46. Millstone Company’s first-quarter 20X3, pretax income is $25,000. The company anticipates an annual tax

credit of $5,500. Millstone is projecting income for the remaining three quarters of $95,000. For the second

quarter of 20X4, Millstone reports $55,000 of pretax income with a projected pre-tax income for the remainder

of the year of $65,000. Millstone does not have any permanent differences between taxable income and

financial income.

In the second quarter, Millstone decided to change their depreciation method used for financial reporting

purposes. The change in depreciation methods has the following effect on the calculation and projection of

income for Millstone:

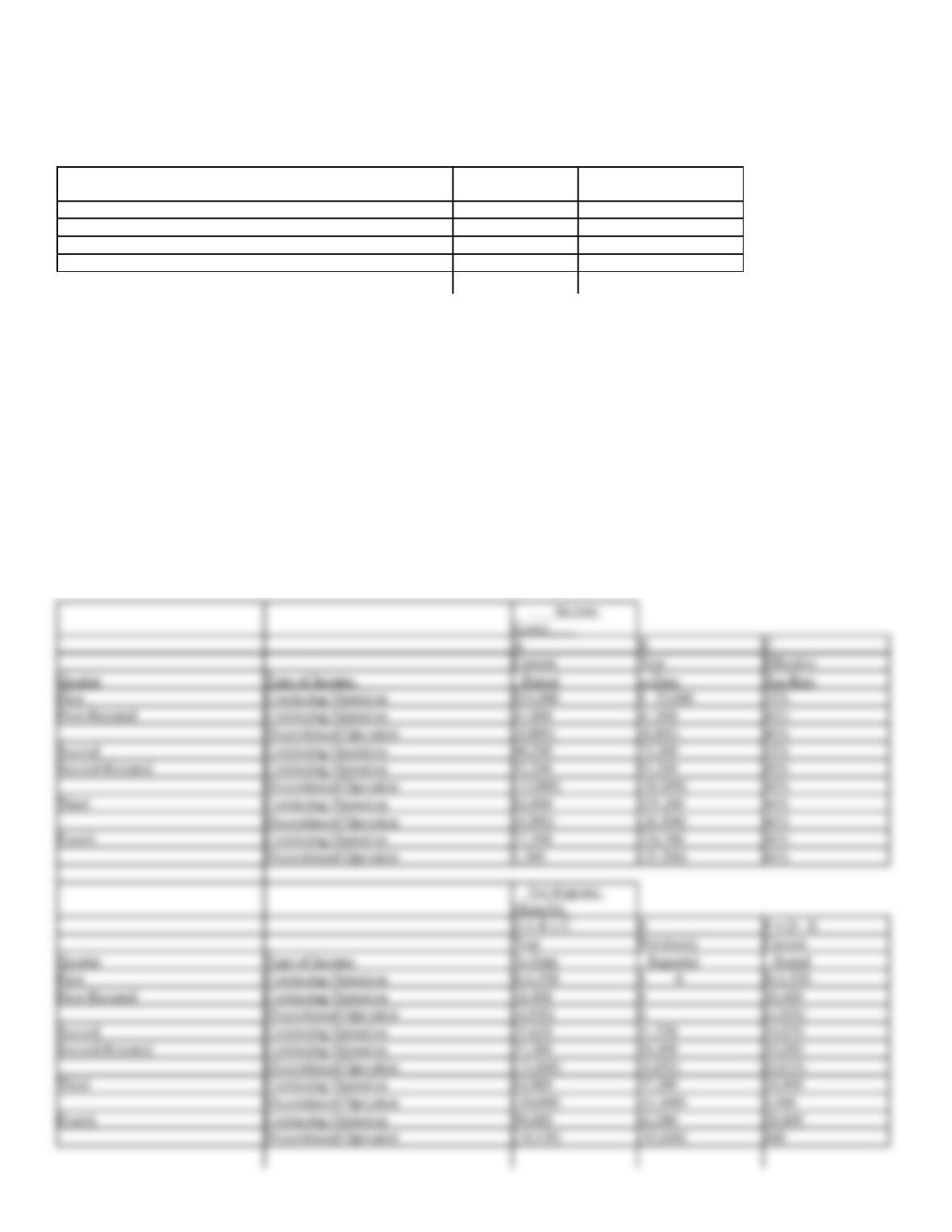

Actual Income

Projected Remainder

Qtr1

20,000

85,000

Qtr2

55,000

65,000

The effect of the change on prior years is a decrease to retained earnings of $30,000.

The current tax schedule is:

$1-$100,000

15%

$100,001-200,000

22%

$200,001-460,000

28%

$460,001 and above

30%

Required:

Calculate the first and second quarter interim tax expenses on continuing income.

(Benefit)

Period

Inc Type

Current

YTD

Effective%

YTD

Previous

Current

ordinary

25,000

25,000

11.58%

2,895

–

2,895

ordinary

55,000

80,000

13.38%

10,704

2,896

7,809

ordinary

20,000

20,000

10.10%

2,020

–

2,020

ordinary

55,000

75,000

13.07%

9,803

2,020

7,783

47. Corriveau Industries decided to switch from an accelerated depreciation method to a straight-line method in

the second quarter of 20X1. This is classified as a cumulative effect of a change in accounting principle. The

first-quarter, pretax income reported was $30,000, and projected pretax income for 20X1 was $90,000. If

Corriveau had used straight-line depreciation for the quarter, pretax income would have been $35,000 and

projected pretax income for 20X1 would have been $110,000. The cumulative effect on prior years from the

change is a $50,000 increase in retained earnings. The second-quarter income using straight-line depreciation is

$20,000, and the expected annual earnings continue to be $110,000. Assume that Corriveau is subject to a flat

25% statutory tax rate for 20X1. Corriveau is expecting $5,000 of tax-free income during the third and fourth

quarters of 20X1.

Required:

For all categories of income, calculate the interim tax expense for the first quarter, first quarter restated, and

second quarter.

48. Futura Corporation reported pretax net income of $30,000 in the first quarter of 20X1. The company

anticipated pretax net income of $90,000 for the year. During the second quarter, after issuing the first-quarter

interim statement, Futura decided to discontinue its electronics division and adopted a formal plan for its

disposal.

During the first quarter, the electronics division reported a pretax loss of $70,000 and estimated a $270,000

operating loss for the year. During the second quarter, the division experienced an operating loss of $35,000

prior to the measurement date and $8,000 in the remainder of that quarter. The anticipated loss on the disposal

of that division’s assets was $40,000.

Futura had a flat 25% tax rate for 20X1. The firm is expecting a $5,000 tax credit attributed to operations

outside of the electronic division. Second-quarter pretax income for the non-electronics operations was $40,000.

As of the end of the second quarter, annual pretax income of $225,000 was anticipated for continuing

operations.

Required:

In good form, prepare a schedule showing the income (loss) and tax expense (benefit) determination for the first

quarter, the restated first quarter, and the second quarter.

49. Consider the following:

Case A

Income (loss) for quarters 1 through 4 is ($50,000), $30,000, $40,000, and $40,000, respectively. Future projected income

for the year is uncertain at the end of quarters 1 and 2. Annual income at the end of quarter 3 is estimated to be $20,000.

No carryback benefit exists, and any future annual benefit is uncertain.

Case B

Assume the same facts as in Case A. However, at the end of quarters 1 through 3, annual income is estimated to be

$40,000.

Case C

Quarterly income (loss) levels were $15,000, ($35,000), ($75,000), and $25,000. A yearly operating loss of $70,000 was

anticipated throughout the year. Prior years’ income of $28,000 is available for carryback. The same tax rates were

relevant to the carryback period

Required:

For cases A through C, complete the schedule that follows: Assume that the statutory tax rate is 15% on the first $50,000 of income, 25% on the next

$25,000, and 30% on income in excess of $75,000.

Income (Loss)

Tax

Tax Expense

(Benefit)

Case

Quarter

Current

Year to Date

Rate

Year to Date

Current

1

2

3

4

50. East Company, a highly diversified corporation, reports the results of operations quarterly. At the beginning

of the third quarter, management decided to discontinue its recreational division. At this time, a formal plan was

authorized, calling for disposal by year end. Results for the current year, excluding taxes, are as follows:

Quarter

Continuing

Operations

Discontinued

Segment

First

$33,000

Second

40,200

Third

62,000

$(6,500)

Fourth

71,500

1,200

The following additional information was provided:

a.

The first two quarters include results of operations of the discontinued segment. The segment reported first and second quarter pretax

losses of $8,000 and $12,000, respectively.

b.

The estimated annual income tax rate in the first and second quarters was 35%. Because of the decision to discontinue, the revised annual

effective tax rate was determined to be 40%.

Required:

For each quarter, present the results of operations and the related tax expense or tax benefit. Where applicable, include the original and restated

amounts in the presentation.

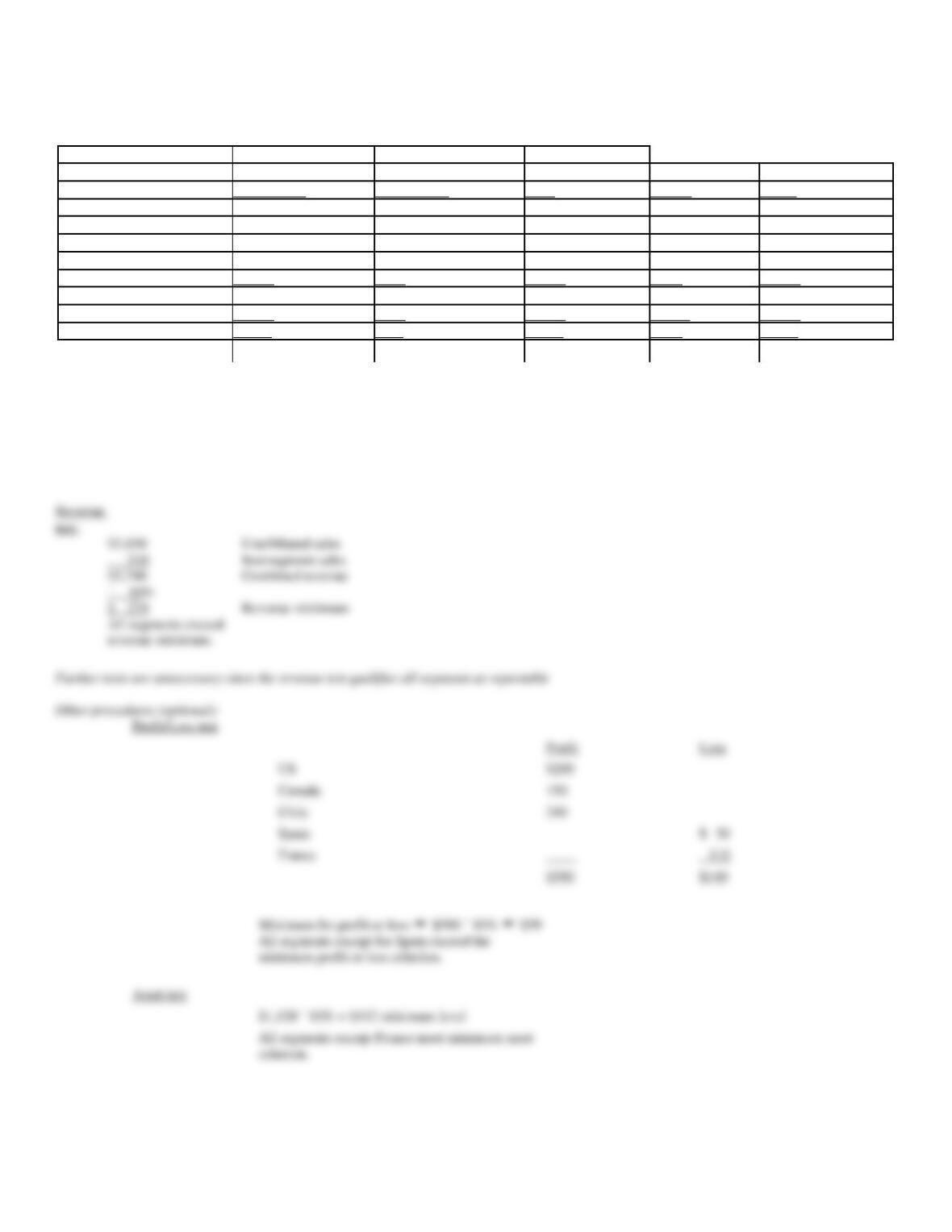

Income

(Loss)

A

B

C

Current

Year

Effective

Quarter

Type of Income

Period

to Date

Tax Rate

First

Continuing Operation

$33,000

$ 33,000

35%

First-Restated

Continuing Operation

41,000

41,000

40%

Discontinued Operation

(8,000)

(8,000)

40%

Second

Continuing Operation

40,200

73,200

35%

Second-Restated

Continuing Operation

52,200

93,200

40%

Discontinued Operation

(12,000)

(20,000)

40%

Third

Continuing Operation

62,000

155,200

40%

Discontinued Operation

(6,500)

(26,500)

40%

Fourth

Continuing Operation

71,500

226,700

40%

Discontinued Operation

1,200

(25,300)

40%

(Benefit)

D = B x C

E

F = D – E

Year

Previously

Current

Quarter

Type of Income

To Date

Reported

Period

First

Continuing Operation

$11,550

$ 0

$11,550

First-Restated

Continuing Operation

16,400

0

16,400

Discontinued Operation

(4,850)

0

(4,850)

Second

Continuing Operation

25,620

11,550

14,070

Second-Restated

Continuing Operation

37,280

16,400

20,880

Discontinued Operation

(11,660)

(4,850)

(6,810)

Discontinued Operation

(10,600)

(11,660)

1,060

Fourth

Continuing Operation

90,680

62,080

28,600

Discontinued Operation

(10,120)

(10,600)

480

51. Adam Enterprise includes seven industry segments. Operating profits (losses) relating to those segments are:

Segment

Operating

Profit (Loss)

1

$ 100,000

2

500,000

3

400,000

4

(295,000)

5

(600,000)

6

(100,000)

7

(105,000)

Required:

Based only on the above operating profit(loss) information, which of Adam’s segments would be reported separately?

Total segments reporting a profit:

1

$ 100,000

2

500,000

3

400,000

Total

$1,000,000

Total segments reporting a loss:

4

(295,000)

5

(600,000)

6

(100,000)

7

(105,000)

Total

$(1,100,000)

The greater absolute value is the total of the (loss) segments.

10% ´ 1,100,000 = 110,000

Any segment reporting a profit exceeding $110,000 or a loss exceeding ($110,000) would be reported.

Reportable segments: 2, 3, 4, 5

52. Santas Corporation is a diversified firm with operations in the United States, Canada, Chile, Spain, and

France, each of which qualifies as a geographic segment. Data with respect to those segments follows:

Revenues (in thousands)

Unaffiliated

Intersegment

Profit

Segments:

Customers

Sales

Total

(Loss)

Assets

US

$ 800

$ 0

$ 800

$200

$ 300

Canada

450

150

600

150

200

Chile

600

60

660

240

350

Spain

280

0

280

(30)

180

France

300

100

400

(110)

90

$2,430

$310

$2,740

$ 450

$1,120

Corporate-level

700

0

700

100

1,000

Total

$3,130

$310

$3,440

$ 550

$2,120

Required:

Determine which of the Santas segments would be reportable segments, and explain why.

test:

$2,430

Unaffiliated sales

310

Intersegment sales

$2,740

Combined revenue

´ 10%

$ 274

Revenue minimum

Minimum for profit or loss $590 ´ 10% $59

53. Information about the seven segments of the Kenny Corporation is presented below. Determine which of the

segments are reportable and why.

General and

Revenue from

Administrative

Total

Segment

All Sources

Cost of Sales

Expenses

Assets

1

$17,450,000

$15,200,000

$ 4,500,000

$ 55,000,000

2

25,200,000

20,000,000

4,000,000

80,000,000

3

9,150,000

7,000,000

1,500,000

28,250,000

4

780,000

300,000

100,000

4,750,000

5

11,500,000

8,900,000

4,250,000

25,500,000

6

6,800,000

3,400,000

2,000,000

12,000,000

7

2,100,000

1,000,000

900,000

10,000,000

Total

$72,980,000

$55,800,000

$17,250,000

$215,500,000

Revenue minimum:

$ 72,980,000 ´ 10%

=

$ 7,298,000

Asset minimum:

$215,500,000 ´ 10%

=

$21,550,000

Passed

Passed

Passed

Profit/Loss

Revenue

Asset

Segment

Operating Profit

Operating Loss

Test?

Test?

Test?

1

$2,250,000

Yes

Yes

Yes

2

$1,200,000

Yes

Yes

Yes

3

650,000

Yes

Yes

Yes

4

380,000

5

1,650,000

Yes

Yes

Yes

6

1,400,000

Yes

7

200,000

Total

$3,830,000

$3,900,000

´ 10%

Profit/Loss Minimum

$ 390,000

75% Test

Revenue-Unaffiliated

US

$ 800

Canada

450

Chile

600

Spain

280

France

300

$2,430

$3,130 = $2,348

portion of business

54. Egan Company, a publicly-traded company, divides its operations into several operating

segments. Determine which of the following segments are reportable and reconcile the reportable segments to

the consolidated revenues and profits.

External Revenues

Intersegment Revenues

Expenses

Assets

Travel agency

$ 621,000

$ 700,000

$ 1,597,000

$ 1,540,000

Hotels

4,543,000

644,000

2,315,000

7,787,000

Amusement parks

2,400,000

220,000

1,570,000

1,940,000

Theater

2,180,000

116,000

2,640,000

1,441,000

Pro soccer team

700,000

–

898,000

1,340,000

Corporate-level items

100,000

–

250,000

200,000

Total

$10,544,000

$1,680,000

$9,270,000

$14,248,000

Revenue to unaffiliated customers

$10,544,000

Intersegment revenues

1,680,000

Corporate-level items (a)

(100,000)

Combined revenue

$12,124,000

External Revenues

Intersegment Revenues

Travel agency

$ 621,000

$ 700,000

$ 1,597,000

$ –

$276,000

Hotels

4,543,000

644,000

2,315,000

2,872,000

–

Amusement parks

2,400,000

220,000

1,570,000

1,050,000

–

Theater

2,180,000

116,000

2,640,000

–

344,000

Pro soccer team

700,000

–

898,000

–

198,000

Total

$3,922,000

$818,000

Total Revenues

Total Revenue

Profit/Loss

Assets

Travel agency

$1,321,000

Yes

Yes

Hotels

5,187,000

Yes

Yes

Yes

Amusement parks

2,620,000

Yes

Yes

Yes

Theater

2,296,000

Yes

Yes

Pro soccer team

700,000

Consolidated revenue

$10,544,000

External revenue of reportable segments (b)

$ 9,744,000

55. Explain the difference in the independent and integral viewpoints of accounting for interim periods. Which

method best describes the accepted accounting practice for interim financial reporting?

56. The management of Trident, Inc. is trying to determine if three of the company’s nonreportable segments

should be combined into one single segment for reporting purposes. In what five ways must these segments be

similar in order to be reported as one?

57. Discuss the criteria emphasized in the “management approach” that is used to define operating segments.

58. The following lists account titles found on the books of Icell Corporation:

a.

Research and Development

b.

Inventory

c.

Annual Bonuses

d.

Unfavorable Materials Usage Variance

Required:

Discuss how each of these items is accounted for in interim financial statements.

59. For purposes of interim reporting, US-GAAP permits certain modifications to year-end inventory rules.

Required:

Comment on the acceptability of the following independent situations concerning inventory valuation for an

interim period:

a.

Management believes that since its firm does not have a perpetual inventory system, it would be too costly to take a physical inventory.

Consequently, management has suggested to the accounting department that they estimate ending inventory.

b.

Since the LIFO inventory base was liquidated in the first quarter, management has recommended that the accounting department switch to

FIFO valuation of inventory.

c.

Since the first quarter is a slow period for a manufacturing firm, management has suggested that the unfavorable volume variances from

the firm’s standard cost system be deferred until year end.

a.

Gross profit and other sound methods of estimating inventory are permitted.

b.

Changing inventory methods must be justified. Switches are rare. Liquidation of a base layer of inventory generally is not an acceptable

a.

Research and Development: This account, under normal fiscal-year policies, would normally be expensed in the current period. For

interim purposes, the account balance may be allocated among those interim periods of the current year that benefit.

recovers. This option extends only until year end. Also, there may be an allowance for LIFO replacement.

c.

Annual Bonuses: A portion of estimated annual bonuses must be allocated to each interim period of the current year. Failure to recognize

such bonuses on an interim basis would reduce the predictive value of the interim data.

interim period in which it occurs.

60. Stidham Company is a large international company with diversified operating segments. These segments

include the following:

61. In addition to disclosures about reportable segments, companies are required to provide enterprise-wide

disclosures. Describe the information included in enterprise-wide disclosures.

If information regarding product groups and/or geographic areas is not provided as part of the segmental

disclosures, such information must be provided on an enterprise-wide basis as an additional disclosure if

practical. The disclosures are required even if there is only one reportable segment. The enterprise is required

to: