend Income

(16,000)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

20,000

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sight Company

Land

Buildings and Equipment

Accumulated Depreciation

Patent

Current Liabilities

Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Dividend Income

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

0

0

Determination and Distribution of Excess Schedule:

Entity

Parent

NCI

Entity FV

660,000

495,000

165,000

Book value:

Common Stock ($10)

100,000

Paid-in Cap in Excess of Par

200,000

RE 1/1/X1

300,000

Book value:

600,000

450,000

150,000

Excess-attributable to patent

60,000

For the worksheet solution, please refer to Answer 8-2.