50. Richardson and George have been partners in the medical supply business since July 18, 20X3. Since the

formation of the partnership, profits and losses have been shared in the ratio of 55:45, respectively. Capital

balances on December 31, 20X7, were $159,000 for Richardson and $106,000 for George. They have agreed to

admit Keller as a partner on January 1, 20X8. Keller will receive a 30% interest in partnership capital, and

future profits and losses will be allocated equally among the partners.

Required:

Prepare journal entries in the partnership books to record Keller’s admission in each of the following situations:

a.

Keller deals directly with Richardson and agrees to exchange land with a book value of $60,000 and a fair market value of $87,000 for

50% of Richardson’s interest in capital. Record Keller’s contribution under the two alternative methods. What assumption is made under

each alternative?

b.

Keller contributes $130,000 cash and a 1-year note with a value of $20,000 to the partnership entity. Record journal entries under the

bonus and goodwill methods.

c.

Using the bonus method, assume that (1) Keller contributes $84,000 and an established clientele, or (2) Keller‘s contribution of $84,000 is

sufficient because existing partnership assets are overvalued.

d.

Keller invests $84,000 in the partnership entity. Use the goodwill method and assume that net assets should not be written down.

51. Rogers, Davis, and Smukalla have capital balances of $50,000, $26,100, and $10,900, respectively. The

partners share profits/losses equally.

Required:

Calculate Rogers’ new capital balance resulting from each of the following independent situations:

Situation 1:

Smukalla sells his interest in the partnership to Rogers for $25,000.

Situation 2:

Meyers purchases a one-fourth interest from the partnership for $35,000. The bonus method is used to account for the

incoming partner.

Situation 3:

The same as Situation 2 except that the goodwill method is used to account for the incoming partner.

Situation 4:

Davis sells her interest to the partnership for $30,000. The total amount of suggested goodwill is to be recorded.

Rogers’ new capital balance is $60,900 ($50,000 $10,900). Because the transaction involves individual partners and

Meyers’ interest of $4,500 ($35,000 – $30,500) is allocated equally among the original partners. (Rogers receives 4,500 x

1/3 or 1,500)

interest in the goodwill as the partners share profits equally.

52. Luc, Denis, and Rollande have capital balances of $30,000, $70,000, and $15,000, respectively. The

partners share profits/losses 2:6:2. All assets’ book values equal market except as noted. The partnership

agreement states the bonus method is to be used to account for partner sale of interest to the partnership.

Required:

Calculate Luc’s new capital balance resulting from each of the following independent situations:

Situation 1:

Rollande sells his interest to the partnership for $25,000. Bonus method is used.

Situation 2:

Rollande sells his interest to Luc for $25,000.

Situation 3:

Martel purchases a 20% interest from the partnership for $35,000. The bonus method is used to account for the incoming

partner.

Situation 4:

The same as Situation 3 except that the goodwill method is used to account for the incoming partner.

remaining partners based on their remaining profit and loss ratios. (2/8 to Luc, 6/8 to Denis so Luc receives 10,000 x 2/8

Situation 2:

Luc’s new capital balance is $45,000 ($30,000 + $15,000). Because the transaction involves individual partners and not

the partnership, Rollande’s balance is merely transferred to Luc’s.

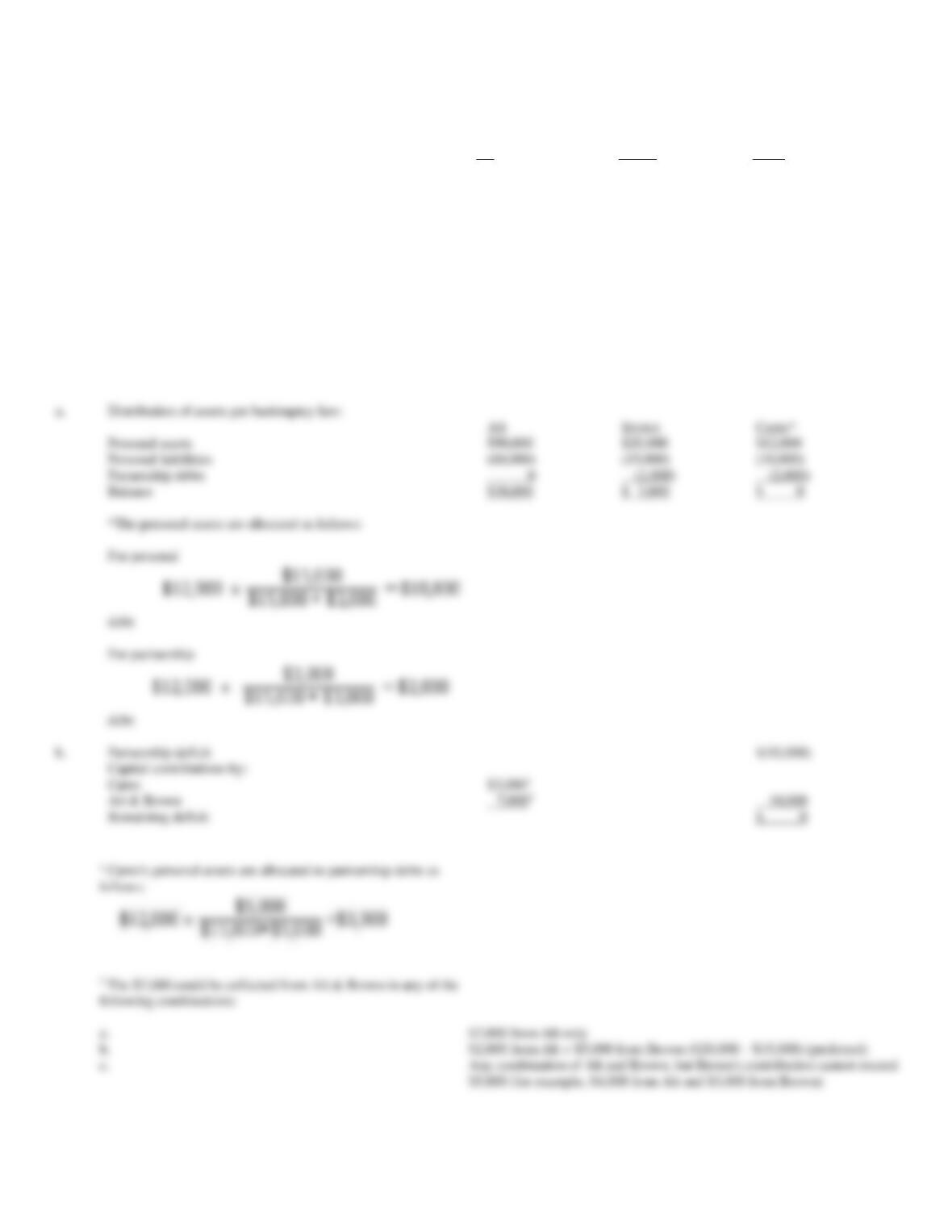

53. Long-term partners, Pop, Ping, and Pam have capital balances of $60,000, $45,000 and $30,000,

respectively. They share in profits and losses 50%-to-30%-to-20%, respectively. All assets are valued fairly.

Pam decides to retire from the partnership. Calculate the remaining partners’ capital balances after the Pam

withdrawal under the following situations:

a.

Pam sells the interest to Ping for $25,000.

b.

Pam sells the interest to the partnership for $25,000; bonus method is used

c.

Pam sells the interest to the partnership for $40,000; goodwill attributable only to the exiting partner is recorded

a.

Capital Balances:

Total

Pop

Ping

Pam

Before retirement:

$135,000

$60,000

$45,000

$ 30,000

Pam Withdraws:

30,000

(30,000)

After Retirement:

$135,000

$60,000

$75,000

$ 0

b.

Capital Balances:

Total

Pop

Ping

Pam

Before retirement:

$135,000

$60,000

$45,000

$30,000

Pam Withdraws:

(25,000)

3,125

1,875

(30,000)

After Retirement:

$110,000

$63,125

$46,875

$ 0

Price paid to Pam = $25,000

Pam Capital = $30,000

respectively.

c.

Capital Balances:

Total

Pop

Ping

Pam

Before retirement:

$135,000

$60,000

$45,000

$30,000

Pam’s share GW:

10,000

10,000

Pam Withdraws:

(40,000)

(40,000)

After Retirement:

$105,000

$60,000

$45,000

$ 0

Price paid to Pam = $40,000

Pam Capital = $30,000

Pam’s share of Goodwill = $10,000

54. Oak, Pine, and Maple are partners with present capital balances of $42,000, $39,000, and $90,000,

respectively. The partners share profits and losses according to the following percentages: 20% for Oak, 20%

for Pine, and 60% for Maple. The existing assets of the original partnership have market values equal to book

values except for the following:

Accounts Receivable:

overvalued by $10,000

Land:

undervalued by $30,000

Pine has agreed to sell her interest to the partnership for $45,000.

Required:

Calculate the capital balances for each individual in the new partnership, assuming use of the bonus and goodwill methods. The goodwill method

should recognize the goodwill traceable to all partners.

Bonus method:

Total

Oak

Pine

Maple

Original capital balance

$171,000

$42,000

$39,000

$90,000

Asset revaluation

(10,000)

(2,000)

(2,000)

(6,000)

Distribution

to withdrawing partner:

Bonus*

( 8,000)

(2,000)

(6,000)

Capital balance*

(37,000)

(37,000)

Total

$116,000

$38,000

$ 0

$78,000

* Price Paid to Pine = $45,000

Pine’s Adjusted Capital = $37,000

(after asset revaluation)

Bonus = $(8,000)

Goodwill method:

Total

Oak

Pine

Maple

Original capital balance

$171,000

$42,000

$39,000

$ 90,000

Asset revaluation

(10,000)

(2,000)

(2,000)

(6,000)

Asset revaluation

30,000

6,000

6,000

18,000

Distribution

to withdrawing partner:

Goodwill*

10,000

2,000

2,000

6,000

Capital balance*

(45,000)

(45,000)

Total

$156,000

$48,000

$ 0

$108,000

* Price Paid to Pine = $45,000

Pine’s Adjusted Capital = $43,000

(after asset revaluation)

55. The partnership of Alt, Brown, and Carns has total assets and liabilities of $30,000 and $25,000,

respectively. Information relating to the partners is as follows:

Alt

Brown

Carns

Total personal assets

$90,000

$20,000

$12,000

Total personal liabilities

60,000

15,000

15,000

Partnership capital balance

(deficit)

10,000

(2,000)

(3,000)

Required:

a.

Assuming that federal bankruptcy laws are applicable, indicate how the partners’ personal assets would be distributed.

b.

Assume that the partnership had a deficit of $10,000, allocated among Alt, Brown, and Carns as follows: $2,000 surplus, $7,000 deficit,

and $5,000 deficit, respectively. Indicate how the deficit would be satisfied when bankruptcy laws are applicable.

a.

Distribution of assets per bankruptcy law:

Alt

Brown

Carns*

Personal assets

$90,000

$20,000

$12,000

Personal liabilities

(60,000)

(15,000)

(10,000)

Partnership debts

0

(2,000)

(2,000)

Balance

$30,000

$ 3,000

$ 0

*The personal assets are allocated as follows:

debt:

b.

Partnership deficit

$(10,000)

Capital contributions by:

Carns

Alt & Brown

10,000

Remaining deficit

$ 0

a.

$7,000 from Alt only

b.

$2,000 from Alt + $5,000 from Brown ($20,000 – $15,000) (preferred)

$5,000 (for example, $4,000 from Alt and $3,000 from Brown)

56. Merz, Dechter, and Flowers are partners in a partnership and share profits and losses 40%, 40%, and 20%,

respectively. The partners have agreed to liquidate the partnership and anticipate that liquidation expenses will

total $14,000. Prior to the liquidation, the partnership balance sheet reflects the following book values:

Cash

$ 25,000

Noncash assets

200,000

Note payable to Dechter

12,000

Other liabilities

165,000

Capital, Merz

40,000

Capital Dechter

18,000

Capital deficit, Flowers

(10,000)

Required:

Assuming that the actual liquidation expenses are $20,000 and that noncash assets are sold for $160,000, determine how the assets will be distributed.

Flowers has net personal assets of $10,000.

Noncash

Capital and

Loan Balances

Cash

Assets

Liabilities

Merz

Dechter

Flowers

Beginning balances

$ 25,000

$200,000

$165,000

$ 40,000

$30,000*

$(10,000)

Liquidation expense

(20,000)

(8,000)

(8,000)

(4,000)

Sale of non-cash assets

160,000

(200,000)

(16,000)

(16,000)

(8,000)

Payment of liabilities

(165,000)

(165,000)

Contribution by Flowers

10,000

10,000

Allocation of Flower’s deficit

(6,000)

(6,000)

12,000

Distribution to partners

(10,000)

(10,000)

0

0

Ending balances

0

0

0

0

0

0

* 18,000 capital + 12,000 loan

57. The partnership of Able, Bower, and Cramer was liquidated. The partners have shared profits and losses in

the ratio of 2:4:4. Prior to liquidation, their capital balances were the following*:

Able

Bower

Cramer

$10,000

$(5,000)

$(15,000)

* Deficit shown in parentheses

Cash totaled $20,000, with liabilities amounting to $30,000. A review of the individual partners’ personal financial status reveals the following:

Assets

Liabilities

Able

$ 5,000

$20,000

Bower

6,000

4,000

Cramer

30,000

20,000

Required:

Prepare a worksheet to liquidate the partnership.

Cash

Liabilities

Able

Bower

Cramer

Beginning:

$20,000

$(30,000)

$(10,000)

$5,000

$15,000

Payment of liabilities:

(20,000)

20,000

$ 0

$(10,000)

$(10,000)

$5,000

$15,000

Cramer/Bower pay in

From personal worth

to cover

deficit balances:

12,000

(2,000)

(10,000)

$12,000

$(10,000)

$(10,000)

$3,000

$ 5,000

Payment of liabilities:

(10,000)

10,000

$ 2,000

$ 0

$(10,000)

$3,000

$ 5,000

Allocation of

Deficit balances:

8,000

(3,000)

(5,000)

$ 2,000

$ 0

$ (2,000)

$ 0

$ 0

Able paid:

(2,000)

2,000

$ 0

$ 0

$ 0

$ 0

$ 0

58. The ALPHA, BETA, AND DELTA partnership has total assets of $260,000. Capital balances for partners

ALPHA, BETA, and DELTA are $50,000, $30,000, and $50,000, respectively. The profit/loss percentages for

partners ALPHA, BETA, and DELTA are 30%, 40%, and 30%, respectively. Included in the liabilities is a

$9,000 loan payable to ALPHA. The partnership has elected to liquidate over the next several months.

Liquidation expenses are estimated to be $15,000.

Required:

Assuming assets with a book value of $80,000 were sold for $60,000, and that $160,000 cash is available after

the sale, how should the available cash be distributed?

59. On July 1, 20X9, the Crawford Company has the following balance sheet:

Assets

Liabilities and Capital

Cash

$ 17,000

Accounts payable

$ 32,000

Other assets

183,000

Due to Palmer

12,000

Other liabilities

70,000

Palmer, capital

24,000

Lake, capital

62,000

Total assets

$200,000

Total liabilities and

capital

$200,000

As of July 1, 20X9, the partners have personal net worth as follows:

Palmer

Lake

Assets

$52,000

$ 76,000

Liabilities

47,000

102,000

The personal net worth of each partner does not include any amounts due to or from the partnership.

Required:

Assume the other assets are sold for $103,000 after incurring liquidation expenses of $4,000. After liquidation of the partnership, determine how

much is available to Lake’s unsatisfied personal creditors based on the following:

a.

Application of the Uniform Partnership Act

b.

Application of common law

Note that if income distribution procedures are not stated in the partnership agreement, RUPA states that

income is to be distributed equally among partners.

a.

For the worksheet solution, please refer to Answer 14-3.

Offset

Other

Capital Balances

Cash

Assets

Liabilities

Palmer

Lake

Beginning balances

$ 17,000

$183,000

$102,000

$36,000

$62,000

Liquidation expenses

(4,000)

(2,000)

(2,000)

Sale of assets

103,000

(183,000)

(40,000)

(40,000)

Balance

116,000

0

102,000

(6,000)

20,000

Contribution

5,000

5,000

Absorb debit balances

1,000

(1,000)

Ending balances

$121,000

0

$102,000

0

$19,000

a)

The $19,000 of cash in the partnership traceable to Lake.

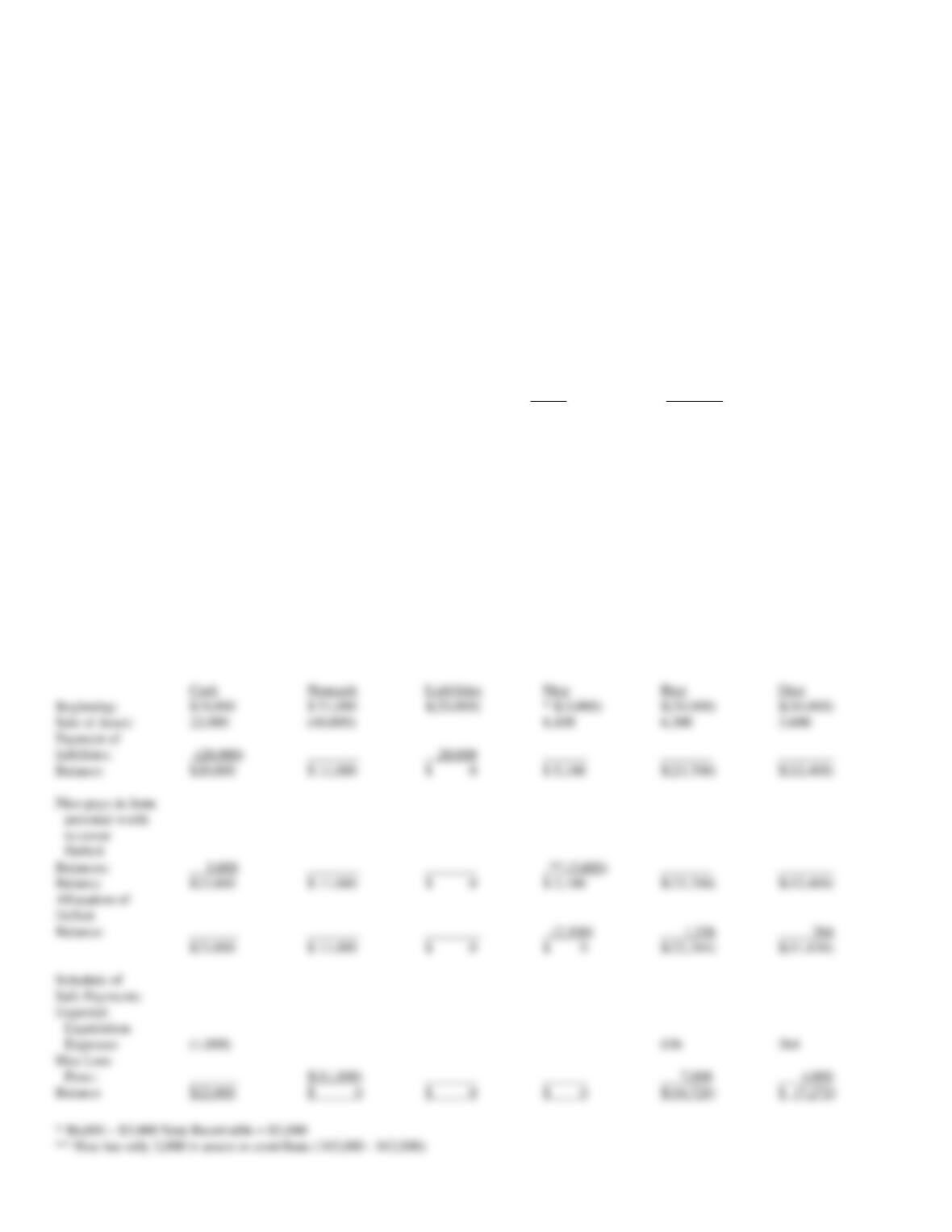

60. The Nice, Rice, and Dice Partnership has not been successful. The partners have determined they must

liquidate their partnership. The partners have agreed to liquidate the partnership and anticipate that liquidation

expenses will total $1,000. Prior to the liquidation, the partnership balance sheet reflects the following book

values:

Cash

$18,000

Noncash assets

51,000

Note receivable-Nice

3,000

Other liabilities

20,000

Capital, Nice

6,000

Capital, Rice

30,000

Capital, Dice

16,000

Profits and losses are shared 45% to Nice, 35% to Rice, and 20% to Dice. A review of the individual partner’s personal net worth reveals the

following:

Assets

Liabilities

Nice

165,000

162,000

Rice

200,000

110,000

Dice

185,000

90,000

The following transactions occur:

a.

Assets having a book value of $40,000 are sold for $22,000 cash

b.

Liabilities are paid, where possible

c.

Partners contribute from their personal net worth, according to RUPA requirements

Required:

Prepare liquidation schedule and determine how the available assets will be distributed using a schedule of safe payments.

Cash

Noncash

Liabilities

Nice

Rice

Dice

Beginning:

$18,000

$ 51,000

$(20,000)

* $(3,000)

$(30,000)

$(16,000)

Sale of Asset:

22,000

(40,000)

8,100

6,300

3,600

Payment of

liabilities:

(20,000)

20,000

Balance:

$20,000

$ 11,000

$ 0

$ 5,100

$(23,700)

$(12,400)

Nice pays in from

personal worth

to cover

Deficit

Balances:

3,000

** (3,000)

Balance

$23,000

$ 11,000

$ 0

$ 2,100

$(23,700)

$(12,400)

Allocation of

Deficit

Balance:

(2,100)

1,336

764

$23,000

$ 11,000

$ 0

$ 0

$(22,364)

$(11,636)

Schedule of

Safe Payments:

Expected

Liquidation

Expenses

(1,000)

636

364

Max Loss

61. The Tyler, Russell, and Colby partnership is liquidating. The three partners share profits and losses equally.

The following is the post-closing trial balance for the partnership:

Dr.

Cr.

Assets

$177,000

Liabilities (including $15,000 loan from Russell)

$85,000

Tyler, Capital

30,000

Russell, Capital

12,000

Colby, Capital

50,000

Required:

Draft a predistribution plan for the partnership liquidation and provide a schedule of payments.

Balances

Absorbable

Tyler

Russell

Colby

Tyler

Russell

Colby

Profit and loss

percentage

1/3

1/3

1/3

Capital and

Maximum loss

absorbable

$90,000

$81,000

$150,000

Amount to reduce

to next highest

ranked MLA

(60,000)

$90,000

$81,000

$ 90,000

Reduction in

capital

(20,000)

New capital

balance

$30,000

$27,000

$30,000

Amount to reduce

to next highest

ranked MLA

(9,000)

(9,000)

$81,000

$81,000

$ 81,000

Reduction in

capital

(3,000)

(3,000)

New capital

balance

$27,000

$27,000

$27,000

ble to

Amount

Liabilities

Tyler

Russell

Colby

First $70,000

$70,000

Next $20,000

100%

Next $6,000

50%

50%

Additional payments

1/3

1/3

1/3

62. The Revised Uniform Partnership Agreement establishes rules governing the priority in which partnership

assets are distributed to creditors and partners. Subject to any agreement to the contrary, what is the sequence

of events to accomplish the settlement of accounts and distributions to the partners?

Subject to any agreement to the contrary, the following sequence must be followed: